Topic outline

Unit 1 YEAR - END ADJUSTMENTS

Key unit competence: To be able to carry out adjustments and preparean adjusted trial balance

Introductory activity

Regardless of the type of the business or the accounting system used, it

is not possible to keep all accounts up to date at all times. At the end of

each financial year, some accounts must be updated by adjusting entries.

Adjustments or provisions are normally made for bad and doubtful

debts, depreciation, prepaid expenses and income, accrued expenses

and income, provisions are also made for corporation taxes payable and

for appropriations such as payment of dividends or proposed dividends,transfers to reserves etc.

After adjusted recorded entries and affected accounts in the adjusted trial

balance, the accounts will reflect the current status of the organization andfinancial statements can then be prepared.

1. Why do businesses make adjustments?

2. List at least four types of transactions that may be the cause of theadjustment

3. How does an adjusted trial balance differ from an unadjusted trialbalance?

1.1.Closing stock

Learning Activity 1.1

During a given period of time, the business purchases items for reselling

them to different customers. By the end of this time some unsold items are

remaining in the store.

a) What is the accounting terminology for goods not yet sold at

reporting date?b) What is their use in determining the cost of goods sold?

1.1.1.Meaning of the closing stock

Closing stock is the amount of inventory that a business still has on hand at

the end of a reporting period. This includes raw materials, work-in-process,

and finished goods inventory. Certain items charged to expense as incurred,

such as production supplies, are not considered to be part of closing stock.

The amount of closing stock can be ascertained with a physical count of

the inventory. It can also be determined by using a perpetual inventory

system and cycle counting to continually adjust inventory records to arrive

at ending balances.

The amount of closing stock (properly valued) is used to arrive at the cost of

goods sold in a periodic inventory system with the following calculation:

Opening stock + Purchases - Closing stock = Cost of goods sold

The opening stock for the next reporting period is the same as the closing stock

from the immediately preceding period.

There are a variety of methods available for calculating the recorded value of

closing stock, including the methods noted below:

• First in, first out method (FIFO)

Under the first in, first out method, the costs of all separately-purchased goods

are stored in cost layers. When a unit is sold, the cost of the oldest item in

inventory is assigned to it. Assuming inflation is present, this tends to result in

a lower cost of goods sold, and therefore more reported profits.

• Last in, first out (LIFO)

Under the last in, first out method, the costs of all separately-purchased goods

are stored in cost layers. When a unit is sold, the cost of the newest item ininventory is assigned to it. Assuming inflation is present, this tends to result in

a higher cost of goods sold, and therefore lower reported profits.

• Weighted average method

Under the weighted average method, the costs of all separately-purchased

goods are combined to create a weighted-average cost. Since it results in an

average cost, it tends to result in reasonable cost of goods sold and profit

figures, irrespective of the inflation rate.

1.1.2. Determine the use of closing stock

Inventory system

For merchandising firms, an initial step in assessing profitability is gross profit

(also called profit margin or gross margin), which is the difference between

sales revenues and cost of the goods sold. When they sell the goods, the cost

of the inventory becomes an expense, cost of goods sold or cost of sales, in the

income statement. We deduct this expense from net sales to determine gross

profit, and we deduct additional expenses from gross profit to determine netincome.

Methods of recording stock (Inventory system)

There are 2 main methods of recording stock. These are: periodic method andperpetual method.

a) Perpetual inventory system

Perpetual inventory system or method is the method that consists to keep a

continuous record of inventories and cost of goods sold. This daily record helps

managers to control inventory levels and prepare interim financial statements.

Perpetual inventory: It is a system of stock maintenance consisting in

continuous taking of stock flows so to provide at any time the stock in tradeand cost of sales.

In the perpetual inventory system, the journal entries are:

• When inventory is purchased:

Merchandise inventory…………..xxx

Accounts payable (creditors) or cash …………xxx

• When inventory is sold:

Accounts receivable (debtors) or cash…yyy

Sales revenue…………………………………………….yyy

Cost of goods sold…………………………….xxxInventory……………………………………………xxx

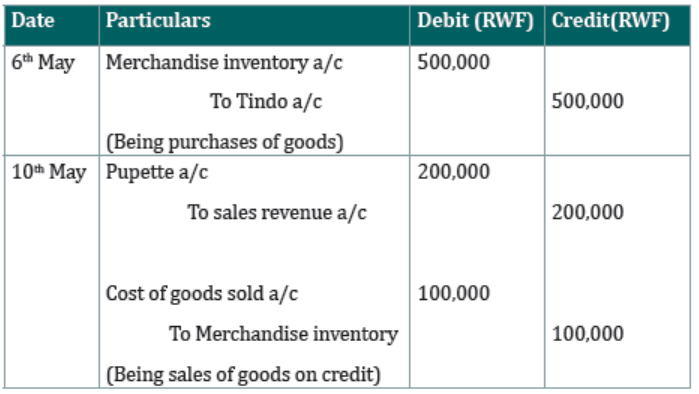

EX: On 6th May, Sosso purchases some merchandises for RWF 500 000 from

Tindo, and agrees to pay for them within the next two weeks. On 10th May,

goods which had cost RWF100 000 were sold on credit to Pupette for RWF 200000. Show journal entries to record the above transaction.

a) Periodic inventory system

Periodic inventory system or method does not involve a day-to-day record of

inventories or of the cost of goods sold. Instead, we compute the cost of goodssold and an updated inventory balance only at the end of an accounting period.

Physical count:

It is the process of examining and identifying all items in inventory. The

physical count allows management to remove damaged or obsolete goods from

inventory and thus helps reveal inventory shrinkage, which refers to losses of

inventory from theft, breakage and loss. Under the periodic inventory method,we delay computing cost of goods sold until we make a physical count:

Beginning Inventory + Purchasing – Ending Inventory = Cost goods sold Goodsavailable for sale – Inventory left over = Cost of Goods Sold

Beginning inventory: Are the goods (products) which are remained at the endof last period

These are goods that we have in our store when we begin the period.

Example ones:

Opening stock: RWF 12,000,000

Periodical Purchasing: RWF 20,000,000

Closing stock: RWF 10,000,000

Calculate: inventory available for sale and cost of goods sold

Solution:

Inventory available for sale = Opening inventory + Purchasing = RWF 12,000,000

+ RWF 20,000 000 = RWF 32,000,000

Cost of goods sold: Opening inventory + purchasing – closing inventory

= RWF 12,000,000 + RWF 20,000,000 – RWF 10,000,000 = RWF 22,000,000

Or: Goods available for sale – Closing inventory = RWF 32,000,000 – RWF

10,000,000 = RWF 22,000,000.

Example two:

Compute the following:

Closing stock: Cost of goods available for sale – Cost of goods sold

Cost of goods available for sale: Opening stock + net purchases

Net purchase: (purchases-purchases returns) + carriage inwards

Purchases…………………. 200,000

Opening stock………….…100,000

Cost of goods sold………...180,000

Purchases return……………50,000

Carriage inwards……….…. 20,000

Solution:

Opening stock…………………………………………….…100,000

Purchases………......................................200,000

Less: Purchases return……………………… (50,000)

150,000

Add: Carriage inwards………………………...20,000

Net purchases………………………………………………. 170,000

Cost of goods available for sale……………….………. 270,000

Less: Cost of goods sold…………………………...........(180,000)

Closing stock…………………………………...…….………90,000

Example three:

Cost of goods sold (C.G.S):

Cost of goods available for sale – Closing stock

Purchases………………....340,000

Opening stock………….…150,000

Closing stock…….………...80,000

Purchases return……………70,000

Carriage inwards……….…. 30,000

What is the cost of goods sols?

Solution:

Opening stock…………………………………………….…150,000

Purchases………............................340,000

Less: Purchases return……………… (70,000)

270,000

Add: Carriage inwards……………..30,000

Net purchases…………………………………………. …. 300,000

Cost of goods available for sale…………………………. 450,000

Less: Closing stock…….………….…………………….... (80,000)

Cost of goods sold...………………………………………..370,000

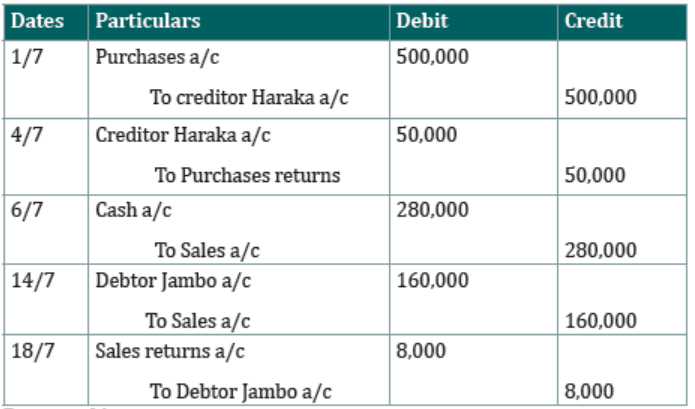

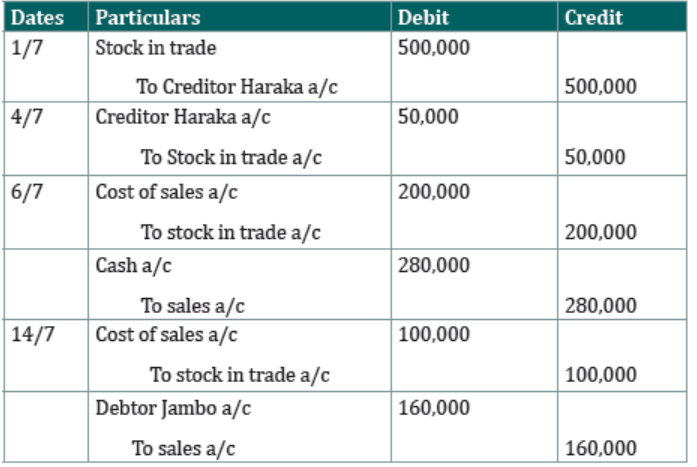

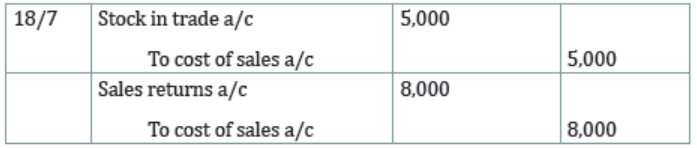

Illustration

– July 1: Goods purchased from Haraka RWF 500,000 (1,000 units at

RWF 500 each).

– July 4: 100 units of goods costing RWF 50,000 are returned to the

supplier being defective.

– July 6: Sold 400 units for cash at RWF700 each.

– July 14: Sold 200 units at RWF 800 each to Jambo on credit.– July 18: Jambo returned 10 units being poor in quality.

Required: Prepare journal entries of the above transactions using periodicand perpetual inventory

Answer:

Periodic inventory

Perpetual inventory

In trading account, when the perpetual inventory is used, the cost of sales is

available without using the formula: Cost of Goods Sold = Opening Stock + Net

Purchases-Closing Stock. One of the advantages of the perpetual inventory is asimple detection of thefts and losses in stock.

Application activity 1.1

1. Define the closing stock

2. How is it used in determining the cost of goods sold?

3. What are the different methods applied for calculating the recordedvalue of the closing stock?

4. Answer by yes or no:

• The opening stock for the next reporting period is the same as the

closing stock from the immediately preceding period.

• The closing stock for the next reporting period is the same as the

opening stock from the immediately preceding period.

• The opening stock from the immediately preceding period is the

same as the closing stock for the next reporting period

• The opening stock for the next reporting period is the same as theopening stock from the immediately preceding period.

1.2. Bad and doubtful debts

Learning Activity 1.2

In large businesses, most of transactions are made on credit basis. Due to

various reasons, the outstanding amounts in debtor accounts are likely

not to be collected fully or partly and then, the book keeper has a task of

providing for this unknown liability:

a) State any two reasons why a debt may be irrecoverable?

b) What can you do if someone who owes you money informed youthat he/she will not pay due to insolvency?

Introduction on bad debts

Bad debt refers to the sum due from the debtors, which remains unrealized,

and so they are written off in the company’s books of accounts. As against,

doubtful debts refer to the debt, with which there is an uncertainty, as to thedegree to which amount will be recovered from the debtor.

Bad debts are incurred when it is reasonably certain that a debtor to a business

will not be paying. For example, the debtor’s business may itself have collapsedleavingno funds in which to pay its obligations.

You should treat bad debts in the same manner as any other expense. In other

words, we pass a journal entry where bad debts are debited, and debtor’saccount is credited.

Doubtful debts, in addition to bad debts, you may also be required to account

for doubtful debts. In practice, businesses have learnt from experience that

some debtors will not pay, but they are not certain which debtors this appliesto at the end of the year.

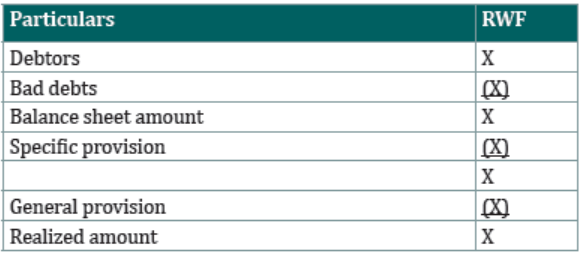

Provision for doubtful & bad debts

The provision for doubtful debts is an estimated amount of bad debts that are

likely to arise from the accounts receivable that have been given but not yet

collected from the debtors. This is subtracted from the trade receivables figure

on the balance sheet so as to give a more realistic figure for the amounts likelyto be collected. It is similar to the allowance for doubtful accounts.

