Unit 6 INTRODUCTION TO COMPANY ACCOUNTS

Key unit competence : To be able to prepare books of accounts for alimited Liability company

Introductory activity

Company accounts analyses Company financial activities over a period of

12 Months. They are prepared and maintained for every period to show

the Company’s performance and its assets against liabilities. Unlike sole

proprietorship or Partnerships, Company accounts records amounts fromshares, debentures etc.

From the knowledge acquired from the previous subjects, what do you

think is the distinction between, a sole proprietorship, Partnership fromCompany accounts?

6.1. Introduction to limited liability Company

Learning Activity 6.1

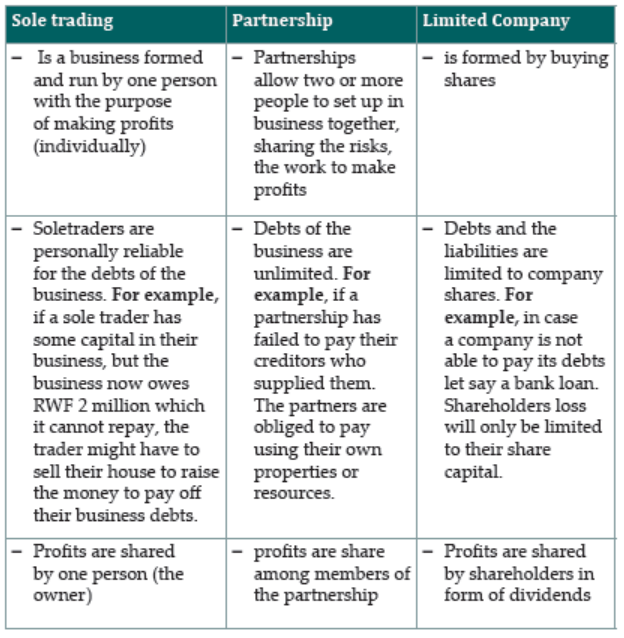

Sole proprietorship, partnership differs from companies in terms of the

size and the share capital.1. What are the benefits of forming companies?

6.1.1. Company as corporate legal body

A company is a legal entity formed by a group of individuals to engage in

and operate a commercial business. Similarly, a company is described as a

voluntary association of persons who have come together for carrying on

business and sharing the profits. Members of the company work together

with the same goal to accomplish particular goal. The members of the Company

are called Shareholders. They are called shareholders because they boughtshares.

Being considered a legal entity in the terms of the law, companies are able

to enter into contracts, hold and dispose of property, raise capital through

the issuance of shares, etc. The members of a company enjoy a separate and

distinct existence from members. Unlike single traders/ sole proprietorships,and partnerships. The company business pays off its liabilities and debt.

According to Rwanda’s Law Governing Companies 17/2018, company

accounts must be filed three months after the year’s end. They frequently

include specific guidelines on the minimal data that must be included in

a company’s financial statements. Non-incorporated enterprises, often

known as unlimited liability companies, frequently experience relativefreedom from statutory regulation.

Companies are classified into two namely ;

1. Limited liability Company

2. Unlimited liability Company.

1. Limited liability Company

What is a limited liability Company ?

A limited company is a company limited by shares or a limited liability

Company is form of company where the shareholders are only limited by theirshares.

Limited liability means that a company’s owners or investors are only liable

for the total amount of money (in form of shares) they have invested in the

business. The shareholders of the business will be protected in the case of

bankruptcy if it is registered as a limited liability company. Furthermore

«limited liability» will imply that the owner’s losses are only restricted to

the proportion of their specific share and that they are not liable for losses

that exceed their shares. In this case, if the company suffers losses or goesBankrupt, they cannot attack their own properties.

2. Unlimited liability

Unlimited liability is the opposite of limited liability. Unlimited liability means

that if the company incurs debts that it is unable to pay, the owners will be

held personally accountable for the unpaid debts and may be required to selltheir personal properties in order to pay back the debts.

Characteristics of limited Companies

1. All members have a limited liability

2. They have a separate legal existence

3. The debts of the company are separate from those of the shareholders

4. Shareholders are not liable for the day to day activities of the business5. It can carry out any activity as long as it does not go against the law.

Advantages of Companies

• Shareholders enjoy limited liability

• Larger capital is raised through larger membership

• Risk of fraud is minimized because their accounts are audited annually.

