General

- Economics S5 SB File Uploaded 28/01/22, 14:53

- S5: Economics TG File Uploaded 11/08/22, 23:04

Unit 1: MARKET STRUCTURES

5. Identify other businesses in Rwanda that may fall under the same market structure.Key unit competence: Learners will be able to analyse the operation of

firms under different market structures.

My goals

By the end of this unit, I will be able to:- Identify the different categories of market structures and their characteristics.

- Explain the process of profit maximisation of firms under different markets in both the short run and long run.

- Explain the advantages and disadvantages of firms under different market structures.

- Explain why firms continue to produce even when they are making losses.

- Explain the conditions for successful price discrimination under monopoly conditions and the different forms.

- Identify the different forms of product differentiation under monopolistic competition.

- Explain how prices are determined under oligopoly firms.

- Describe the conditions under which different market structures operate.

- Analyse the operation of firms under different markets in both the short run and long run.

- Illustrate the process of profit maximisation of firms under different markets in both the short run and long run.

- Illustrate the break even and shut down point under perfect competition.

- Analyse how firms under oligopoly win markets without price wars.

- Illustrate the kinked demand curve under an oligopoly.

- Make a comparison between different market structures and appreciate the conditions under which they operate.

1.1 Introduction to market structures

1.1.1 Meaning

A market is any arrangement that brings buyers and sellers into close contact to transact business with an aim of making profits. It may be a physical place, communication through telephone, fax and mail. Different markets have different characteristics, participants and conditions. Thus, markets differ in number of sellers and buyers, nature of the product, entry conditions, degree of knowledge, cost conditions, etc. The conditions that prevail in the market which determine how the market players operate are what we call the market structures. Therefore, a market structure is a range of unique features or characteristics that describe a given market.Market structure is categorised into two:1. Perfect markets: These include perfect competition.2. Imperfect markets: These include monopoly, oligopoly, monopolistic competition, etc.Activity 1

Basing on figure 1 on page 5:1. Distinguish between a market and a market structure.2. Identify the features found in the two markets a and b.3. Describe the differences between the two markets.

1.2 Perfect markets

Activity 2

Basing on figure 2 below:1. Identify the nature of commodities.2. How many sellers can you recognise in the picture?3. What type of market structure is seen in the figure below and why

Facts

Under perfect markets, there is basically one market situation that is known as perfect competition.1.2.1 Perfect competition

Perfect competition is a market structure where there are several buyers and sellers dealing in a homogeneouscommodity and possessing perfect knowledge of market conditions at that particular time.Conditions/features for perfect competition

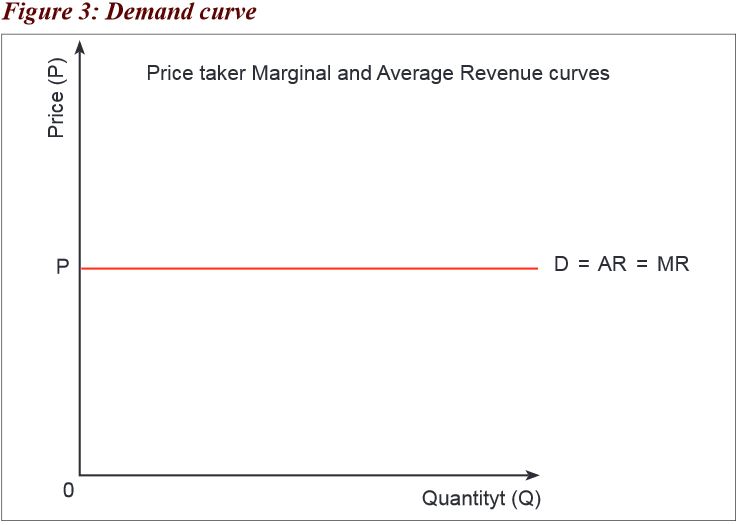

Perfect competition is said to exist where there are the following conditions or features:• There are many buyers and sellers in the market. No seller/buyer controls the market conditions independently.Each participant in the market cannot independently influence the price of the commodity.Therefore, firms underperfect competition are price takers, i.e. they take the price that is determined by automatic forces of demand and supply.• All the commodities sold are similar or homogeneous. All firms in the industry produce the same product such that there isno way a consumer can prefer one producer’s product to the other.• There is no government intervention in form of fixing prices. All participants in the market abide by the price that is set byforces of demand and supply. Such a price rules all over the industry.• The demand curve of a perfect competitor is perfectly elastic. This indicates a constant price for the whole industry.At this point, marginal revenue is equal to average revenue which is equal to the price. • The firms under perfect competition do not incur transport costs. Under perfect competition, it is assumed that the rawmaterials, the firm, the consumers, are all found in the same place or locality• There is perfect mobility of factors of production from one production unit to another. Factors of production can easilymove from places of low payment to better paying places. It is further assumed that labour is easily acquired.• Buyers and sellers have perfect knowledge about the market conditions. It is assumed that the price, quality, quantity andthe location of the product in question are known by all the participants in the market.• There is no persuasive advertising. This is because the commodities are the same and the consumers have perfectknowledge about the market conditions. There may be some informative advertisements to make the consumers awareof the products.• There is free entry and exit in the industry. Firms can freely join the industry if they anticipate making profits and can alsofreely leave the industry if they make losses.• The major aim of firms is profit maximisation. This is attained at a point where the marginal cost is equal to the marginalrevenue (MC = MR).

• The firms under perfect competition do not incur transport costs. Under perfect competition, it is assumed that the rawmaterials, the firm, the consumers, are all found in the same place or locality• There is perfect mobility of factors of production from one production unit to another. Factors of production can easilymove from places of low payment to better paying places. It is further assumed that labour is easily acquired.• Buyers and sellers have perfect knowledge about the market conditions. It is assumed that the price, quality, quantity andthe location of the product in question are known by all the participants in the market.• There is no persuasive advertising. This is because the commodities are the same and the consumers have perfectknowledge about the market conditions. There may be some informative advertisements to make the consumers awareof the products.• There is free entry and exit in the industry. Firms can freely join the industry if they anticipate making profits and can alsofreely leave the industry if they make losses.• The major aim of firms is profit maximisation. This is attained at a point where the marginal cost is equal to the marginalrevenue (MC = MR).Examples of perfect competition

In the real world, its hard to find examples of industries which fit all the criteria of ‘perfect knowledge’ and‘perfect information’. However some industries are close and these may include:1. Foreign exchange markets: Here currency is all homogeneous and traders will have access to many buyers and sellersand there will be good information about relative prices.2. Agricultural markets: In some cases, there are several farmers selling identical products to the market e.g. tomatoes,pineapples, Irish potatoes, bananas, etc. and many buyers. At the market, it is to compare prices.3. Internet related industries: It is easy to compare prices quickly and efficiently and entry barriers are lower.Note : At times, a distinction is made between pure competition and perfect competition.Pure competition is characterised by: Many firms and buyers, product homogeneity, free entry and exit, profit-maximisation,no government interference, no transport costs, no persuasive advertising.Perfect competition, on the other hand, requires the fulfillment of two additional conditions: Perfect mobility of factors of production and perfect knowledge of market conditions.Therefore, perfect competition is a wider term than pure competition. In other words, pure competition is a subset of perfect competition.The demand curve for a firm under perfect competition

Activity 3

Make research in the nearby market and find out the following.1. What is the price of tomatoes? (ask at least three sellers).2. Why do they sell at that price?Facts

Each firm in a perfectly competitive market faces a perfectly elastic demandcurve because variations in the firm’s outputhave no noticeable effect on price. The perfectly elastic demand curve does not indicate that the firm could actually sell an infinite amount at the prevailing price. It only indicatesthat the variations in production will leave the price unchanged because their effect on total industry output will be negligible. The firm’s output variation has only a tiny percentage effect on industry output. The price is determined by the industry. As shown in Figure 3 above, the demand curve is equal to the average revenue curve and equal to marginal revenuecurve. (D=AR=MR)

As shown in Figure 3 above, the demand curve is equal to the average revenue curve and equal to marginal revenuecurve. (D=AR=MR)Cost curves under perfect competition

Activity 4

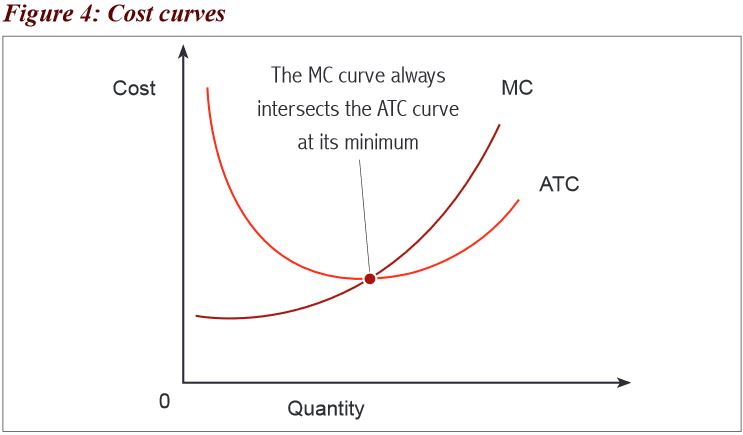

Basing on the knowledge of the theory of costs:1. Distinguish between marginal cost and average cost.2. Describe the nature and relationship between the two above.Both the Marginal Cost (MC) and Average Cost (AC) are U-shaped under market structures because of the law ofdiminishing returns and economies and diseconomies, respectively. The MC and AC are both U-shaped but the MC curve cuts the AC curve from its lowest point (i.e. optimum point of a firm).

