General

- Economics S5 SB File Uploaded 28/01/22, 14:53

- S5: Economics TG File Uploaded 11/08/22, 23:04

Unit 10: PUBLIC FINANCE 2

Key unit competence:

Learners will be able to analyse the role of public finance in economic development.

My goals

By the end of this unit, I will be able to:

Explain the common terminologies used in taxation

Explain the principles and role of taxation.

Identify the problems encountered in collecting taxes and policies to improve tax collection in LDCs.

Explain the functions, tools and forms of fiscal policy.

Analyse the role of taxation in Rwanda.

Describe the types and the classification of taxes.

Analyse the effects of taxation on individuals and on the level of economic activity in Rwanda.

Examine the problems encountered when assessing and collecting taxes in Rwanda.

Analyse the policy measures taken to improve tax assessment and collection in Rwanda.

Compare and contrast debt financing and taxation financing.

Discuss the functions, tools and forms of fiscal policy.

Appreciate the role of taxation in government revenue and advocate for tax assessment and collection improvement.

Acknowledge the role of fiscal policy in regulating the level of economic activity.

10.1 Taxation

10.1.1 Meaning

Taxation is a process of collecting tax revenue from different sources to be used by the government in the development of the economy. Taxation can either be through direct taxation or indirect taxation depending on the base on which it is imposed.

Activity 1

There are many ways of how different people earn income. Some are business personnels who own property while others are employed and given salary. At the end of a certain period, these people are charged a certain fee by the responsible authority. Sometimes this affects their standard of living, a reason why some refuse to pay. For standardisation, the body responsible had to introduce electronic billing machines and tap to pay cards so as to avoid refusing to pay.

Explain the following:

1. What name is given to the fee mentioned above and which body is responsible for collecting it in Rwanda?

2. The process of collecting that fee is known as..........

3. Explain the role that the fee mentioned above plays to the government.

4. What are the two types of the fee mentioned above?

5. What are the effects of such a fee on the people of Rwanda?

Facts

In Rwanda the body responsible for this process of taxation is called the Rwanda Revenue Authority. The body is advanced to the extent that cases of evasion and avoidance are not to the extremes. This has been due to the introduction of electronic billing machines (EBM) that are fixed in buses that move in Kigali especially KBS and different restaurants and bars. These machines have eased the tax payment.

The Central Government through the Ministry of Finance was responsible for tax collection. The Rwanda Revenue Authority was established under the law n°15/97 on 8 November 1997 as a quasi-autonomous body with the mission of assessing, collecting, and accounting for tax, customs duties and other specified revenues.

A tax is a non quid-proquo compulsory contribution by the residents of the country levied by a public authority. Each person who is legible to pay a tax has to do so without exceptions apart from exemptions and tax holidays that are given to the investors for a specific period of time.

Common terms used in taxation

Tax base: Activities or items upon which taxes are imposed. The activities may be farming, manufacturing and processing, selling in kiosks, restaurants among others. The items on the other hand may be land, houses, cars, and people themselves among others. Basing on what is taxed, the tax may either be direct or indirect.

Taxable income: This is income which is liable to taxation by the tax authority. According to the tax system in Rwanda, there is a certain amount of income that is liable to taxation and below that, there are no taxes imposed.

Taxable capacity: This is the ability of the tax payer to pay a tax levied without affecting his or her standard of living. Sometimes individuals are left in a poor state, i.e. they are not able to sustain a good standard of living they are accustomed to. So the ability to pay a tax and at the same time remain in the same state of life is taxable capacity.

Tax evasion: This is the deliberate refusal of the tax payer to pay the tax levied on him. This can be through willful non-payment of due taxes or deliberately under stating his taxable income. Whereas tax evasion is an offence (punishable by both civil and criminal penalties), tax avoidance is not.

Reasons for tax evasion

Discontent with the services provided. Sometimes the people are not contented with the services that are offered to them after paying tax so they decide not to pay anymore.• Lack of adequate information about taxes. Some people lack information about the taxes they are supposed to pay so they end up not paying the tax.

Low income levels. Some people have got very low incomes such that if they pay a tax, they may not be able to sustain their well being so they decide to evade taxes.

Desire to retain all earnings. After making the profits, some people may desire to retain or take all the profits for their own benefit so they decide to evade the profits.

Loopholes in the tax system not to follow up the people who evade taxes. Sometimes there may be loopholes in the tax system such that they are not able to follow up those who evade the taxes so they also keep on doing the same

Opposition by the political leaders. Some oppositional leaders encourage local people not to pay tax in order to win their support.

Tax avoidance/ tax mitigation: This refers to the exploitation of the loopholes by the tax payer to pay less or no tax at all. Or it can be defined as the use of legal methods to modify an individual’s financial situation in order to lower the amount of income tax owed. This is generally accomplished by claiming the permissible deductions and credits.Tax impact: This is the first resting place of a tax. Or is a person from whom government collects money in first instance. For example, suppose government levies a tax on bottled water in Rwanda the tax will be paid to government in first instance by manufacturers of water such as Inyange, Nill and Nyirangarama industries respectively. Impact of tax is, therefore, on them. If the processing firms add tax to price and succeed in selling water to consumers, burden of tax is thus shifted on to consumers.