• They are more permanent in nature because the death or retirement

of a

• Shareholder does not affect the company.

• Companies can easily access funds from financial institutions.

• Companies operate in legal frame work-companies Act.

Disadvantages of companies

• They pay formation and registration costs

• Burden of taxes : companies pay corporation tax.

• The shares of a company are scattered and the transferability of the

shares

• Kills the morale of the shareholders and when the morale is down,

the affairs of the company are not considered which gives chance to

managers to promote their own interests.

• Companies are difficult to form because they have to produce a number

of documents and have to follow legal procedures before they are

formed.

• If profits are made, they are reduced as they have to be shared among

shareholders.

6.1.2. Difference between Sole trader, Partnership and LimitedCompany.

Formation of registration of companies in Rwanda :

A company is formed by incorporation. Incorporation is done by :

• Filling appropriate forms for Memorandum of association and may

have also

• Articles of association given to registrar of companies with appropriatefees and a certificate of incorporation is issued.

Memorandum of association is a document that shows the relationship between

the company and the outsiders. It contains the following ;

• The name and address of the company,

• The objectives of the company, showing whether it is :

– Limited or unlimited– Private or public and the authorized share capital

Articles of association shows the rules and regulations for the company internalstructure.

It contains items like :

• The number of directors,

• When the annual general meetings are to be held.

• The voting rights of the shareholders,

• Dividends policy, and• Other rules.

NOTE : It is a pre-requisite for companies to prepare Articles and Memorandum

of Association and get them notarized by a Public Notary. One copy is retained

at the Notary’s Office, one at the Registrar General’s Office at RDB and one atthe Office of the Official Gazette for publication.

Certificate of incorporation

A certificate of incorporation is obtained at the Company registry at RDB upon

submitting an application letter addressed to the Registrar General, a receipt

of registration fees payable at the National Bank of Rwanda and three copiesof the articles and memorandum of Association

Establishing a subsidiary/branch

Foreign companies wishing to establish a branch or a subsidiary company

in Rwanda apply to the Minister of Trade and Industry for authorization to

establish a branch and the Registrar General of RDB for registration in the

registry of companies. RDB is the principal Government Agency responsible

for facilitating investors to realize their investment projects in Rwanda

They must present a board resolution/declaration of the company to invest in

Rwanda, articles and memorandum of association of the parent company andcertificate of incorporation.

6.1.3. Shares and share capital

Definition of shares

A share is a unit of Capital to a company. It is the interest a shareholder or

owner has in a company. Memorandum of association (company constitution)must statea fixed amount of a share.

Types of shares

Shares are broadly divided into two;

• Ordinary shares

• Preference shares.

Ordinary shares

Ordinary shares are those shares which do not carry a fixed rate of dividends

and the dividend rate depends on amount of profits and directors` decisions.

Ordinary dividends are paid after tax and after full payment of preference

dividends. The holders of ordinary shares are called ordinary shareholders

and they are paid ordinary dividends out the profits make by companybusiness.

Ordinary shares are considered as risk takers as they get their dividends after

the full payment of the preference dividends. However, they are able to usetheir rights to manage the firm’s affairs by voting at meetings of the company.

Preference shares

Preference shares right a fixed rate of dividends out of profits distributed for

any year and their holders claim first their dividends before ordinary shares.

Ordinary dividends cannot be paid before preference shareholders are paid in

full. The holders of preference shares are called preference shareholders and

are entitled to preference dividends out of the profits made by the company

business. In the event of a company’s liquidation, preference shareholders

will have priority over ordinary shareholders in receiving their capital back.Preference shareholders do not carry a voting right.

Types of preference shares

Cumulative preference shares: These shares entitle their holders to a

fixed rate of dividend. If there are not sufficient profits to pay this fixed rate

in a particular year, arrears will be paid in the following year or at a firstopportunity when profits are made.

Non-cumulative preference shares: These also claim a fixed rate of

dividend and if there are not sufficient profits to pay in a particular year theirholders do not claim arrears in the following year.

Example Dividends on ordinary shares and preference shares

UMUCYO Ltd has issued 50, 000,000 ordinary shares of RWF500 each and

20,000,000 7% preference shares of RWF100 each. Its profits after taxation

for the year to 30 September 20X5 were RWF840 million. The management

board has decided to pay an ordinary dividend (ie a dividend on ordinaryshares) which is 50% of profits after tax and preference dividend.