The MC and AC are both U-shaped but the MC curve cuts the AC curve from its lowest point (i.e. optimum point of a firm).Relationship between average revenue (AR) and marginal revenue (MR), price and demand of a firm under perfect competition

The AR curve is the same as MR curve under perfect competition. This is because selling an extra unit of output adds the same amount to the total revenue since the price is constant, i.e. AR=P=D=MR as illustrated below. As shown in Figure 5 on page 10, the price is equal to demand, marginal revenue and average revenue (P=D=AR=MR).

As shown in Figure 5 on page 10, the price is equal to demand, marginal revenue and average revenue (P=D=AR=MR).Short-run equilibrium position of a firm under perfect competition

Activity 5

Using the photos in figure 6 below:1. Describe the situations in the two photos.2. Define the term equilibrium.3. When do you think the firm is in equilibrium?

Facts

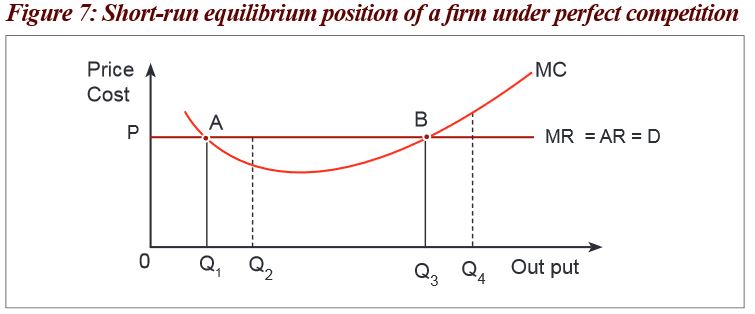

Equilibrium can be defined as a state of balance when variables under consideration have no tendencies to change.The firm is in equilibrium at a point where marginal cost (MC) is equal to the marginal revenue (MR), and it is when profits are maximised. The firm aims at producing the level of output which maximises a difference between TR and TC. This is when it pays the firm to keep output unchanged. The slope of MC must be greater than the slope of MR at the equilibrium output.This is when the MC curve cuts the MR curve from below. For the competitive firm which is maximising profit,we have P = AR = MR = MC. This can be illustrated in the figure below As shown in Figure 7, at point A (output 0Q1), the firm is in equilibrium, i.e. MC = MR. However, this is not sufficient. It,therefore, requires the firm to increase output to a higher output e.g. 0Q3 in order to fetch more revenue compared to thecost incurred in its production.At point B, the firm fulfils the sufficient condition of equilibrium by producing a high output 0Q3 where MC= MR and MCis rising. At equilibrium, the firm may either make abnormal profits or incur losses (sub-normal profits) depending on thelevel of averagetotal cost (ATC).

As shown in Figure 7, at point A (output 0Q1), the firm is in equilibrium, i.e. MC = MR. However, this is not sufficient. It,therefore, requires the firm to increase output to a higher output e.g. 0Q3 in order to fetch more revenue compared to thecost incurred in its production.At point B, the firm fulfils the sufficient condition of equilibrium by producing a high output 0Q3 where MC= MR and MCis rising. At equilibrium, the firm may either make abnormal profits or incur losses (sub-normal profits) depending on thelevel of averagetotal cost (ATC).Price and output determining of a firm under perfect competition in the short-run

(Equilibrium of the firm in short-run)

Activity 6

Umutesi and Murenzi started separate businesses of selling tomatoes on 1st of January 2016. They each started with 5000 FRW. After two months of activity, Umutesi received 7000 FRW while Murenzi received 4000 FRW.From the case study above:1. Identify the costs and revenues of each seller.2. Calculate the difference between Umutesi and Murenzi’s earnings.3. Describe the nature of their earnings.4. Illustrate the above information on graphs.Facts

In the short-run, the firm can either make abnormal profits or losses.Losses are made because the firm may be new and incurring higher costs of production.Abnormal profits in the short-run

The firm will be in equilibrium at a point where marginal cost (MC) = marginal revenue (MR) and it will come under the following conditions:• The average revenue (AR) must be greater than the average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be below the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. As shown in Figure 8 on page 13, the firm produces output 0Q at total cost

As shown in Figure 8 on page 13, the firm produces output 0Q at total cost and sells it at price 0P getting total revenue

and sells it at price 0P getting total revenue , hence making abnormal profits CPAB.

, hence making abnormal profits CPAB.

Loss making firm under perfect competition

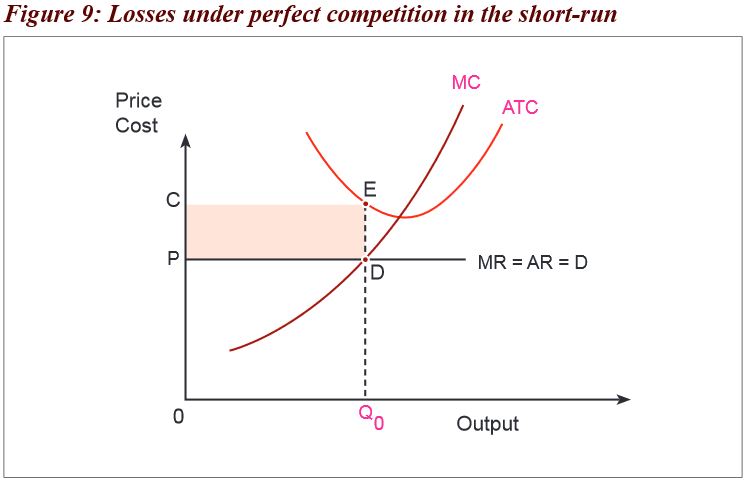

It comes under the following conditions:• The average revenue (AR) must be less than average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be above the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. As shown in Figure 9 above, the firm produces output 0Q at total cost

As shown in Figure 9 above, the firm produces output 0Q at total cost and sells it at price 0P, getting total revenue

and sells it at price 0P, getting total revenue  ,hence making losses PCED because the AC is greater than the AR.

,hence making losses PCED because the AC is greater than the AR.

Price and output determining under perfect competition in the long-run

Activity 7

With reference to the case study in activity 6, due to the abnormal profits earned by Umutesi after two months, Umubyeyi and Sibomana joined the businesses of selling tomatoes in the same market starting with 5000 FRW each. After three months of the activity, they realised that what they used for starting the business is what they all earned.From the case study above:1. Identify the costs and revenues of each seller.2. Calculate the difference in earnings of Umutesi, Umubyeyi and Sibomana.3. Describe the nature of their earnings.4. Illustrate the above information on graphs.Facts

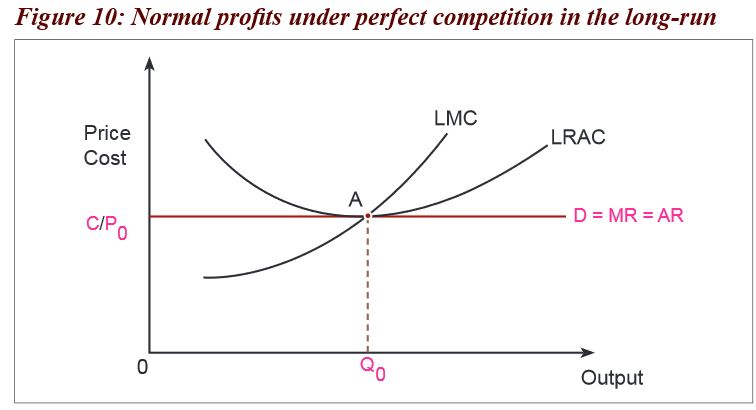

In the long-run, because of the abnormal profits in the short-run, other firms join the business hence the abnormal profits will be shared among all firms. Therefore, each firm will get zero or normal profits as seen below. It comes under the following conditions:• The average revenue (AR) must be equal to the average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be tangent to the average revenue line.• Marginal cost curve cuts the average cost curve at the lowest point. As shown in Figure 10 above, the firm produces output 0Q0 at Total cost

As shown in Figure 10 above, the firm produces output 0Q0 at Total cost and sells it at price 0P0 getting total revenue

and sells it at price 0P0 getting total revenue , hence making zero profits (normal profits).

, hence making zero profits (normal profits).