Tax incidence: Tax incidence is the final resting point of a tax i.e. who finally bears the burden of the tax. For example if a father in a home who takes care of the family is taxed, his family members will bear the burden of a tax when the necessities that were being bought before taxation are no longer being bought.

Effect of a tax: This refers to the repercussions or consequences of imposition of a tax on individuals and on community in general. This may be in form of poor standard of living due to failure to afford the basic needs in life.

Tax transformation: This refers to substituting the production of a taxed commodity by a non taxed commodity so as to avoid the effect of a tax for example if a person has been importing clothes in Rwanda and they are taxed, he or she can shift to electronics like computers that are tax free.

Tax rebate: This is a refund on taxes when the tax liability is less than the taxes paid. Or this refers to the reduction of tax rates to private investors to encourage investments.

Tax burden: This refers to direct impact/ effect felt by the person who pays the tax. e.g. when a person pays tax, he may remain with little disposable so tax leads to loss of money by the tax payer.

Tax shifting: This refers to transferring part or whole amount of the tax liability/burden from the original tax payer to someone else i.e. producer/ seller to consumer or raw material provider. It may either be:

(a) Forward shifting: Here the tax payer shifts the burden/ liability to the next party in the chain of distribution inform of high prices e.g. producer shifts it to the consumer by charging him or her high prices.

(b) Backward shifting: Here the tax payer shifts the liability/ burden to the previous party in the chain of distribution. E.g. producer to the raw material provider in form of paying low prices for the raw materials.The purpose of taxation

Activity 2

Describe the role of taxation in Rwanda.

Facts

The aims of taxation should not be confused with the principles or canons of taxation, although an aim may well be to arrange the tax system as much as possible in accordance with the principles of taxation. Governments impose taxes to:

1. Raise revenue

The purpose of taxation is to raise revenue for the government with legitimate revenue requirements which can only be met through some form of taxation. It is the responsibility of the people who benefit from the activities of government to pay individually a portion of those costs as taxes. The purposes of collecting taxes are to pay the debts, and provide for the common defense and general welfare of the citizens of the country. The revenue obtained can be used to finance development. It is used to promote economic growth.

2. Protect home industries especially the infant industries

Taxes are imposed on imported goods in order to protect home industries especially the infant industries. This consequently encourages the consumption of domestic goods.

3. Fight inflation

Taxes may be imposed for the reason of fighting inflation. If direct taxes are imposed on incomes, there will be less disposable income leading to a fall in the demand for goods. This consequently will lead to a fall in prices.

4. Correct a balance of payments deficit

When taxes are imposed on incomes, there is less disposable income. The demand for goods including the foreign goods falls leading to a fall in foreign exchange expenditure and hence an improvement in the balance of payments position. The imposition of taxes on commodities leads to increases in commodity prices. The demand for goods reduces leading to a fall in the foreign exchange expenditure and hence an improvement in the balance of payments position.

5. Discourage the importation of certain goods

The government can improve taxes on goods with hope of discouraging the importation of certain goods. For instance, heavy taxes could be imposed on cigarettes, alcohol etc.

6. Discourage dumping

Dumping is the selling of a commodity abroad at a cheaper price than at home. Such goods may discourage the development of local industries since they are cheaper than the locally produced commodities. To overcome this problem, taxes may be imposed on the dumped commodities.

7. To correct market failures

One of the major reasons why government intervenes in the economy is to correct or reduce various market failures. The government is justified in using taxation to:

Tax monopoly profits, both to deter monopoly and to remove the “windfall gain” accruing to a monopolist as a result of barriers to entry and inelastic supply.

Finance the collective provision of public goods and merit goods. The market might fail to provide public goods such as roads and defence, while education, health care and other merit goods might be under consumed at market prices.

Discourage the consumption of demerit goods. Demerit goods such as tobacco might be over consumed at market prices. Note that a conflict may arise between the revenue raising aim of taxation and the aim of reducing the consumption of demerit goods.

Alter the distribution of income. The government may decide that the distribution of income resulting from unregulated market forces is undesirable. Taxation and transfers can be used to modify the distribution of income resulting from market forces. A progressive tax system is used to redistribute income.

Principles of taxation/canons of taxation

Activity 3

Visit the library or internet, research and describe the following:1. Canons of taxation 2. Classification of taxes

Facts

A tax is a non quid-proquo compulsory payment from the public to the government. It imposes a burden on the tax payer by reducing his disposable income. It is precisely because of its adverse effects on tax payers that economists have debated “what constitutes a good tax”.

