Unit 5 PUBLIC SECTOR ACCOUNTING

Key unit competence: To be able to prepare accounts for public sectororganizations

Introductory activity

MASENGESHO has previously worked as accountant for a limited liability

company. In May 2022 he has changed the employer and became a chief

accountant for Gatsibo District just during the period of closing fiscal year.

One of his duties is to prepare financial statements for the district. Besides

his not familiar of preparing them because he was in private sector.

Required: Enumerate five financial statements prepared in publicorganizations.

5.1. Public Finance management (PFM) legal framework

Learning Activity 5.1

HABAKUBANA Elaste, a budget Manager, asked you to describe the PFM

cycle which is different from accounting cycle described in senior four.Required: Convince him by describing the PFM cycle.

5.1.1. Introduction to Public Sector Accounting

According to International Public Sector Accounting Standards Board (IPSASB),

the term” Public sector” refers to national governments, Regional (eg: State,

provincial, territorial) governments, local (eg; City, town) governments

and related government entities (eg; agencies, boards, commissions andenterprises).

Public sector plays a fundamental role in the political and economic structure

of a country.

The Rwanda Public Sector consists of the Following:

– Central Government, Ministries, Donor projects, Embassies

– Local government eg. Kigali city council

– Public enterprises or parastatals eg. RITCO, WASAC, National post

office, BNR– Charitable organizations

Government organizations differ from business organizations discussed inprevious units in that:

– Governments have no stockholders or other owners;

– They render services with no expectation of earning profit, and

– They have power to require taxpayers to support financial operations

whether or not they receive benefits in proportion to tax paid.

– Similarly, non-profit organizations exist to lender services to the people

with no expectation of earning profit from those services, have no

owners, and seek financial resources from persons who do not expect

either repayment or economic benefits in proportion to the resources

provided

– Governments and non-profit organizations are governed mainly by

their budgets not by the market place. Through the budgetary process,

these organizations control or strongly influence both their revenuesand expenditures.

Public sector organisations provide a great number of diversified services to

the community. These organisations are also regarded non-profit organisation.

All public sector bodies have one feature in common. Their specific powers arederived from parliament and their responsibilities are ultimately to parliament.

Examples of public sector activity may include delivering Social security;administering urban planning and organizing national defence.

The organization of the public sector can take several forms, including:

Direct administration funded through taxation; the delivering organization to

meet commercial success criteria and production decisions are determined bythe government.

5.1.2. Public finance

Public finance describes finance as related to sovereign states and sub-national

entities (states/provinces, countries, municipalities, etc.) and related publicentities (eg. schools, districts) or agencies.

Public finance is concerned with:

• Identification of required expenditure of a public sector entity

• Sources(s) of that entity’s revenue

• The budgeting process

• Debt issuance (municipal bonds for public sector works projects)

Public Finance deals with the finances of public. It thus deals with the finances

of government. The finances of the government include the raising and

disbursement of government funds. It is concerned with the operation of thepublic treasury.

5.1.3. Role of Public sector in the economy

In the developing countries also the growth of public sector has beenphenomenal.

a) Information control

To ensure that the general public has adequate information to make informed

choices, the government ensure that business make available all necessary

information to the public. This includes proper labelling on all goods availablefor sale. In this way, the government protects public health and safety.

b) Monopoly control

To keep any one business or company from becoming too powerful and

concerning the market place, the government has to create antitrust laws to

control or break up any monopolies. This allows the consumer to have a varietyof fair option the market to choose from.

c) Regulation Control

To ensure that the businesses are held accountable for their actions, the

government has created strict regulations for each different type of business.

Individual businesses must take ownership of any negative effects created while

doing business. Any example of a business creating negative effects includes afactory creating pollution.

d) To drive Economic Development

Most countries desire to achieve a high rate of economic development. However,

the resources required to achieve the desired growth far exceeds the resources

of local private enterprise and spontaneous will proactively intervene throughthe concept of state entrepreneurship

e) Industrialization

Industrialization is the most important requisite for economic development.

Industrialization in the developing countries necessitates the extension

of the public sector. In the developing countries the state is the only force

that possesses the necessary levers for influencing the economy, the means

for mobilizing and properly utilizing financial, natural, labor and material

resources, applying scientific and technological achievements and overcominga number of difficulties and contradictions typical of developing countries.

f) Promotion of Science and Technology & Research

Scientific and Technological revolution has an important bearing on economicdevelopment.

The public sector has become the instrument for the development of science

and technology and also the vehicle for the application of scientific andtechnological achievements in industrial and agricultural production.

g) Planning

Economic planning also has provided a stimulus to public sector in many

countries. Expansion of the public sector is essential to make planning moreeffective.

h) Public Utilities

There are certain types of services known as public utilities such electricity, city

transportation, water supply, railways, etc., are the examples of public utilities.

The provision of these services needs huge investment. They are also

monopolistic in nature. It has been realized that these services can be provided

efficiently, economically and continuously only when the public utilities will beowned and operated by the state

i) Resource Allocation

The nature and pattern of resource allocation has an important bearing on

economic development. The main reason for the expansion of the public sector

in India, for example, lies in the pattern of resource allocation fixed in the plans.

The nature and volume of public investment substantially affects the tone andtexture of economic activity.

j) Prevent Exploitation

Sometimes the monopolist private producers have a tendency to reduce their

output and raise the prices, and thus exploit the consumers in the process.

Public takeover through nationalization a method by which exploitation ofconsumers can be prevented

5.1.4. PFM Legal Framework and Institution Arrangement

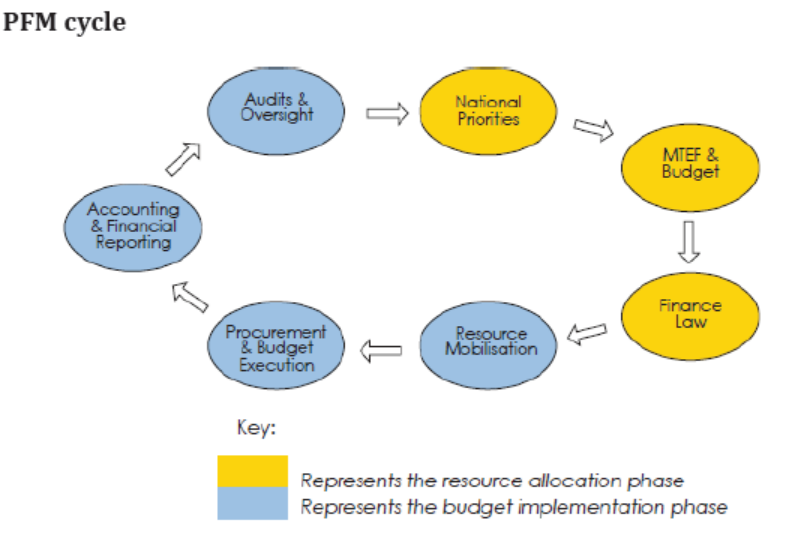

a) The public Finance Management Cycle

The government of Rwanda Public finance management(PFM) cycle entails

determination of national priorities, developing MTEF and the Budget,

preparation and approval of the finance law, resources mobilization,

procurement and budget execution, accounting and financial reporting, auditand legislative oversight.

The PFM cycle described above generally covers a three years’ period.

Therefore, at any one point in time, three years budgets are at different points

in the cycle: for example, in October of any year, the budget of the previous

year is being audited, the budget of the current year is being executed, and next

year’s budget preparation has already started.

b) PFM legal framework

Laws and regulations: The Government has put in place laws and regulationsto enforce an effective and functional PFM system.

– The 2003 Rwanda Constitution (as revised in 2015) especially

Articles, 162,163,164,165,167,166,167 dealing with the PFM functionof GoR.

– Organic Law No12/2013/OL on State Finances and Property of

2013 which is the principal law on the financial management withinthe Government of Rwanda and is subsidiary to the constitution.

Under Article 13 of Organic law on State Finance and Property; Minister has

the responsibility to enforce this Organic law and any prescribed norms and

standards including any prescribed standards of accounting practice and

uniform classification systems, in central and local Government administrativeentities.

– Ministerial order no 001/16/10/TC of 26/01/2016 relating to

Financial regulations, 2016 on the Organic on State Finances and

Property – which elaborates more on the implementation of theOrganic law on State Finances and Property of 2013.

– Laws and regulations on public procurement – which prescribe theprocurement procedures within the General Government

– Law establishing sources of revenues and property of decentralized

entities- which provides for the list of taxes, fees and other charges

levied by decentralized entities and determining their thresholds.

Law describes and regulates the sources of revenues for decentralizedentities in Rwanda.

– Laws on Taxes – which prescribe provisions, on which tax payers

including government agencies must also, adhere to in fulfilling taxobligations. They include:

i. Law on direct taxes on incomes as modified and complemented to date;

ii. Law establishing the value added tax

iii. Law on tax procedures as modified and complemented to date;

iv. Ministerial Order and Commissioner General’s governing direct taxes on

income; andv. Any other law or modifications to the above laws.

Human resource management and payroll – the following legislationsgovern human resource management and payroll:

• Law regulating labor in Rwanda;

• Law on general statutes for Rwanda Public service;

• Presidential Order governing modalities for the recruitment of public

servants;

• Presidential Order determining the amount of salaries and other

fringe benefits to state high political leaders and modalities of their

allocation;

• National employment policy;

• Guidelines for fixing salaries in the Rwandan Public Sector;• Any other law or modifications to the above laws.

– Asset management – underpinned by the following laws, regulation,

policies and procedures:

• Ministerial order determining the organization and functioning of the

asset disposal evaluation committee to set value for state private assets

to be sold, exchanged, donated or completely destroyed;

• The fleet policy of government of Rwanda;

• Law on disposal of state assets which determines the procedure

governing the disposal of State private assets; and

• The law governing privatization of public institutions and national

investment.

• Any other law or modifications to the above laws.C) PFM Institutional arrangements

In accordance with Article 61 and 65 of the 2003 Constitution of Rwanda asrevised in 2015, the PFM institutional framework of the GoR comprises of:

i. Legislature/Parliament – The Constitution establishes a bi-cameral

parliament comprising the Chamber of Deputies (Deputies) and the Senate

(Senators) to carry out legislative and oversight function by debating andpassing laws. It also legislates and exercises control over the Executive.

ii. The executive – Article 97 of The Constitution vests all executive power

on the President of the Cabinet. The cabinet is accountable to both the

president and parliament in accordance with the Constitution. TheCabinet through the Minister retains the overall financial accountability.

iii. The judiciary – The Constitution establishes the judiciary and provides

that the judicial authority is vested in the judiciary composed or ordinary

Courts and Specialized Courts. Courts consist of ordinary and specialized

Courts. Ordinary Courts are comprised of the Supreme Court, the High

Court, Intermediate Courts and Primary Courts. Specialized Courts arecomprised of Commercial Courts and Military Courts.

iv. The Office of Ombudsman – the Ombudsman as an independent public

institution to carry out the following responsibilities:

• To act as a link between the citizen and public and private institutions;

to prevent and fight against injustice, corruption and other relatedoffences in public and private administration;

• To receive and examine complaints from individuals and independent

associations against the acts of public officials or organs in order tofind solutions to such complaints if they are well founded;

• To receive declaration of assets of the president of the Republic, the

president of the Senate, the Speaker of the Chamber of Deputies, thePresident of the Supreme Court, The Prime Minister; other members of

the Cabinet and other public officers entrusted with the managementof state finances and property.

v. Office of the Auditor General – Under Article 65 of The constitution

provides for the Office of Auditor general and to complete the accountability

cycle, the Article 66 of The Constitution requires the Auditor General tosubmit an annual audited financial report to Parliament.

The audit report indicates the manner in which the budget was utilized,

unnecessary expenses which were incurred or expenses which were contrary

to the law and whether there was misappropriation or general misuse of public

funds.

Parliament reviews, debates and provides oversight function on the executive.

The Auditor general submits a copy of the report to the President of the republic,

Cabinet, the President of the Supreme Court and The Prosecutor General of the

Republic.

The Parliament, after receiving the report of the Auditor General referred to

in this article, examines the report and takes appropriate decisions within sixmonths.