Required

Show the amount in total of dividends and of retained profits, and calculatethe dividend per share on Ordinary shares.

Answer :

RWFm

Profit after tax 840

Preference dividend (7% of RWF100 u 20, 000,000) 140

Earnings (profit after tax and preference dividend) 700

Ordinary dividend (50% of earnings) 350Retained earnings (also 50% of earnings) 350

The ordinary dividend is RWF7 per share (RWF350 million by 50 million

ordinary shares).

The appropriation of profit would be as follows :

RWFm RWFm

Profit after tax 840

Dividends : preference 140

Ordinary 350

490

Retained earnings 350

As we will see later, appropriations of profit do not appear in the statement ofprofit or loss, but are shown as movements on reserves.

Share capital of the company

Share capital is the amount of money a company raises by selling shares topublic and private sources or investors.

The company act provides that the Memorandum of association must state

the amount of share capital with which the company has to register and thedivision of the share capital into shares of a fixed amount.

The share capital of the company forms the permanent fund in the companyand is reported in the balance sheet.

The investor will then pay for and be issued with the shares and therefore,

they become owners. Each share has a flat value called Par value/face value/nominal value.

Example 1

For example, if a company decides to set up a share capital of RWF 200,000, itmay decide to issue :

200,000 shares of RWF1 each per value. (200,000 x 1=200,000RWF)

100,000 shares of RWF 2 each per value. (100,000 x 2= 200,000RWF)400,000 shares of RWF 0.50 each per value. (400,000 x 0.50=200,000RWF)

Forms of share capital:

The capital of the company is called share capital because it consists of or

raised by selling shares. The following are forms of share capital:

1. Authorized or registered share capital or nominal capital: This is

the maximum amount as stated in the memorandum of association, acompany may raise by selling shares.

For example

If a company wishes to sell 1,000 shares of RWF1,000 each, its authorized

share capital is RWF. 1,000,000

i.e number of shares *price of the share=1,000*1,000=RWF. 1,000,000

2. Issued share capital: This is the value of the shares that have been

issued whether or not the full amount against them has been called up.It is also called Subscribed capital

For example

If the above company has issued 600 shares for sale, the issued share capital

would be RWF. 600,000.i.e number of shares *price of the share=600*1000=RWF600,000

3. Called up share capital: This is the amount that the shareholders have

been asked to pay. When shares are issued or allotted, a company does

not always expect to bepaid the full amount for the shares at once. It

might instead call up only a part of the issue price, and wait until a latertime before it calls up the remainder.

e.g. if the above company has asked its shareholders to pay only 600 RWF pershare, it’s called up share capital would be 600*600 =360,000RWF.

4. Uncalled up share capital: This is the total amount which is to be receivedin future, but which has not been asked for. 600*400=240,000RWF.

5. Paid up share capital: This is the amount that has actually been received

from the shareholders. Like everyone else, investors are not always

prompt or reliable payers. When capital is called up, some shareholders

might delay their payment (or even default on payment). Paid-up capitalis the amount of called-up capital that has been paid.

e.g. in the above case shareholders holding 50 shares have failed to pay a call of200RWF per share, the paid up would be;

Called up 360,000

Less: arrears 10,000

Paid up capital 350,000

6. Calls in arrears: This is total amount which has been asked i.e. (calledfor) but has not yet been paid by shareholders. 50*200=10,000 RWF

7. Minimum share capital: This is the amount stated by the promoters

when making application for registration of the company as the minimumrequired amount to commence trading effectively.

Application activity 6.1

1. What is a share?

2. What is the difference between ordinary and preference shares?

6.2. Accounting and adjustments of shares

Learning Activity 6.2

A company ABC wishes to issue shares as per stated in its memorandum

of Association. The members only know about the market value of shares

and they do not know about other relevant information. They need you as

a professional accountant to give you some clarification such as:

a) Distinguish between a share issues at par, an issue at premium, at

a discount

b) The market value of a share is irrelevant to the company whenpreparing its financial statements.’ Discuss this statement’

6.2.1. Stages on issue of shares

When the company has been registered the following stages should be takenfor the company to be able to collect money from the public by issuing shares :

1. Prospectus.

When a public company plans to raise capital by selling shares to the general

public. A copy of prospectus asks the public to submit an offer to purchasecompany share on or before the date of publication and this copy must be sent

to the registrar of businesses for registration.