It was not until 1776 that qualities of a good tax were laid down. Writing in his book “Wealth of Nations”, Adam Smith laid down his four canons of taxation, which he said should be followed when imposing a tax. These canons concerned four aspects of taxation — equality or equity, certainty, convenience and economy.

1. Equality or equity principle

A good tax should impose equal sacrifice on all tax payers. The burden should be distributed according to people’s ability. Equity is said to well serve progressively in a given tax. Equity considerations are of two types;

(a) Horizontal equity. People with similar income situation should be treated equally e.g. people with same incomes charged equally.

(b) Vertical equity. People with un similar income situations should be treated differently e.g. the rich should be charged differently from the poor by being charged a higher rate.

2. Principle of certainty

The time of payment, the manner of payment, the amount to be paid, ought in all cases to be clear and plain to the contributor and to every other person. What Adam Smith had in mind was simply that the imposed tax should be simple and easy to understand by tax payers. It should be clear to him in terms of liability.

3. Principle of convenience

Adam Smith stated that every tax ought to be levied at the time or in the manner in which it is most likely to be convenient for the contributor to pay it. Individuals should be taxed when it is most convenient for them to pay. The time and the mode of payment of the tax should be convenient. For instance, farmers are taxed when they sell their crops; office workers are taxed when they receive their salaries etc.

4. Principle of economy

It should be economical to the government. The cost of collection of the tax should be small in relation to the tax revenue. It should be unwise to spend too much on collection relative to the actual amount collected. The cost of collection should not exceed 5% of the total tax revenue. With changed times and changing thinking on taxation, other principles have been added on the four originally stated by Adam Smith. These are:

5. The principle of productivity (adequacy)

It should bring in a lot of revenue. It is now widely believed that a tax must produce sufficient revenue to justify its imposition. A tax system must be capable of providing the flow of funds deemed appropriate by the government in any given period.

6. Principle of elasticity

A tax system should be income-elastic. As national income increases, the share of taxation in national income should rise more than proportionately.

7. Simplicity

It should be easy and simple to understand as well as to administer. The tax system must be set in the clearest language easily understood by the people to whom it applies.

8. Comprehensiveness

A good tax system should have multiple taxes rather than a single tax. It should not cover a single base but a wide range of tax bases.

9. Flexibility

A tax system should be flexible depending on the economic circumstances and according to the requirements of the state. The system should be able to change according to the prevailing conditions in the economy i.e. during times of boom and a depression.

10. Neutrality

A good tax system should minimise distortion of relative prices. It should reduce the inequality of incomes. Neutrality is important because a tax is to enable the government’s role of protecting the economy and providing for the general welfare. A tax that oppresses any element of the economy is thus counterproductive. Taxes that discourage consumption, investment and production are undesirable.

11. Political acceptability

It must be politically acceptable to the people. The government should be able to collect the necessary revenue without incurring the hostility of the tax payers.

12. Consistence

This means that a tax should be in line with national economic objectives especially in allocation of resources.

10.1.2 Classification of Taxes

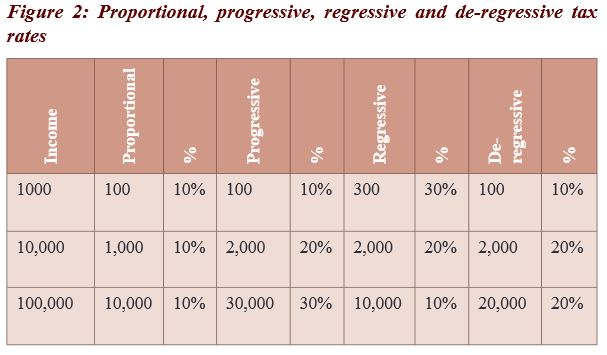

Taxes can be classified according to the behaviour of their rates or related to the tax base. They can be classified as proportional, progressive, regressive or de- regressive.

1. A proportional tax

This is a tax system where the tax rate is the same for all income levels. It has a uniform percentage for different income groups. I.e. the rich pay more than the poor in real terms but the percentage is the same e.g. All the people may pay a tax rate of 10% but still some people may pay more than others in real terms.

2. A progressive tax

This is a type of tax system where the rate of tax increases with increase in income level. The higher income group pays a higher amount of a tax both in real terms and percentage terms than the low income earners. The rate of increase of the tax is more than the rate of increase in the income. It has the following effects:

• Redistributes tax in an economy where the rich are taxed highly than the poor.

• Raises more income revenue to the government.

• Discourages work effort by the high income earners.

• Reduce the level of savings and investments.

• Encourages tax avoidance by the rich in the economy.

• Discourages foreign investors from investing in the country.

3. A regressive tax

This is a tax system where the rate of tax decreases with increase in income. The poor are taxed more than the rich in relative means as those who get more income suffer less. The rate of increase of this tax is less than the rate of increase in the income. Those who get more income suffer less from this tax. It has the following effects:

• Leads to exploitation of the poor.

• Widens the gap between the poor and the rich.