Provision is an amount set aside for a probable loss of receivables which cannot

be calculated with absolute accuracy. When a debtor becomes bad / doubtful, aprovision for bad debt is to be created.

Reasons for bad and doubtful debt

1. Failure to pay despite persistent reminders

2. Death of a debtor

3. Bankruptcy of a debtor

4. Default by debtor5. Etc

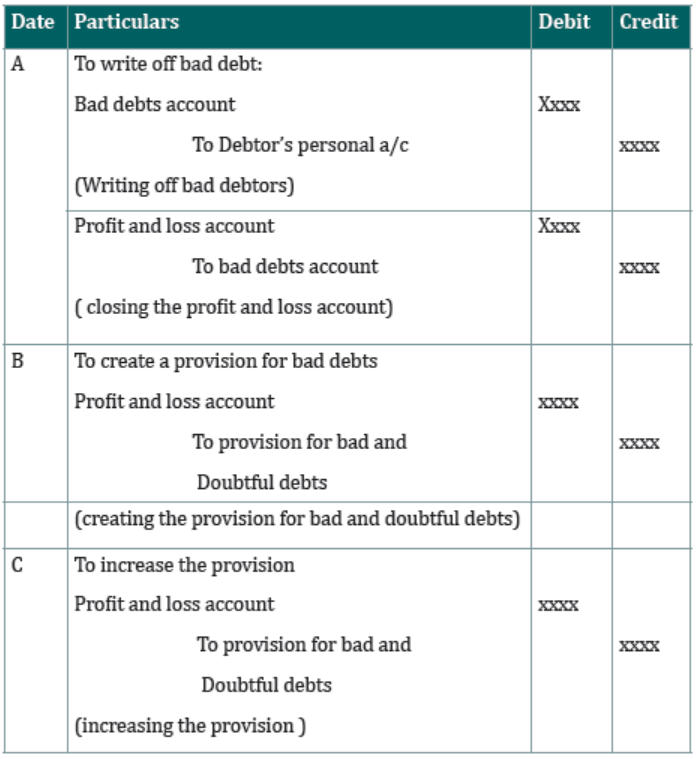

Creating provision for bad and doubtful debts

Provision for bad debts should be created for all those accounts that have a highpossibility of not being collected. For example, a company has debtors totaling

RWF 5,000,000 but 10% of them are doubtful and are likely not to pay. If it is

the 1st year of trading (1st year of making provision), a provision for bad anddoubtful debts should be created by making the following entry:

Dr: Bad and doubtful debts expense A/C 500,000

Cr: Provision for bad and doubtful debts A/C 500,000

Bad and doubtful debts account above is sometimes simply referred to as baddebts expense account.

A provision for doubtful debts can either be for a specific or general provision.

A specific provision is where a debtor is known and chances of recovering the

debt are low. The general provision is where a provision is made on the balanceof the total debtors i.e. debtors less bad debts and specific provision.

Writing off a bad debt

In some cases, the debtors who were once doubtful truly become bad and

their amounts are irrecoverable. Their accounts have to be written off. The

accounting entry to write off a debt for which a provision had been created,using the above example:

Dr Provision for bad and doubtful debts A/C RWF 500,000

CR Debtor’s A/C RWF 500,000

Direct write off of a bad debt

For small debtor’s amounts or receivables, there is no need to create a provision

for bad debts, a direct write off can be made to the profit and loss A/C. For

example, Jane deals in sale of stationery items, she sold a pen to John for RWF

10,000 on credit but John has defaulted and is not likely to pay.The accounting entry to write off the small amount is as follows:

Dr Profit and Loss (P&L) A/C (bad debts) 10,000

Cr Debtor’s A/C (John’s A/C) 10,000

Increasing the provision for bad debts

At times the provision for bad debts might have to be increased beyond the

current provision i.e. in the subsequent periods. For example, if the current

provision for bad debts is RWF 2,000,000 but has to be increased to RWF3,000,000.

The accounting entry is as follows:

Dr Bad debts expenses A/C 1,000,000

Cr Provision for bad debts A/C 1,000,0000

The accounting entry is performed with the difference ie. RWF 3,000,000 –RWF 2,000,000 = RWF 1,000,000

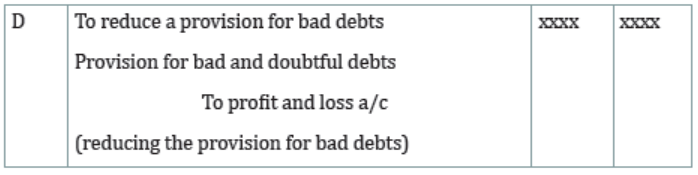

Decreasing the provision for bad debts

If debtors start pa and there is little doubt about the amounts being collected,

a provision for bad debts which was once high can be reduced. For example, a

provision of RWF 5,000,000 had been made against bad debts; the provision isnow to be reduced to RWF 3,000,000.

Accounting entry is as follows:

Dr provision for bad debts A/C 2,000,000

Cr Profit and Loss A/C (Reduction in bad debts provision) 2,000,000

Collecting a bad debt that had been written off

An account that had been written off as irrecoverable, or bad can be collected

at a future date may be after 2 or more years. For instance, Mary sold goods

to Joseph for RWF 10,000,000 on credit. Joseph failed to pay and disappeared

for long time and was subsequently written off by Mary as a bad debtor.

Surprisingly after 5 years, Joseph surfaced and paid Mary by cheque in fullsettlement of his debt.

The accounting entries to record the above are as follows:

The first step is to reinstate Joseph as a debtor and the following entry is made:

Dr Debtor’s (Joseph’s A/C) 10,000,000

Cr Bad debts recovered A/C 10,000,000

The second step is to record the receipt of a cheque using the following entry:

Dr Bank A/C 10,000,000

Cr Debtors A/C (Joseph’s A/C) 10,000,000

The third step is to close the bad debts recovered A/C to the profit and loss A/Cby using the following entry:

Dr Bad debts recovered A/C 10,000,000

Cr Profit and Loss A/C 10,000,000

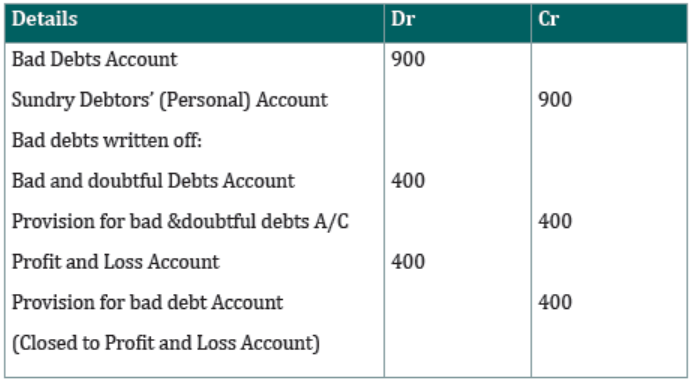

The following journal entries illustrate the points discussed above:

Example

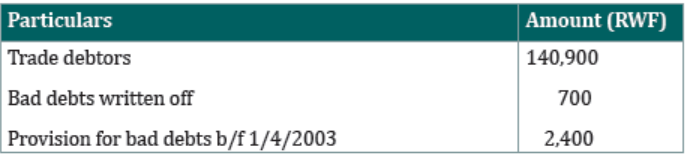

The following information related to trade debtors in the books of Joel, a retailer,at 31st March 2004.

A further RWF 900 is to be written off as an additional bad debt while the

provision for bad debts is to be adjusted to 2% on the remaining balance of

debtors. The accounting book closes each year on 31st March.

Required: Record the above information in Joel’s journal and ledger.

Solution:

Joel

Adjusting Entries-Journal

Application activity 1.2

1. State any two reasons why a debt may be irrecoverable

2. What does the supplier do when it is confirmed that the customer

will not settle his/her account?

3. State the respect steps to adjust the provision for bad and doubtful

debts4. Distinguish bad debts from doubtful debts

1.3. Prepayments and accruals

Learning Activity 1.3

By the end of the reporting period, some expenses and income may be

incurred/occurred but not yet paid or received. On the other hand, some

expenses and income may be paid or received but not yet occurred or

incurred.

1. State some reasons why expenses or income may be incurred /

occurred by the end of the reporting period but remain unpaid oruncollected

1.3.1. Accruals

Accruals are revenues earned or expenses incurred that impact a company’s

net income on the income statement, although cash to the transaction has not

yet changed hands. Accruals also affect the balance sheet, as they involve noncashassets and liabilities

a) Accrued expenses/outstanding expenses

The expenses incurred in one financial year but not paid until the next financial

year, are called accrued expenses.

– They are added to the expenses actually paid– In the balance sheet they appear as current liabilities (CL)

Accounting entries

Dr Profit and Loss account or respective Expenses account

Cr Accrued expenses account

For instance, a company’s financial year ends on 31st December. During a

particular financial year, December salaries totaling RWF 4,000,000 could not

be paid until January the following year. Record the adjusting entry at the endof the financial year for the accrued salaries.

Dr Salaries A/C 4,000,000

Cr salaries payable A/C 4,000,000

Instead of using the word salaries payable, accrued salaries could have beenused.

b) Accrued income/ incomes outstanding

Income earned in one financial year but not received until the following

financial year is called accrued income. It is treated as a current asset in thebalance sheet.

– Incomes outstanding are added to incomes actually received for the

period.

– Accrued income is a current asset in a balance sheet.

Accounting entries:

Dr Accrued income A/C

Cr Profit and Loss or respective Income received or gain A/C

For instance, Peter offered consultancy services to a client and invoiced him

RWF 3,000,000 but the client could not pay in the financial year and promised

to pay in the next financial year. Record the adjusting entry for the consultancyfees which accrued at the end of the financial year.

Dr consultancy fees receivable A/C (Debtor’s A/C) 3,000,000

Cr Consultancy fees (revenue/income) A/C 3,000,000

Illustration

1. Monthly rent of A&B stores is RWF 4,000. Rent paid during the year

amounted to RWF 40,000. Show the entries in Rent Account and Profitand Loss Account as at 31st December.

Answer:

Entries in rent account and profit and loss account:

Dr: Rent account/profit and loss account 48,000

Cr: Cash/bank account 40,000

Cr: Accrued rent account 8,000

Or:

Dr: Rent account/profit and loss account 40,000

Cr: cash/bank account 40,000

Dr: Rent/ profit and loss account 8,000

Cr: Accrued rent account 8,000

1.3.2. Prepayments

Prepayment refers to paying off an expense or debt obligation before the due

date. Often, companies make advance payments for expenses as well as goodsand services to shed their financial burden.

a) Prepaid expenses/ expenses paid in advance or unexpired values

These are expenses paid in advance. Adjustment must be made for expenses

that are paid in one financial year but benefit the next/following financial year.

• Such expenses are deducted from the period’s expenses in the profit

and loss account• Expenses in advance are current assets (CA) in the balance sheet.

Accounting entries:

Dr: prepaid expenses account

Cr Profit and Loss Account or respective Expenses account

Example 1

Rent of RWF 3,000,000 cash was paid on 1st January 1999 to cover a period to

31st March 2000 (15 months). Record the adjusting entry for the prepaid rentat the end of the financial year on 31st December 1999.

Monthly rent payment = RWF 3,000,000/15= RWF 200,000

Since the financial year is 12 months and the rent had been paid for 15 months’rent spills to the following financial year and is called prepaid rent.

Prepaid rent = 200,000 × 3 = RWF 600,000

Adjusting entry for the prepaid rent is as follows:

Dr: Prepaid Rent A/C 600,000

Cr: Rent 600,000

Prepaid rent of RWF 600,000 will appear in the balance sheet as an asset whilein the income statement, the rent expense will be RWF 2,400,000

i.e: RWF 3,000,000 – RWF 600,000

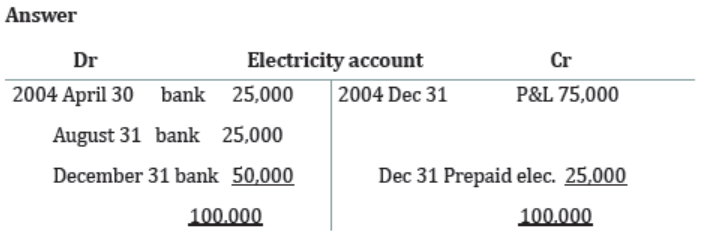

Example 2

During 2004, electricity is paid RWF 25,000 every 4 months. An excess of RWF

25,000 has been made as a prepayment, and thus it is paid and therefore carriedforward to the next year. Show the electricity account

b) Prepaid income/ income received in advance

Some businesses receive income before it is earned. For instance, it is a common

practice in Rwanda for landlords or land ladies to ask tenants to prepay or pay

rent in advance for 2 years, 3 years etc. Adjustments must be made for that

income which was received but services were not offered to the customer.

Unearned income is treated as a current liability in the balance sheet.

– The incomes received in advance are subtracted from the incomes for

the period in income statement

– In the balance sheet, income in advance is short term liability.

Accounting entries:

Dr: Profit and Loss A/C or Income received account

Cr: Income received in advance or respective income or gain A/C

Example

A tenant was made to pay rent of RWF 1,800,000 cash for the period of 1 ½years.