Break even and shut down points of a firm

Activity 8

With reference to the case study in Activity 7, Umutesi, Umubyeyi and Sibomana all earned normal profits.Munezero joined the businesses too and they all shared the same customers, leading to a reduction of the profits furtherup to the point when they could not cover all the costs of production.From the case study above:1. Explain why you think Munezero joined the business.2. Illustrate the points where:(a) All the sellers are earning normal profits.(b) All the sellers cannot cover all the costs of production.Facts

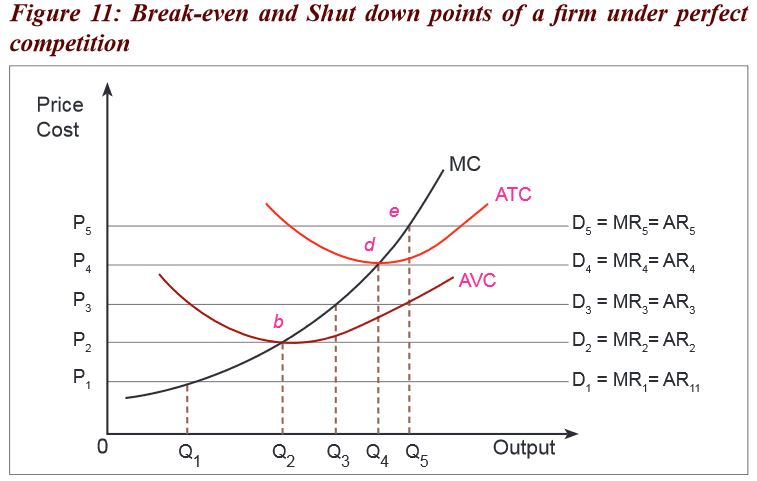

Break-even point is a point where the firm is earning normal profits and where the average revenue is equal toaverage cost. The firm can only cover the costs of production without earning any profit.Shut-down point is a point below which a firm cannot continue to operate because it covers only average variable cost. As shown in Figure 11 above, in the long-run, many firms join the business because of the abnormal profits in the short-runat point e and in the end, all firms get normal or zero profit at point d and they are only able to cover costs of production asshown by the ATC curve. Point d is the break-even point where the firm earns normal profits.Other firms will still join the business up to when the firm is not able to cover all the costs of production but only coversvariable costs as shown by the AVC curve.Point b is the shut-down point where the firm only covers variable costs. Below this point (point b),the firm cannot continueoperation.

As shown in Figure 11 above, in the long-run, many firms join the business because of the abnormal profits in the short-runat point e and in the end, all firms get normal or zero profit at point d and they are only able to cover costs of production asshown by the ATC curve. Point d is the break-even point where the firm earns normal profits.Other firms will still join the business up to when the firm is not able to cover all the costs of production but only coversvariable costs as shown by the AVC curve.Point b is the shut-down point where the firm only covers variable costs. Below this point (point b),the firm cannot continueoperation.Why firms continue to operate even when making losses (not covering all the costs)

Activity 9

With reference to the case study in Activity 8; explain why Umutesi, Umubyeyi, Sibomana and Munezero may all continueto operate even when they cannot cover all the costs of production.Facts

Sometimes, a firm may continue to operate even though it cannot cover all its costs of production. As long as it is in positionto cover its variable cost of production, it may continue operating. This may be explained by the following reasons:• Some firms fear to lose their skilled manpower which it would have trained at a high cost, which labour may be necessaryin the near future thus they continue to operate.• Some firms do not want to lose their established markets/customers as a solution to the problems sought.• Firms continue to operate because they fear to lose their suppliers of raw materials for their industry.• Firms may expect to get loans in future to cover the costs.• Some firms fear to be taken over by the state through nationalisation.• The firm may be a beginner firm, thus is still in its infancy and it expects to make profits in the long-run.• Some firms keep operating when they hope to change or restructure management, if it believes current losses are due topoor management.• A loss-making firm may be a branch of a bigger firm which is making profits and the losses can be shared by the otherbranches so as to cover the costs.• Some firms are not meant to be making profits but to give services such as welfare improvement in case of governmentorganisations.• Some firms may be set up for research/experimental purposes so they operate even if they are making losses.• Difficulties might be short-run and, therefore, hope to make improvements in the long-run.• Some firms keep operating when they fear to lose their reputation or good name in society.Supply curve of a firm under perfect competition

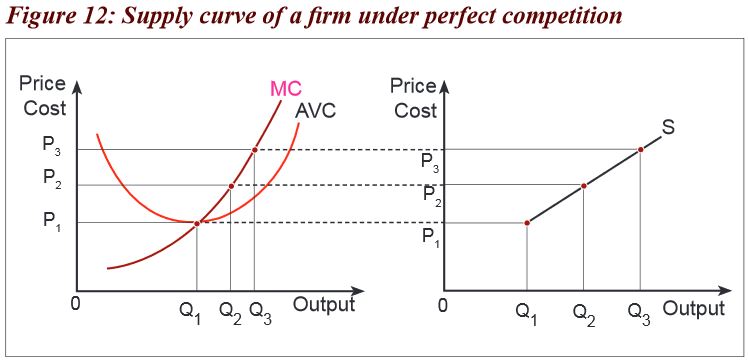

The supply curve under perfect competition is derived from the MC curve. Every time a firm determines its output, it will be where MC=MR. From that point, a perpendicular line is dropped to get the level of output. Therefore, each level of output will have a correspondence on the MC curve as illustrated in the figure below. As shown in Figure 12 above, the firm can only produce a high output if the price is high. If the price is less than minimumAVC, the firm does not produce. However, it does not mean that the firm leaves the industry. It only means a temporaryhalt in production.If the price is equal to or greater than

As shown in Figure 12 above, the firm can only produce a high output if the price is high. If the price is less than minimumAVC, the firm does not produce. However, it does not mean that the firm leaves the industry. It only means a temporaryhalt in production.If the price is equal to or greater than , the firm may continue to produce from output

, the firm may continue to produce from output  because of an increasein price, hence determining the supply curve.

because of an increasein price, hence determining the supply curve.Advantages of perfect competition

Activity 10

Present the arguments for and against perfect competitive markets.Facts

• Perfect competition encourages optimum use of resources because factors of production can freely move from oneplace to another.• There is production of better quality goods because of competition within the industry.• There is no wastage of resources because no advertisement costs are incurred.• There is no consumer exploitation because prices are determined by the forces of demand and supply.• There is a lot of output because of many suppliers and buyers.• Producers are able to expand their firms and use modern technology because of the abnormal profits in the short-run.• Perfect competition eliminates income inequality because in the long-run all firms earn normal profits.• The plant is used to full capacity in the long-run. This is mainly because firms operate at the least average cost and sothere is no resource wastage.Disadvantages or shortcomings

• Unemployment is likely to occur because of the inefficient firms leaving the production.• Buyers have little or no choice because the goods produced are the same.• There are no abnormal profits in the long-run, so, expansion of the firm is hard.• Research is difficult because of little of no profits in the long-run.• Firms aim at profit, maximisation and this discourages the production of public utilities such as water supply which arevital for society but are non-profit making.• Profits are reduced because the seller is supposed to sell at the same price as others.• Perfect competition cannot exist in reality and so cannot be relied upon for development.1.2.2 Imperfect markets

Activity 11

Basing on figure 13 below:1. Identify the activities dealt in.2. Suggest other institutions in Rwanda that deal in the same activities.3. What type of market structure is this?4. What are the characteristics of such markets?

Facts

Under imperfect markets, there are many market situations such as monopoly, monopolistic competition and oligopoly,among others.1.3 Monopoly

Monopoly is a market situation where there is one producer or supplier of a product, which has no close substitutes andentry into the market is highly blocked.Extreme forms of monopoly may include:1. Pure monopoly: This is a market situation where there is production of a commodity that has no substitutes at all.In practice, there is no pure monopoly because people can always forge substitutes for that commodity.2. Monopsony: This is market situation where there is only one buyer of a commodity or a factor of production,e.g. one employer.3. Bilateral monopoly: This is a market situation consisting of a single seller and a single buyer of a commodity.Features/characteristics of monopoly

The noticeable example is:(a) Water and Sanitation Company Limited (WASAC)(b) Energy and Utility Company Limited (EUCL)(c) National Bank of Rwanda (NBR)The bases/sources/origin of monopoly (Factors which give rise to monopoly)

Activity 12

Manzi Publishers Rwanda, is the sole supplier of economics books in Rwanda. Describe the factors that may have favouredit to carry out that activity alone and make presentations.Facts

• Patent rights e.g. writers of books, where the law forbids other firms to deal in the same commodity.• Ownership and control of strategic raw materials usually under government control e.g. minerals.This leads to natural monopoly.• Exclusive methods of production. This gives the producers monopoly of the skills that are needed for production.E.g. doctors.• Long distance among producers where each producer monopolises the market in his/her locality. This leads to spatialmonopoly• Advantages of large-scale production which do not allow small firms to compete successfully with large firms.• Protectionism: This is where trade barriers are imposed on the product to exclude foreign competitors. In such cases,the home producer may become a monopolist.• Take over and mergers: ‘Take-over’ is when one firm takes over the assets and Organisation of another whereas mergersare formed when firms combine their assets and organisations into one to achieve strong market position. Both situationsmay result into a monopolist firm.• Collective monopoly or collusive monopoly: This is where firms come together in a formal or informal agreement (cartel)to achieve monopoly power. Such firms can fix quotas (maximum output each may put on the market). They may also setthe price very low with the objective of preventing new entry of other firms. This is called limit pricingEquilibrium position of a firm under monopoly

Activity 13

Using the photographs in figure 14 on page 24:(i) Describe situations in the two photographs.(ii) Define the term equilibrium.(iii) When do you think the firm is in equilibrium?