5.1.5. Accounting Policies

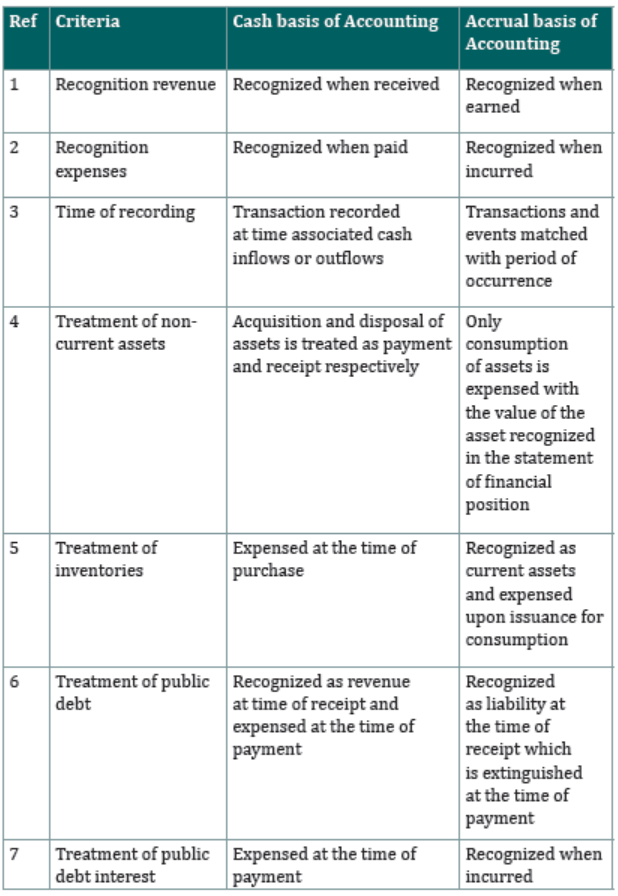

In general, there are two alternative bases of accounting:

i. Cash basis of accounting

ii. Accrual basis of accounting.

The cash basis of accounting is an accounting methodology under which

transactions and events are recognized in the books of accounts only when

cash and cash equivalents is received or paid by the entity. Therefore, the

transactions and events are recorded in the books of accounts in the period inwhich the associated cash flows occur.

Cash is defined as the cash on hand, cash at bank and demand on deposits.

Whereas, cash equivalents is defined as short term, highly liquid investments

(with maturity is less than three months from the date of purchase) that are

readily convertible to known amounts of cash and which are not subject to asignificant risk of change in value.

The accrual basis of accounting is an accounting methodology under which

transactions and other events are recognized in the books of accounts when

they occur (and not only when cash or cash equivalent is received or paid).

Therefore, the transaction and events are recorded in the books of accountsand recognized in the financial statements of the period to which they relate.

The following table shows a summary of differences between the two accountingbases:

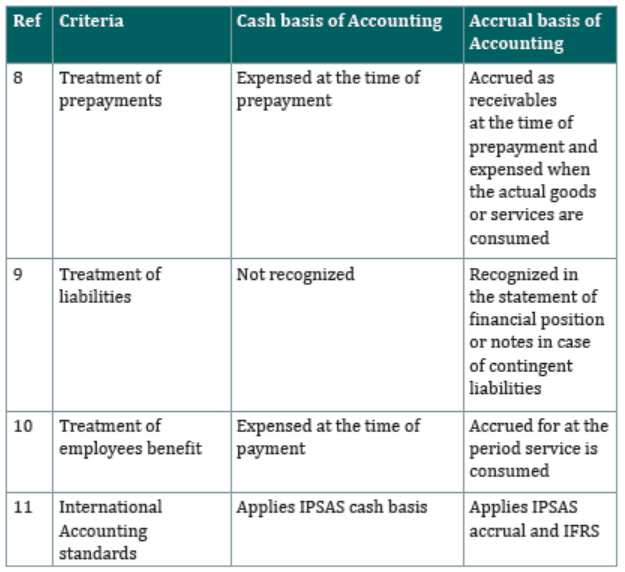

In between the basis of accounting described above, are the following modified

bases of accounting:

• Modified cash basis of accounting; and

• Modified Accrual basis of accounting

Under the Modified cash basis, the main basis of accounting is cash i.e. for all

intents and purposes economic transactions of a reporting entity are measured,

recorded, and reported on the basis of cash, with a few exceptions to the general

rule, where certain economic events are identified, measured, recorded andreported on, not strictly on receipt or payment, but are “accrued”.

Conversely where the main basis of recognizing, measuring, recording and

reporting on economic events and transactions is the “accrual basis” but the

reporting entity has allowed a few exceptions to the general rule, for example

certain of its expenses and or income are only recognized on cash payment

(cash outflow) or receipt (cash inflow), then the basis of accounting is referredto as “modified accrual basis”.

Except for the subsidiary entities affiliated to the centralized entities, public

entities were used to maintain their books of accounts on a modified accrualbasis of accounting.

The subsidiary entities affiliated to the decentralized entities were used to

maintain their books of accounts on a modified cash basis of accounting and

progressively move to the same accounting basis as that of the rest of the

public entities but now the Government of Rwanda is moving to accrual basisin maintaining its books of account.

Application activity 5.1

1. There are several arguments that justify government intervention

in economies. The following are included in these reasons withexception of:

A. Market Failure

B. Redistribution

C. Political ideology

D. Monetary Policy

2. Choose the most accurate statement among the following inrelation to Public Finance Management (PFM) cycle:

A. In Rwanda, the government’s national budget runs from 30 June to1 July

B. In Rwanda, budgets should be approved by the legislature, whichshould be able to effectively scrutinize government plans

C. In Rwanda, annual financial reports should be subject to dependentexternal audit and scrutiny

D. There should be no predictability but control in the budget execution

In public finance management, the three fundamental aspects totreasury management include:

i. The financing of operations in a way that minimizes funding costs andmatches cash flow needs

ii. The management of working capital

iii. The management of financial risks to which cash flows are exposed

A. (i) Only

B. (i), (ii)&(iii)

C. (i)&(iii) only

D. None of the above

5.2. Record Government Revenues and Expenditures

Learning Activity 5.2

You are hired as a public accountant, what are the minimum books ofaccounts will you keep?

5.2.1. Books of accounts

The finance department shall maintain the necessary books of accounts to

ensure that financial information is comprehensive. In keeping books of

accounts, double entry concept will be applied. This entails that a financial

transaction gives rise to two equal and opposite entries one debit and the other

credit.

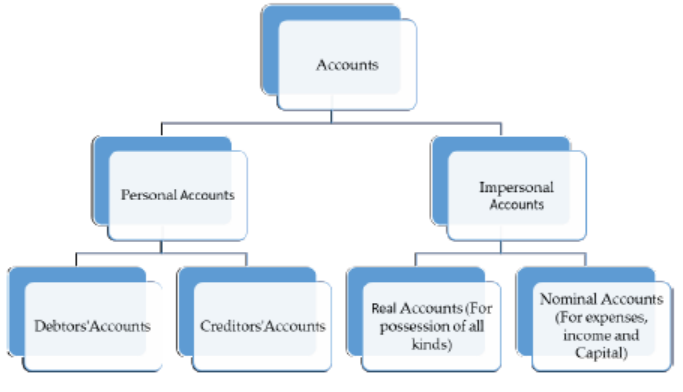

An account is a record in ledger form summarizing all the transactions that have

taken place to a particular event or activity that ledger record relates. These

can be classified as Personal and Impersonal Accounts. Personal accounts are

those that relate to debtors and creditors (customers and suppliers) while

Impersonal Accounts can be divided between Real account and Nominal

accounts. Real accounts are those in which possessions are recorded such as

buildings, machinery, fixtures and fittings, stocks while nominal accounts arethose in which expenses, income and capital are recorded.

Public entities should at a minimum maintain the following books of accounts

in electronic or manual form:

1. Cash book

2. Petty cash book

3. General ledger

4. Accounts payable ledger

5. Accounts receivable ledger

6. The journal

Note: Description of the books above have been seen in Senior 4 units 3 and 4

5.2.2. Government standard chart of accounts

1. Overview of the Standard Chart of Accounts

The Standard Chart of Accounts (SCoA) is a classification system by which

financial transactions are recorded. Article 97 of the Ministerial Order No.

001/16/10TC of 26/01/2016 relating to financial regulations requires the

Minister and upon the advice of the Accountant General to issue a standardised

Chart of Accounts generally applicable to all public entities excluding public

institutions. Under the regulations, public institutions are empowered to

develop their own chart of accounts adapted to their financial operations. The

SCoA provides a basis for a uniform budget classification and execution. It is

mandatory for all Government entities within general Government to use the

coding structure of SCoA to budget and execute the budget. For entities using

IFMIS, the SCoA is already set up in the system, however, for entities using standalone systems the SCoA has to be set independently.

Consistent with Article 97 of the Ministerial Order No 001/16/10/TC of

26/01/2016

Relating to financial regulations, the coding structure of the SCoA comprises

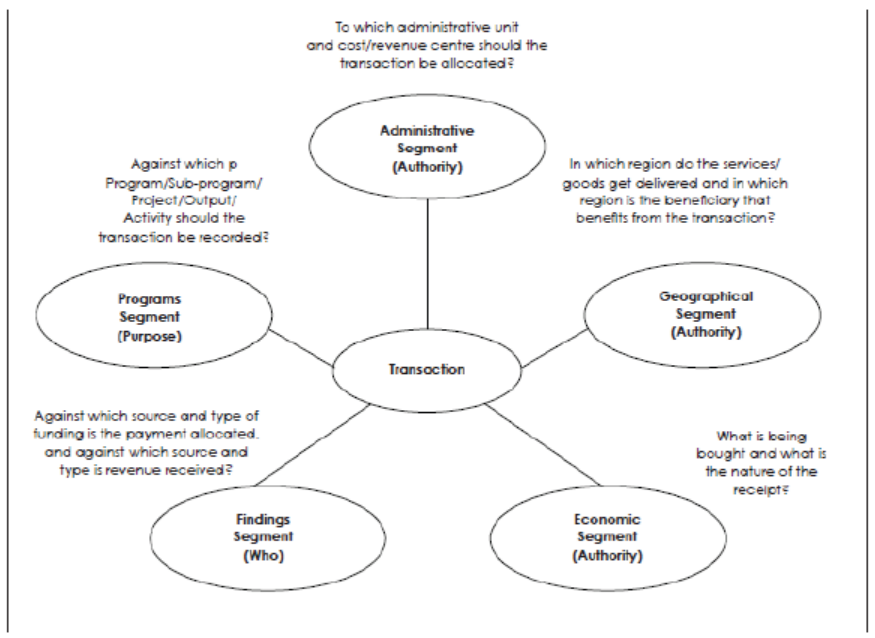

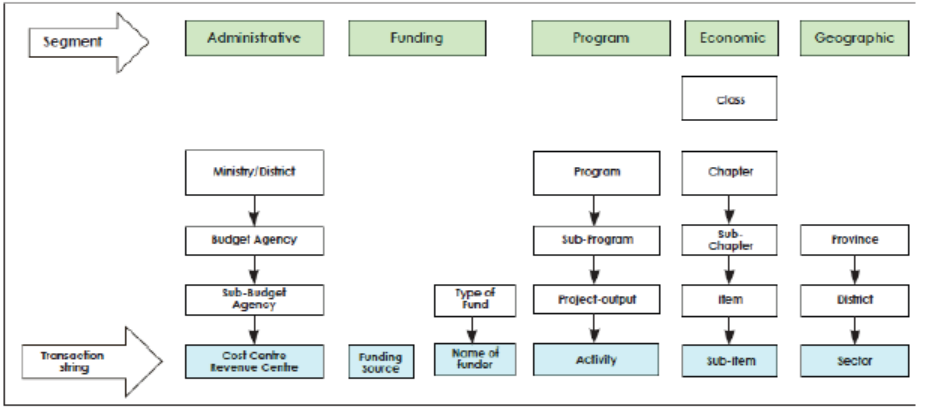

five segments. When recording a transaction, a selection must be made from

each of the five segments, meaning that all segments must be used for recordinga single transaction by answering the questions provided in the diagram below:

1. The structure of the SCoA

The diagram below illustrates the structure of the SCoA of the Government and

shows the interaction between the segments and classifications within eachsegment

The following is a description of each of the five segments of the SCoA:

a) Administrative Segment

This is based on administrative responsibility, which Executive (Ministry/

District) has overall responsibility and accountability for the inflows and

outflows of financial and other resources, and also provides for the lowerdelegated levels of responsibility and accountability.