It must provide a summary/information of the business, its track/past record,

and the project that the company is issuing shares for. It also includes the

starting and the closing date of the issue of shares, application fee, at the

time of allotment and on calls, name of the Bank for application fee deposit,accepted minimum number of shares to be issued etc.

2. Application

After the public have finished reading and they are satisfied, they can apply to

the company for the purchase of shares on the printed subscribed form. After,

the public sends an application form together with the application money to

specified bank account and receives a receipt. The application money cannotbe withdrawn by the company until the allotment is done.

3. Allotment

Company shares are issued on the understanding that they are payable byinstallments and the following points would be considered;

That when the public apply for shares, they send a sum of money known as

the application money. This is not a guarantee that they will receive shares

and this money can always be refunded to the applicants. At this stage the

directors will send what is known as allotment letters to the successful

applicants. These letters reflect the acceptance of the allotment of shares andthe binding contract now exists between the company and the subscriber.

Finally, the applications and the allotment account must only remain with the

right nominal value expected on application and allotment. The amounts inthese accounts is transferred to shareholder’s share capital account.

Accounting entries made

There are two methods by which accounting entries are made on applicationand allotment :

Method 1

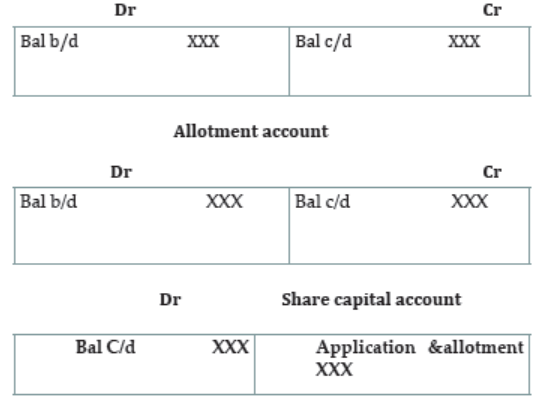

In this first method, application and allotment account should be treated

separately. In this case the application account records, the application money

and allotment account records the money (share capital) from the allottedshares.

Application account

Method 2 :

Here both the application and the allotment account are treated the same andthe accounting entries are the following ;