• Lowers standard of living of the poor.

• Encourages tax evasion by the poor.

• Leads to social unrest and tension in the society.

• Encourages hard work by the poor and rich.

4. De-regressive tax

This is a tax system which has progressive elements at lower levels of income but the amount remains uniform at higher levels of income.

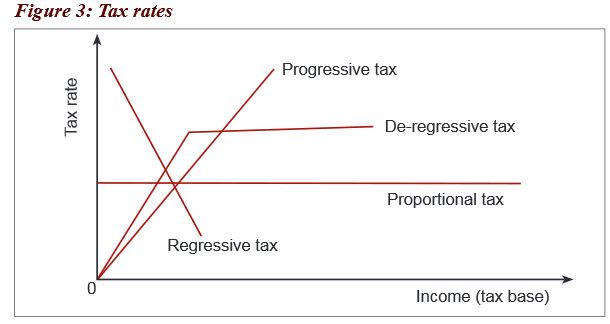

These types of taxes can be shown below:

From the figure above, it is seen that;

• Proportional tax, the tax rates are the same for different income groups,

• Progressive tax, the rates increase with increase in incomes

• Regressive tax, the tax rate reduce with increase in income

• De-regressive tax, the tax rates increase first then they become constant at some state. i.e. it has progressive nature and then proportional rate at a later stage.

The rates can further be illustrated as seen below.

From Figure 3 above, it is seen that, Proportional tax rates are the same for different income groups, Progressive tax rates increase with increase in incomes, Regressive tax rates reduce with increase in income and De-regressive tax rates increase first then they become constant at some state.

Types of taxes

Activity 4

Mr Nkurunziza works in king Faisal hospital as a doctor. He earns a gross salary of FRW100, 000 at the end of the month. After removing taxes, his net income is worth Frw60, 000 which is not enough to cater for his basic needs and worse still, he is discouraged to work and sometimes stays home to carry out farming to supplement his little income. Respond to the following questions:

1. What type of tax is charged on Mr Nkurunziza’s income?

2. What are the effects of such a tax on Mr Nkurunziza’s family?

Facts

Direct Taxes

A direct tax is a tax levied on the individual’s or company’s income or wealth. The total burden of paying is suffered by the tax payer and is inescapable. It is a tax paid by the person on whom it is imposed. The government expects that the tax burden rests permanently on the person who pays the tax. The tax paid normally varies with the status of the tax payer. Examples include;

(a) Income tax: This is a tax levied on individuals who receive income over and above a certain amount (taxable income) in a given period of time.

(b) Corporate tax: Levied on company profits or any other trading organisations.

(c) Estate duty (death tax): Tax paid on the assessed wealth or estate of a person at the time of his death.

(d) Gift tax: Payable on the assessed wealth of a person at a time of transfer to another person.

(e) Capital gains tax: Imposed on increase in the value of an asset when imposed at a higher price than the acquired value.

(f) Poll tax: Imposed on a fixed rate on every individual,household irrespective of one’s income.

(g) Graduated tax: Levied on one’s income mostly for the employed wage or salary earners.

Property tax: Levied on properties like land, houses among others.

(i) Inheritance tax: Levied on inheritors of property who may be one or many. The greater the value of the property inherited, the greater the tax.

Merits of direct taxes

• Equitable: The burden is equitably distributed as they are progressive in nature. It affects the rich more than the poor ones. Horizontal and vertical equity are satisfied. Certain direct taxes are based on the canon of certainty. Time of payment and amount are known.

• Reduce income inequalities: It tends to redistribute income within the economy since it is in most cases progressive.

• Fight inflation: A direct tax can reduce inflation since disposable income reduces. The fall in disposable income leads to a fall in demand.

• Simplicity: They are simple and easy to understand.

• Economical: The cost of collection of direct taxes is low. This is especially true with the income tax. The salaries of the individuals working in the government are automatically reduced by the amount of the tax.

• Flexibility: The government can increase or decrease the rates of direct taxes according to the requirements of the economy.

Demerits of direct taxes

• Inconvenience: In most cases, direct taxes are payable in advance and in lumpsum except in the case of salaried persons. This represents an inconvenience to the tax payers.

• Burden to tax-payers: Direct taxes are a burden to tax-payers because they have to be paid directly out of their incomes.

• Evasion: They may not be paid and this results into loss of revenue to the government.

• Discourage saving and investment: When people know that with the increase in the income and wealth, they will have to pay a large portion in the form of taxes, they are reluctant to save and invest.

• Employment opportunities will be limited: On the other hand, since direct taxes reduce disposable incomes, there will be less demand. The fall in the demand acts as a disincentive to producers and hence less investment.

• Discriminatory tax: Direct taxes are not imposed on all income groups. This is normally true with the low income group which is exempted from paying the tax.

• Wage- Push inflation: When direct taxes are imposed, disposable income decreases. Workers may then demand higher wages resulting into wage-push inflation.