Required:

– Journalize the entries when the rent was paid

– Journalize the adjusting entry at the end of the financial year (1st 12months)

Answer:

i. Dr Cash A/C 1,800,000

Cr Unearned rent Income A/C 1,800,000

Monthly rent payment = RWF 1,800,000/18 =RWF 100,000

Rent earned for the year =RWF 100,000 × 12 = RWF 1,200,000

The following entry is then performed to recognize the income which wasunearned but has now been earned.

ii. Dr: Unearned rent income A/C 1,200,000

Cr: Earned rent income A/c 1,200,000

Application activity 1.3

1. Distinguish prepaid income from prepaid expenses

2. How do accrued expenses differ from accrued income?

3. Answer by yes or no:

• Accrued income is a current liability

• Accrued expense is a current asset

• Prepaid income is a current liability

• Prepaid expense is a current asset

• To adjust for accrued expenses, debit the amount outstanding to the

respective expenses account and credit it to the liability account.

4. Insurance of RWF 4,000,000 had been prepaid cash for 2 years. At

the end of the 1st year half of the prepaid insurance had expired orgot used up.

Required: Record the adjusting entry at the end of the first financialyear.

1.4. Depreciation for non-current assets

Learning Activity 1.4

Non-current assets may be characterized as assets that will generate

economic value for one or more fiscal periods into the future. For example,

consider a business that owns manufacturing equipment; an effective

management team will use that equipment to manufacture products for as

long as it is safe and practical to do so. The economic benefit materializes

in the future when those products are sold to generate revenue and then,

these assets decrease their original value progressively.

a) State the causes why a fixed asset decreases its valueb) How do they call this decrease in value of an asset?

1.4.1. Meaning of depreciation

Depreciation is the loss of value sustained by non-current asset over its lifetime

in the business. Depreciation of fixed assets is an accounting term that is

used to represent how much of an asset’s value has been used up over

time. Depreciation is therefore a calculated expense, which leads to a decrease

in earnings. Depreciation is an expense to the business even if it does not

necessarily involve cash outlay. It is prudent to charge depreciation annually tothe profit and loss account.

1.4.2. Causes of depreciation

Depreciation on non-current assets is caused by:

a) Wear and tear

b) Passage of time

c) Obsolescence

d) Physical factors

e) Economic factors

1.4.3. Reasons for providing depreciation

Once a decision is made to depreciate an asset, the amount of depreciation

written off is transferred to the profit and loss account as an operating expense

for the period. Depreciation is debited to the profit and loss account for theperiod thus reducing current profits otherwise profit will be overstated.

Provision for depreciation is made for the following reasons:

a) It ensures that revenues recognized during a particular accounting

period bear the full cost of the permanent resources used up duringthe same period,

b) It allocates the depreciable amount of an asset over its useful life,

ensuring that each accounting period bears part of the depreciationexpense,

c) It provides a meaningful base of valuation and disclosure of noncurrentassets in financial statements,

d) It ensures that provision is made for the loss sustained by non-currentassets.

e) It ensures availability of tax benefit

1.4.4. Factors for depreciation

• Cost of the asset: purchase cost + transportation Cost (if any) +

installation costs (if any) + other costs that should be capitalized.

• Estimated useful/economic life of an asset: this refers to the period

during which an asset is expected to serve the business.

• Scrap/residual value/ estimated salvage: the estimated amount that

the owner of a fixed asset expects to receive at the time of disposing offthe asset.

1.4.5. Methods of charging depreciation

There are four (4) different methods of calculating the depreciation:

a) Straight line method

A fixed amount of depreciation is charged on the non-current asset, over its

useful life, from the date of its acquisition. The useful life is the estimated life

of the asset will remain in the business. Depreciation charge is calculated as a

fixed percentage on the cost of the asset each year, until it is completely writtenoff. This method is also known as the fixed instalment method.

Annual depreciation is calculated as under:

Or, depreciable value × depreciation rate

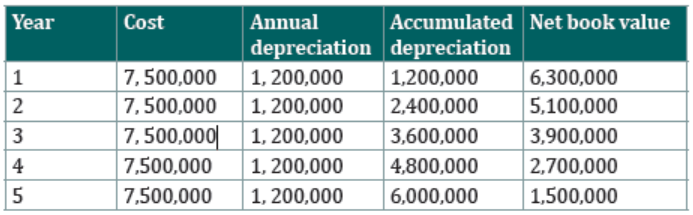

Illustration:

A motor vehicle was purchased from Japan at Cost, Insurance and Freight (CIF)

Mombasa at a value of RWF 5,000,000. It costs RWF 500,000 to transport the

vehicle from Mombasa to Kigali. Total taxes paid on the purchases transaction

of the vehicle amounted were to RWF 2,000,000. The vehicle is expected to beused for 5 years, the end of which it will have a scrap value of RWF 1,500,000.

Required:

a) Calculate the depreciation expense for each year and expense for each

year and accumulated depreciation to year 5b) Draw up the depreciation schedule

Solution

Total cost of the vehicle up to Kigali: RWF 5,000,000 + RWF 500,000 + RWF

2,000,000 = RWF 7,500,000

Scrap/salvage/residual value: RWF 1,500,000

Number of years of useful life: 5 years

Depreciation expenses are thus calculated:

Depreciation per annum could be expressed as a percentage of depreciable cost

as follows:

=1,500,000/6,000,000*100=25%

The depreciation schedule looks like:

b) Reducing balance method (Diminishing or declining balance

method)

It is also known as declining or diminishing balance method. An appropriate

percentage is applied to the net value of the non-current asset brought forwardto obtain the depreciation expense for the period.

Depreciation is therefore calculated as a constant proportion of the book

value (cost less depreciation) of the asset after deducting the total amount of

depreciation expense previously written off. As the depreciation is calculated

on the reduced balance of the asset brought forward, it declines the asset over

the years the asset is retained in the business, hence the name reducing balancemethod.

A gradual decreasing amount of depreciation charge is recorded on the asset

over the years as a constant percentage is being applied to a decreasing bookvalue of the asset.

The depreciation rate (expressed in percentage) is found as under:

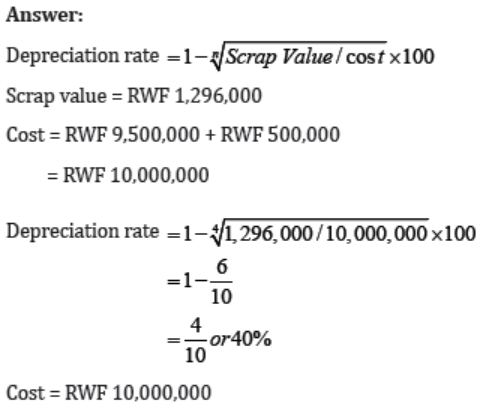

Illustration:

A machine was bought at a cost of RWF 9,500,000. Installing the machine before

use cost of RWF 500,000, scrap value is expected to be RWF 1,296,000 at theend of estimated life of 4 years.

Required: calculate depreciation expense and accumulated depreciation at theend of each year using normal reducing balance method.

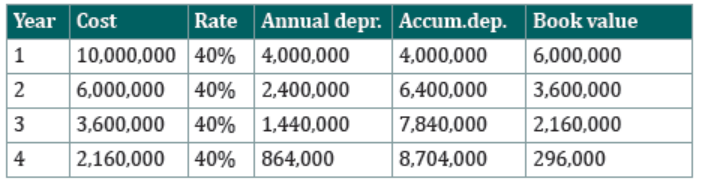

c) Sum of years method or digital method

Under this method, the depreciation charge is calculated by applying a givenrate on the depreciable value until it is completely written off.

Example:

Let a fixed asset having a useful life estimated at five (5) years, its annualdepreciation rates are calculated as follows:

Sum of years: 1+2+3+4+5 = 15

• Rate of the period one: 5/15

• Rate of the period two: 4/15

• Rate of the period three:3/15

• Rate of the period four: 2/15• Rate of the period five: 1/15

Illustration:

A fixed asset was bought at a cost of RWF 8,000,000, has estimated salvagevalue of the RWF 800,000 and estimated useful life of four years.

Calculate the depreciation expense for each year using sum of years/digitsmethod.

Solution

d) Unit of production method

Unit of production depreciation, also called the activity method, calculates

depreciation based on the unit of production and ignores the passage of time

over the useful life of an asset; in other words, a unit of production depreciation

is directly proportional to production. It is mainly used in the manufacturing

sector.

The value of the same asset may be different due to its usage. For example, one

asset, X, produces ten units, and another asset, Y, produce 20 units. Both are the

same asset, but the depreciation of Y will be higher as compared to the X asset

because of more units produced.Under this method:

Where the depreciation rate changes period by period depending on the annual

production and then, it is calculated as under:

Annual depreciation rate = annual production/total production

And the annual depreciation is found as under:

Depreciable value * annual depreciation

Illustration:

1. A plant costing RWF 110 million was purchased on April 1st, 2020.

The salvage value was estimated to be RWF 10 million. The expected

production was 150 million units. The plant was used to produce

15 million units till the year ended December 31, 2020. Calculate thedepreciation on the plant for the year ended December 31st, 2020.

Solution:

Depreciation = (15/150) × ( RWF 110 million – RWF 10 million) = RWF 10million

2. A coal mine was purchased by X Corporation for RWF 16 million. It was

estimated that the mine has capacity to produce 200,000 tons of coal.

The company extracted 46,000 tons during its first year of operation.Calculated the depreciation.

Solution:

Depreciation = (46,000/200,000) × RWF 16 million = RWF 3.68 million

Working hours method:

Depreciation is computed based on the number of hours the asset is expected

to run in its useful life.

Depreciation expense = (number of hours worked in the year/estimatednumber of working hours in productive life) × (cost-salvage value).

Example

A machine costs RWF 400,000 with a salvage value of RWF 20,000. Its useful

life is six years. In the first year, 4000 hours, in the second year, 6,000 hours and

8,000 hours on the third year. The expected flow of the machine is 38000 hoursin six years. What is the depreciation at the end of the second year?

Solution

a) Solve for the depreciation per hour

Depreciation per hour = (FC - SV) / Total number of hours

Depreciation per hour = (400,000 - 20,000) / 38000Depreciation per hour = 10

b) Solve for the depreciation at the end of 2nd year

Depreciation = 10 (6,000)Depreciation = RWF 60,000

Application activity 1.4

1. Define the depreciation

2. Give some four causes for depreciation

3. What are the depreciation methods?

4. A firm bought a machine for RWF 3,200,000. It is to be depreciated at

a rate of 25 per cent using the reducing balance method. What wouldbe the remaining book value after 2 years?

a) RWF 1,600,000

b) RWF 2,400,000

c) RWF 1,800,000

d) Some other figure

5. A machine costs RWF 400,000 with a salvage value of RWF 20,000.

Its useful life is six years. In the first year 4000 hours, in the second

year 6000 hours and 8000 hours on the third year. The expected flow

of the machine is 38000 hours in six years. What is the depreciationat the end of the second year?

1.5. Disposal of non-current asset

Learning Activity 1.5

KEZA Company Ltd, a manufacturer, holds a machine purchased 4 years

ago. The machine with the useful life estimated at 10 years is depreciated

annually under reducing balance method. The machine is no longer

appropriate to company manufacturing and it is decided to replace the old

machine by a new one which is appropriate.

1. What will the company do with the old machine?2. What will happen in the books of account?

Introduction

The usual way of disposing of a non-current asset is by sale though an

asset could be disposed by donation, trade-in, damage, etc. Whatever

approach is used the non-current asset account in respect of the asset sold

must be eliminated from the books to record the fact that such an asset no

longer forms part of the net worth of the business. Also, the accumulated

depreciation on the asset being disposed must be eliminated from theprovision for depreciation account.

Disposal or sale of fixed asset is not defined as a sale in accounting and should

not be credited to the sales account if the asset was bought with no intention

of selling to make a profit. Credits are made to sales account for the sale of

those goods that were bought with the prime intention of selling them and thedomain of the business is in sale of such goods or assets.

Sale or disposal of fixed assets is not routine but incidental. It should be noted

that it is only the gain on disposal of fixed assets that is credited to the profit

and loss account as miscellaneous income while the loss on disposal is debitedto the profit and loss account as an expense.

Gain/loss on disposal=sale/disposal amount-book value

N.B. If sale or disposal amount is greater than the book value a gain on disposal

results and if the sale or disposal proceeds’ are less than the book value, the nitis a loss on disposal

Accounting entries for a disposal transaction

Recording a disposal transaction requires a series of entries as follows:

1. On a fixed asset disposal account and credit that account and debit that

account with the cost of fixed asset disposed off. A credit is made to thefixed asset account for fulfilment of double entry.

Dr. Disposal a/c with the cost price xxx

Cr. Fixed asset a/c with the cost price xxx

It should be emphasized that the above entries are performed using the cost of

the asset disposed off.

2. Transfer the accumulated depreciation of the asset being disposed off tothe disposal account. The following entry is made:

Dr. Accumulated depreciation a/c

Cr. Disposal a/c

3. Record cash received on disposal a/c i.e. disposal proceeds

Dr. Cash/bank a/c with the cash received

Cr. Disposal a/c with the cash received

4. On closing the disposal accounts to the profit and loss account, thebalancing figure is either a gain or a loss on disposal.

a) Gain on disposal

Dr. Disposal a/c

Cr. Profit and loss a/c

b) Loss on disposal

Dr. Profit and loss a/c

Cr. Disposal a/c

Note: Alternatively gain or loss on disposal can be computed by deducting net

book value of the disposed asset from the proceeds received upon disposal.