1. Application money received :

• Debit : Bank account

• Credit : Application and allotment account

2. Application money refund to unsuccessful applicants :

• Debit : Application and allotment account

• Credit : Bank account

3. On allotment of shares

• Debit : Application and allotment account

• Credit : share capital account

4. Allotment money received :

• Bank account

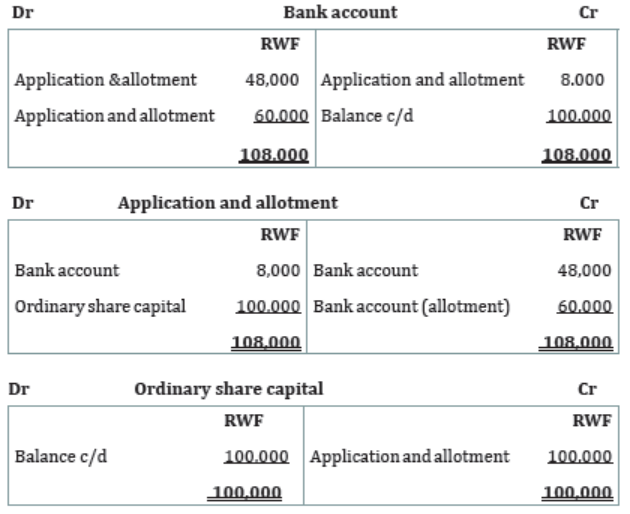

• Credit : Applicant and allotment accountExample

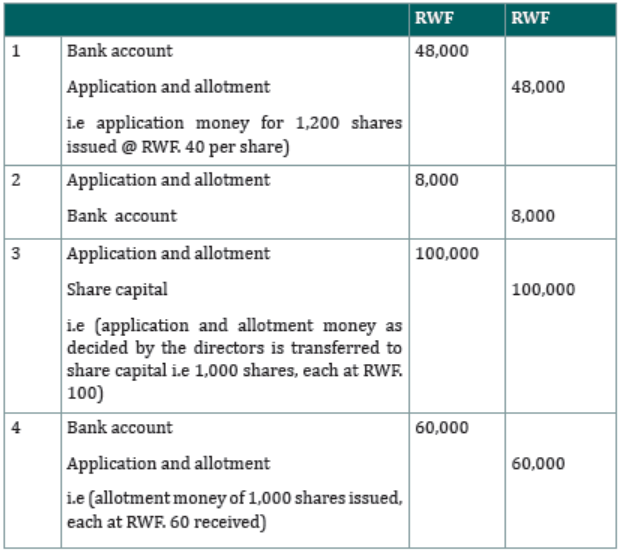

ABC ltd issued 1,000 ordinary shares each at RWF100, payable on the followingconditions ;

– RWF.40 on application

– RWF. 60 on allotment

Applications received were 1,200 shares. On 2nd March, allotment was done and

the excess applicant were returned to the unsuccessful applicants.

Required: Show the journal entries and ledger a/cs to record the above

transactions and extract a balance sheet at 31th March 2021, assuming that thesums of money were received in due time.

ABC LTD

I. The Journal

II. The ledger

6.2.2. Issue of shares

On market shares are sold on the following conditions :

1. At par/nominal value : This is where a share is issue at the price that isstated in the memorandum of association of a Company.

2. At premium : This is where on the market the share is issued at price

above par value of nominal value. In this case a share is issue at a premium

and the amount of the shares is called share premium. If a company

issue shares at a premium, they need to open a separate account called

share premium account that appears in the credit side of the balancesheet.

3. At discount : This is where shares are issued at a price lower than theprice that is stated in the memorandum of association of the Company.

Share premium:

The amount at which the shares are issued may exceed their par value.

Premium means additional cash due to the difference between the issueprice of the share and its par value.

When a company is first set up the issue price of its shares will probably be

the same as their par value and so there would be no share premium. If the

company does well, the market value of its shares will increase, but not the

par value. The price of any new shares issued will be approximately theirmarket value.

For example, 1 : A company might issue 100,000 shares of RWF100 at a

price of RWF120 each. Subscribers will then pay a total of RWF12, 000,000.

The issued share capital of the company would be shown in its accounts at

par value, RWF10, 000,000. The excess of RWF2, 000,000 is described not as

share capital, but as share premium or capital paid-up in excess of parvalue.

Example 2. The difference between cash received by the company and the

par value of the new shares issued is transferred to the share premiumaccount.

i.e if Umucyo Ltd issues 1,000 RWF100 ordinary shares at RWF260 each thebook entry will be :

FRW FRW

DEBIT ; Cash 260,000

CREDIT : Ordinary shares 100,000

Share premium account 160,000

A share premium account is an account into which sums received aspayment for shares in excess of their nominal value must be placed.

Once established, the share premium account constitutes capital of the

company which cannot be paid out in dividends, i.e it is a capital reserve. The

share premium account will increase in value if and when new shares are

issued at a price above their par-value. The share premium account can be

‘used’ – and so decrease in value – only in certain very limited ways, which

are largely beyond the scope of yourbasic financial accounting syllabus.

One common use of the share premium account, however, is to’finance’ the

issue of bonus shares. Other uses of this account may depend on nationallegislation.

The reason for creating such non-distributable reserves is to maintain the capital

of the company. This capital ‘base’ provides some security for the company’s

creditors, bearing in mind that the liability of shareholders is limited in the

event that the company cannot repay its debts. It would be most unjust – and

illegal – for a company to pay its shareholders a dividend out of its base capitalwhen it is not even able to pay back its debts.

Example Share issue

AB Co issues 5, 000,00 at 500RWF for 6, 000RWF million. What are the entriesfor share capital and share premium in the statement of financial position ?

Share capital Share premium

A. 5,000 RWF million 1,000 RWF million

B. 1,000 RWF million 5,000 RWF million

C. 3,500 RWF million 3,500 RWF million

D.2, 500 RWF million 3,500 RWF million

Solution

Price per share is 500 RWF each (ie par value/face value /nominal value) and

shares were issued at 1,200RWF each (ie RWF 6,000m/5 shares). Of this, 500

RWF is the price of the share capital and 700 RWF is share premium price.Therefore, option D is the correct answer.