Facts

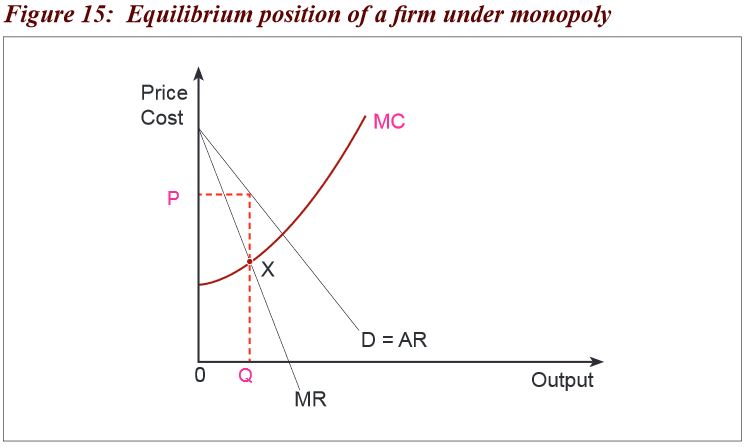

The monopolist is in equilibrium at a point where MC = MR and the slope of MR must be less than the slope of MC at the equilibrium output. The price is fixed on the demand curve in such a way that P = AR > MR = MC.The AR curve is above the MR curve. The price is fixed at the point where the demand curve is elastic. It can be illustrated below: As shown in Figure 15, the firm is in equilibrium at point x where MC=MR.

As shown in Figure 15, the firm is in equilibrium at point x where MC=MR.Profit maximisation of a firm under monopoly in the short-run

Activity 14

Mr and Mrs Gatete started a sugar producing firm in Kibungo with 1,000,000 FRW. After two months, they realised revenuesof 2,000,000 FRW. As they continued to produce, they made 800,000 FRW which is less than what they put in at the start.From the case study above;1. Identify the costs and revenues of Mr and Mrs Gatete’s firm.2. Describe the nature of their earnings in both situations.3. Illustrate the above information on graphs.Facts

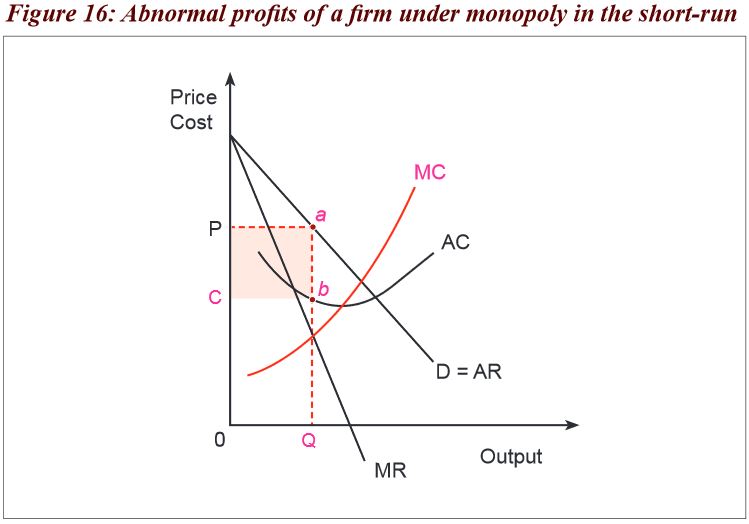

A firm under monopoly is in equilibrium where MC=MR and in the short-run, the firm can either make abnormal profitsor losses. Profits are made as seen below:Conditions

• The average revenue (AR) must be greater than average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be below the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. As shown in Figure 16 above, the firm produces output 0Q at total cost 0CbQand sells it at price 0P getting total revenue0PaQ,hence getting abnormal profits CPab.

As shown in Figure 16 above, the firm produces output 0Q at total cost 0CbQand sells it at price 0P getting total revenue0PaQ,hence getting abnormal profits CPab.Profits = TR-TC. 0PaQ -0CbQ= CPab

Losses under monopoly in the short-run

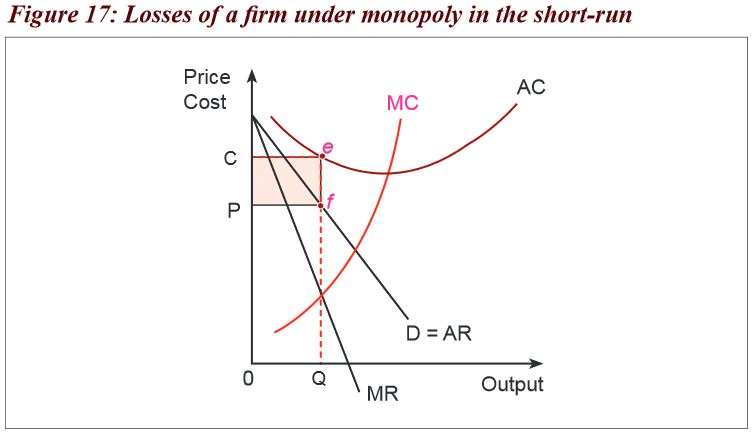

Conditions

• The average revenue (AR) must be less than the average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be above the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. As shown in Figure 17, the firm produces output 0Q at total cost 0CeQ and sells it at lower price 0P, getting total revenue0PfQ and thus makes losses PCef because the costs are greater than the revenue.

As shown in Figure 17, the firm produces output 0Q at total cost 0CeQ and sells it at lower price 0P, getting total revenue0PfQ and thus makes losses PCef because the costs are greater than the revenue.Equilibrium position of a firm under monopoly in thelong-run

Activity 15

With reference to the case study in Activity 14, after one year, Mr and Mrs Gatete continued to earn more than whatthey put in at the start.From the case study above;1. Present the reasons why they continued to do so.2. Illustrate the above information on graphs.Facts

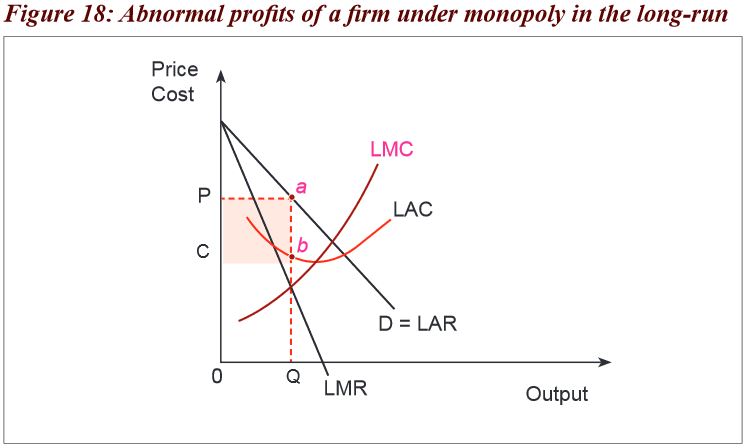

In the long-run, the firm under monopoly will still earn abnormal profits because it is the only firm in the production process.The firm will be in equilibrium where the long-run marginal cost curve is equal to long-run marginal revenue curve. This is shown as follows:Conditions

• The average revenue (AR) must be greater than average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be below the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. In Figure 18, the firm produces output 0Q at total cost 0CbQ and sells it at price 0P, getting total revenue 0PaQ hencegetting abnormal profits CPab.