The administrative segment provides for four levels as follows:

• Level 1 – Ministry/District: represents the highest level of administrative

responsibility

• Level 2 – Public entity: represents the public level where budget

appropriations are made.

• Level 3 – Sub public entity: at the disposal of the public entities which

may wish to drive accountability to lower levels of their structures.

• Level 4- revenue/cost centre: at the disposal of the public entities whichmay wish to drive accountability to lower levels of their structure

b) Fund Segment

This segment defines the source and type of funding. The segment helps track

revenues and expenditures per source and type of funding. The segment applies

to both revenues (inflows) and expenditures (outflows). “Source of funding”defines the source of funding for inflows.

In broad term, there are two broad sources of revenues – Domestic and External

sources. Domestic sources may be from Government of other local institutionsand individuals.

c) Program/Function/EDPRS Segment

This segment defines the purpose of the transactions through programmatic

classification. The Government programmes and sub-programmes reflectGovernment policy, goals and objectives.

d) Economic Segment

This segment defines the natural accounting nature of the transaction, visà-

vis, revenue, expense, asset, liability and capital (consolidated fund).

The classification includes the five (5) classes accordingly. The economic

classification is closely aligned to the GFS system in terms of operating revenuesand expenses.

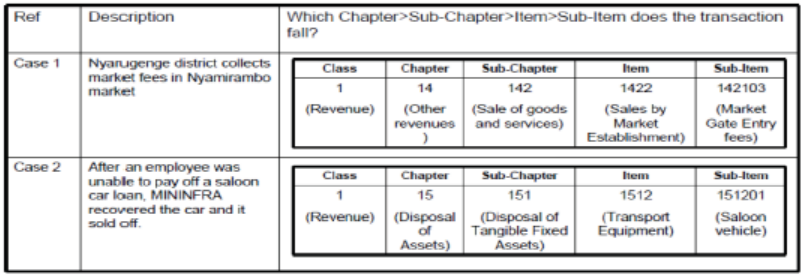

The categorisation for economic item under the chart of accounts is classifiedas follows: Class – Chapter – Sub-chapter – Item – Sub-item.

The following illustrates coding under the economic segments of the SCoA:

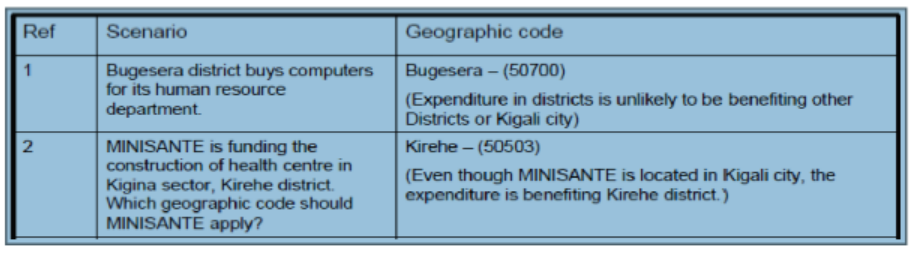

e) Location Segment

The geographical segment defines where the authority for budget execution

(e.g. expenditure) lies. However, some expenditure made centrally for example

in a Ministry Headquarters will actually be benefiting the people in a district,

e.g. the building of a district hospital or school.

This segment comprises 5 digits and provides for classifying the beneficiary

of the spending by Province, District (Akarere) and Sector (Umurenge).The following illustrates coding under the location segments of the SCoA:

3. Updating the Government SCoA

The accountant General may on his or her own or, on the proposal of a Chief

Budget Manager modify the Chart of accounts. The final authority for updatingthe chart of accounts rests with the Accountant General.

The following procedures will be followed in updating the chart of accounts:

a) Where a Chief Budget Manager has identified the need for new accounts

codes, he or she apply to the Accountant General for the new codes.

b) The Accountant General shall review the request submitted and

determine whether it is justified after making any consultations that he

or she may consider necessary. Where the request is not justified and

the existing Chart of accounts can be used to track the transactions, the

Accountant General shall advise the Chief Budget Manager on whichcodes to use and how to report on their transactions.

The Accountant General shall publish the updated CoA whenever an updates ismade

5.2.3. Purpose of Government Accounting

The purposes of government accounting include:

• Demonstrating the proprietary of transactions and their conformity

with the law, established rules and regulations

• Measuring current performance

• Providing useful information for the efficient control and effective

management of government operations

• Facilitating audit exercise to be carried out

• Planning future operations• Appraising those in the authority, in efficiency and effectiveness

Users of Government Accounting Information

There are two groups of users of Government Accounting information: internaland External.

Internal Users and Interest Areas

This group of users includes:

• The Labour union in the public service which will press for improved

conditions of employment and security of tenure for their members.

• The Members of the Executive Arm of Government: such as the

President, Ministers, Governors, and Mayors. Their interest areas

are to ensure probity and accountability through score keeping

and performance control which are achieved through accountinginformation.

• The Top Management members: Permanent Secretaries of various

Ministries for example. They are the conduit of accounting information

generation and transmission and serve as liaison officers betweenGovernment, employees and the public.

External Users and Areas of Interest

External Users include

• Members of the Legislature at both National, State and Local

Government levels. Information in the accounts of Government is the

major media through which politicians render stewardship to their

constituencies and appraise them of the endeavours of governance.

• The Members of the Public, to demonstrate accountability and assistthe people to appreciate or otherwise the efforts of Governments

• Researchers and Financial Journalists: Researchers are expected

to develop new and better ideas of governance. Financial journalists

cherish accounting information to advise existing and potentialinvestors.

• Financial Institutions, such as Commercial Banks, World Bank,

International Monetary Fund. Accounting information assists them toevaluate the credit rating of a borrowing Nation.

• Governments, apart from the ones reporting: Governments

collaborate on ideas of investment and research. They requireaccounting information on the well-being or otherwise of each other.

• Suppliers and Contractors: Suppliers and contractors are eager to

ascertain the ability of a Government to pay for goods and servicesdelivered. Only Accounting information can be revealing.

5.2.4. Source of Government Finance

The Government revenue means the amounts which are received by the

Government during a particular year. In other words, the income of the

Government is known as public or government revenue. The sources may beclassified as:

1. Internal sources

2. External sources

These sources are explained as under:

I. Internal sources

Internal sources consist of those amounts which are received by the Government

internally or from the individuals of the country. The main internal sources ofrevenue of Rwanda Government are:

• Direct taxation

This taxation includes income tax, corporation tax and capital gains tax. About

70% of Rwanda Government’s revenue comes from direct taxation.

• Indirect taxationIndirect taxation includes:

1. Tax on domestic manufacturers

2. Customs duty on import and exports

3. Excise duties: It is duty imposed mostly on production activities for

sales purposes, largely collected at manufacturing stage, showingdownward trend

4. VAT

Indirect taxation is the major source of Government revenue from internal

sources. This taxation contributes about 50% of Government revenue inRwanda.

• License fees

The Government of Rwanda receives fees from business and trading licenses,

license fees under traffic act and other miscellaneous licenses. This sourcecontributes about 5% of Government revenue in Rwanda.

• Fines and penalties

Fines and penalties is another source of revenue. These fines and penalties

are imposed on the individuals for not obeying the laws, rules and regulations

of the country. This source contributes about 5% of total income of RwandaGovernment from internal sources.

• Sale of goods, services and properties

The Government also receives income from the sale of different goods and

services properties. About 3% to 4% of income of Government of Rwandacomes from this source

• Rent

Closed school buildings, empty state-owned buildings, and park shelter and

reception facilities are examples of facilities that can be rented out. Government

agencies also earn rent proceeds for the use of property by other agencies. For

example, if the federal government needs space in a small town, the feds might

arrange to rent out an unused office in the town hall from the municipality.Unusable properties are sold off.

• Investments

Government sometimes uses revenues as a means of earning interest and

dividends. While the investment might be made up of tax francs, the interest,

dividends and capital gains are considered non-tax revenue. The investment

opportunities might be in the form of mutual funds, bonds, foreign exchange

rates and government-backed loans to businesses and individuals, such assmall business loans and mortgages.

• Grants and Gifts

Gifts are Voluntary contributions by individuals or institutions to the

government. Gifts are significant source of revenue during war and emergency.

A grant from one government to another is an important source of revenue inthe modern days.

The government at the Centre provides grants to State governments and the

State governments provide grants to the local government to carry out their

functions. Grants from foreign countries are known as Foreign Aid. Developing

countries receive military aid, food aid, technological aid, etc from developedcountries.

• Borrowings

The government may force various individuals, firms and institutions to lendto it at a much lower rate than the market would have offered.

• Other sources

In addition to the above sources, the Government receives income from some

other miscellaneous sources. These sources contribute a small amount ofGovernment revenue.

II. External sources

External sources of Government revenue consist of external loans and grants.

These loans and grants are obtained by the Government for development

purposes. These loans and grants are the main sources of income of capitalbudgets.

These loans and grants are obtained from different countries and international

organizations. The Rwanda government obtains loans and grants mainly from

the U.S.A, Germany, Japan, Netherlands, Denmark, U.K and so on.

The main international organizations which provide loans to Rwanda are World

Bank, African Development Bank, International Monetary fund, Arab League,European Economic Community, International Development Agencies, etc

Government expenditure

Government expenditure means those amounts which are spent by the

Government for different purposes. The Government expenditure may beclassified as:

a) Recurrent expenditure

b) Development expenditure

These are explained as under:

Recurrent expenditure

Recurrent expenditure means revenue expenditure. This expenditure is

incurred by the Government on normal activities. The amounts which are

spent by the Government on regular activities like defense, health, education,

administration, etc, are referred to as recurrent expenditure the mainexpenditure heads of recurrent expenditure are:

General public administration

This expenditure is incurred on general administration of the country. About10% to 15% of total expenditure in Rwanda is incurred for this purpose.

Defense

Defense of the country is of great importance for its stability. The government

of Rwanda spends about …. % of recurrent expenditure on the defense. Thispercentage is very low as compared to other countries.

Education

Education is the main priority of Rwanda Government. About 20% to 25% ofrecurrent expenditure is incurred on education.

Health

The government spends on health facilities. About 6% of recurrent expenditureis incurred for providing health services.

Social welfare

The government of Rwanda spends on social services like housing, sports; etcthe share of this head in total recurrent expenditure is about 2%.

Economic services

The government of Rwanda spends huge amounts on providing economic

services. These include agriculture, forestry, fishing, electricity, gas, water,

transport and communication, etc. About 16% of total recurrent expenditure isincurred for this purpose.

Other services

There are some miscellaneous items of recurrent expenditure. About 30% oftotal expenditure is incurred for this purpose.

Development expenditure

Development expenditure is incurred for the establishment of new agricultural

and industrial projects, installation of new plant and machinery, constructionof new roads and buildings, purchase of new equipments etc.

Development expenditure is mainly financed from external loans and grants.

Internal borrowing is also another source of financing the developmentexpenditure. Development expenditure is shown in capital budget.

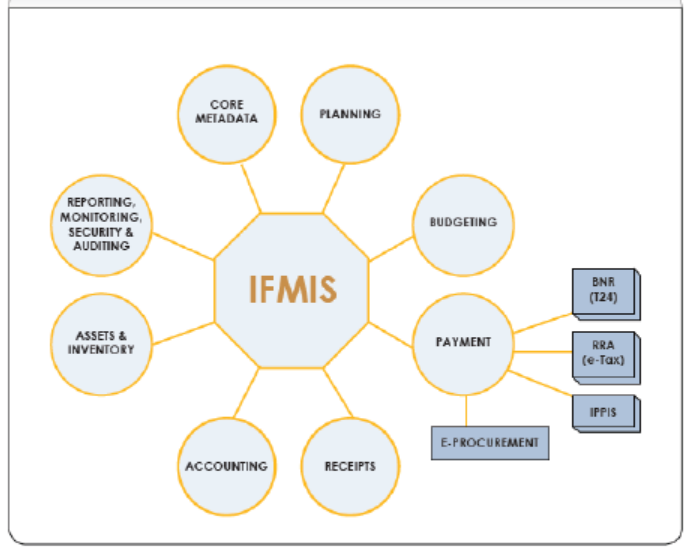

5.2.5. Role of IFMIS in Effective PFM

The Government has put in place an Integrated Financial Management

Information System (IFMIS) as the principal system of Government for

financial management. It is intended that the system will cover all the General

Government entities with the implementation being carried out in a phasedmanner. Accordingly, the IFMIS shall be used for the following purposes:

• Centerpiece of the government financial management processes of

planning, budget preparation, budget execution, revenue management,

inventory management, assets management, accounting and financial

reporting.