• Direct taxes affect the workers’ effort: People’s willingness to work may be affected by direct taxes. It is hard to determine one’s taxable capacity. Individuals have different sources of income which may not be known to the taxation authorities.

• Direct taxes discourage production: This is usually the case with corporation taxes which are charged according to the profits made.

Indirect tax

Activity 5

Referring to activity 4, Mr Nkurunziza decided to quit working at the hospital and got engaged in farming, concentrating on growing rice and matooke. He harvested a lot that he sold to different markets in the country and further continued to surrounding countries like Burundi and Congo. He realised still that there was always a tax he had to pay when processing his goods and when exporting among others.

Respond to the following questions:

1. What type of tax is charged on Mr Nkurunziza’s activities?

2. What are the effects of such a tax on Mr Nkurunziza’s activities ?

Facts

Indirect tax is a tax levied on the activities of an individual and companies. They are levied initially on the importer, producer or whole seller but ultimately paid by the consumer since they are included in the price of the final products sold at the market. This depends on the price elasticity of demand. Examples include:

(a) Value Added Tax: This is a tax charged on the activities at every stage of production process.

(b) Customs duty: Levied on goods being moved across the boundaries of a country. It’s composed of import and export duty

(c) Excise duty: Taxes imposed on locally manufactured goods whether they are for home consumption or export.

(d) Sumptuary tax: Levied on commodities to discourage their consumption by making their prices high.

(e) Octori tax: Charged on goods passing through the territories of a country.

(f) Specific tax: Tax levied per unit of output.

(g) Advalerem tax: This is a tax charged according to the value of the commodity. The more valuable the commodity, the more tax that is charged.

(i) Consumption tax: Tax paid by the consumer when buying the goods for consumption. This tax is paid unknowingly by the consumer.

Merits of indirect taxes

• Avoidance of high direct taxes: Indirect taxes save the government the problem of imposing heavy direct taxes. The government for instance, can impose a tax of FRW.15 million on imported goods but cannot impose it on one’s income without resulting in serious disincentives on effort and initiative.

• Indirect taxes are convenient: They are less inconvenient and less burdensome. They are paid only when a commodity or a service is bought. Since these taxes are included in the prices of commodities, buyers do not feel the burden of these taxes.

• Less Evasion: Indirect taxes can hardly be evaded since they are included in the prices of commodities. They can be evaded only when consumers do not buy the taxed commodities.

• Less harmful to effort and initiative: Incentives and enterprise are not harmed, as in the case of direct taxes. This is because indirect taxes are not linked to earnings.

• Wide coverage: Indirect taxes cover a variety of commodities and services. The government is sure of sufficient tax revenue from all income groups. Indirect taxes are therefore very productive.

• Flexibility: Indirect taxes can be adjusted either downwards or upwards depending on the country’s prevailing economic situation.

• Check the consumption of harmful goods: Indirect taxes can be used to discourage the production of goods that are injurious to the welfare of society. Indirect taxes can check the consumption of harmful goods when the government levies heavy taxes on such commodities.

• Economical: Indirect taxes are easy to collect. They involve little cost of collection.• Indirect taxes do not discourage work’s efforts: Workers do not offer less hours of work instead they put in more work effort in order to be able to buy those commodities that cannot be avoided.

• Powerful tool of economic policy protection of home industries: The government can levy heavy import taxes on the foreign goods if it wants to protect and develop the domestic industry. In this way, output and employment opportunities will increase. Indirect taxes can be imposed to protect against dumping. Dumping can discourage the development of home industries.

Demerits of indirect taxes

• Indirect taxes are regressive in nature: The rich and the poor have to pay the same amount of tax on essential goods — say on soap, kerosene. The burden of tax is heavier on the low income group. Indirect taxes therefore do not satisfy the canon of equity.

• Unreliable revenue: Indirect taxes can be unreliable as a source of government revenue. It is not possible to accurately estimate the effect of indirect taxes on the demand for products.

• Inflation: Indirect taxes lead to higher prices, higher costs of production, higher cost of living and therefore higher wages. Note the problems of inflation.

• Adverse effects on production and employment: Indirect taxes may at times adversely affect the production of certain commodities.

• Indirect taxes tend to raise the prices of commodities, which lead to the fall in demand. The fall in the demand is a disincentive to producers. Consequently, production and employment opportunities all decline.

• Diversion of resources: Indirect taxes lead to the diversion of resources from taxed commodities to non-taxed commodities which may lead to the misallocation of resources.

General Effects of taxation

Positive effects

- Redistributes revenue in an economy where the rich are taxed highly than the poor hence reducing income inequality.

- Raises more income revenue to the government and this plays a big role in the economy.

- Encourages hard work. Sometimes the poor are encouraged to work harder in order to sustain their way of life.

- Reduces consumption of harmful commodities in excessive amounts since it increases their price and hence reduction in the consumption.