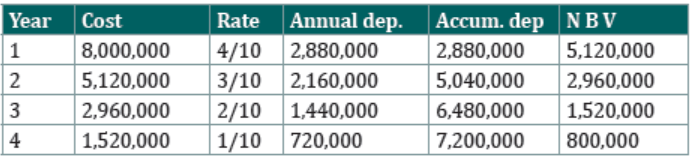

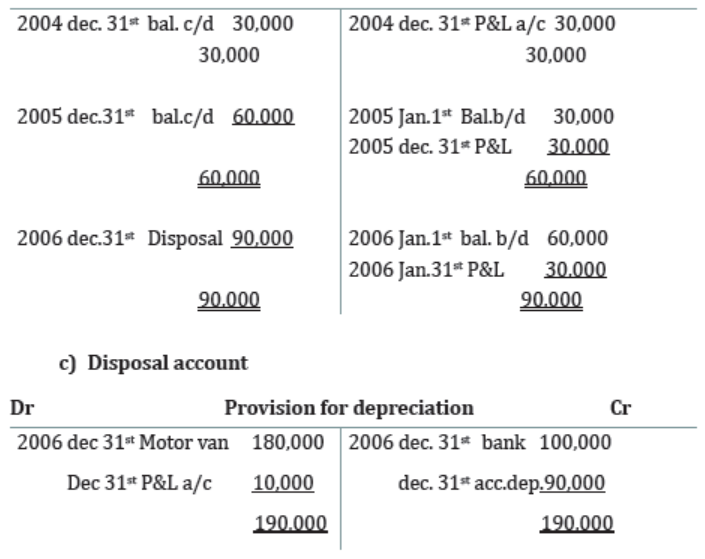

Illustration:

Kelly Ltd bought a motor van on 1st January 2004 at RWF 180,000 estimated

to last for 5 years after which it will have a scrap value of RWF 30,000. The vanwas sold on 31st December 2006 for RWF 100,000.

Required:

a) Motor van a/c

b) Provision for depreciation a/c

c) Disposal of Motor van a/c

Solution: a. Motor vehicle account

Note: There are 2 ways of considering when calculating provision for

depreciation for an asset bought or sold:

1. Full year’s depreciation is calculated on the assets purchased (on

acquisition) irrespective of the date of purchase during any accounting

period and no depreciation charged in the year of sale of the assets.

2. Depreciation is calculated on the basis of number of months that asset

was in ownership of the business but fractions of the months are usuallyignored.

Application activity 1.5

1. State different ways of disposing an asset.

2. Why must the asset account be closed off when the asset has beensold?

3. In disposal account, the total debit records must be compared to

the total credit records. What is the meaning of the equality of total

debit records and credit records in the disposal account?

4. Brighton Ltd Company bought a motor van on 1st January 2002 at

RWF 180,000 estimated to last five years after which it will have

a scrap value of RWF 30,000. The van was sold on 31st December2004 for RWF 350,000

Required:

a) Motor van account

b) Provision for depreciation on motor van accountc) Disposal of motor van account

1.6.Provision for discount allowed

Learning Activity 1.6

As discussed above in 1.2, in large businesses, most of transactions

are made on credit basis and the businesses, in order to stimulate their

customers to buy a bulk quantity or pay promptly, they decide either to

reduce monetary amount or a percentage of the normal selling price of a

product or service, or to reduce the total amount payable on the invoice

for an early payment discount on credit sales.

1. Why do these businesses allow this kind of discount?2. What is the impact of this discount to the net profit?

1.6.1. Meaning of discount

A discount is the reduction of either the monetary amount or a percentage of

the normal selling price of a product or service. For example, a discount of RWF

10 may be offered from the list price of a product, or as a 10% discount fromthe list price.

Discount results in the reduction of the selling price of the product, which

makes it more attractive for the customer. Reduction in price makes a

psychological impact on the customer which results in the purchase. The twotypes of discount offered are trade discount and cash discount.

Discounts are reductions of the regular price of a product or service in order

to obtain or increase sales. These discounts also commonly referred to as

“sales” or markdowns are utilized in a wide range of industries by bothretailers and manufacturers.

A discount allowed is when the seller of goods or services grants a payment

discount to a buyer. This discount is frequently an early payment discount on

credit sales, but it can also be for other reasons, such as a discount for paying

cash up front, or for buying in high volume, or for buying during a promotion

period when goods or services are offered at a reduced price. It may also

apply to discounted purchases of specific goods that the seller is trying toeliminate from the stock, perhaps to make way for new models.

A discount received is the reverse situation, where the buyer of goods orservices is granted a discount by the seller.

The examples just noted for a discount allowed also apply to a discountreceived.

A discount may be given for a variety of reasons, including:

• Earlier payment than the normal credit terms offered to customers,

such as a 1% discount in exchange for paying within 10 days,

• A price breaks due to the purchase of an unusually large number of

units, such as a 5% discount if at least 100 units are ordered,

• A price break if a purchase is made by a specific date, such as the end

of the month.

• A price break to take goods damaged in transit, or which differ fromwhat the customer ordered.

1.6.2. Types of discount

The two types of discount offered are trade discount and cash discount :

Trade discount

Trade discount is referred to the discount that is offered by a seller to the

buyer of the product in the form of reduction in the price of the item.

Trade discounts are offered to increase the sales of the product and make thecustomers feel that they are getting the best offer.

Cash discount

Cash discount is referred to the discount that is offered by the seller of a product

to the buyer at the time of payment for the purchase. This reduction is provided

at the value of the invoice. Cash discount is offered to make the customer or

the buyer pay for the product promptly, it helps the business in reducing oravoiding the credit risk completely.

Such discounts are mostly used in business transactions, where a creditor will

be reducing the amount to be paid by the debtor, if the payment is processed

within the time limit. Proper records are maintained for all such discounttransactions both by the buyer and seller.

1.6.3. Differences between trade discount and cash discount

As we have discussed the meaning and example of the two types of discount,

now we will move forward to talk about the differences between trade discountand cash discount :

Trade Discount is a subtraction from the list price of the goods, allowed by

the trader to the customer at an agreed rate. On the contrary, a Cash Discount

is a discount allowed to the customer, when he/she makes cash payment of thegoods purchased, within the stipulated time.

Trade discount is based on the amount of purchase or sales, i.e. the more the

sales the more will be the rate of discount, whereas cash discount is based on

time, i.e. the earlier the payment made by the debtor, the more will be the cashdiscount allowed.

Trade Discount is always provided to the customer in fixed percentage, whereasthe percentage of cash discount may or may not be fixed.

Trade Discount is allowed to the customers because of business considerations

like trade practices, bulk orders, etc. Conversely, Cash Discount acts as anincentive or motivation for stimulating payment within the specified time.

Trade Discount is provided to increase sales in bulk quantity, while CashDiscount is given to the customers to encourage early and prompt payment.

Trade discount is allowed on both cash and credit transactions. In contrast, acash discount is allowed to the customers only on cash payments.

Trade Discount is not specifically shown in the company’s financial books, and

all the transactions are entered in the purchases or sales book in net amountonly.

In contrast, Cash Discount separately appears in the financial books, as anexpense in the Profit and Loss Account.

Trade Discount is deducted from the invoice value or catalog price of the goods.As against, Cash Discount is deducted from the invoice value of goods

1.6.4. Provision for discount allowed

Provision for discount allowed is an additional allowance created to adjust the

debtor values in addition to losses experienced from the aforementioned cashdiscount and provision made on doubtful debts.

Provision for discount is recorded in similar way as provision for bad and

doubtful debts. It is important to also note that debtors written off are not

allowed any discount. The amount set aside as a provision for bad and doubtful

debts is therefore exempted from any provision for discount. Then, when

calculating the amount of provision for discount, they first must deduct fromthe debtor, total that amount already provided for bad and doubtful debts.

Application activity 1.6

1. Why do these businesses allow this discount to their customers?

2. What is the impact of this discount allowed to the customers on netprofit?

3. Answer by true or false:

a) Trade Discount is a subtraction from the list price of the goods,

allowed by the trader to the customer at an agreed rate. On the

contrary, a Cash Discount is a discount allowed to the customer,

when he/she makes cash payment of the goods purchased, within

the stipulated time

b) Cash discount is allowed on both cash and credit transactions. In

contrast, a trade discount is allowed to the customers only on cash

payments.

c) Trade Discount is provided to increase sales in bulk quantity,

while Cash Discount is given to the customers to encourage earlyand prompt payment.

1.7. Adjusted trial balance

Learning Activity 1.7

The accounting cycle states that after journalizing all business transactions,

the ledger account is prepared in order to go on with the preparation of the

trial balance. The prepared trial balance is, sometimes inaccurate due to

some transactions that need adjustments. Once the adjustments are made,

a new trial balance is needed to present a true performance and picture of

the company.

1. Is it necessary to prepare the new trial balance after adjustments for

the company?2. In which purpose the adjusted trial balance is prepared?

1.7.1.Meaning of the adjusted trial balance

An adjusted trial balance is a listing of a company accounts that will appear

in the financial statement after year-end adjusting entries have been made.

Preparing an adjusted trial balance is the fifth step in the accounting cycle andis the last step before financial statements can be produced.

1.7.2. Preparation of the adjusted trial balance

There are two methods for the preparation:

a) The first method is similar to the preparation of an unadjusted trial

balance. The ledger accounts are adjusted for the end of periods and

the account balance is listed to prepare an adjusted trial balance. This

method takes a lot of time, but it is very systematic and usually used bylarge companies where many adjustments need to be made,

b) The second method is quite fast and straightforward, but it is

not systematic and usually used by small companies where less

adjustments need to be done. In this adjustment, entries are directly

added to the unadjusted trial balance to convert it to an adjusted trialbalance.

Note: in each case, the format of the adjusted trial balance does not differ from

that of the unadjusted one. i.e any trial balance contains three columns asfollow:

a) a column of particulars

b) a column of debit balances

c) a column of credit balances

1.7.3. Purpose of the adjusted trial balance

• The primary purpose of the trial balance is a document that shows

the total amount of debit against the total amount of credit. It is not

considered as a financial statement because it is only used as an

internal document.

• Hence, it is beneficial for big companies to adjust many entries. It

also ensures that entries are done correctly; if balances entered into

financial statements are incorrect, the financial statements themselves

will be inaccurate, and the total must be equal.

• Any difference indicates some error in entries, ledger, or calculations.

So it gives a clear picture of the performance and financial position of

the company. It also helps to monitor the company’s performance as

the adjusted trial balance is prepared after considering all adjustmentsof entries of different accounts.

1.7.4 Difference between trial balance and adjusted trial

balance

• The trial balance is prepared first, whereas adjusted trial balance

prepared post-trial balance. The trial balance excludes some entries

like accrued expenses, accrued income, prepaid income, prepaid

expenses and depreciation, whereas adjusted trial balance includes

the same.

• A trial balance is a list of closing balances of ledger account on a

particular point in time. In contrast, adjusted trial balance is a list of

general accounts and their balances at a point of time after the adjustingentries have been posted.

Application activity 1.7

1. Is it necessary to prepare the new trial balance after adjustments

for the company?

2. In which purpose the adjusted trial balance is prepared?

3. Give some two aspects of how the adjusted trial balance differs fromthe unadjusted trial balance

Skills Lab 1

Students in small groups prepare an adjusted trial balance from case

studies. Through a case study, students conduct a field visit to school

bursar office, check how the students pay the school fees, where they find

three different categories of payment: (i) some of them, at the end of the

term, only totally pay the due amount, (ii) other students do not pay in full

the due amount, (iii) a few number of students pay the total amount dueand a part of the coming term.

End unit assessment 1

1. Distinguish bad debts from doubtful debts

2. Answer by yes or no:

• Accrued income is a current liability

• Accrued expense is a current asset

• Prepaid income is a current liability

• Prepaid expense is a current asset

• To adjust for accrued expenses, debit the amount outstanding tothe respective expenses account and credit it to the liability account

3. In disposal account, the total debit records must be compared to

the total credit records. What is the meaning of the equality of totaldebit records and credit records in the disposal account?

4. At the end of the fiscal year, account receivable has a balance of RWF

100,000 and allowance for doubtful debts account has a balance

of RWF 7,000. The expected net realizable value of the accountreceivable is

a) RWF 7,000

b) RWF 93,000

c) RWF 100,000

d) RWF 107,000

5. A manufacturing company Ltd acquired a plant for RWF 15,500,000

on 31st August 2015 while its accounting period starts on 1st January

every year. The management administration decided to depreciate

the plant using declining balance method in 5 years at the end ofwhich, remaining value of the plant will be RWF 5,000,000

As an accountant of the organization, what is the schedule of thedepreciation you propose to administration manager?

Unit 2 FINANCIAL STATEMENTS FOR A SOLE TRADER AFTER ADJUSTMENTS

Key Unit competence: To be able to prepare financial statements of asole trader after adjustments.

Introductory activity

Joyce, a sole trader in Remera, she records her business transactions

daily. After preparing the trial balance for the year 2022, she found out

some additional information which caused the trial balance to be adjusted

following the accounting cycle. The step of accounting cycle after adjustedtrial balance is to prepare financial statements.

Required:

a) As a professional accountant, advice Joyce (sole trader) on the

main financial statements that can be prepared for the proper

books of accounts of her business.

b) Show the main elements of each financial statement to be preparedby Joyce.

2.1. Income statement/ Statement of Profit or Loss afteradjustments

Learning Activity 2.1

ABC business has been performing well almost for five years since 2016

and currently it is experiencing a drop/loss in their profits according to

the financial performance for the year 2021. Apart from this drop, after

deep checking, some additional information needs adjustments. Owners

are complaining about the current performance of their business. As an

accountant of ABC Business, explain to the owners about the performanceof their business.

a) The loss for the period can be identified using which component of

financial statement?b) Show the main parts/components of statement of profit or Loss.