• Preparing financial management reports: these enable improved

management decisions making through provision of real time financial

statements.

• Harmonizing processing of transactions: transaction processing across

Government is made uniform through use of SCoA therefore offering a

common integrated enterprise platform for consistency in process and

procedures;

• On-line inquiries: users can access the system from any location with

the required authorization details;

• Controls for commitments, expenditure and budgetary adjustments

are made possible; and

• Special accounting needs such as development projects and special

funds are also provided.The figure below summaries the typical structure of the IFMIS

5.2.6. Recording Government Revenue and Expenditure

Although the recording of government revenue and expenditure is based on

the concept of double entry but the procedure of recording transactions in the

government sector is different from a commercial enterprise. In the governmentsector, the theory of fund accounting is followed.

A fund is an independent fiscal and accounting entity with resources and

obligations. Each government unit can be regarded as a fund and complete

accounting records maintained for each fund. There are various government

ministries and in each ministry there are various departments. For example,the ministry of commerce has the following departments:

General administration and planning

• Department of internal trade

• External trade services• Inspectorate of weights and measures

Each department of the ministry of commerce can be regarded as a separatefund.

Major steps in the government accounting in Rwanda are the following:

Annual estimates

These estimates are prepared by the various ministries and these submitted to

the treasury. These estimates include revenue and expenditure figures for thenext year.

Presentation of the budget

The Minister of finance presents the budget for the next financial year before

the parliament in the month of June every year. The financial year of thegovernment starts from 1st July and ends on 30th June next year.

The budget contains the estimate of government revenue and government

expenditure for the next year. The various proposals of the budget are

debated in the parliament. After the approval of the parliament the budget isimplemented.

Spending by Ministries

Some specific amounts are appropriated by the Parliament to different

ministries. The government ministries can spend the amounts appropriated

to them. Appropriated amounts can be used by the ministries to perform theirduties, there are different vote numbers assigned to different ministries.

These votes may be further divided into recurrent (R) and development (D)

votes. These vote numbers are used for reference purposes. For example, vote

R- 11 and D11 are recurrent and development vote numbers for the ministry

of health. In each Ministry, there are sub votes for different departments of anyministry.

The Fund System of Governmental Accounting

Public funds are monies owned by the Nation and controlled and applied by

the central government for public works and services. In Rwanda, all resources

(revenue from tax, non-fiscal revenues) are recorded into a fund known as

a consolidated fund. The consolidated fund account is kept by the treasury

under the ministry of finance, and all revenues and grants received by the

Government are paid into this account. No money can be withdrawn from this

account without approval of Parliament, i.e. Parliament is the sole signatory tothis account.

The fund accounting system is a concept which is used to describe how

government resources are accounted for from one major fund source. The word

fund is therefore used to describe the whole government set up as one big fundin terms of structure.

Governmental fund

Government funds are used to finance general government activities such as

police and fire protection, courts, inspection, and general administration. Most

of their financial resources are subsequently budgeted (Appropriated) forspecific “general government” uses (expenditures) by the legislative body.

Government funds include:

– The general Fund

– Special Revenue Fund

– Capital Project Funds

– Debt Service Funds

The accounting equation of most governmental funds is:

Current Assets – Current Liabilities = Fund Balance

Thus, Governmental funds are essentially “Working capital” funds and their

operations are measured terms of sources and uses of working capital, that itis, changes in working capital.

When Fund Balance is positive, there is a greater likelihood that the government

will pay it is liabilities. When Fund Balance is negative, short term creditorsmay not be paid, and public organization may be forced into bankruptcy.

A. The General Fund

The primary governmental is used to account for most routine operations of the

governmental entity. All general governmental resources that are not required

to be accounted for in another fund are accounted for in the General Fund.

– General fund revenue consists primarily of taxes (Property, sales,

income, and excise), licenses, fines, and interest.

– General fund revenue expenditures are budgeted and appropriated forby council or other legislative body.

Typical journal entries include:

a) To record the budget :

Estimations revenues XX

Appropriations XX

Fund Balance for the last year XX

Note: The budgetary entry causes the Fund Balance account to be carried

during the year at it is planned end of year balance.b) To record revenues

Cash or receivable XX

Allowance for collectives’ receivables XX

Revenues XX

c) To record collection of receivables and write off of uncollectible

Cash or receivable XX

Receivable XX

Allowance for uncollectible receivables XX

Receivable XX

d) To record purchase order issued or contract commitment

Encumbrances (Expected expenditures) XX

Reserve for encumbrances XX

e) To record Expenditures upon receipt of invoice

Reserve for encumbrances XX

Encumbrances (Expected expenditures) XX

Expenditures (Actual cost) XX

Vouchers Payable XX

Note: While goods and services committed for by purchase order or other

contract are encumbered in governmental funds to avoid overspending

appropriations, many expenditures are controlled by other means and need

not to be encumbered. For example, wages are set by contract and controlledby established payroll procedures and are not encumbered.

f) To record supplies

Supplies inventory XX

Fund Balance reserve for supplies inventory XX

The supplies inventory indicates that portion of fund balance is not available

Note: This customary entry compounds these two more proper entries.

6a. Supplies inventory XX

Fund Balance XX

6b. Fund Balance XX

Fund balance reserve for supplies inventory XX

The entry (ies) would be reversed had supplies inventory decreased. The

increase (decrease) in supplies inventory is reported as an “other Financing

Source (Use)” in the governmental fund “Operating Statement”, the statement

of Revenues, Expenditures, and Change in Fund Balance.g) To record closing entries at year end

Revenues XX

Appropriations (budgeted) XX

Collection of prior year error XX

Fund balance (difference – Debit or credit) XX

Estimated revenues XX

Expenditures XX

Encumbrances XX

Cumulative effect of change in accounting XX

Appropriations is the authorizations of asset outflows of uses estimated offund working capital

h) To record encumbrance reversing entry – beginning of next year

Encumbrances XX

Fund balances (reserves) XX

The encumbrance system is used in most governmental fund to prevent over

expenditure and to demonstrate compliance with legal requirements. When itcomes to close the end of fiscal year the encumbrance account is credited.

B. Special Revenue Funds

They are used to account that are externally restricted or designated by the

legislative body for specific general government purposes. For example, motor

fuel taxes used to finance the provincial road construction would be accountedfor in a Special Revenue Fund.

C. Capital Project Funds

The capital project funds used to account for acquisition and use for financial

resources to construct or otherwise acquire long-lived general government real

property and equipment. For example, to construct a new city hall, conferencecenter, stadium, Airport.

D. Debt Service Funds

The Debt Service Funds used to account for repayment of all general government

long term debit recorded in the General Long Term Debt Account Group and

payment of related interest and fiscal agent charges. Debit Service Fund

budgetary may be used to record the estimated revenues (e.g., from taxes),

estimated other financing sources (e.g. from inter fund transfer from GeneralFund) and estimated income (e.g., from investment)

Example:

1. To record tax revenues and other financing sources

Cash or receivables XX

Allowances for uncollectible taxes XX

Tax revenues XX

Operating transfer from General Fund XX

2. To record investment made

Investment XX

Cash XX

3. To record investment income

Cash XX

Investment revenues XX

4. To record expenditures for debt principal retirement (at maturity date)

and interest (at due date)

Expenditures XXBonds payables (At maturity date) XX

Interest payable XX

5. To record payment of matured debt and interest due

Bond payables XX

Interest payable (At maturity date) XX

Cash XX

E. Account groups

Account groups are memorandum list and offset accounts that provide a record

of general government fixed assets and long term debt, which are not recordedin the governmental funds.

Account groups include:

The general Fixed Assets Account Group (GFAAG)

The account group accounting equations are:

GFAAG: General Fixed Assets = Investment in General Fixed Assets

GLTDAG: Amount Available in Debt Service Fund for GLTD Retirement

+ Amount to be provided in Future Years for GLTD Retirement

-------------------------------------------------------------------------

= General Long Term Debt Payable

Example for some records:

1. To record general fixed assets (e.g., Police cars fire trucks) acquired theGeneral Fund or Special Revenue Funds:

Machinery and equipment (Police cars or fire trucks) XX

Investment in General Fixed Assets XX

2. To record general long term debt incurred

Amount to be provided for payment of bonds XX

Amount to be provided for payment of long-term notes XX

Amount to be provided for payment of capital lease principal XX

Bonds payable XX

Long term notes payable XX

Capital lease (Principal) payable XX

Proprietary Funds

Proprietary funds are used to finance a government’s self-supporting “businesstype” activities (e.g., utilities).

Proprietary funds include:

– Enterprise Funds (Electricity, Gas, water)– Internal Service Funds (supplies, photocopies)

The accounting equation of proprietary funds:

curr. Assets + Fixed Assets +Other Assets

−Curr.Liab.+ Long term Debt +Contrib.Capital

+Retained Earnings

The accounting equation of proprietary funds is identical to that of a business

corporation, it includes accounts for all related assets and liabilities, not just

for current assets and current liabilities as well as for contributed capital andretained earnings.

Proprietary fund operations are measured in terms of revenues earned,

expenses incurred, and net income or loss.Sample entries:

1. To record operating revenues :

Cash XX

Revenue from sale XX

Revenue from appliances XX

Revenues from Other XX

2. To record governmental grants for operating and capital purposes

Cash or receivables XX

Cash construction XX

Revenues – State grants XX

Contributed capital (Capital Grant) XX

3. To record operating expenses

Expenses - cost electricity purchased XX

Expenses – depreciation XX

Expenses – Salaries and wages XX

Expenses – other XX

Accumulated depreciation XX

Cash XX

Payable XX

4. To close the account at year-end

Revenues from sales XX

Revenues from sale of appliances XX

Revenues – State Grants XX

Revenues from Other XX

Expenses –cost purchased XX

Expenses –depreciation XX

Expenses Salaries and Wages XX

Expenses – Interest XX

Expenses – Other XX

Retained earnings (Dr or Cr) XX

– The General Long-Term Debt Account Group (GLTDAG)

Fiduciary Funds

Fiduciary Funds are used account for government’s fiduciary or stewardship

responsibilities as an agent (Agency Funds) or trustee (Trust Funds) for othergovernments, funds, organizations, and or individuals.

Fiducially funds include:

– Nonexpendable Trust Funds (e.g., Donations)

– Expendable Trust Funds (e.g., library books)

– Pension Trust Funds (Pension, retirement)– Agency Funds (e.g, City, Schools district…)

Expendable Trust Funds are accounted for like governmental funds, and

both nonexpendable Trust Funds and Pension Trust Fund are accounted for

like proprietary funds. Agency Funds are purely custodial (Current Assets =Current Liabilities).

For agency Funds, the government has no equity. Further, Agency Funds do not

have operating accounts and no operating statement is prepared for AgencyFunds.

F. Some Special Funds

In relation to fund accounting in the public sector, there are some special fundswhich are established. These are explained as under:

a) Trust funds

Trust funds are those funds whereby the government receives money in

the capacity of a trustee e.g. Survivors fund, widows and children’s pension

fund. In this fund, all married civil servants contribute a certain amount of

their monthly salaries and they get the refund on the retirement. Some other

examples of trust funds are former known as National Social Security Fund(N.S.S.F) and RAMA. (Currently known as RSSB: Rwanda Social Security Board)

A trust fund is an independent accounting entity. It may own some property

and other assets like investments etc. Withdrawals from a trust fund are made

in accordance with some statutory provisions. A trust fund is also known as afiduciary fund.

b) Sinking funds

These funds are created with the purpose of the repayment of public debts.