In Figure 18, the firm produces output 0Q at total cost 0CbQ and sells it at price 0P, getting total revenue 0PaQ hencegetting abnormal profits CPab.Profits = TR-TC. 0PaQ-0CbQ= CPab

Advantages of monopoly

Activity 16

Present a skit about the advantages and disadvantages of monopoly firms.Facts

• There is no duplication of services and this saves resources e.g. if there is one hydroelectric power plant, there may notbe the need to set up another one in the same area.• Economies of scale can be enjoyed by the firm because it is capable of expanding using the abnormal profits earned.• There is a possibility of price discrimination. (Parallel pricing). This refers to the selling of the same commodity at differentprices to different customers which benefits the low-income earners.• Research can easily be carried out using the abnormal profits.• There is no wastage of resources in persuasive advertising which may increase prices.• Public utilities such as roads, telephones, etc. are easily controlled by the government as a monopolist.• Infant industries can grow up when they are monopolies and are protected from foreign competition.• It encourages innovations by protecting copyright and patent owners.Disadvantages of monopoly

• Because there is no competition, the firm can become inefficient and produce low quality products.• Monopoly firms produce at excess capacity, i.e. they under-utilise their plants so as to produce less output and sell ata high price.• Monopoly firms may charge higher price than firms in perfect competition.• In case a monopolist stops operating, there would be shortage of the commodity.• Monopoly firms tend to exert pressure on the government and sometimes they can influence decision making becausethey are the controllers of production.• Discrimination of consumers: This may be based on political or religious affiliation other than the factors respectedby economics.• Monopoly leads to income inequality. The monopolies who overcharge earn more compared to others.• Restriction of choices: A monopolist normally produces one type of commodity, thus consumers are denied a chanceto choose among the alternatives.Measures of controlling monopoly

Activity 17

Suggest the ways that the government of Rwanda can use to reduce monopoly powers.Facts

Because of the above disadvantages of monopolies, the following methods can be used to control their activities.• The government can fix prices of commodities through price legislation.• Anti-monopoly (anti-trust) legislation, i.e. laws imposed to control monopolies: Such laws can prohibit monopolisation,and collusion among firms to raise prices or inhibit competition.• There may be nationalisation of monopoly firms by the government so as to lower the prices.• Subsidisation of new firms: This can help the new times to competewith the already established firms favourably.• There may be resale price maintenance whereby the producers set prices at which sellers should sell the goods toavoid charging high prices.• Imports may be encouraged to compete with the commodities of monopoly firms in the country.• There may be demonstration by consumer groups especially boycotting the goods of monopolists so that the prices canbe lowered.• Government-owned firms may be set up to compete with the monopoly firms.•Removal of deliberate monopoly bases such as protectionism and taxation to encourage competition among the firms maybe an option.• Taxation: The government can impose taxes to reduce the profits of the monopolists. Such taxes may include:(a) Sur tax: This is an incentive tax that provokes monopolists to increase their scale of production.(b) Advalerem tax: This is a tax levied on the value of the commodity.(c) Specific tax: Tax charged per unit of out put.(d) Lamp-sum tax: Tax levied on the total amount produced and it does not change even if output changes.Price discrimination under monopoly (parallel pricing)

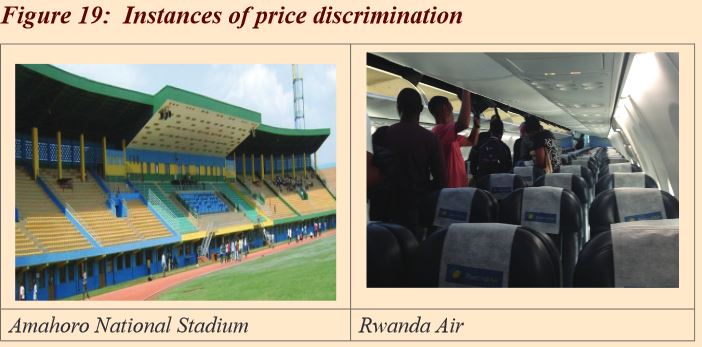

Activity 18

Basing on the photographs in Figure 19 below, examine;1. How customers are charged for the services rendered?2. The considerations followed while charging the customers in the photographs below?3. What conditions must be in place to charge customers in such a way?4. Merits and demerits of charging customers in such a way.

Facts

Price discrimination exists when a commodity is sold at different prices to different customers irrespective of the cost of production. It can also be referred to as parallel pricing.Forms of price discrimination

• Discrimination according to personal income: For example, income differentiation among buyers, e.g. doctors charginglow prices on the poor and high prices on the rich for the same services.• Discrimination according to age: For example, charging low prices on the young people than old people on tickets towatch football or for a film show.• Discrimination according to sex: Where different prices are charged to females and males for example, for discothequeswhere for ladies’ nights, ladies enter for free and males are made to pay.• Geographical discrimination for example, dumping where commodities are sold cheaply in other countries to disposeoff surplus.• Discrimination according to the time of service for example, tickets for video shows charged at high prices in afternoonswhen there are many people than in morning hours when there are few people.• Discrimination according to nature of the product, for example, a soft cover book may be cheaper than a hard cover book.• Discrimination according to the number of uses of the product, for example, a soft cover book may be cheaper thana hard cover book.• Discrimination according to the number of uses of the product, for example, electricity used for industrial purposesis cheaper than electricity for domestic use.• Discrimination by differentiation of commodities, for example, high prices on travellers in first class in the train andlow charges of other classes such as the economy class.Conditions for price discrimination to be successful• The commodity must be sold by a monopolist so that even when the price is increased, the buyer has nowhere else to go.• Elasticity of demand should be different in different markets. A higher price should be charged in the market where elasticityof demand is lower than where elasticity of demand is high.• The cost of dividing the markets should be very low, for example, in case of dumping costs of transport should be low.• Buyers should not know how much is charged on others. This is possible especially where goods are sold on orders withno advertising.• It should be impossible for buyers to transfer the commodity from where the price is low to where the price is high.This is possible especially with services of doctors, teachers, etc.Advantages of price discrimination

• It enables the poor to get essential services at low prices, for example, cheap houses to civil servants and doctorscharging low prices on poor patients.• To the sellers, it increases total revenue because output sold increases.• It is one way in which the rich subsidise the poor thus a method of income distribution. The rich are charged highlyon commodities while the poor are subsidised on the same commodities.• It increases sales and consumption, for example, for air time, the first units, may be charged higher price than otherextra units. Therefore, the more units of air time you use, the less charges you would pay for extra units.• It helps producers to dispose of surplus and poorly manufactured commodities, for example, dumping.• Increased efficiency: The increased profits from the higher charges make the firms efficient and such profits arere-invested.Disadvantages of price discrimination

• It may encourage consumption of some commodities in undesirable excessive amounts. For example,when childrenare charged less for entrance in cinema halls, they may spend more time watching films thanon studies or leisure.• It increases monopoly powers of firms by limiting entrance of other firms in the market. One firm serves all categoriesof customers irrespective of their incomes, ages or sex.• It can lead to low quantity of products/services, for example, in some airlines, travellers in the economy class(where fares are lower) are sometimes not well treated by airline staff like those in the first class (where fares are higher).• Discrimination in form of dumping discourages local industries.• Poor quality output normally arises. Such output is sold to the less privileged who yearn for the less prices.• Misallocation of resources: Price discrimination may bring about divergence of resources from their socially optimal usesto those who can reward highly.1.3.1 Monopolistic competition

Activity 19

Using the photographs in figure 20 below:1. Identify the nature of services offered.2. How many sellers do you think deal in such a business in Rwanda?3. Identify some in your area.4. What type of market structure is seen in the figure below and why?5. Identify other businesses in Rwanda that may fall under the same market structure.

Facts

Monopolistic competition market structure has characteristics similar to that of perfect competition except that the commodity dealt with in monopolistic competition is not homogeneous. It is a market structure in which a large number of firms sell differentiated products with close substitutes. Product differentiation may be in form of packing, design, quality, branding, advertising, blending, giving credit, etc. There is a need for persuasive advertising in monopolistic competition. Monopolistic competition lies between perfect competion and monopoly.Because of product differentiation, the seller has some control over the market price. Examples of monopolistic firms are soap industry, bread industry, hotel industry, washing powder, hair salons, shoe repairers, etc.Characteristics of firms under monopolistic competition

• There are many buyers and several sellers.• Firms deal in differentiated products although they remain close substitutes.• There is a lot of persuasive and informative advertising.• The demand curve is fairly elastic in nature because of the presence of many substitutes.• There is production at excess capacity, i.e. production less than the required output so as to charge at a high price.• The firms in the industry are large but none of them dominates the market.• The major aim is to maximise profits and this is done at a point where marginal revenue is equal to marginal cost (MR=MC).• Firms are price makers to some extent and price takers to a certain extent.• There exists brand loyalty, i.e. consumers exercise a lot of loyalty by sticking on a particular commodity believing thata particular brand is superior.Equilibrium position of a firm under monopolistic competition

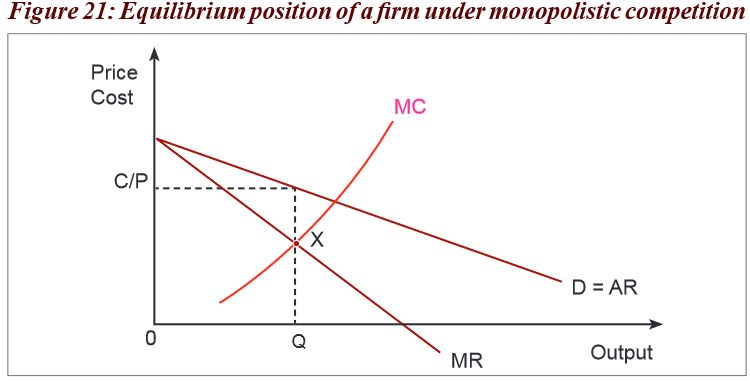

The firm under monopolistic competition is in equilibrium when the MC=MR and in the short-run the firm will either make abnormal profits or losses. The supernormal profits will exist in the short-run because new firms cannot enter the industry. In the short-run, the firms may attempt to maximise their profits by changing the quality and the nature of the product and by increasing advertisement expenditure. But since there are many close substitutes, neither of the strategies would be of much avail in the short-run. Point x in Figure 21 above shows the equilibrium point where MC=MR.