- Sometimes reduces imported inflation since it raises prices of imports hence reducing their demand. However it should be known that demand for imports in LDCs is inelastic even if the prices increase, demand always remains the same.

Negative effects

- Discourages work effort by the high income earners. The progressive tax will affect the rich since they will pay depending on their income

- Reduces the level of savings and investments among the people since their income is taken by the tax authorities.

- Discourages foreign investors from investing in the country. The corporate tax is charged at the profit of the business where by the more profits you earn, the more tax you pay.

- Leads to exploitation of the poor. The poor are exploited especially in the regressive tax system where they pay a large percentage rate the rich.

- Widens the gap between the poor and the rich. Regressive taxes always make the rich become richer than the poor hence leading to a big gap between the rich and the poor.

- Lowers standard of living of the poor since they cannot afford to buy the basics in life.

- Leads to social unrest and tension in the society since people don’t have money to pay in form of a tax.

- High level of taxation may lead to social evils like smuggling in order to save the little income they earn.

Structure of taxation in Rwanda

Structure of taxation refers to the composition, ways taxes are levied and its effects on the citizens. The structure can be seen below

1. Composition: Most of the tax revenue is got from indirect taxes like customs, sales among others.

2. Tax administration: Revenue is normally collected by Rwanda Revenue Authority on behalf of the central government and the local government authorities.

3. Objective of taxation: Major objective is to raise revenue for recurrent and development expenditure.

4. Tax base: Tax base is narrow because system is not comprehensive as not all wealth, income and expenditure is taxed.

5. Taxable capacity: This is low because of a large subsistence sector and high levels of poverty.

6. Taxation impact: Most taxes especially indirect taxes are regressive and they tend to affect the poor more than the rich.

7. Taxation effort: Direct taxes which are progressive tend to discourage the work effort of the people hence there is reduction in productivity.

8. Tax avoidance and evasion: Rate of evasion is high especially through defaulting. Tax avoidance is low because most indirect taxes are levied on essential goods. However this has been solved by introduction of the electronic billing machines.

9. Tax GDP ratio: The proportion is not very much because of low taxable capacity and low tax base however the trend is increasing.

Problems facing taxation system in Rwanda

Activity 6

The government of Rwanda in its attempt to ensure further development in the country is to use borrowing or continue to tax the citizens so as to raise the funds. All the two methods have different outcomes, importance and problems.Basing on the photo (a) in figure 4 below, the revenue collected by Rwanda Revenue Authority in the first half of the financial year, was more than what was expected. One wonders why this hasn’t been the case for the previous years.Basing on the photos in figure 4 below, respond to the followingquestions:

1. What problems do you think affected RRA previously that led to low revenues?

2. What policies have been adopted by RRA such that the revenues have increased as shown in the New times?

3. In what ways does the government of Rwanda use its tax revenue collected?

4. Explain why Rwanda should resort to borrowing other than taxation in order to raise revenue for development.

Facts

• Difficulty in determining the taxable income because the government lacks records of all the people’s incomes and jobs. This is because some people do a lot of activities some of which may not be declared to the government.

• High rates of tax evasion and avoidance: There has been lots of people refusing to pay taxes and others under declaring their incomes to the tax authority. This has however been reduced by the introduction of electronic billing machines which have been put in public buses like KBS, Royal buses among others. These machines automatically cut off the revenue when the user uses it.

• Large subsistence sector reduces tax base: Most of the people grow food for home consumption. They therefore do not have money to pay taxes. This has led to a narrow tax base.

• Scattered tax payers and this increases the cost of collecting the tax revenue. Since people do not carry out business in the same area, it may involve the tax collector to move from one place to another hence increasing the cost of collecting tax.

• Hostility of the tax payers especially in case of unfair direct taxes. Some tax payers are very hostile because of some taxes that may seem unfair to them. So they end up being hostile to the tax collectors.

• A high rate of smuggling reduces the tax base and revenue to the government sometimes the goods are smuggled into the country without paying taxes. This reduces the tax collected.

• There is a low level of income per capita because of poverty hence low revenue. By 2014 the per capita income of Rwanda was 695.7. This implies that the people were earning little income therefore their ability to pay was very low.

• High rates of corruption and embezzlement and this reduces the revenues meant to be collected by the government.

• Many illegal activities which yield income but are not taxed e.g. prostitution. This also leads to low tax base to the government hence little revenue.

Policies to improve tax collection in LDCs

• Improvement in administrative machinery, which will help to minimise the rates of tax evasion and avoidance hence increase tax revenue.

• Encourage income generating activities especially in rural areas to provide opportunities for employment so as to expand the tax base. This will increase the revenue to the government.• Providing adequate facilities to ease the process of tax collection e.g. transport, computers. This will reduce problems of computerised taxation and also access areas that are inaccessible.

• Tax diversity. New taxes have to be introduced. These will help to widen the tax base and the government will be able to receive more revenue.