Mostly, these funds are set up by the approval of the Parliament. Some annual

appropriations are made in these funds. The amounts appropriated are

invested to earn some interest. When any public debt matures then the sinkingfund is used to redeem this debt.

c) Revolving funds

These funds are also set up by the approval of the parliament. These funds

provide the financial resources for achieving some specified objectives.Some Government enterprises are set up through revolving funds. The initial

appropriation in these funds is made out of the consolidated fund. The receipts

generated in such funds are automatically used by the respective enterprises inaccordance with the provisions of the Act that set up the fund.

d) Capital project funds

The purpose of capital project is to provide resources for the completion of

some specific capital project. Main sources of financing include the proceeds of

bond issues, grants and transfers from other funds. A separate capital projectfund is created for each major project.

Conclusion

Most governmental fund accounting systems use both budgetary accounts andregular accounts

– Budgetary accounts are nominal accounts used to record approved

budgetary estimates of revenues and expenditures (appropriations)

– Regular accounts are used to record the actual revenues, expendituresand other transactions affecting the funds

The followings accounts are usually employed in governmental funds:

– Estimated revenues: Estimated sources of fund working capital.

The estimated account is debited to record the revenue budget and i

closed at the end of the period.

– Appropriations: Estimated uses of fund working capital (except for

other financing uses). The appropriation account is credited to recordthe budgeted expenditures and is closed at the end of the period.

– Revenues

– Other financing sources: Non revenues sources

– Expenditures

– Fund balance and Reserve

Application activity 5.2

A police department orders some stationary on 11 December 2012. On

15 December 2012, the police department received an invoice requesting

payment for the stationary that had been ordered. Payment was requested

to be made by 11 January 2013 but the police department actually paid for

the stationary by same-day bank transfer on 3 January 2013. The stationary

order was delivered to the police department and signed as received on 28December 2013.

The police department’s financial year runs from 1 January to 31 December.

Compare how the police department would report the stationary orderunder:

a) Cash basis

b) Modified cash basis, with one month specified periodc) Accruals basis

5.3. Preparation of financial statements for publicinstitutions

Learning Activity 5.3

Your District Accountant is hiring you to help him in closing the financialperiod due to the numerous activities to be done during a given period.

Required: Discuss any five financial statements that you will need toprepare for your District.

General guidance relating to preparation of financial statements

Financial statements must present fairly the financial position, financial

performance and cash flows of an entity to ensure that the users of financial

statements are provided with useful information for decision making

purposes. The general qualitative characteristics of financial reporting are:

• Understandability – the information must be readily

understandable to users of financial statements. This means that

information must be clearly presented, with additional informationsupplied in the supporting notes as needed to assist in clarification.

• Relevance – The information must be relevant to the needs of the users,

which is the case when information influences the financial decisions

of users. This may involve reporting particularly relevant information,

or information whose omission or misstatement could influence thefinancial decisions of users.

• Reliability – The information must be free of material errors and bias,

and not misleading. Thus, the information should faithfully represent

transactions and other events, reflect the underlying substance of

events, and prudently represent estimates and uncertainties throughproper disclosure.

• Comparability – The information must be comparable to the financial

information presented for other accounting periods, so that users

can identify trends in the performance and financial position of thereporting entities.

• Going concern assumption – When preparing financial statements,

a public entity is required to assess whether it can be assumed that it

is able to continue as a going concern. Generally, financial statements

of a public entity are prepared on going concern basis unless there

is an intention to liquidate the entity or discontinue business or

administrative operations or there is no alternative but to do so. Suchuncertainties must be disclosed.

• Consistency of presentation – The presentation and classification of

items in the financial statements must be consistent from one period

to another unless required otherwise by a significant change in thenature of the entity’s operations or a change in one or more IPSASs.

• Materiality and aggregation – Each material class of items in the

financial statements must be presented separately. Aggregating items

of a different nature or function is permitted only if they are immaterialindividually.

• Offsetting – Assets and liabilities, and revenue and expenses, may notbe offset.

• Comparative information – comparative prior period information

must be presented for all amounts shown in the financial statements

and notes to the extent relevant for understanding of the currentperiod’s financial statements

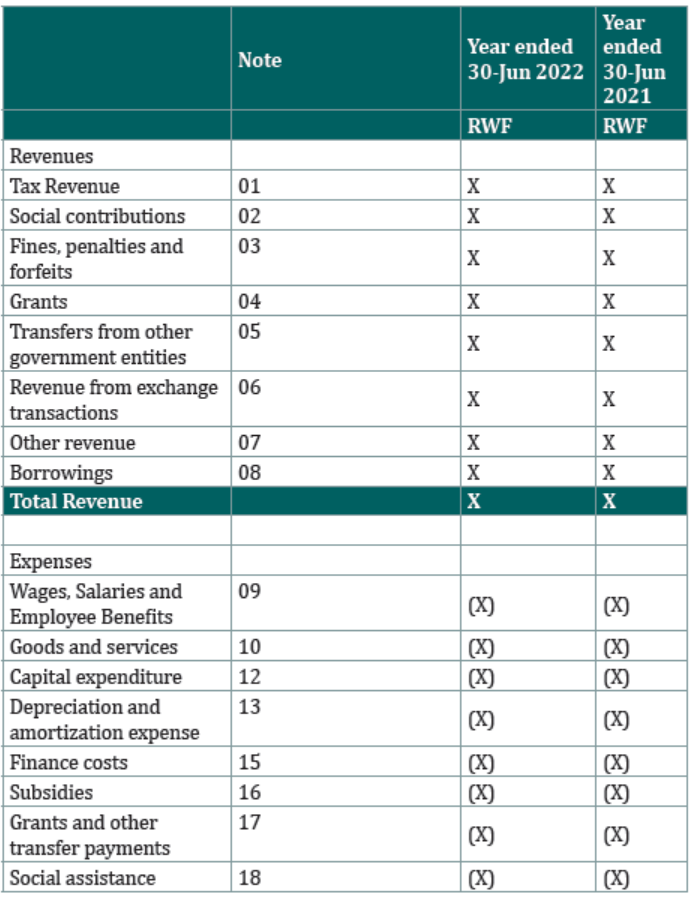

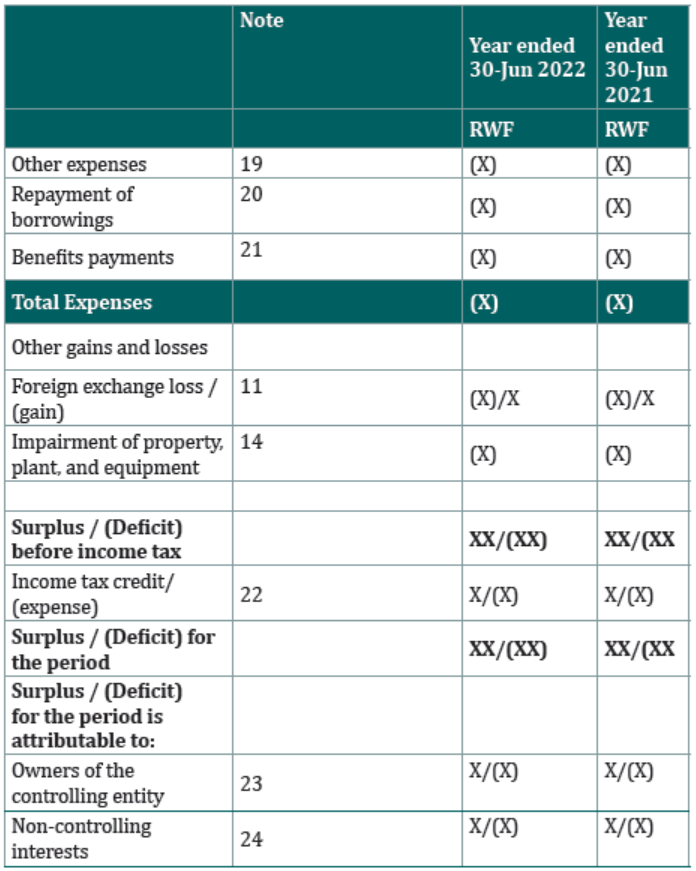

5.3.1. Statement of financial performance

Statement of performance is a financial report which shows revenues andexpenditures.

The following illustrates the format of statement of performance:

Statement of Financial Performance

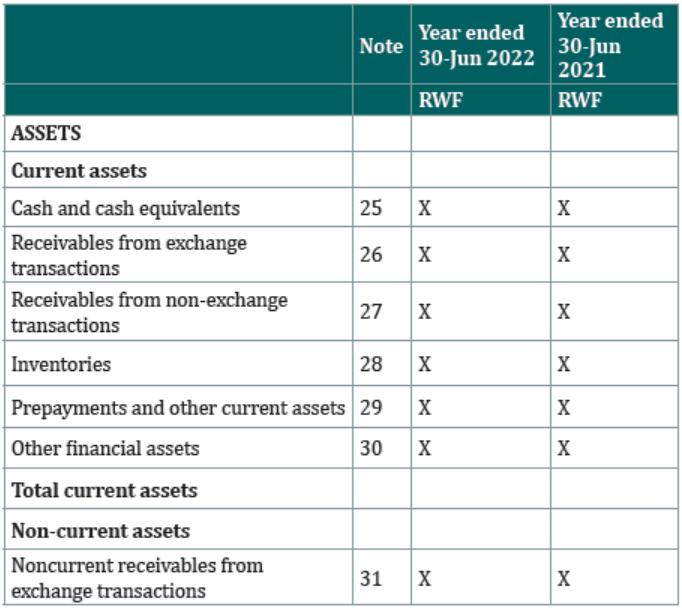

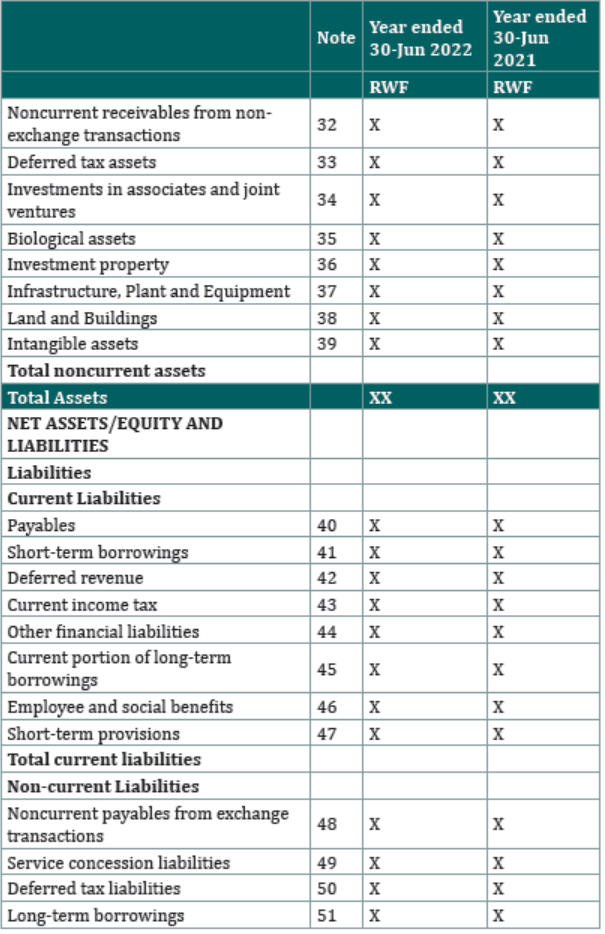

5.3.2. Statement of financial position

Statement of financial position is a statement showing at a given date, assetsand liabilities of an entity.