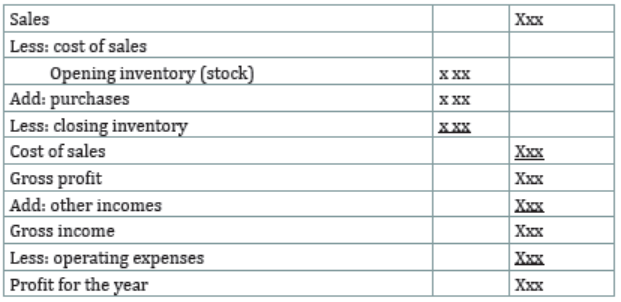

As seen in Senior 4 unit 10, at the end of year, every business must ascertain itsnet profit/loss. This is done in two stages.

1. Finding out the Gross Profit / Gross Loss which is got with Trading

Account2. Finding out the Net Profit / Loss which is got with Profit or Loss Account

2..1.1.Determination of Gross Profit /Gross Loss after adjustments

The entries/items that will appear in the Trading Account to ascertain the GrossProfit/Loss will be: (some items will be debited while other will be credited)

i. Items to be debited

1. Opening stock

It speaks of the inventory that was on hand at the start of the prior accounting

year. Opening stock is the quantity of an item present at the start of a new period

for keeping inventory. It contains the worth of the goods that the companydeals in and serves as the opening stock for the current accounting year.

2. Purchases

It refers to the value of goods (in which the concern deals) which are purchased

either on cash or on credit for the purpose of resale. The balance of purchases

account, appearing in the trial balance, reflects the total purchases made during

the accounting period. While dealing with purchases, we must bear in mind the

following aspects:

a) Purchase of capital asset should not be added with the purchases. If it

is already included in purchases, it should be deducted immediately.

b) If goods are purchased for personal consumption and they are added

with the purchases, they should be excluded. These types of purchases

should be treated as drawings.

c) If some of goods purchased are still in transit at the year-end, it is

better to debit stock-in-transit Account and credit Cash or Supplier’sAccount.

d) If the amounts of purchases include goods received on consignment, on

approval or on hire purchase, these should be excluded from purchases.

e) Cost of goods sent on consignment must be deducted from thepurchases in case of trading concern.

3. Sales return/ Return Inwards

In the books of account, Returns Inwards Account or Sales Returns Account

is debited and buyer’s account is credited. It appears on the debit side of Trial

Balance. We can show the sales returns in Trading Account in two ways. It may

be shown by way of deduction from sales in the Trading Account. An alternative

way to show the sales returns is in the debit side of the Trading Account.

4. Direct expenses/carriage inwards

These types of expenses are directly incurred in connection with purchases,

procurement or production of goods. These expenses are directly related to the

process of production. They also include expenses that bring the goods up to

the point of sale.

ii. Items to be credited

1. Sales

It refers to the sale of goods in which the business deals and includes both

cash and credit sales. It does not include sale of old, obsolete or depreciated

assets, which were acquired for utilization in business. However, goods sent to

customers on approval basis, free samples and sales tax, if any, included in thesales figure should be excluded.

2. Purchases returns

It may come about that due to some reasons: the goods are sent back to the

supplier. In that case, the supplier is debited in the books of accounts and

purchases returns or returns outwards are credited. It appears on credit side in

the trial balance. There are two ways of showing the purchases returns in the

income statement. It may be shown by way of deduction from purchases in the

income statement. An alternative way is to show the purchases returns in thecredit side of the income statement.

3. Closing stock

It refers to the value of goods lying unsold at the end of any accounting year.

This stock at the end is called closing stock and is valued at either cost or market

price, which is lower. The trial balance generally does not include closing stock.

Therefore, the following entry is recorded to incorporate the effect of closingstock in the income statement;

Dr. Closing Stock A/C

Cr. To Trading A/C

However, if closing stock forms a part of Trial Balance, it will not be transferred

to Income Statement but taken only to the statement of Financial Position. In

case of the goods that have been dispatched to customers on approval basis,such goods should be included in the value of closing stock.

Ascertain the Gross Profit or Loss

After recording the above items in the respective sides of the income

statement, the balance is calculated to ascertain Gross Profit or Gross Loss.

As seen in Senior 4, if the total of credit side is more than that of the debit side,

the excess represents Gross Profit. Conversely, if the total debit side is more

than that of the credit side, the excess represents Gross Loss. Remember thatthe Gross profit is ascertained using the Trading Account.

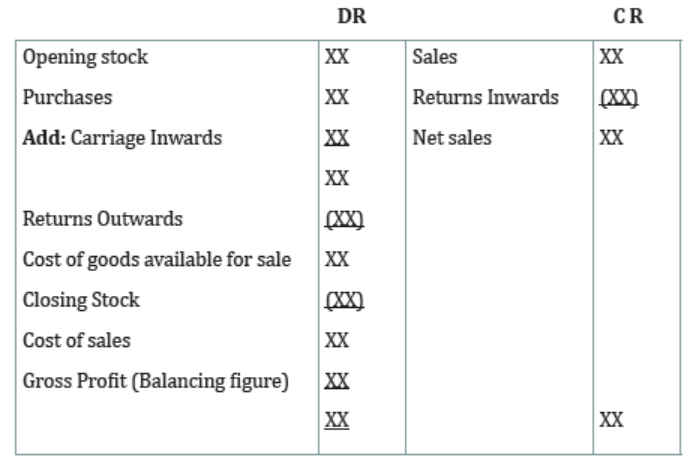

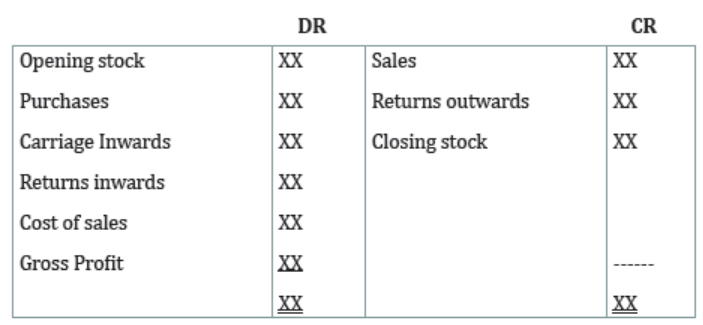

TRADING ACCOUNT (HORIZONTAL FORMAT)

Name of the company (date/month/year)

Or

TRADING ACCOUNT (HORIZONTAL FORMAT)

Name of the company (date/month/year)

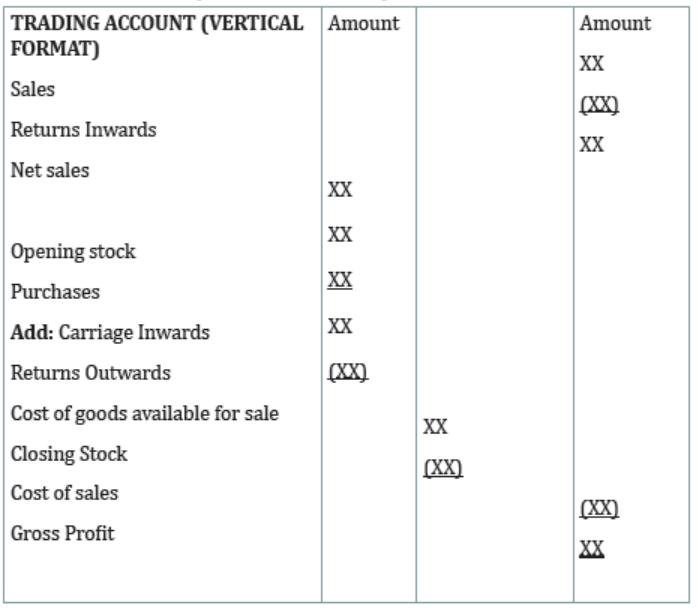

TRADING ACCOUNT (VERTICAL FORMAT)

Illustration1

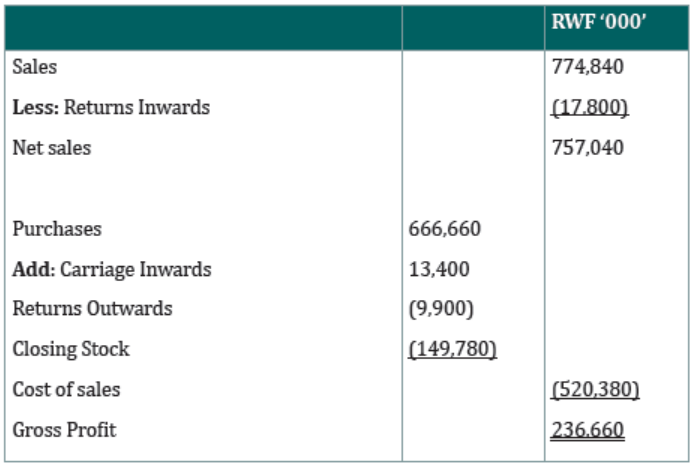

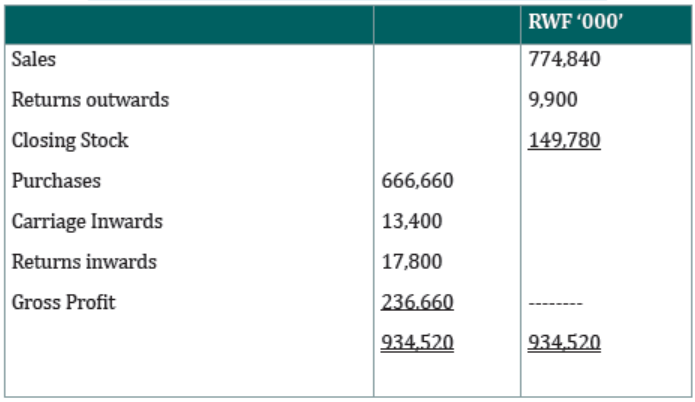

From the following details draw up the trading account of Mr Kamanda for theyear ended 31st December 2022, which was his first year in business.

Mr Kamanda

Trading Account for the year ended 31 December 2022

Mr. Kamanda

Trading Account for the year ended 31 December 2022

Illustration 2

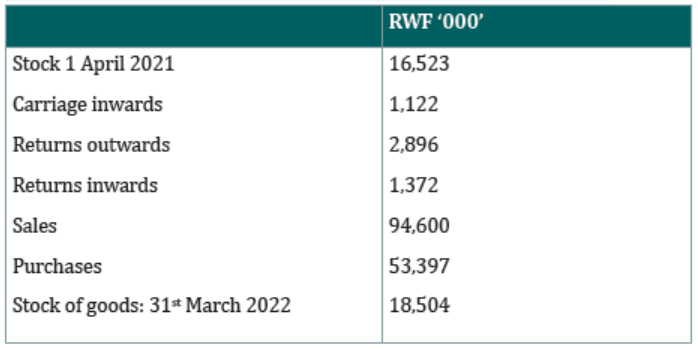

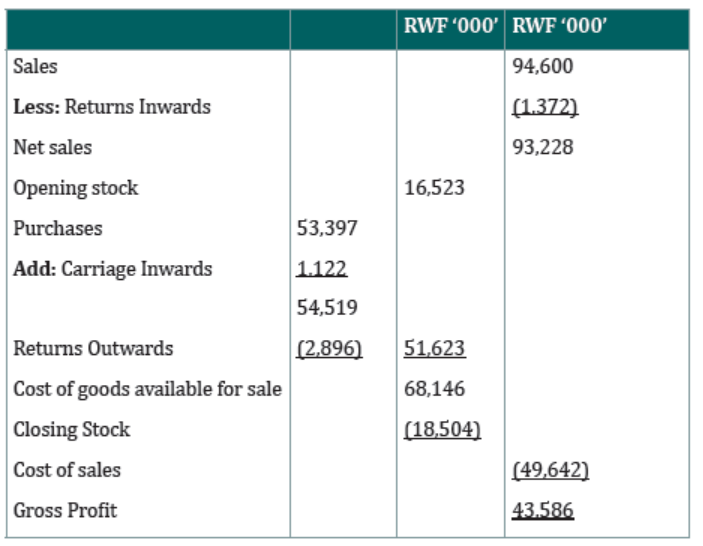

The following details for the year ended 31st March 2022 are available for

Bosco’s business. Draw up the Trading account of Bosco for that year.

Bosco

Trading Account for the year ended 31 March 2022

Determination of net profit (or Loss) after adjustments

After ascertaining the gross profit, the subsequent step is to ascertain net profit

or net loss during an accounting period. The net income/profit is measured by

matching revenues and expenses. Net income is the difference between totalrevenues and total expenses.

a) Items to be debited to the Income Statement

i. Management expenses

These are the expenses incurred for carrying out the day-to-day administration

of a business. Expenses under this head include office salaries, office rent andlighting, printing and stationery, telegrams, telephone charges etc.

ii. Selling and distribution expenses

These expenses are incurred for selling and distribution of products and

services, as the name indicates, they comprise of commissions and salaries ofsalesmen, advertising expenses, packaging, bad debts etc.

iii. Maintenance Expenses

These expenses are incurred for maintaining the fixed assets of the

administrative offices in a good condition. They include expenses towardsrepairs and renewals.

iv. Financial expenses

These expenses are incurred for arranging finances necessary for running the

business. These include interest on loans, discount on bills, brokerage and legalexpenses for raising loans etc.

v. Abnormal losses

Some abnormal losses may arise during the accounting period. All types of

abnormal losses are treated as unusual expenses and debited to Profit and Loss

Account. Examples are stock lost by fire but not covered by insurance, loss onsale of machinery, cash defalcation etc.

vi. Wages and salaries earned by the worker-whether paid or not

N.B: To ascertain the amount of expenses to be debited to the income statement,

four types of events are essentially considered and then cash payment is madein connection with these events they are as under:

Expenses incurred and paid out in that year: those will be debited to theincome statement.