Point x in Figure 21 above shows the equilibrium point where MC=MR.Price and output determining of a firm under monopolistic competition in the short-run

Activity 20

Colgate and Whitedent are two competing toothpaste firms. They all started the business using the same capital of 2,000,000 FRW each. After three months of operating, Colgate firm received revenues more than the amount it put in; while Whitedent firm, received less revenue than what it put in.From the case study above;1. Describe the nature of their earnings.2. Suggest reasons to support the above situation.3. Illustrate the above information on graphs.Facts

A firm under monopolistic competition is in equilibrium where MC=MR and in the short-run the firm can either makeabnormal profits or losses. Abnormal profits are made as seen below:Conditions

• The average revenue (AR) must be greater than the average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be below the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. From Figure 22 above, the firm produces output

From Figure 22 above, the firm produces output at cost

at cost  and sells it at price

and sells it at price  ,getting total revenue

,getting total revenue .

.

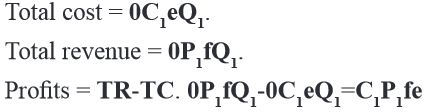

Losses under monopolistic competition in the short-run

The firm can also make losses when it is in the production processes. This is shown below:Conditions• The average revenue (AR) must be less than average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be above the average revenue curve.• Marginal cost curve cuts the average cost curve at the lowest point. From Figure 23, the firm produces output

From Figure 23, the firm produces output at cost

at cost  and sells it at a lower price

and sells it at a lower price  .

.

Equilibrium of the firm under monopolistic competition in the long-run

Activity 21

With reference to the case study in Activity 20, due to the abnormal profits earned by Colgate, other firms such as Delident, Close up and ABC joined the business. After three months of the activity, they realised that what they used for starting the business is what they all earned.From the case study above;1. Describe the nature of their earnings.2. Explain reasons for such a nature of their earnings.3. Illustrate the above information on graphs.Facts

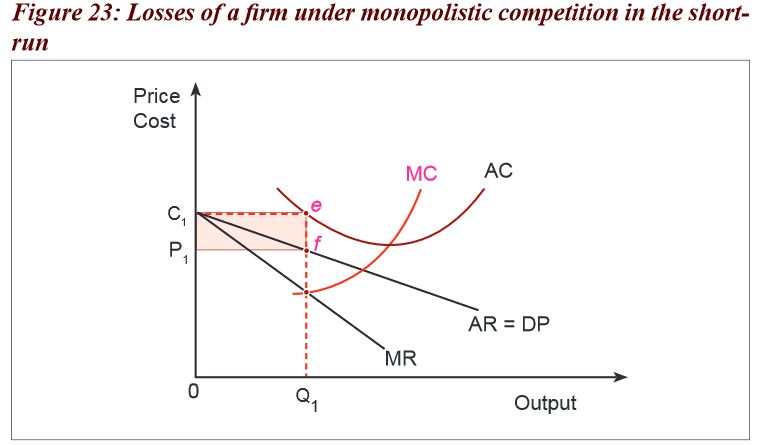

Due to the supernormal profits in the short-run, new firms join the industry with new brands. Output increases,Product differentiation increases. Consumer choice widens but the firms reduce the level of their output sincethe market has remained the same.The firms that were previously incurring losses leave the industry. Therefore,the demand curve would keep onshifting to the left until a point is reached where the demand curve is tangent to the ATC (LAC) curve.Equilibrium is attained at point where Long-run Marginal Cost Curve (LMC) = Long-Run Marginal Revenue (LMR).Conditions

• The average revenue (AR) must be equal to the average cost (AC).• The average revenue curve determines the price while the average cost curve determines the cost of the firm.• Average cost curve must be tangent to the average revenue line.• Marginal cost curve cuts the average cost curve at the lowest point From Figure 24, output

From Figure 24, output is produced at a high total cost

is produced at a high total cost  and sold at the same price OP1/C. The total cost is 0C/

and sold at the same price OP1/C. The total cost is 0C/ and the total revenue

and the total revenue  .The firm produces a lower output

.The firm produces a lower output as shown by point A. However, it should produce output

as shown by point A. However, it should produce output as shownby point x where

as shownby point x where is excess capacity, i.e. the difference between actual output and expected output.

is excess capacity, i.e. the difference between actual output and expected output.Product differentiation under monopolistic competition

Activity 22

Through research, in businesses near your school, find out about:1. The methods the sellers use to make their products different from others that serve the same purpose.2. Advantages and disadvantages of such businesses to the societyFacts

This is a situation where a producer is in position to make his or her product appear different from other products of other firms. It may take the following forms. Packaging, Design / shape, Branding, Colour, Scent, Labelling, Salesmanship, Size, etc.Advantages of monopolistic competition

• Product differentiation enables consumers to get a variety of products.• Firms compete to make improvement in the quality of products to choose from.• In case one firm collapses, substitutes are available for the consumers.• The price charged is lower than that of a monopolist because of competition from substitutes.• The freedom of entry gives a chance to any willing entrepreneur to enter the industry which createsemployment opportunities in the country.• Individual firms gain a lot of popularity due to specialisation in their own brands.• In the short-run, abnormal profits earned are used to improve on the quality of products; undertake research;and expand the size of the firmDisadvantages of monopolistic competition

• There is under-utilisation of resources in the short-run and in the long-run and this leads to excess capacity.• In the long-run, there is no profit to make improvements. So, the firm may not expand to enjoy economies of scale.• The price charged on buyers is higher than in perfect competition.• In the long-run, there are no profits to invest in research since the firm earns normal (zero) profits.• To maintain the market share, the seller has to persuasively advertise and this may increase costs and the price.• There are limited employment opportunities as firms operate at excess capacity.• The output produced is less than that in perfect competition.1.3.2 Oligopoly

Activity 23

Using the photographs in figure 25 on page 43;1. Identify the nature of services offered.2. How many sellers do you think deal in such a business in Rwanda?3. What type of market structure is seen in the photographs and why?4. Identify other businesses in Rwanda that may fall under the same market structure.5. Identify characteristics of such a market structure.

Facts

Oligopoly is a market structure which is characterised by a few sellers and many buyers of closely related commodities. Such commodities can either be homogeneous or differentiated.If the commodities dealt in are homogeneous then the market is known as perfect oligopoly.If the products dealt in are differentiated then the market is known as imperfect oligopoly.Examples of firms under oligopoly

Mobile telephone companies such as MTN, Tigo, Airtel; petroleum companies such as Kobil, SP, Mount Meru;soft drink companies such as Coca Cola and Pepsi Cola; beer companies such as Bralirwa and Skol;newspaper firms such as The New Times, Umuseso, Imvahonshya, etc.Features/characteristics of oligopoly

• There are few, unequal, competing firms. Each firm, although faced with competition from other firms,has enough market power and, therefore, cannot be a price taker.• There is non-price competition such as advertising, quality of services, etc. If one firm reduces the price,others would do the same and all firms would end up losing.• Each firm is concerned with the activities of other firms so as to act accordingly, for example it can reducethe price when others reduce the price.• In most cases, there is product differentiation.• Presence of monopoly power: There are very few oligopoly firms and this makes it easy for collusion as a formof price determination leading to monopoly.• Uncertainty: There is a lot of uncertainty in oligopoly industry, as one firm takes a decision say to increase the price,it cannot be certain of the reaction of other firms.• There is limited entry into the production process.• There is price rigidity. Prices tend to be stable for a long period of time.• Firms are faced with a kinked demand curve, i.e. a curve that has a bend (kink) and it is elastic above the kink andinelastic below the kink.• There are price wars, i.e. when one firm reduces the price, other firms reduce theirs even lower.Forms of oligopoly

1. Perfect oligopoly/pure oligopoly: This is a form of oligopoly where there are few firms which sell ahomogeneous product such as petroleum companies.2. Imperfect oligopoly: This is a form of oligopoly where there are few firms dealing in differentiated commoditiesfor example dealers in soft drinks, tea industry, tobacco industry etc.3. Duopoly: This is an extreme form of oligopoly where there are only two firms in the market.4. Duoposony: This is a form of oligopoly where there are two buyers in the market.5. Oligopsony: This is a form of oligopoly where there are a few buyers in the market.Price determination under oligopoly