The following illustrates the format of statement of financial position:

Statement of Financial Position

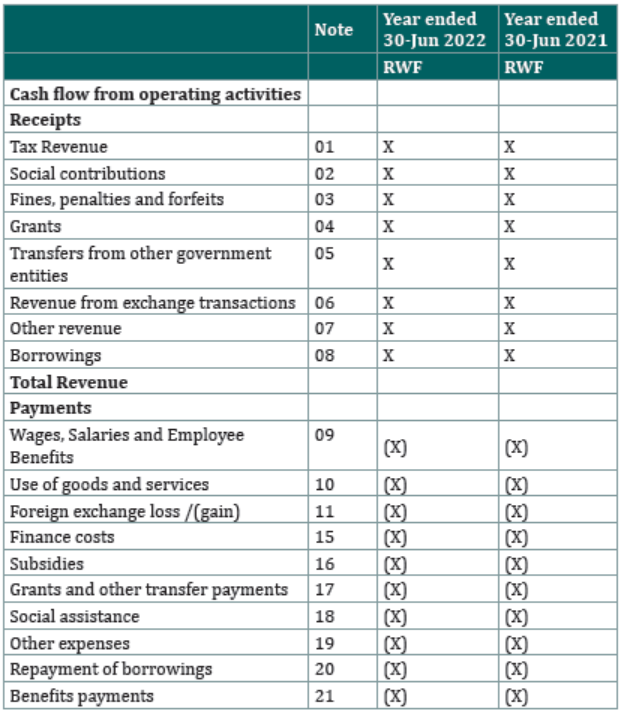

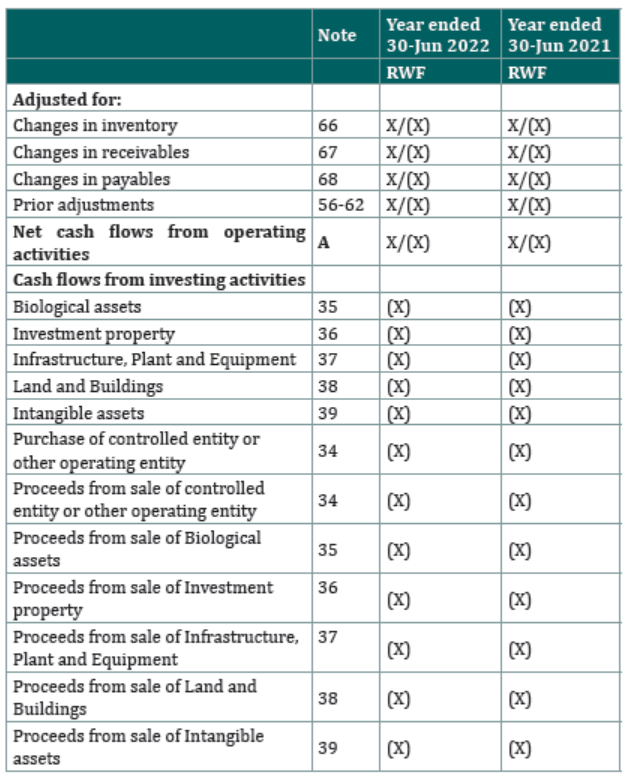

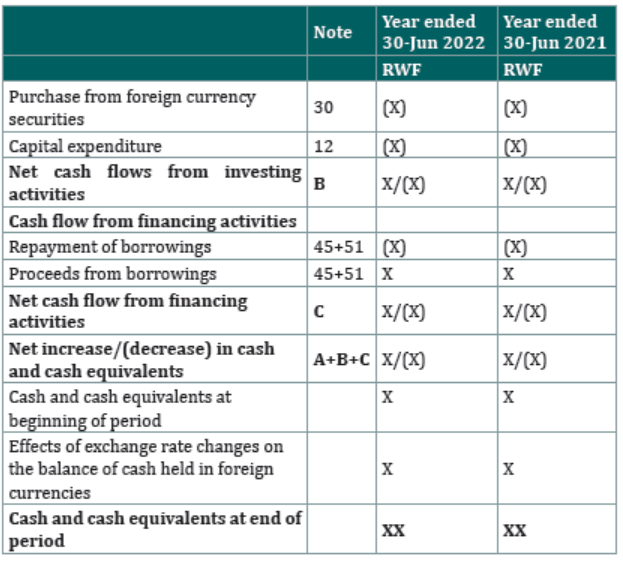

5.3.3. Statement of cash flows

This statement shows, at a given date inflows and outflows of cash and cashequivalent.

Statement of Cash Flows

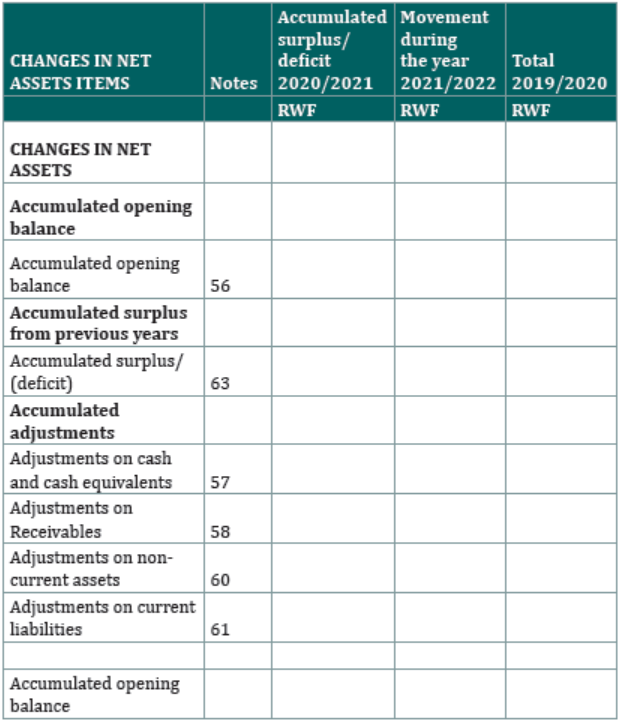

5.3.4. Statement of change in net assets

Statement of Changes in Net Assets/Equity

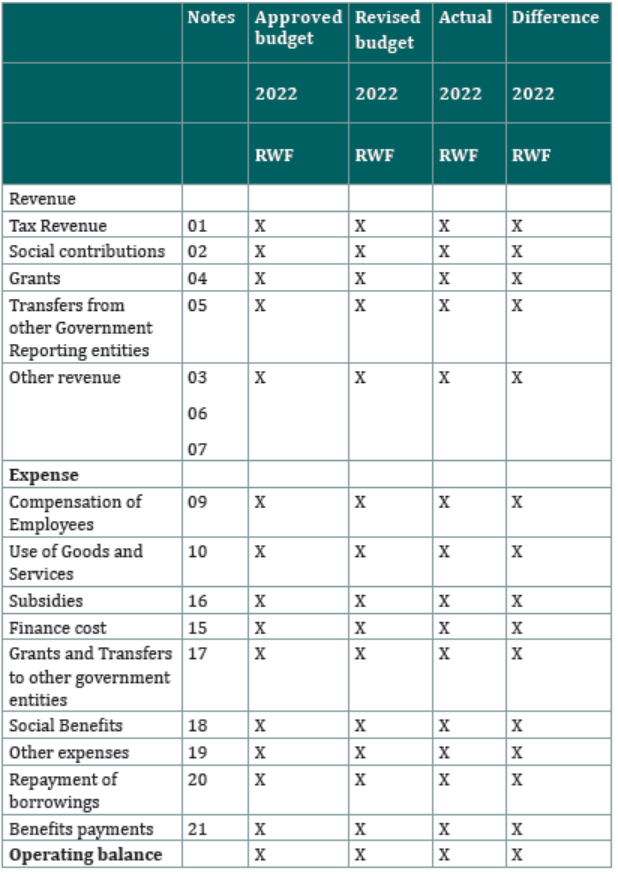

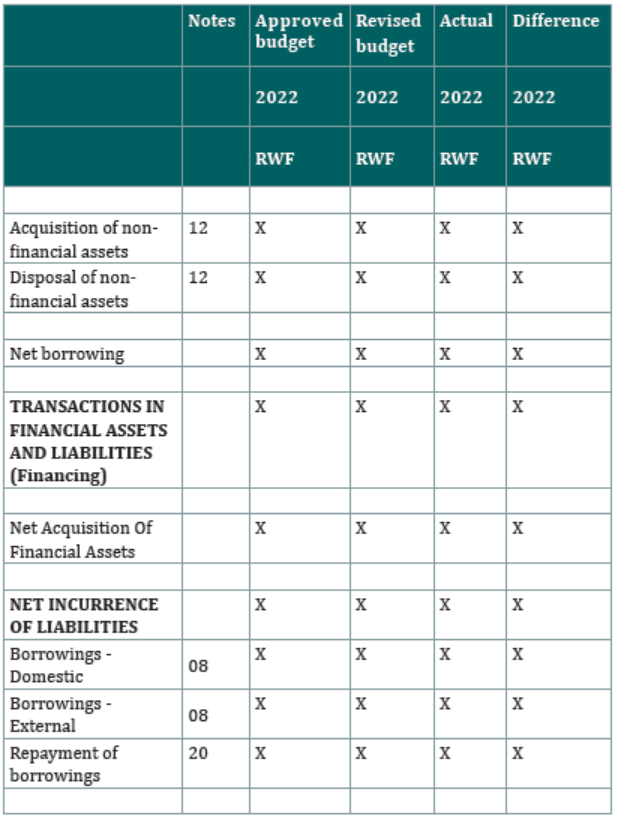

5.3.5. statement of Comparison of Budget and Actual Amounts

Statement of comparison of Budget and Actual Amounts

The following notes and schedules should accompany a complete set of

financial statements:

i. Accounting policies followed in the preparation of Financial Statements;

ii. Bank reconciliation statements and supporting copies of bank statements

for entities;

iii. Petty cash account certificates;

iv. Detailed schedules of debtors and other receivables, creditors and other

payables;

v. Summary of physical assets extracted and reconciled to the fixed assets

register and summary of inventory;

vi. Summary of intangible assets;

vii. Summary of investments made by the entity to date;

viii. Summary of consumable inventory;

ix. Summary of contingent liabilities;

x. Trial balance;

xi. A statement showing the purposes of implementation of audit

recommendations; and

xii. Any other schedule that will enhance easy understanding of the financialstatements.

Application activity 5.3

Identify the key users of the financial statements for a public entity andconsider their information needs.

5.4. Government budget in accordance with therequirements of IPSAS24

Learning Activity 5.4

Mr GATERA criticized the annual government budget prepared advancing

the reason that an annual budget is short sighted, he was provided with

long –term government programs that cover several years and he also

found them to have a long-term perspective such that there is another tool

necessary to link the budget to such long-term program.

Required:

a) As an accountant, who understands the budgeting process in

Rwanda, identify for Mr GATERA, a tool used in planning and

budget process that can serve as a link between annual budget and

long-term government programs and briefly explain how the tool

works.

b) Explain the objectives of the tool used in planning and budget

process that can serve a link between annual budget and longtermgovernment programs.

5.4.1. Government budgeting

A budget is a quantitative expression of a plan of action prepared in advance

of the period to which it relates to. Budgets set out the costs and revenuesthat are expected to be incurred or earned in future periods.

Purposes of budgeting

Planning for the future, in line with the objectives of the organization

Evaluation: To judge managerial performance.

Controlling costs: To compare with actual results to enable investigationsinto significant differences.

Coordination of different activities to ensure goal congruence

Authorization of expenditures

Motivation of managers by encouraging them to beat targets set at thebeginning of the budget period. Bonuses are often based on beating budgets.

Communication: Budgets communicate the targets of the organization toindividual managers.

Budgeting in Public Sector

• Budgeting and financial management are at the core of economic and

public sector reform programs in most nations around the world.

With the growing pressures for enhanced service delivery and the

challenges of budgetary crises and fiscal shocks, the need for improved

budget processes and innovative financial management techniques isespecially critical in developing and emerging economies.

To the government, budget usually serves as:

• An estimate of revenue and expenditure for a given fiscal year;

• A guide towards the execution of the year’s activities; and• An instrument of evaluating performance.

Based on the information above, budget in the public sector is normally

used as an effective instrument for the following.

• As an instrument for economic policy

• Instrument for effective management• Instrument for evaluating performance

Approaches to Budgeting

• Traditional or Incremental Based Budgeting

• Zero Based Budgeting

• Program and Planning Based Budgeting• Performance Based Budgeting

5.4.2. International Public Sector Accounting Standards(IPSAS)

The IPSASB develops and publishes the IPSAS. Now, the IPSASB aim to develop

high quality accounting standards to support public sector entities to prepare

general purpose financial reporting and improve the quality and transparency

of financial reporting in the public sector.

Many IPSAS are based on the International Financial Reporting Standards

(IFRS) or the former International Accounting Standards (IAS) which tend to

be adopted in the private sector.