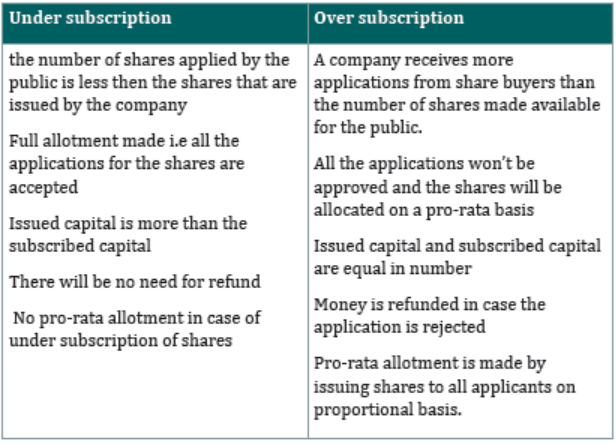

6.2.3. Under and Over subscription of shares

Under Subscription is defined as the situation where the number of shares

applied by the public is less than the shares that are issued by the company.

Companies that have just started or lack a good reputation will experience

under-subscription.

Oversubscription is defined as the situation where a company receives more

applications from share buyers than the number of shares made available for

the public. In simpler terms, oversubscription happens when the demand for

shares exceeds the supply. Oversubscription does not always guarantee a

company’s success, since projected success must happen in order for sharesto remain in high demand.

Differences between under and over subscription

Let’s consider a situation where MBC directors allot to applicants only a

fraction of shares applied for. Following such kind of allotment, the company is

required to refund the applicant money for the fraction of shares that are not

allotted. On the hand, the applicants once allotted some shares, become liable

for payment of the required balance on their allotted shares. Other than refund,

the company therefore retains the un-used applicant money to make paymentagainst the allotment money when it becomes due.

The following are the accounting entries ;

i. On application : record the total value of the application money received

ii. On allotment : successful applicants (applicants who receive a fraction ofshares applied for) will pay allotment money.

Example : MBC ltd. Company offered 100,000 ordinary shares each of 10RWFat a premium of 2 RWF payable in installments.

i. On application 3RWF

ii. ON allotment (including premium) 7RWF

iii. On first call and final 2RWF

12 RWF

Applicants received 130,000shares and the allotment was done as follows ;

Applicants for 80,000 shares- full shares allotted

Applicants for 40,000shares - 20,000 shares allottedApplicants for 100,000 shares - rejected

Excess application money for partially accepted applicants is to be used to

reduce the amount due on allotment. All money due on allotment and first and

final call was received expect 6,000 shares allotted to Mugabo, who failed to payfor the first and final call.

Workings

a) Application money received : 130,000 shares *3 RWF=390,000 RWF,

The number of shares offered are 100,000 less than number

of shares applied for thus ; there is going to be a refund tounsuccessful applicants ie

b) Application refund=30,000 shares*3RWF=6,000 RWF

c) Total value payable on application and allotment=100,000shares

*8RWF=800,000 RWF

d) Excess on application ; 40.000shares applied were allotted 20,000

shares ie20, 000shares *3=60,000RWF

e) Premium cash/money=10,000 shares *2RWF=20,000RWF

f) Received on allotment including premium=allotment due (includingpremium) - Excess application :

100,000shares *7 RWF= 700,000

Less : Excess application= 60,000

640,000

g) Money received on first and final call

94,000 shares *2 RWF= 188,000 RWF

h) Calls in arrears =6,000*2=12,000RWF6.2.4 Forfeiture and reissue of forfeited shares

Forfeiture of shares refers to the cancellation of shares allotted to theshareholders for non-payment.

There are instances in business where a stakeholder loses their share due to

non-payment of their financial liability of installments or dues. The only waya company can forfeit a share is if the firm’s articles of association permit it.

Also, Shareholders whose shares are forfeited lose their shareholder rights andinterests as well as their membership in the organization.

A person whose shares have been forfeited ceases to be a member in respect of

the forfeited shares but remain liable to pay the company all the monies which

at the time of forfeit, were payable. To record forfeit of shares, open a forfeited

shares account. The total nominal value of the shares forfeited is credited to

this account and debited to share capital account. The amount unpaid on theshares in arrears account and debited to the forfeited shares account.