• Improving economic activities like in the manufacturing sector, monetary expansion to increase investments and employment opportunities. This will also increase the revenue.

• Ensuring political stability so as to access areas from which taxes can come. The tax collectors will be able to cover those areas without any fear hence increasing tax revenue.

• Adopting a tax payer friendly system where the tax payers can freely pay at their time of convenience without pressure from the tax authority.

• Reduction on the grace period like tax holidays and exemptions given to investors. This will as well increase the tax base of the country.

• Reviewing the existing tax structure, policies and programs so that they are in line with the required targets.

Debt financing versus taxation financing

Debt financing refers to the government act of fulfilling its expenditure requirements through public borrowing either from internal or external sources or both. Or it is a practice in which a government spends more money than it receives as revenue, the difference being made up by borrowing or minting new funds.

Taxation financing refers to the government act of meeting its expenditure requirements through raising revenue from taxation. Taxation can either be direct or indirect which can either be levied on people’s income or goods and services.

Advantages of debt financing over taxation financing

Activity 7

Explain the arguments for and against debt financing over taxation financing on an economy.

Facts

• Borrowing is a more reliable source of income than taxation which has high rates of tax avoidance and evasion.

• More revenue is realised through borrowing unlike taxation whose revenue comes in bits.

• Borrowing encourages savings because the public is able to buy government securities which is a means of savings while taxation which reduces peoples income and savings.

• External borrowing increases aggregate demand because it may increase money in circulation unlike taxation which reduces people’s disposable income .

• Borrowing is cheaper in terms of costs administration and time unlike taxation with its high administration costs.

• Borrowing strengthens ties between the lending and borrowing country than taxation which causes unrest in the country once high taxes are levied.

• Internal borrowing can be used to fight inflation than taxing the people.

• Borrowing can be used to raise money in times of emergence which is quite hard with taxation.

• Individuals and institutions are willing to lend because of the interest involved than paying tax.

Disadvantages of debt financing/ advantages of taxation

• Borrowing increases dependence on other countries and international bodies unlike taxation which enhances self –reliance.

• Borrowing is associated with debt servicing which encourages capital flight unlike taxation where funds remain in the economy.

• Borrowing increases the debt burden which may lead to BOP disequilibrium.

• Borrowing involves strings attached such as use of expatriate manpower thus capital flight unlike taxes which is non-quid pro quo.

• Repaying the loans has external and internal burden to the citizens of the borrowing country which may not be the case with taxation.

• Borrowing may be inflationary in the long-run, if it is a dead weight debt yet taxes on incomes reduce or may control inflation.

• Borrowing may lead to wastage if the borrowed funds are not properly utilised i.e funds may be mistaken to be free money which is not the case with taxation.

• The burden of borrowing may be shifted to the future generation who may not have borrowed from the borrowed funds which isn’t possible with taxation.

10.2 Fiscal policy

Activity 8

Visit the school library or the internet and research on the following:

1. Meaning of fiscal policy.

2. Tools and functions of fiscal policy.

Facts

Fiscal policy refers to the deliberate use of taxation, borrowing and government expenditure to regulate the level of economic activities or stabilise development. In more developed countries, the role of the fiscal policy is to stabilise the economy, while in less developed countries, the fiscal policy is designed as an instrument of economic development. The policy instruments of fiscal policy include the following;

(a) Taxation. This is the most effective instrument of the fiscal policy. Taxes can either be direct or indirect.

(b) Public borrowing. This is either internal or external and can be either national borrowing or public borrowing.

(c) Government expenditure. This involves ways of how the government uses the revenue got. It can either be through re-current expenditure (expenditure for day to day activities) or capital expenditure or development expenditure (expenditure on development like infrastructure).

10.2.1 Forms of fiscal policy

There are two basic types of fiscal policy.

1. Expansionary fiscal policy: This type of fiscal policy is aimed at stimulating the economy and creating more growth. The government either spends more or cuts taxes, or both if it can. The idea is to put more money into consumers’ hands, so they spend more. This jumpstarts demand, which keeps businesses running and hopefully adds jobs.

2.Contractionary fiscal policy: This type mainly is used to control inflation and hence to slow economic growth. The tools of contractionary fiscal policy are used in reverse: taxes are increased, and spending is cut leading to reduction in demand.

10.2.2 Objectives of fiscal policy

The fiscal policy aims at achieving the following;

1.To increase the rate of economic growth: Fiscal policy promotes and accelerates the rate of investment both in private and public sectors. This can be done by reducing consumption while encouraging savings which can be used to finance investment. Public expenditure on economic and social overheads provides larger employment opportunities, raises incomes and increases the productive capacity of the economy.

2. To increase employment opportunities: Fiscal policy can be used to create employment. The Government can increase its expenditure on social and economic overheads. When the Government starts public works like the construction of roads, power projects and the like, it creates employment opportunities.