Activity 24

When Kobil fuel station increased its price, other companies such as SP, and Mount Meru, among others,never followed. Hence, the customers of Kobil fell drastically and so did its revenue. Kobil decided to reducethe price even further lower than its rivals and also the rivals reacted by reducing their prices to the same level.They, therefore, found themselves selling at the same price. Each firm designed unique measures to win the marketother than price wars.From the case study above;1. Identify the methods of price determination in oligopoly.2. Illustrate the nature of the demand curve under oligopoly.3. Which measures do you think can be used by rival firms to win market.Facts

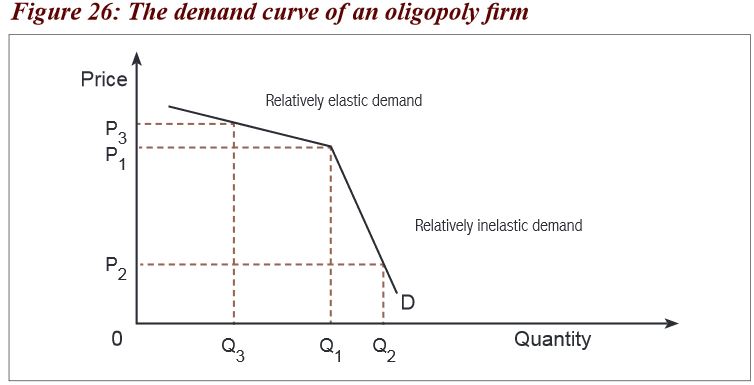

Under oligopoly, there is no single method of price determining but prices are determined by any of the following methods:1.Independent pricing:This is where each firm or seller sets its own price for profit maximisation.2.Perfect collusion: This refers to cartel agreement where independent firms within the same industry cometogether to determine the price and output with the purpose of reducing unnecessary competition.An example is OPEC.3.Imperfect collusion: Here there is price leadership where the dominant firm decides on the price for others to eitherfollow if it is favourable or exit the industry if it is unfavourable.The demand curve of an oligopoly firmThe demand curve is kinked because the demand for their products largely depends on the behaviours of other rival firms.This brings uncertainties in the industry because no single firm can predict the reaction of another firm in case they take their own decision. The kinked demand curve is elastic above the kink and inelastic below it. This is shown below. From Figure 26 above, P1 is the market price or administered price. Should any firm increase its price above that priceto price P3, it would lose its customers (Q1- Q3) to other firms. If a firm decides to set price below P1 to price P2,other firms will react by reducing their price even further or lower to win more customers, hence increase in quantitysold will be lower (Q1-Q2) than the reduction in price. Hence, the demand curve has a kink meaning that the priceswill remain rigid/stable for a long period of time.

From Figure 26 above, P1 is the market price or administered price. Should any firm increase its price above that priceto price P3, it would lose its customers (Q1- Q3) to other firms. If a firm decides to set price below P1 to price P2,other firms will react by reducing their price even further or lower to win more customers, hence increase in quantitysold will be lower (Q1-Q2) than the reduction in price. Hence, the demand curve has a kink meaning that the priceswill remain rigid/stable for a long period of time.Non price competition under oligopoly

This is a situation where firms compete on the basis of other things other than price in an attempt to widentheir markets in the same industry. It is a common feature in oligopoly.The forms of non-price competition used by oligopolistic firms in Rwanda

• Persuasive advertisement using various media such as radios, television, newspapers, etc. to make people awareof the commodity.• Branding and blending, i.e. use of appealing brand names such as Rwanda tea.• Offering credit facilities to customers to encourage them to keep buying.• Offering gifts and free samples to encourage them to buy more such as petrol stations giving soap to customers.• Opening many branches in different locations in the country.• Offering after sales services such as free delivery of purchases to customers’ premises; guaranteeing spare partsall which attract customers to the firm involved.• Sponsoring social events such as sports and music, for example Guma Guma with Primus thus winning the market.• Organising promotions through raffle draws which are intended to increase the number of customers who are attractedto buy the commodity in order to join the draw, for example MTN Sharama, join the millionaires club by Tigo.• Organising trade fairs and exhibitions to make their products known to customers.• Offering mobile shops: This is where the firm puts its products in a vehicle/ bicycle and moves from place to place sellingits products, for example bread firms.• Renovation of premises of customers by rival firms for example telecommunication networks (Tigo, MTN, Airtel),beer firms (Primus, Skol).• Use of stop-shopping centres such as supermarkets at fueling stations.• Use of differentiated attractive packaging and convenient designs of products by firms to outcompete each other,for example Blue Omo.• Quality improvement and introduction of new variables in order to increase their market share.• Use of appealing slogans which attract customers to their products, for example MTN-everywhere you go,Tigo-live it love it, Airtel-express yourself.Equilibrium position and profit maximisation of a firm under oligopoly

Activity 25

Choose the best alternative:1. The firm under oligopoly is in equilibrium when(a) MC = MR (c) MC = AC(b) AC = AR (d) AR = MR2. The firm under oligopoly earns: (a) Normal profits (c) Abnormal profits(b) Losses (d) None of the above3. Oligopoly firms operate at (a) Optimum capacity (c) Over capacity(b) Excess capacity (d) Equilibrium point4. The demand curve under oligopoly is:(a) Elastic (c) Inelastic(b) Perfectly elastic (d) kinkedFacts

Under oligopoly, the firm is in equilibrium where the MC=MR and oligopolists make abnormal profits both inthe short and long-run as shown in figure 27 on page 49: From Figure 27 above, the firm produces output 0q at total cost 0Cxq and sells it at price 0P getting total revenue 0PKq.

From Figure 27 above, the firm produces output 0q at total cost 0Cxq and sells it at price 0P getting total revenue 0PKq. The marginal revenue curve is not continuous between sections T and S because of uncertainties.The firm is, therefore, in equilibrium at point T where MC = MR and earns abnormal profits shown by the area CPKx.

The marginal revenue curve is not continuous between sections T and S because of uncertainties.The firm is, therefore, in equilibrium at point T where MC = MR and earns abnormal profits shown by the area CPKx.Advantages of oligopoly

Activity 26

Present a case for and against oligopoly market structure.Facts

• There are low prices to the consumers due to existence of intensive competition and fear of other firms reaction.• It eases consumer budgeting due to price stability.• It widens consumer choice production of a variety especially with imperfect oligopoly due to branding and productdifferentiation.• There is production of good quality goods due to competition.• There is increased innovation due to competition.• There is increased output due to production on large scale.• Stable prices are charged due to the presence of price rigidity.• Consumer awareness of the commodity is high due to extensive advertising.• Most oligopoly firms operate on large scale, which enables a firm to enjoy economies of scale.• Provision of gifts to customers such as books, soap, pens, etc. improves on customer welfare.• A lot of abnormal profits earned are spent on research and development which leads to technological advancementand a high standard of living in the country.Demerits of oligopoly firms

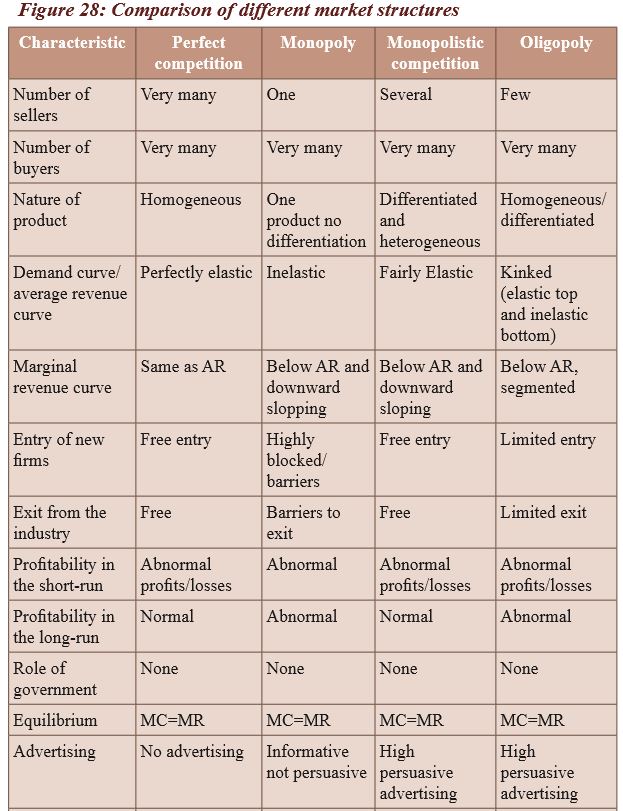

• There is consumer exploitation through overcharging due to collusion.• There is duplication, hence wastage of resources.• Small firms collapse when they are outcompeted.• There is under-exploitation of resources due to production at excess capacity.• Industries with large firms exert pressure on government.• Oligopoly distorts consumer choices due to excessive advertisements.• It worsens income inequality due to limited entry of other firms.• Some firms at times engage in price wars where each firm keeps on reducing on prices of its products tooutcompete rival firms, which results into losses.• Profits are limited due to price rigidity and this may affect further expansion.• Firms incur high costs on advertising, which increases on the price of the commodity.• The market structure is characterised by uncertainties about the reactions and activities of other firms, which limitthe ability of an individual firm to make independent decisions.1.3.3 Comparison of the different market structures