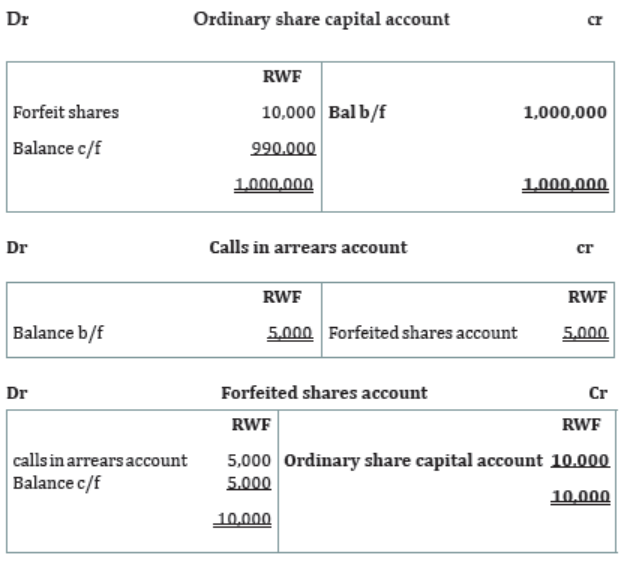

Example

UWUNO Co. Ltd have an authorized capital 1.000,000 RWF divided into 20,000

ordinary shares of 50 RWF issued and fully paid except 200 shares held ofMUCYO on which only 5,000RWF has been paid.

Following many reminders and demands for payment, the board of directorsmade a decision to forfeit the shares held by MUCYO.

Required :

Show the journal entries in the company’s journal and ledger recording theforfeiture of shares.

Solution

Journal entries

Dr Cr

Ordinary share capital account 10,000

Forfeited shares account 10,000

(200 ordinary shares of RWF 50 each forfeited

For non-payment of call as per resolution of directors)

Forfeit shares account 5,000

Calls in arrears account 5,000

(Calls in arrears RWF 25 per share on 200

Ordinary shares forfeited)

Re-issue of forfeited shares

If shares are forfeited the membership of the shareholder stands cancelled and

the shares become the property of the company. Thereafter, the company has

an option of selling such forfeited shares. The sale of forfeited shares is called

‘reissue of shares’

Therefore, re-issue of shares is the selling of forfeited shares. When re-issuing

shares the new purchaser must be pay the shares at the nominal value. if shares

are re-issued at the value above the nominal value, the surplus should go to

share capital account and the following are the necessary accounting entries;

1. Debit : forfeited shares re-issued account

Credit : Share capital account(With nominal value of shares re-issued)

2. Debit : Forfeited shares account

Credit : forfeited shares re-issued account(With amount received before to forfeiture in respect of shares re-issued)

3. Debit : Bank account

Credit : Forfeited shares re-issued account(With amount received on re-issue of forfeited shares)

4. Debit : Forfeited shares re-issued account

Credit : Shares premium account(With the balancing figure on the forfeited shares re-issued account)

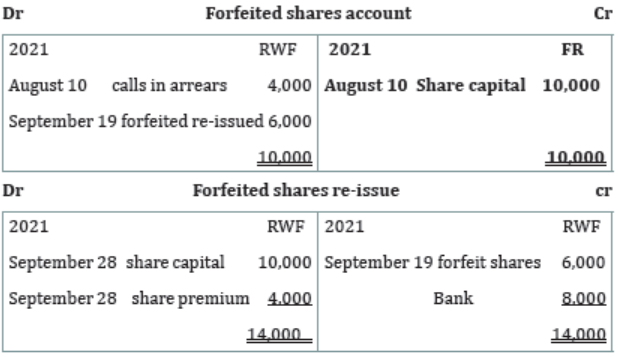

Example

UCOMO Company ltd issued 3,000 ordinary shares of RWF10 at RWF 120 eachas shown below ;

On application RWF 3

On allotment RWF 5 (including premium)

On first and final call RWF 4

Applications were received and the allotment was med to successful applicants.

All the installments were paid expect the first and final call of RWF for 1,000

shares held by MUHIMA whose shares were forfeited on 10th August 2021 andre-issued on 19th September 2021each at RWF 8.