3.To reduce inflation: The fiscal policy can be used to overcome inflation. Taxes can be used on people’s incomes so as to reduce their demand. The fall in demand results into a fall in prices. However, the aim of the fiscal policy is not only to overcome inflation but also maintain stability in the general price level.

4. To reduce balance of payment deficit: A balance of payments deficit can be overcome through taxation. Direct taxes reduce the disposable income leading to a fall in demand for all goods including foreign goods. This consequently improves the balance of payments position since there is a fall in demand for foreign exchange.

5. To reduce income inequality: The fiscal policy can redistribute income from the rich to the poor. A progressive tax can be used to redistribute income. The amount of tax revenue obtained from the rich can be invested in productive projects which can help to increase the income of the poor.

Unit assessment

1. Analyse why Rwanda Revenue Authority has to levy taxes.

2. Examine the reasons as to why some people in Rwanda refuse to pay taxes.

3. Why does Rwanda rely more on borrowing than taxation to finance her development budget?

4. Advise the government of Rwanda on how to increase the tax base and capacity in the country.

10.3 Glossary

Advalerem tax: This is a tax charged according to the value of the commodity.

Backward shifting: This is where the tax payer shifts the liability/ burden to the previous party in the chain of distribution. E.g. producer to the raw material provider in form of paying low prices.

Customs duty: This is a tax levied on goods being moved across the boundaries of a country. It is composed of import and export duty.

Consumption tax: This is a tax paid by the consumer when buying the goods for consumption.

Debt financing: The government act of fulfilling its expenditure requirements through public borrowing either from internal or external sources or both.

Direct tax: This is levied on the income or property of the consumer the burden of which cannot be transferred to another person.

De-regressive tax: This is where a tax rate has progressive elements at lower levels of income but the amount remains uniform at higher levels of income.

Excise duty: This is a tax imposed on locally manufactured goods whether they are for home consumption or export.

Forward shifting: This is where the tax payer shifts the burden/ liability to the next party in the chain of distribution inform of high prices e.g. producer to the consumer.

Fees: Payment made by an individual for personal services rendered to them by the government.

Fines: These are penalties imposed on citizens who break laws.

Horizontal equity: This states thatpeople with similar situation should be treated equally e.g. people with same incomes charged equally.

Indirect taxes: These are taxes imposed on goods and services.

Licenses: This is a payment made to the government to secure permission to carry out any gainful activity.

Octori tax: is tax charged on goods passing through the territories of a country.

Proportional tax: This is where the tax rate is the same for all income levels. It has a uniform percentage for different income groups.

Privatisation: This is the transfer of ownership from the public sector to the private sector.

Progressive tax: This is where the rate of tax increases with increase in income level. The higher income group pays a higher amount of a tax both in real terms and percentage terms than the low income earners.

Rent: This is the provision of government assets to private individuals for commercial purposes.

Regressive tax: This is where the rate of tax decreases with increase in income. The poor are taxed more than the rich in relative means as those who get more income suffer less.

Specific tax: This is a tax levied per unit of output.

Sumptuary tax: This is a tax levied on commodities to discourage their consumption by making their prices high.

Sales tax: This is a tax levied on sales and paid by the seller

Structure of taxation: This refers to the composition, ways taxes are levied and its effects on the citizens.

Taxation financing: This refers to the government act of meeting its expenditure requirements through raising revenue from taxation.

Taxable capacity: This is the ability of the tax payer to pay a tax levied without affecting his or her standard of living.

Tax transformation: This refers to substituting the production of a taxed commodity by anon taxed commodity so as to avoid the effect of a tax.

Tax rebate: This refers to the reduction of tax rates to private investors to encourage investments.

Tax burden: This refers to direct impact/ effect felt by the person who pays the tax.e.g. loss of money.

Tax: This is a non quid-pro-quo compulsory payment by an individual to a tax authority.

Tax base: This refers to all activities or items upon which taxes are imposed.

Taxation: This is a process of collecting tax revenue from different sources to be used by the government in the development of the economy.

Taxable income: This is income which is liable to taxation by the tax authority.

Tax evasion: This is the deliberate refusal of the tax payer to pay the tax levied on him.

Tax avoidance: This refers to the exploitation of the loopholes by tax payer to pay less or no tax at all.

Tax impact: This refers to the first resting place of a tax.

Tax incidence: This is the final resting point of a tax.

Tax shifting: This refers to transferring part or whole amount of the tax liability/burden from the original tax payer to someone else.

Value Added Tax: This is a tax charged on the value of activities at every stage of production process.

Vertical equity: This states that people with un similar situations treated differently e.g. the rich should be charged differently from the poor.

Unit summary

• Meaning and common terms used in taxation• Purpose of taxation• Principles of a good tax system• Classification of taxes• Progressive• Proportional• Regressive• De-regressive• Types of taxes• Direct taxes• Indirect taxes• Structure of taxation in Rwanda• Problems and policies to improve taxation• Debt taxation and taxation financing• Fiscal policy• Forms• Functions