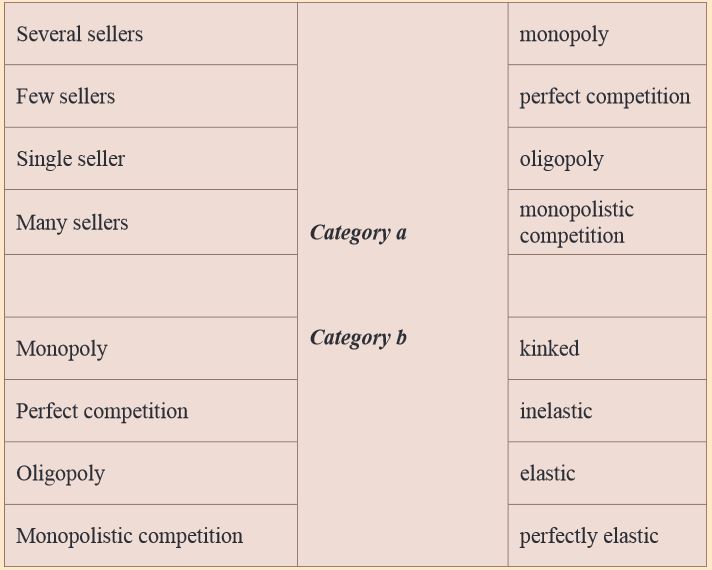

Activity 27

Match the following

Facts

Unit assessment

1. (a) How are market structures categorised?(b) What distinguishes the different firms in market structure in Rwanda?2. (a) Describe the basis of monopoly in Rwanda. Give examples.(b) Why do you think it is necessary to interfere with monopoly firms in Rwanda?(c)Why do you think there is need of state monopolies in Rwanda? Give examples of state monopolies.3. Having tackled all market structures in which firms in Rwanda operate, which would you recommend formost effective utilisation of resources and solving macro-economic problems in Rwanda and why?4. (i) Define the term price discrimination.(ii) Explain the different forms of price discrimination.(iii) Analyse the conditions necessary for price discrimination to be successful.1.4 Glossary

- Advalerem tax: A tax levied on the value of the commodity.

- Bilateral monopoly: A market structure consisting of a single seller and a single buyer of a commodity.

- Break-even point: The short-run rate of output and sales at which a supplier generates just enough revenue to cover fixed and variable costs, earning neither a profit nor a loss.

- Break-even price: The level of price at which it “breaks even,” covering costs but earning no profit.

- Buyer’s monopoly: The condition which exists when there are numerous sellers but only one buyer

- Cartel: A contractual association of independent business organisations, located in one or more countries, formed for the purpose of regulating the prices, purchasing, production or marketing of goods by the members. It acts basically as a monopoly in price and output decision.

- Collusion: An agreement among sellers of a commodity or commodities to set a common price and/or share market.

- Dumping: The selling of a commodity abroad at a lower price than in the home market. This practice may be pursued by a producer when a large volume of production lessens the unit cost of the product, and when, because of the large production, the price of the product would be reduced if sold entirely in the domestic market. By restricting the supply offered in the home market, the producer may sell the balance of the supply abroad at a lesser price and still gain more profits than they would gain if the supply were sold at home.

- Duopoly: The condition that exists when only two producers offer identical or nearly identical products.

- Economic profit: The return on capital above that necessary to keep it in a particular use; also known as pure profit or supernormal profit.

- Equilibrium: A state of balance, when variables under consideration have no tendency to change.

- Equilibrium price: The price at which quantity supplied equals quantity demanded. It is determined by intersection of supply and demand curves.

- Equilibrium quantity: The quantity at which a market is in equilibrium. It is determined by intersection of supply and demand curves.

- Excess capacity: A situation where the firm produces less than the installed capacity, i.e. state of under-utilisation of the available resources.

- Imperfect collusion: Here, there is price leadership where the dominant firm decides on the price for others to follow.

- Imperfect oligopoly: An oligopolistic market situation where the commodities dealt in are heterogeneous (differentiated).

- Independent pricing: This is where each firm or seller sets its own price for profit maximisation.

- Infant industry: In foreign-trade theory, this is an industry that has not had sufficient time to develop the experience or expertise, or that has not grown enough to exploit the economies of scale needed to compete successfully with more mature industries producing the same commodity in other countries. Infant industries are often thought to need tariffs or quotas to protect them while they develop.

- Lamp-sum tax: Tax levied on the total amount produced and it does not change even if output changes.

- Limit pricing: A situation where oligopoly firms set very low prices so as to block entry of other firms into the production.

- Long-run: The period of time in which a firm can increase or decrease all of its inputs. All inputs are variable.

- Long-run average cost curve: The curve enveloping, target to, all possible short-run average total cost curves for a firm. It shows the lowest possible average cost when all inputs are variable.

- Long-run costs: Costs when all factors of production are variable.

- Long-run equilibrium: The equilibrium when all costs are variable. In pure competition, when P = AR =SMC = SAC = LMC = LAC.

- Marginal cost: The additional cost incurred by producing one additional unit of output.

- Marginal revenue:The change in total revenue due to a unit change in the quantity sold, the additional revenue a firm would obtain if it sold one unit of output. In perfect competition, this is the same thing as price. Under imperfect competition, MR is less than price because in order to sell the extra unit the price must be reduced on all prior units sold.

- Market: The area within which buyers and sellers are in communication with one another and within which exchanges take place.

- Merger:The combination of two or more firms into a single firm.

- Monopolistic competition: The market structures in which many firms produce similar products but with some degree of product differentiation, resulting in each firm’s having a partial monopoly. An example is a bread industry.

- Monopoly: One firm has 100% of the market. This rarely occurs in the actual structure.

- Monophony: The market structure with only one buyer of a good

- Monopsony: A market structure where there is only one buyer of a commodity or a factor of production.

- Mutual interdependence: The interdependence of firms in an oligopoly because each firm is affected by what its rivals do.

- Natural monopoly: A monopoly due to natural conditions.

- Non-price competition: The methods of competition, such as product differentiation advertising, that are not based on changes in prices.

- Oligopoly: A market structure in which the number of firms is small enough that changes in price and output of one firm will affect the price and output decision of the others.

- Over production: Production in excess of what is demanded.

- Patent: The legal monopoly over a product or process granted by government for a period of 17 years.

- Perfect collusion: This refers to cartel agreement where independent firms within the same industry come together to determine the price and output with the purpose of reducing unnecessary competition.

- Perfect competition: A market structure with all characteristics of pure competition, perfect knowledge, no transport costs and perfect mobility of factors of production.

- Perfect oligopoly: An oligopolistic market situation where the commodities dealt in are homogeneous.

- Predatory pricing:A situation where oligopoly firms set very low prices to get little profits so as to drive out already existing firms from production.

- Price discrimination: A situation where a commodity is sold at different prices to different people.

- Price leader:A firm in an oligopolistic industry that signals a new price by announcing a price increase or decrease. All other firms follow with similar price changes. The price leader firm is normally the largest producer or a low-cost firm.

- Price taker: A purely competitive firm. A firm unable to influence the market price.

- Product differentiation: The attempt to make a product seem different from its rivals. This is frequently accomplished through advertising, design changes and quality.

- Profit: The difference between total revenue and total cost.

- Pure competition: A market structure with a large number of buyers and sellers of a commodity. No buyer or seller can affect price.

- Revenue: The price of each unit of output times the quantity of output sold.

- Short-run:The period of time in which some of the firm’s inputs are fixed.

- Short-run average total cost curve: A curve showing average total costs over possible outputs for a given firm size — the plant is fixed.

- Short-run costs: Costs when some inputs are fixed.

- Short-run equilibrium: Equilibrium when some costs are fixed; in pure competition, when P = MC = MR.

- Shut-down price: The point where market price is so low that the firm’s losses per period just equal its fixed costs. Thus,it might just as well shut-down. The shut-down point comes at the point where the market price is just sufficient to cover average variable cost, and no more.

- Specific tax: A tax charged per unit of output.

Unit summary

• Meaning and categories of market structure• Perfect markets• Perfect competition• Imperfect markets• Monopoly• Monopolistic competition• Oligopoly• Comparison of different market structures- Economics S5 SB File Modified 1/11/21, 13:59

- Economics S5 TG File Uploaded 9/11/21, 16:03

- QUESTIONS AND ANSWERS FOR SECONDARY 5 File Uploaded 24/04/20, 07:16