Required :

Show the following accounts as they appear in the ledger

i. Forfeited share account

ii. Forfeited shares re-issued account

NOTE : Ignore completing double entry in the rest of the accounts

Working ;

i. Calls in arrears forfeited =1,000 shares *RWF 4=RWF4, 000

ii. Amount received before forfeiture

Application 1,000 shares *RWF 3=RWF 3,000

Allotment 1,000 shares * RWF3=RWF 6,000

iii. Amount received on re-issue=1,000 shares *RWF 8=RWF8, 000

iv. Nominal value of re-issued shares=1,000shares*RWF 10=RWF10, 000

v. Share premium on re-issue =1,000 shares*RWF2=RWF12, 000Application activity 6.2

1. A company issues five million RWF100 shares at a price of RWF125

per share. How much should be posted to the share premium

account?

A. RWF 5 million

B. RWF 1.25 million

C. RWF 6.25 million

D. RWF 6 million

5. KAMANI co.ltd has the authorized share, 500,000 @ 120RWF

per share, and shares issued were 380,000. The company asked

shareholders to pay 100RWF per share who actually paid 80RWFper share.

Required:

Calculate for the following;

i. Authorized share capital

ii. Issued share capital

iii. Called up share capital

iv. Uncalled share capitalv. Paid-up share capital

End unit assessment 6

1. UTC Ltd. Co.ltd issues 100000 equity shares of face value of 100 RWF

on 1st June 2018 at 20% premium. The arrangements for payment

are:

June 1, 2018: On Application 20RWF

July 1, 2018: On Allotment including Premium 70RWF

September 1, 2018: On First and final call 30RWF

The company receives applications for 285000 shares. This is a case of

oversubscription. It deals with them in the following manner:

1. Applicants for 25000 shares receive a full allotment.

2. The applicants for 225000 shares receive one share for every three

shares applied for on pro-rata basis.

3. It rejects the applications for 35000 shares.

The company duly receives the entire amount. Pass necessary journalentries.

REFERENCE

Jin, Z. (2010). Accounting for nonprofit organizations : a case study of BritishRed Cross (Master’s thesis).

Belverd E.D. (2011). Principles of Financial Accounting (11th edition). USA:Cengage learning.

Donna, R.H., Charles. T., Sundem, G.L., Gary L. & Elliott, J. A. (2006). Introductionto Financial Accounting (9th edition). Prentice-Hall.

Asiimwe, H. M. (2009). Mk Fundamental Economics. Kampala: MK PublishersLtd.

ICPAR (2018). Certified Accounting Technician (CAT) Stage 1, Recording FinancialTransactions (First edition). London: BPP Learning Media Ltd.

ICPAR (2018). Certified Accounting Technician (CAT) Stage 2, Preparation ofbasic accounts (First edition). London: BPP Learning Media Ltd.

ICPAR (2018). Certified Accounting Technician (CAT) Stage 3, FinancialAccounting (First edition). London: BPP Learning Media Ltd.

Kimuda, D. W (2008). Foundations of accounting. kampala: East AfricanEducation Publishers Ltd.

Marriot, P., Edwards, J.R., & Mellet, H.J (2002). Introduction to accounting (3rdedition). London: Sage publications.

Mukasa, H. (2008). New Comprehensive Accounting for Schools and Colleges(first edition). Kampala.

Needles, B. E. (2011). Principles of Financial Accounting. Northwestern: CengageLearning.

Omonuk, J.B. (1999). Fundamental Accounting for Business: Practical Emphasis.

Makerere Universty of University of Business School, Kampala: Joseph BenOmonuk.

Roman, L.W., Katherine, S. & Jennifer, F. (2010). Financial Accounting: An introductionto concepts, methods, and uses (14th edition). USA: Cengage Learning.

Saleemi, N.A. (1991). Financial Accounting Simplified. KENYA.

Sangster, F. W. (2005). Business Accounting. London: Prentice Hall.

Uwaramutse, C. (2019). Financial Accounting I. University of Lay Adventist of

Kigali (UNILAK). Kigali.

Weygandt, J.J, Kimmel, P.D. & Kieso, D.E. (2009) Accounting Principles (9thEdition). USA: John Wiley & Sons.

Wood, F. & Sangster, A. (2005). Business Accounting 1 (10th edition). UK: Prentice-Hall.

Wood, F. & Sangster, A. (2005). Business Accounting 2 (10th edition). UK: Prentice-Hall.