Expenses incurred but not paid out, partly or fully, during the current year

(outstanding expenses): on the date of the final accounts, those are in form of

both the expenses and a liability and they exist without having been recorded

in the books of accounts. For recording it, the following entry is to be passed:

• Dr. Expenses A/C Dr. (will be shown in the income statement account)

• Cr. Outstanding Expenses A/C (will appear in the liabilities side ofstatement of Financial Position)

• Expenses paid for during the current year, but not incurred as

yet, partly or fully (prepaid expenses): these are assets and will beshown in the Statement of Financial Position.

• Expenses of the current year, likely to arise in subsequent period:

in such case, we make a provision for the anticipated loss and a charge

is created against the profit for the current period. This provision is

shown as either a liability or contingent asset, i.e. it appears in the

statement of Financial Position as a deduction from some other assets.The best example of this anticipated expense is Provision for Bad Debt.

a) Items to be credited to the Income Statement

i. Other incomes

Sometimes a business might generate some profits, which is not due to the sale

of its goods or services because the business may have some other source of

financial income. The examples are discount or commission received.

ii. Non-trading Income

The business may have various transactions with the bank. At the end of the

year, the business may earn some amount of interest, which will find a place in

the profit & Loss Account as non-trading income. The business may have some

investment outside the business in the form of shares, debentures or units. All

sorts of gains obtained from such kinds of investments are considered as nontrading

income and are treated accordingly.

iii. Abnormal gains

There may be capital gains arising during the course of the year, e.g. profit

arising out of sale of a fixed asset. The profit is shown as a separate income

on the credit side of the Profit & Loss Account. We must remember that all

incomes from the abnormal gains or other incomes should be credited to the

Profit &Loss Account if they arise of accrues during the period. Similarly, income

received in advance should be deducted from the income.

Ascertaining the net Profit &Loss

Once the respective accounts are transferred from trial balance to income

statement, gross profit/ loss ascertained and all adjustments are taken care of,

the income statement will now be balanced. The totals of incomes and expenses

are computed and the difference between these totals is either a net profit or

net loss. If the total of expenses exceeds the total of incomes, there is a net Loss,

whereas when the total of incomes exceeds the total of expenses, there is a netprofit. Net profit/ loss is the last item to be recorded in income statement.

When the Profit and loss account shows a net profit, we pass the followingentry:

Dr. Profit &Loss A/C

Cr. Net Profit A/C

If the Profit and Loss Account shows a net loss, the entry will be reserved.

Format of income Statement

The Formats of Statement of Profit or Loss was discussed in S4 Unit 10

Illustration 1

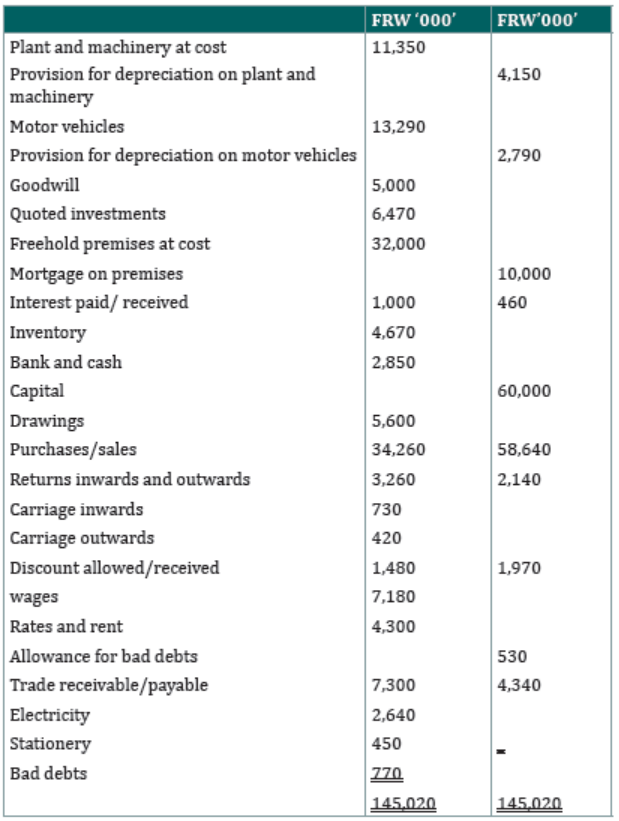

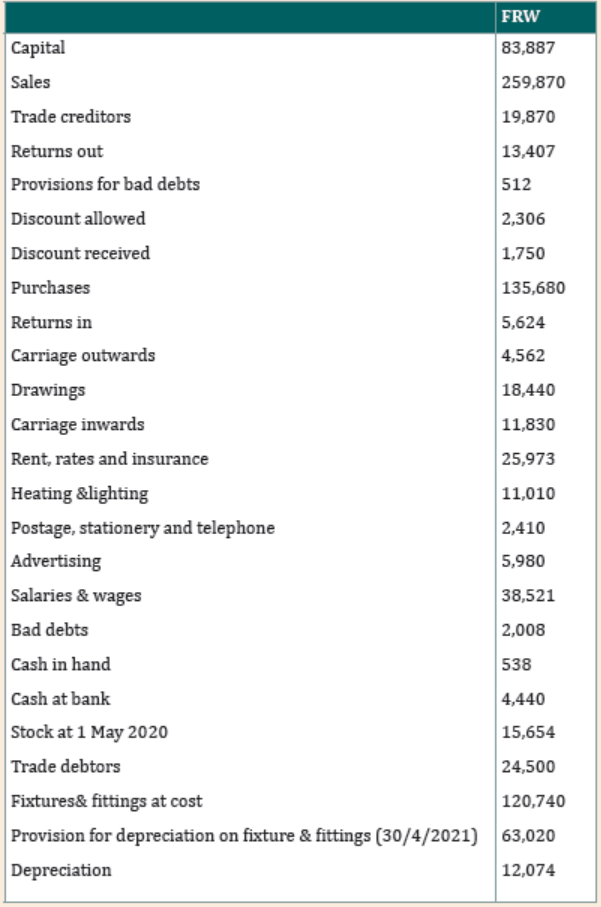

The following trial balance was extracted from the books of Mugabe, a soletrader as at 31st August 2022.

Additional information

1. Inventory as at 31st August 2022 was valued at FRW 3,690,000

2. Allowance for bad debts is to be adjusted at 10 % of debts

3. Goods which costed FRW 300,000 had erroneously been invoiced to a

customer for FRW 400,000 and had been accounted for in sales

4. Electricity accrued as at 31st August 2022 was FRW 130,000 and

prepaid rates amounted to FRW 210,000 as at 31st August 2022

5. Stock of stationery as at 31st August 2021 was FRW 230,000

6. Depreciation is to be provided on pro rata basis as follows:

• Motor vehicles 20% on reducing balance method

• Plant and machinery 25% on reducing balance

7. A motor vehicle was sold on credit on 1st December 2021 for FRW

458,000. The motor vehicle had been bought on 1st June 2020 for FRW

1,000,000 the sale had not been recorded to the ledger., proportionatedepreciation is applicable until disposal date

8. During the year, Mugabe took goods worth FRW 350,000 from the

business for his own use.

Required: Prepare Income Statement/ Statement of Profit or Loss for theyear ended 31st August 2022

Solution

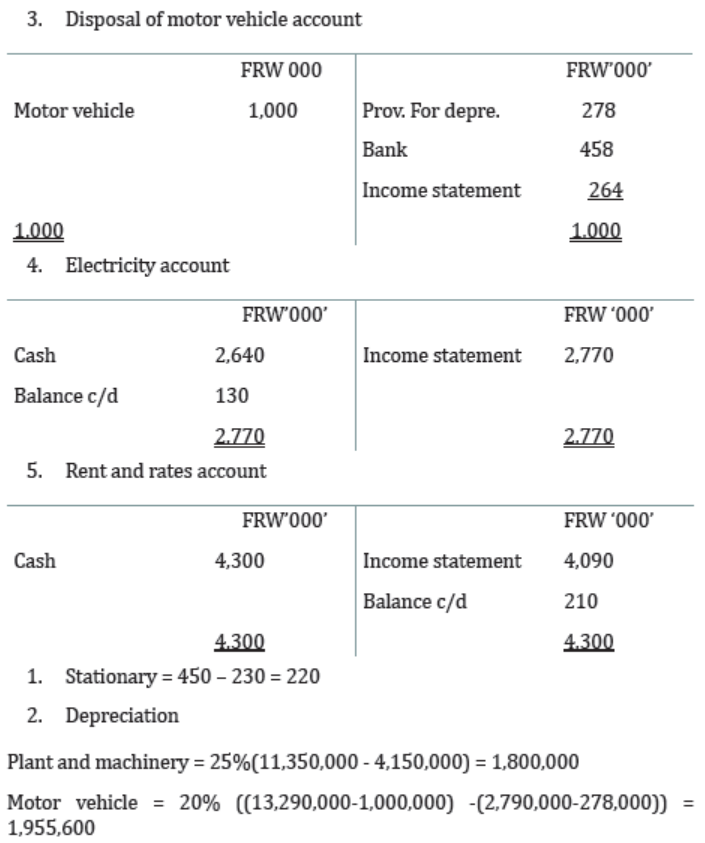

Workings:

1. Provision for bad debts = 7,300,000*10% = 730,000

Increase in previous for bad debts = 730,000 - 530,000 = 200,000

2. Motor vehicle depreciation:

1st period of 3 months 20%*1,000,000*3/12 50,000

2nd period full year 20%*(1,000,000 - 50,000) 190,000

3rd period 20% (1,000,000-50,000 - 190,000) *3/12 38,000

278,000

NBV = 1,000,000 – 278,000 = 722,000

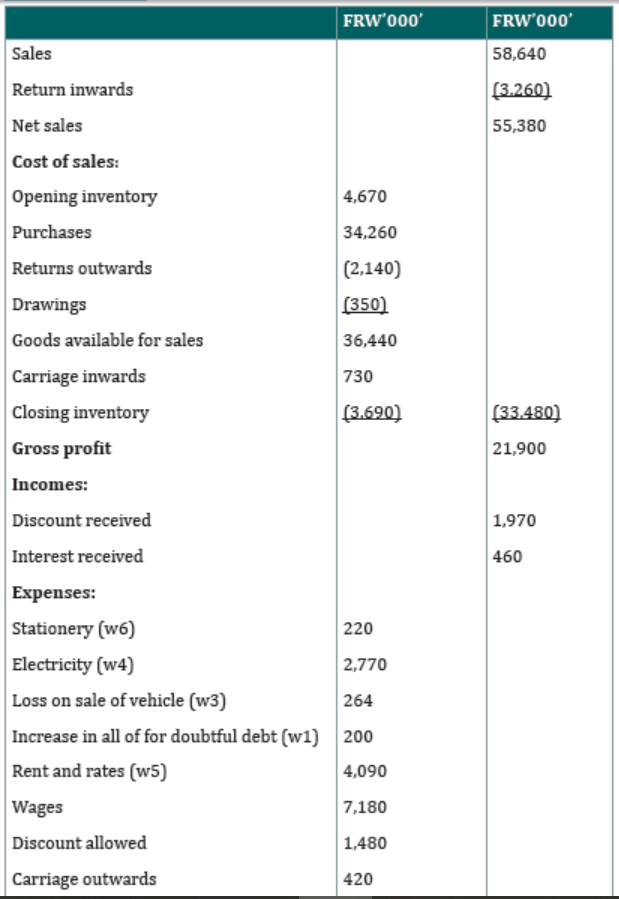

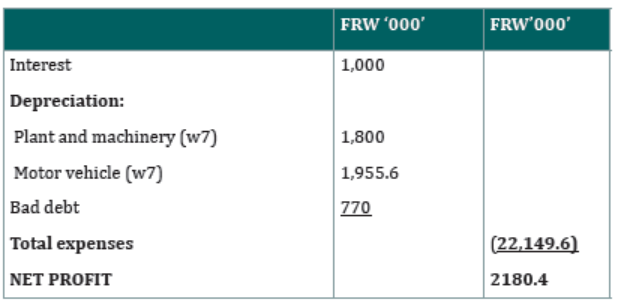

Mugabe Income statement/ statement of Profit or Loss for the year ended

31st August 2022

Illustration 2

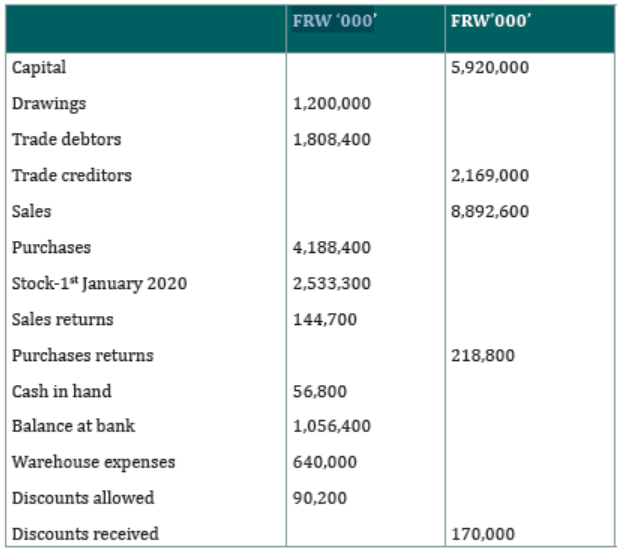

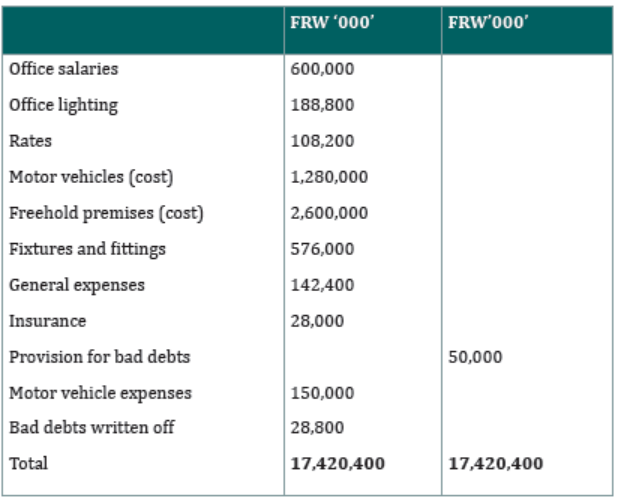

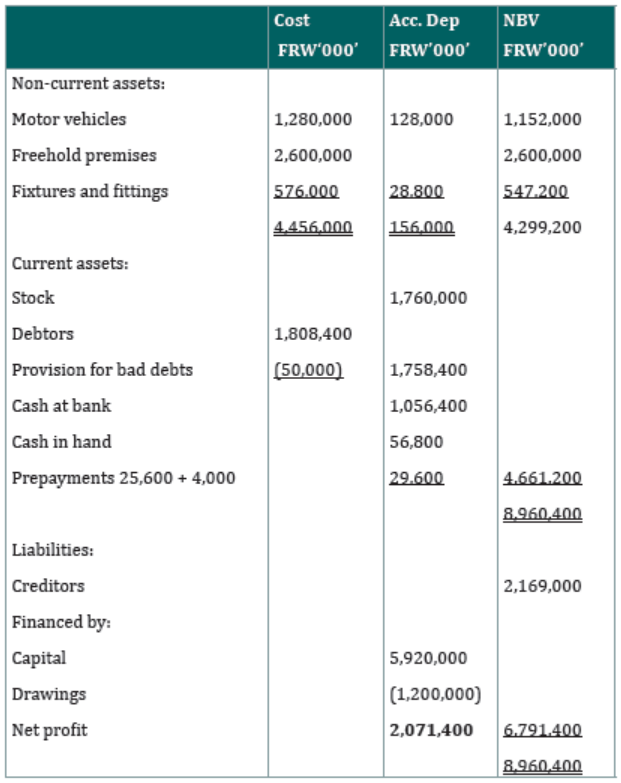

The following trial balance was extracted from the books of MIRIMO, a sole

trader for the year ended 31st December 2020FRW ‘000

Additional information:

1. Stock as at 31st December 2020 was valued at FRW 1,760,000

2. Depreciation on fixtures and fittings and motor vehicle is to be provided

at the rate of 5% and 10 % per annum respectively

3. Rates prepaid as at 31st December 2020 amounted to FRW 25,600,000

4. Unexpired insurance as at 31st December 2020 is to be made at FRW 4Million.

5. Additional FRW 1,758,240 Discount received is to be madeRequired:

Prepare Statement of Profit or Loss for the year ended 31st December 2020

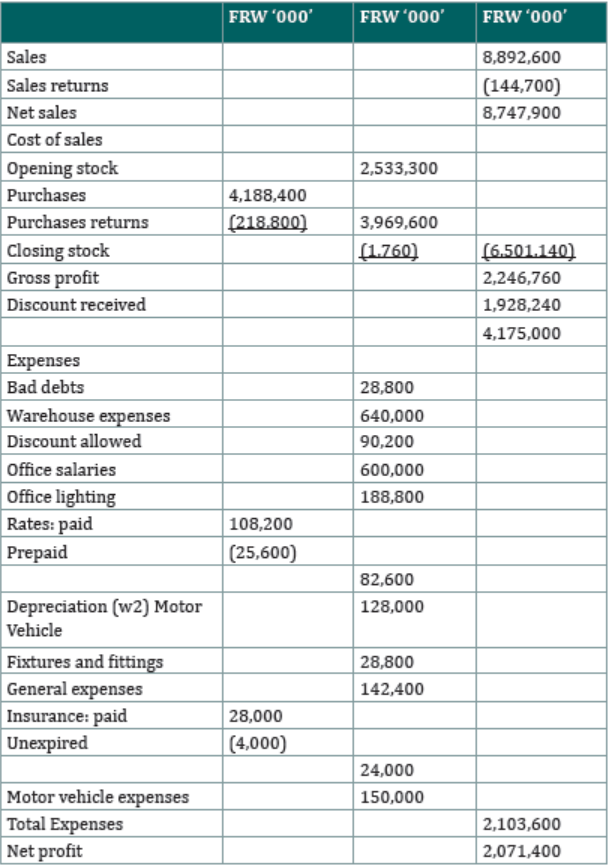

Solution

MIRIMO

Statement of Profit or Loss for the year ended 31December 2020

Illustration 3

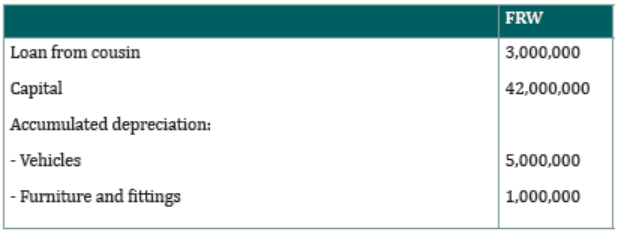

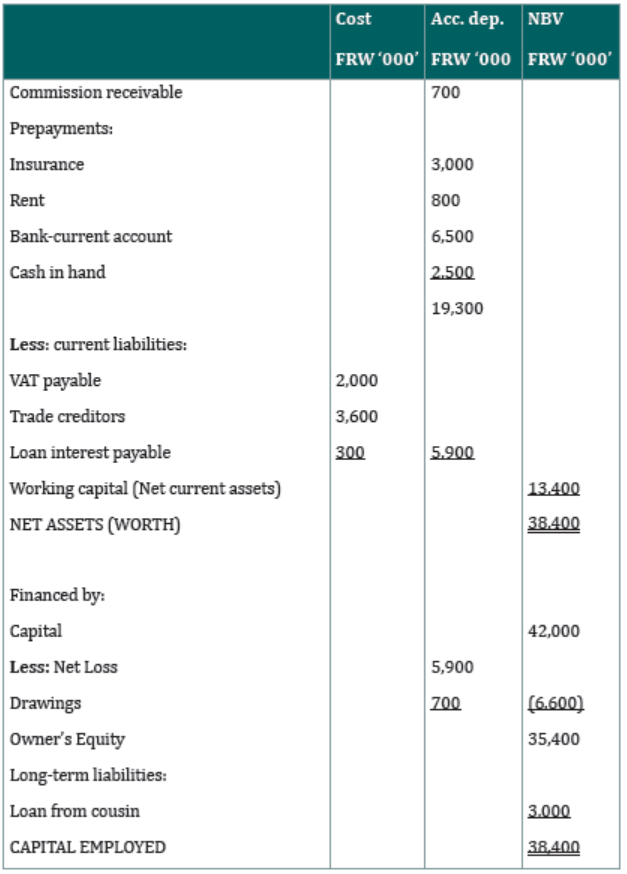

The following balances were extracted from ENOCK’s accounting books at theend of the financial year on 30th June 2020.

Additional information

a) Stock of goods in trade was valued at FRW 1,800,000 at the end of the

year

b) FRW 300,000 of the carriage relates to purchases and the balance

relates to sales

c) Enock receives a commission of 1% of gross purchases. The outstanding

balance of the commission for the year ended is to be received on 5th

day of the following financial year.

d) The provision for bad debts is to be reduced by 10% of the trade

debtor’s figure

e) Rent was paid on the first day of the financial year to cover a period of

18 months.

f) The loan from cousin was acquired on 1st January (within the financial

year), it is at interest rate of 20% per annum. Interest due for the period

is outstanding.

g) Vehicles are to be depreciated by 20% per annum on reducing balance

method and furniture and fittings by 10% per annum on cost.

h) Prepaid insurance of FRW 1,000,000 expired on 30th June 2020 (thelast day of the financial year).

Required:

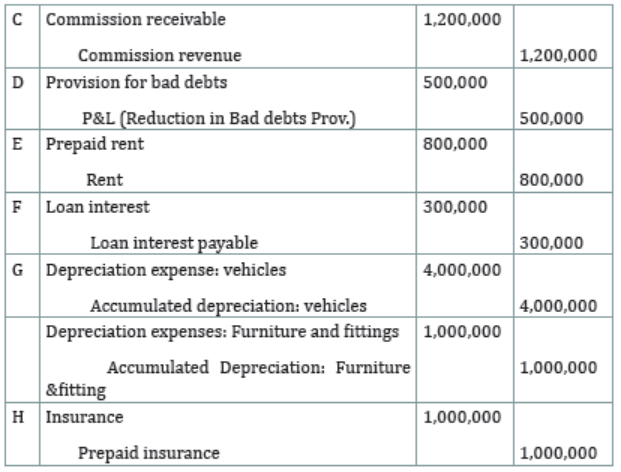

a) a) Journal entry to record adjusting information c-h

b) b) Statement of Profit or Loss (Income Statement) for the year ended

30th June 2020.

Solution:

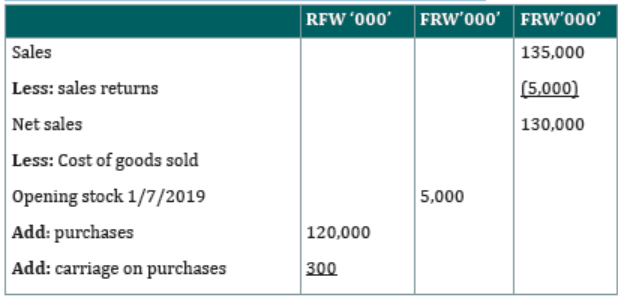

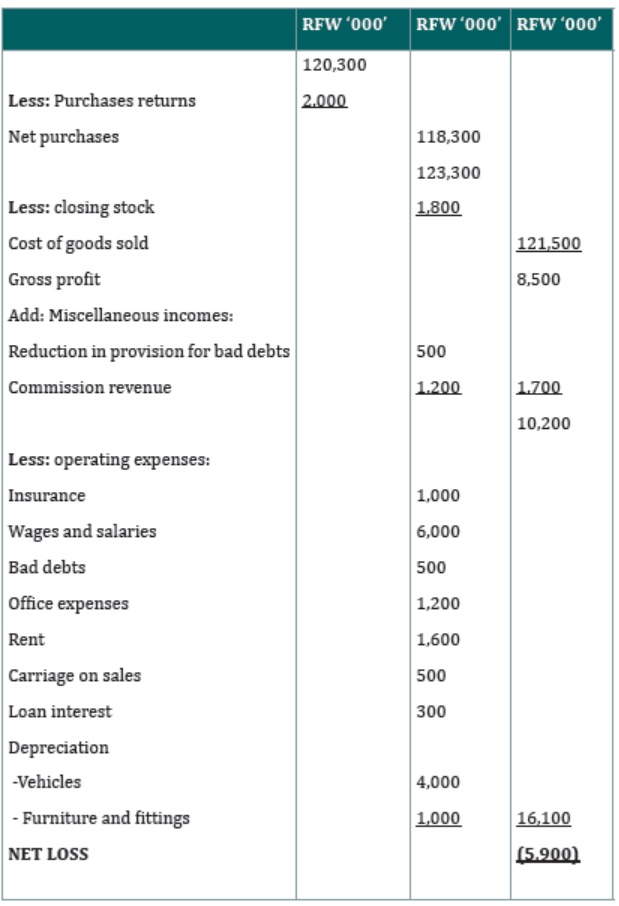

Enock

Journal entries to record Adjusting information on 30/6/2020

Enock

Statement of Profit or Loss for the year ended 30/6/2020

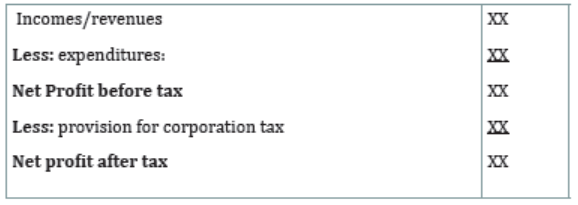

Income statement/ Statement of Profit or Loss in service firms

The income statement/ Statement of Profit or Loss for service sector firms e.g.

banks; insurance companies, etc are simple to draw up as it does not containthe trading Account. Their formats are shown as follows:

Statement of Profit or Loss

Illustration 4

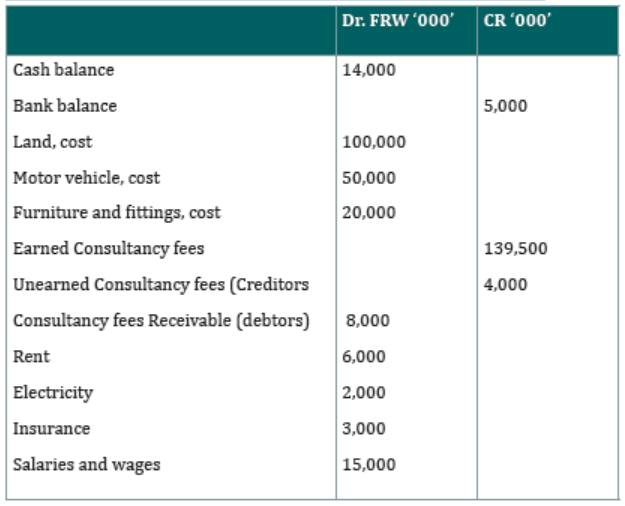

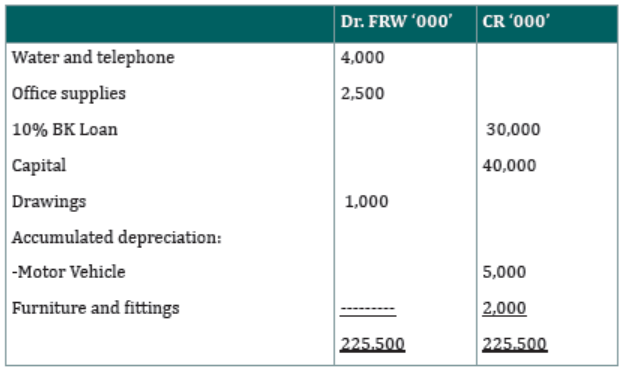

Peter, a consultant in accountancy services prepared the following trial balancefor his Door way consultancy for the financial year ended 31/8/2019

Information for adjustments at the end of the year

1. Consultancy fees of FRW 2,000,000 which were unearned were earned

on 31/8/2019. The trial balance does not reflect this information.