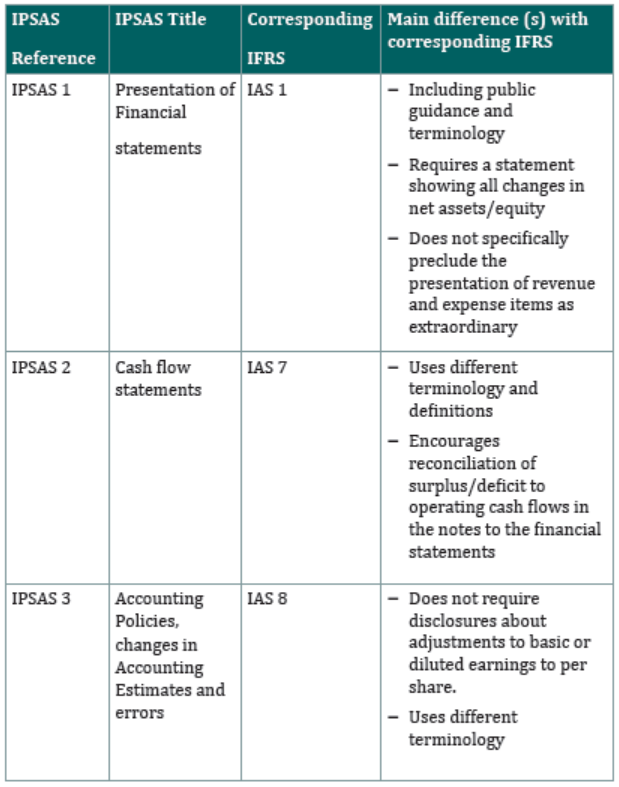

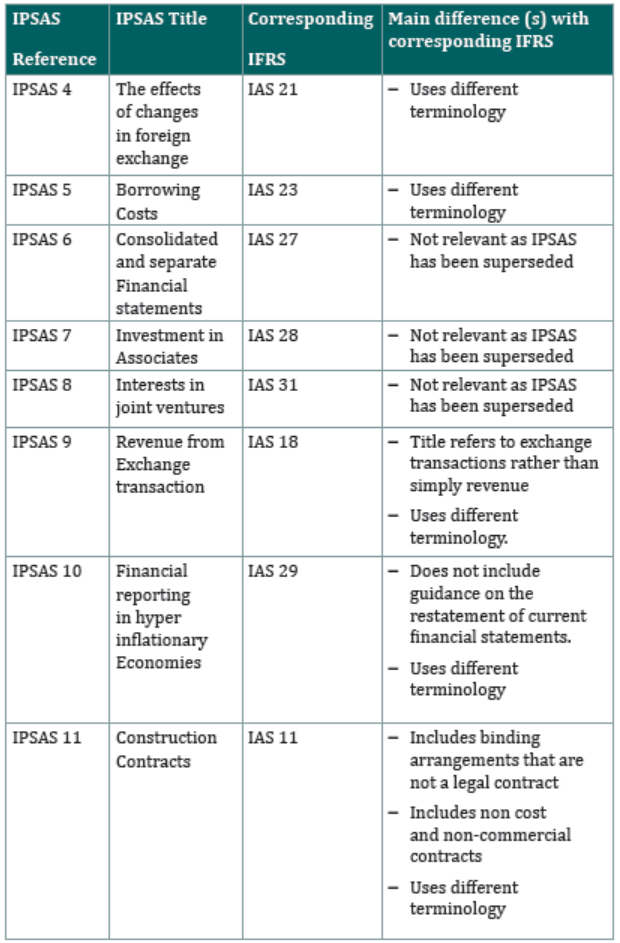

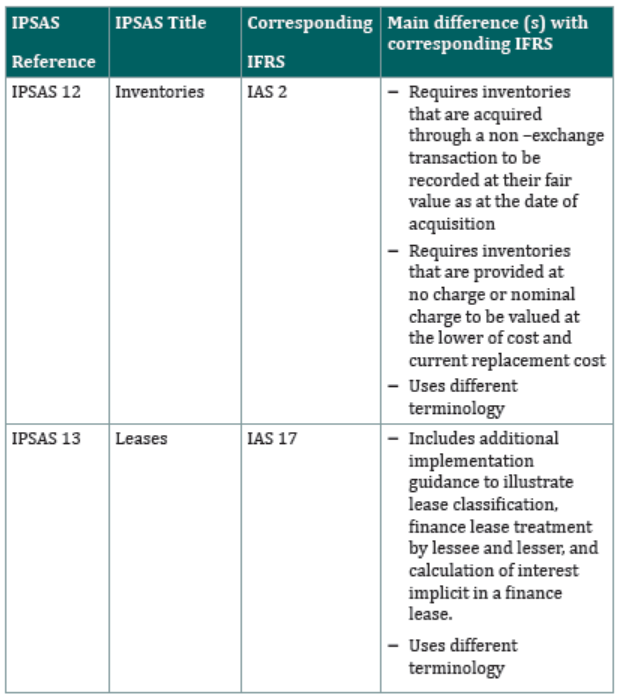

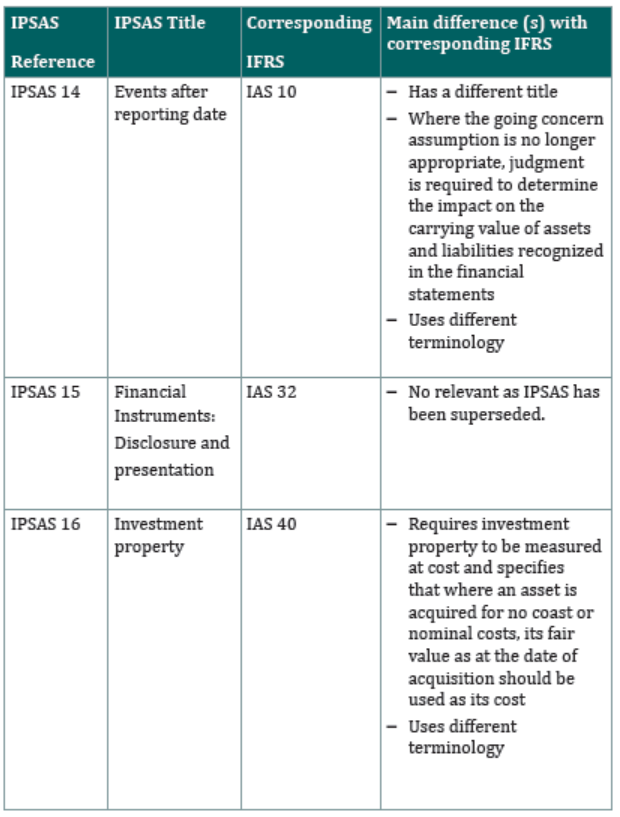

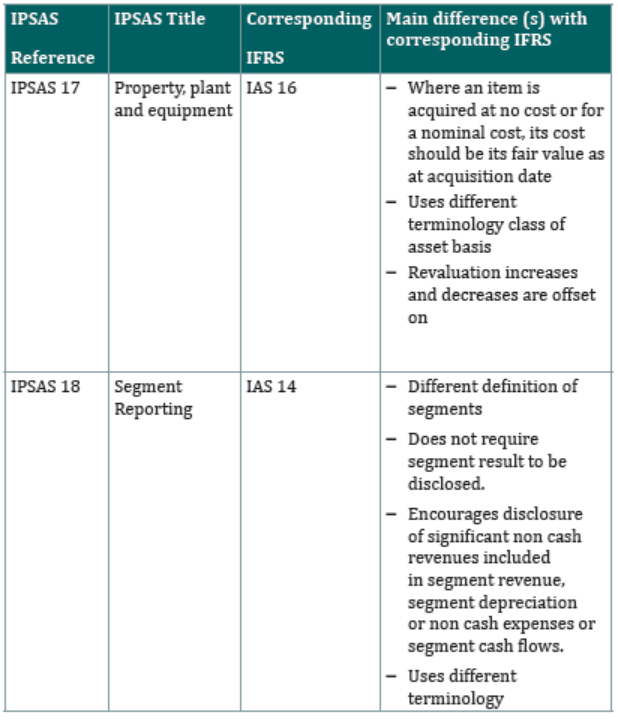

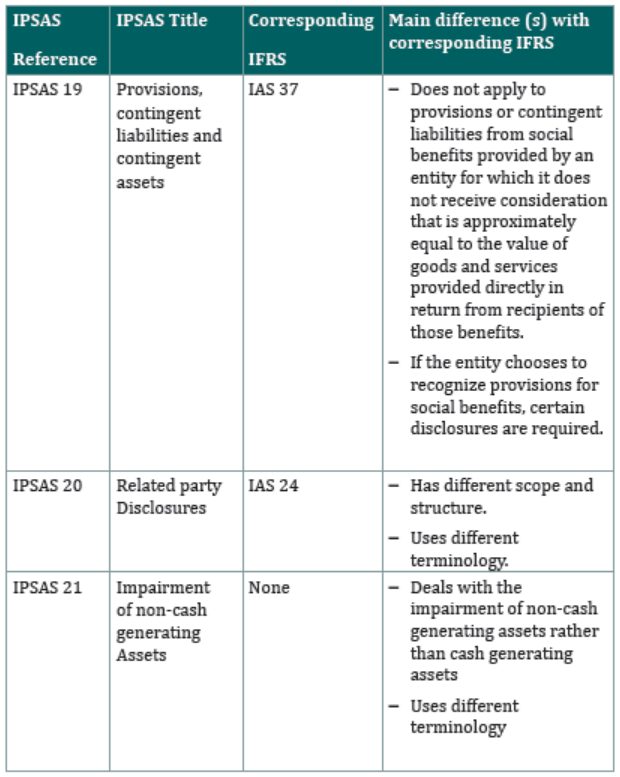

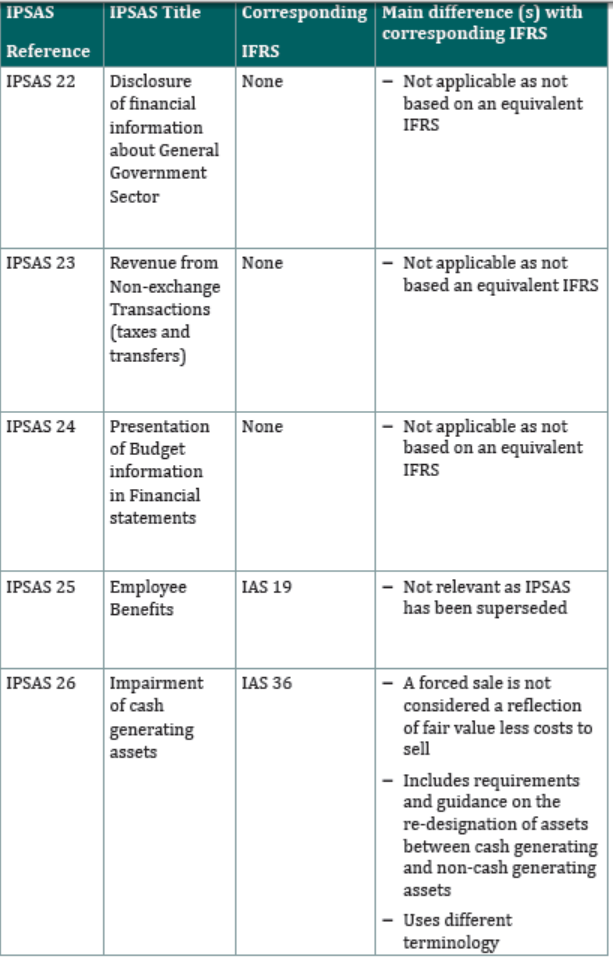

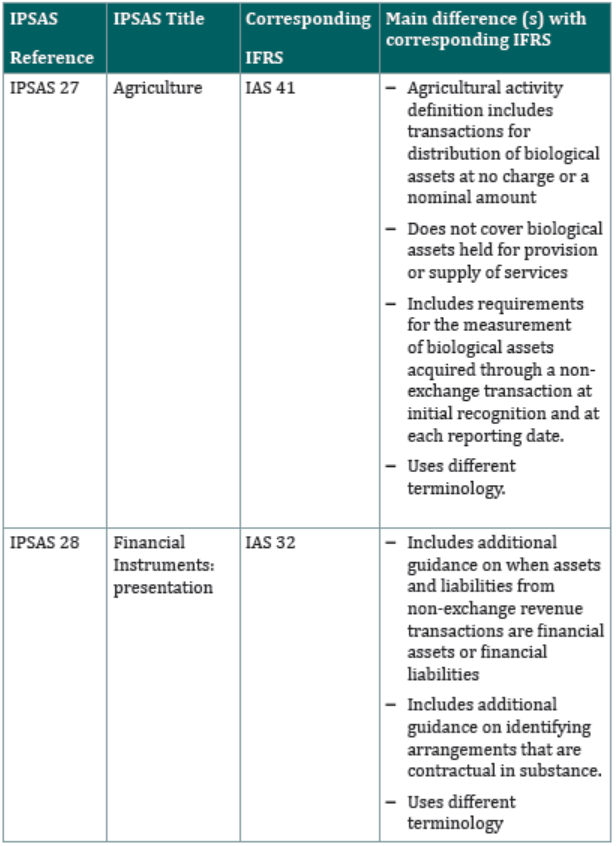

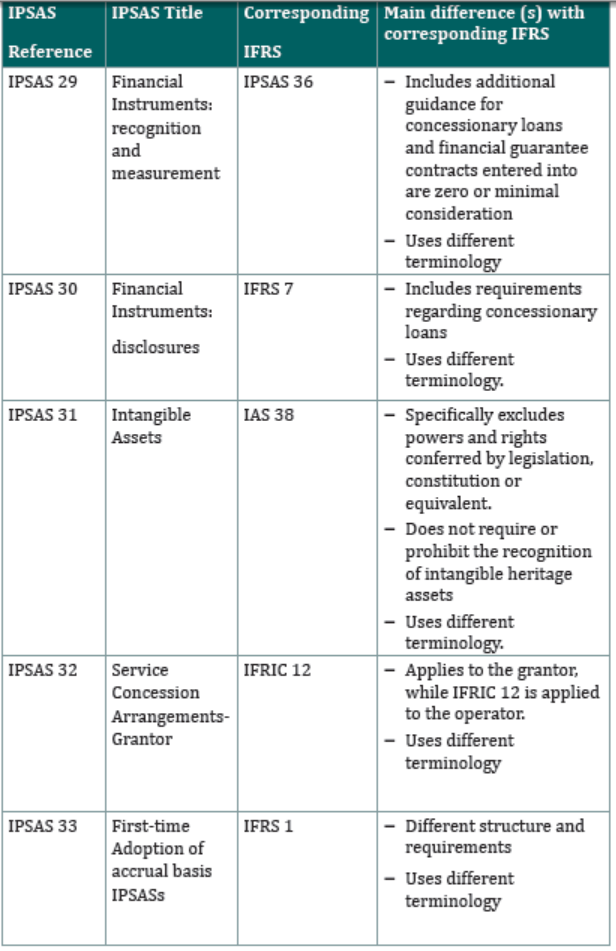

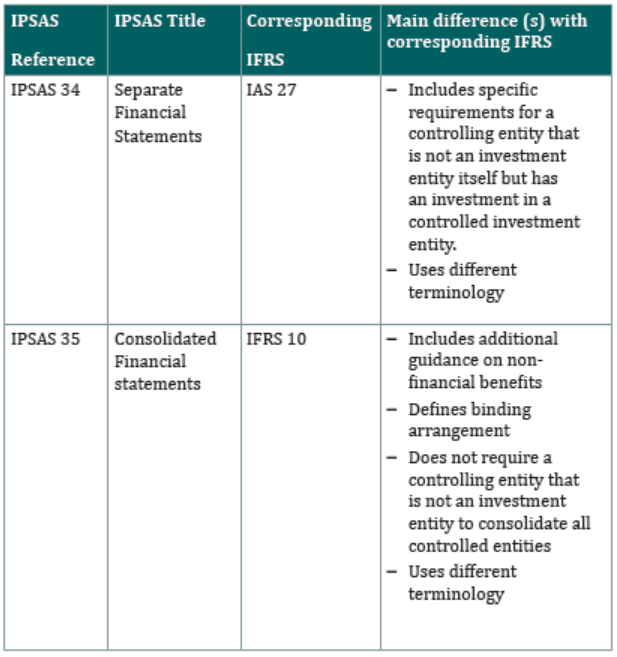

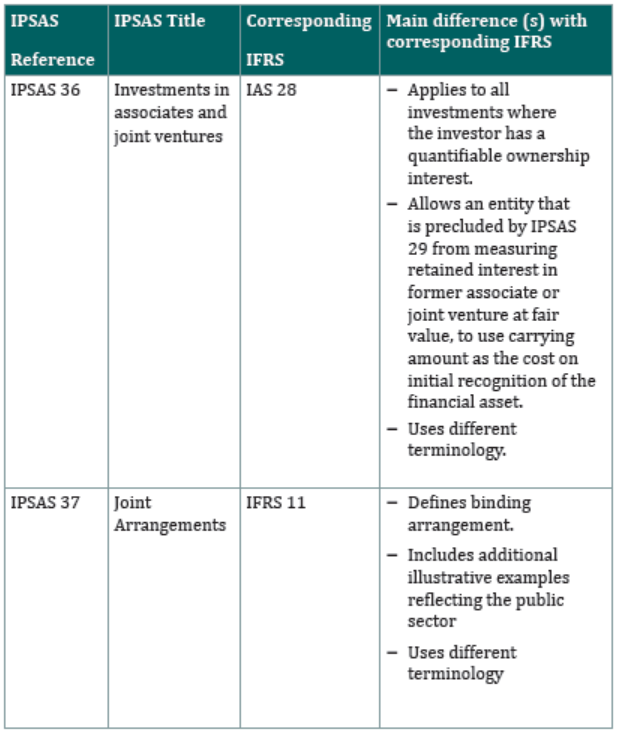

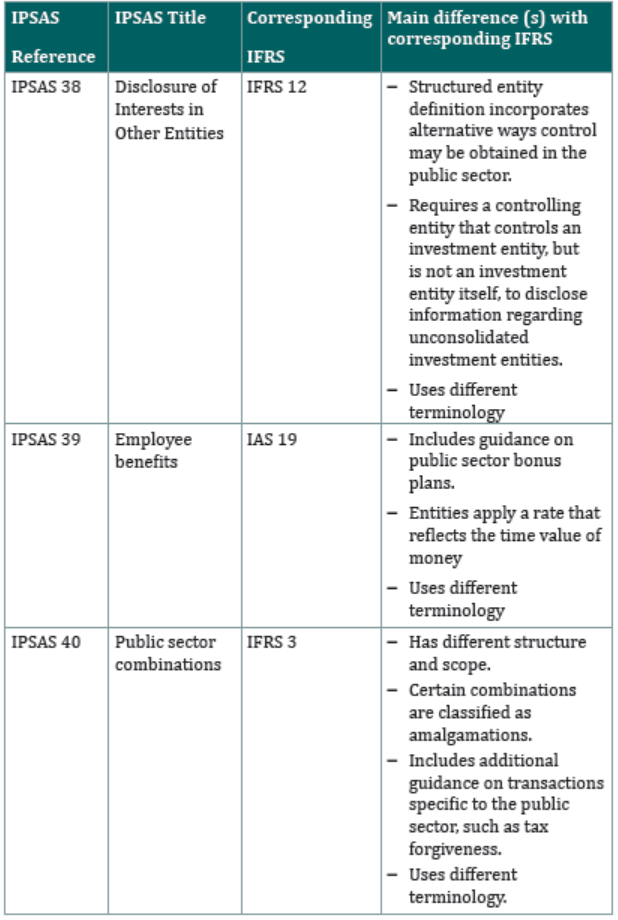

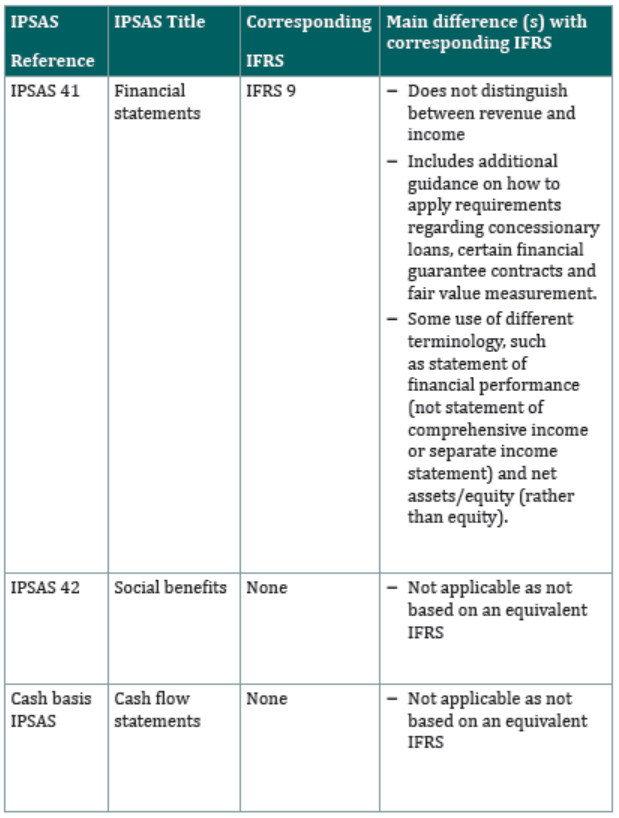

The following table illustrates IPSAS and corresponding IFRS. IPSAS continueto be published. However, as at June 2019 the following are in publication

As you can see from the table above, many of the IPSAS use different terminology

to the IAS or IFRS on which they are based. This is perhaps unsurprising as thenature of public sector entities also differ.

You may have also noticed that the final entry in the table is the Cash Basis IPSAS.

It is worth highlighting that all other IPSAS are based on the accrual method of

accounting which reflects the IPSASB’s preference for accrual based reporting.

Indeed, one of the aims of the IPSASB is to move public sector organizations

from the cash to the accruals basis of accounting and even the cash basis IPSASis intended to be a stepping stone towards achieving accruals reporting.

Application activity 5.4

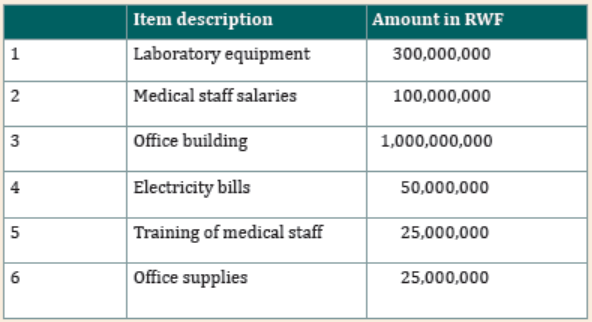

The budget officer of the Ministry of Health is preparing a consolidated

budget for the financial year 2021/2022. During that exercise one of itsbudget including the following items:

Required:

a) Differentiate recurrent from development budgets

b) Classify the above provided items under recurrent and developmentbudget

Skills Lab 1

With the teacher, students carry a visit to nearest Public sector entity. They

ask for some books of accounts held by the entity and available financial

statements for previous years from the Accountant officer. They observe,and share findings thereafter.

End unit assessment 5

1. The Government of Rwanda adopted the use of IFMIS as aninformation management tool. The benefits of using IFMIS include:

i. Enabling government reform and improving efficiency and controls

ii. Improving confidence through transparency

A. (i) only

B. (i) & (ii) only

C. (i), (ii) & (iii)

D. (ii) & (iii) only

2. A government that follows full IPSAS accrual must present a

statement of financial position that complies with IPSAS for the

line items presented. The IPSAS that guide the presentation ofproperty, plant and Equipment is:

A. IPSAS 16

B. 1PSAS 1

C. IPSAS 19

D. None of the above

3. One of the important Public Financial Management (PFM) reforms

that the government of Rwanda has put in place is the use of

Integrated Financial Management Information System (IFMIS).

The implementation of IFMIS came with a lot of benefits but it

also presents certain risks which include but not limited to lack ofcapacity, weak commitment to change and technical challenges.

Required:

Explain any Five (5) internal controls that can be put in place to minimizethese risks associated with the use of IFMIS