2. Customers who were provided with services during the year ended

to June 2019 amounting to FRW 3,500,000 were not yet invoiced by

31/8/2019.

3. Hand count of office supplies on 31/8/2019 revealed that office supplies

worth FRW 500,000 remained in inventory

4. Depreciate Furniture and fittings and motor vehicles by 10% on cost

5. Loan interest for one year accrued

6. Electricity bills amounting to FRW 1,500,000 remained outstanding on

31/8/2019

7. A provision of corporation tax to be paid at the rate of 30% of pre-tax netprofit should be made.

Required:

Statement of Profit or Loss of Peter’s Consultancy at the end of the FinancialYear on 31/8/2019

Solution

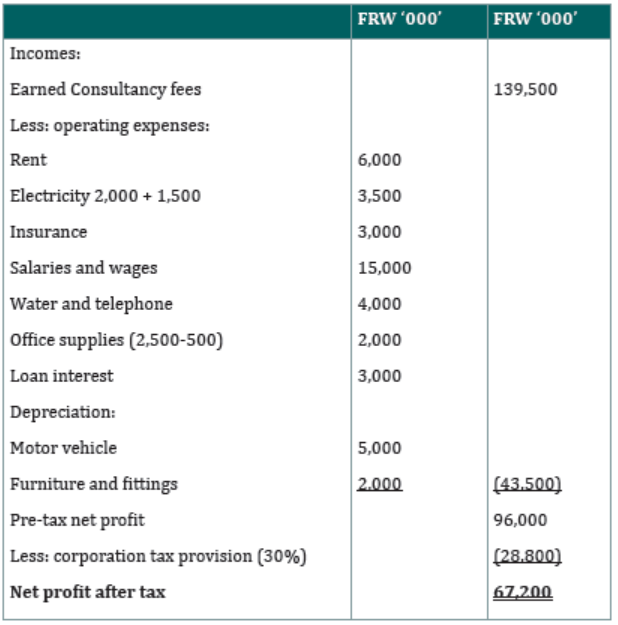

Door way Consultancy Income Statement/ Statement of Profit or Loss for

the period ended 31/8/2019

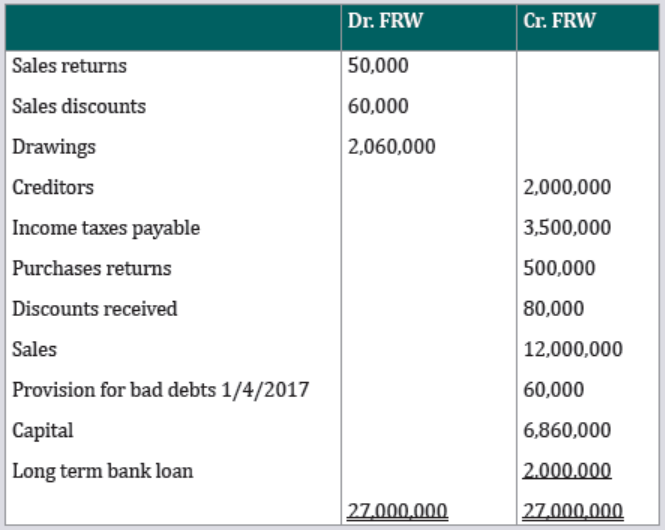

Application activity 2.1

Mr Amandi has been trading for some years as Wine merchant. The

following list of balances has been extracted from his ledger as at 30 April2020, the end of his financial year.

Additional information:

a) Stock at the close of business was valued at FRW 17,750.

b) Insurance has been prepaid by FRW 1,120

c) Heating and lighting is accrued by FRW 1,360

d) Rates have been prepaid by FRW 5,435

e) The provision for bad debts is to be adjusted so that it is 3% of trade

debtors

REQUIRED: Prepare Mr Amandi’s trading, profit and Loss account for the yearended 30 April 2020.

2.2. Balance sheet (statement of Financial position) afteradjustments

Learning Activity 2.2

A local business located in Nyabihu District owned by Annette collects and

distributes Irish potatoes. At the end of 2022, while closing the financial

period, Annette was not aware on the statement to be prepared. You are

asked

1. To advise her on which statement to be prepared in order to knowthe financial position of her business.

Learning Activity 2.2

A Statement of Financial Position is a summary of the financial balances of a sole

proprietorship, business partnership or a company. It is a statement that helps

us to establish the financial position of a business enterprise on a particular

date, i.e. on a date when financial statements or final accounts are prepared or

books of accounts are closed.

In facts, this statement treats the balances of all those ledger accounts that have

not yet been squared up. These accounts relate to assets owned, expenses due

but not paid, incomes accrued but not received or certain receipts which are

not due or accrued. In other words, it deals with all those real and personal

accounts which have not been accounted for in trading or Profit & Loss accounts.

Therefore, an important feature of a statement of financial position is to showthe exact financial picture of a business concern on a particular date.

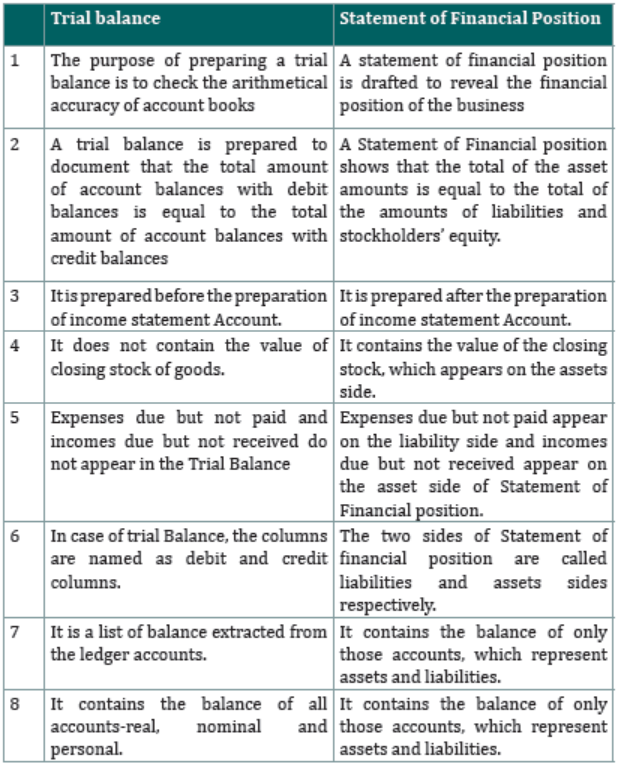

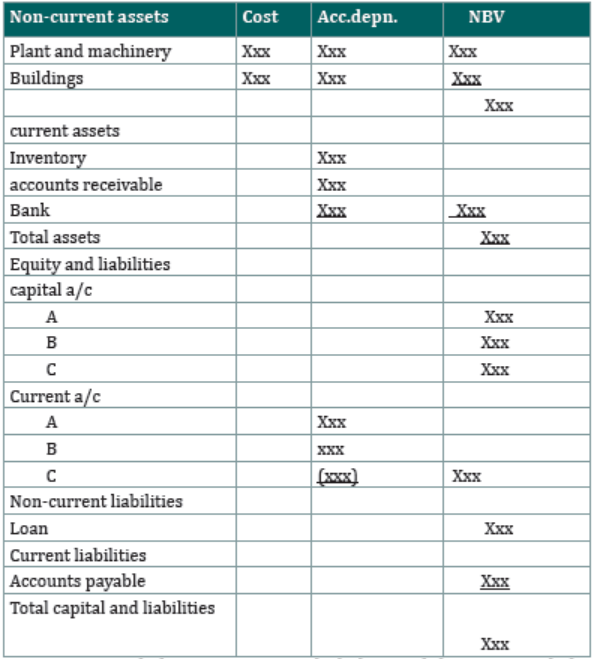

2.2.1. Difference between trial balance and Statement of FinancialPosition

2.2.2. Preparation and presentation of statement of Financial

position

The process of preparation and presentation of statement of financial positioninvolves two steps:

• Grouping

• Marshalling

Grouping

In the first step, the different items to be shown as assets and liabilities in the

Statement of Financial Position are grouped appropriately. For this purpose,

items of similar nature are grouped under one head so that the Balance Sheet

could convey an honest and true message to its users. For example, stock,

debtors, bills receivables, bank, cash in hand etc. are grouped under the

heading current Assets and land and Building, plant and Machinery, Furniture

and fittings, tools and equipment under Non-Current Assets. Similarly, sundry

creditors for goods must be shown separately and distinguished from moneyowing, other than due to credit sales of goods.

Marshalling

The second step involves marshalling of assets and liabilities. This involves

a sequential arrangement of all the assets and liabilities in the statement ofFinancial Position. There are two methods of presentation:

• The order of liquidity

• The order of permanence

Under liquidity order, assets are shown on the basis of liquidity or reliability.

These are rearranged in an order of most liquid, more liquid, liquid, least liquid

and not liquid (fixed) assets. Similarly, liabilities are arranged in the order in

which they are to be paid or discharged.

Under order of permanence, the assets are arranged on the basis of their useful

life. The assets predicted to be most fruitful for the business transaction for

the longest duration will be shown first. In other words, this method puts the

first method in the reverse gear. Similarly, in case of liabilities, after capital,

the liabilities are arranged as long term, medium term, short term and currentliabilities. This is the commonly used method.

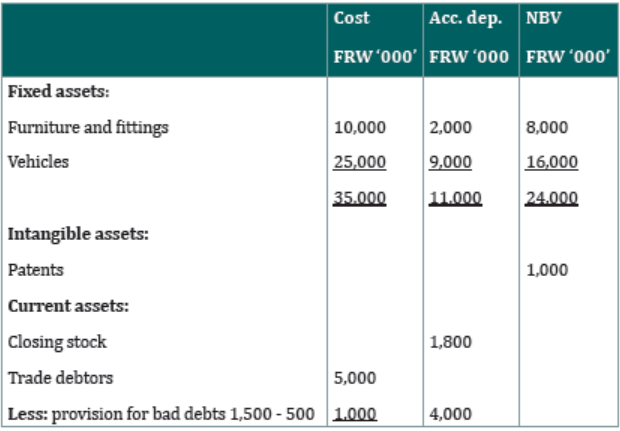

Classification of assets

1. Non-current assets

2. Intangible assets

3. Current assets

4. Fictitious assets

5. Wasting assets

6. Contingent assets

i. Non-current assets

These are those assets, which are acquired for the purpose of producing Goods

or rendering services. These are not held for resale in the normal course of

business. Fixed assets are used for the purpose of earning revenue and hence

these are held for a longer duration. Investment in these assets is known as‘Sunk Cost”. All fixed assets are tangible by nature.

ii. Intangible assets

Intangible assets are those capital assets, which do not have any physical

existence. Although these assets cannot be seen or touched, they are long lasting

and prove to be profitable to owner by virtue of the right conferred upon them

by mere possession.

They also help the owner to generate income. Goodwill, trademarks, copyrightsand patents are the example of intangible assets.

iii. Current assets

Current assets include cash and other assets, which are converted or realized

into cash within a normal operating cycle or say, within a year.Current assets are also known as Floating Assets or Circulating Assets.

iv. Liquid or quick assets

These are current assets that can be converted into cash at a very short notice

or immediately, without incurring much loss or exposure to high risk. Quick

assets can be worked out by deducting Stock (raw materials, work-in-progressor finished goods) and prepaid expenses out of total current assets.

v. Fictitious assets

These are the non-existent worthless items which represent unwritten-off

losses or costs incurred in the past, which cannot be recovered in future or

realized in cash. Examples of such assets are preliminary expenses (formation

expenses), advertisement expense, underwriting commission, discount on

issue of shares and debentures, Loss on issue of debentures and debit balance

of income statement account. These fictitious assets are written off or wipedout by debiting them to income statement account.

vi. Wasting assets

An asset that has a limited life and therefore windless in value over time it is

called wasting asset. This type of asset has a limited useful life by nature and

depletes over a limited duration. These assets become worthless once their

utility is over or exhausts. During the life of productive usage, assets of this type

produce revenue, but eventually reach a state where the worth of the assets

begins to diminish. Such assets are natural resources like timber and coal, oil,mineral deposits etc.

vii. Contingent assets