Unit 4 INTRODUCTION TO NONPROFIT ORGANIZATIONS

Key unit competence: To be able to prepare financial statements fornon-profit organizations

Introductory activity

Schools, hospital, clubs, Charitable Organizations, NGOs etc share common

features as they do not operate like trading organizations. Their objectives

are rather limited to various social and charitable features. Thus the nature

of their accounting records must reflect the nature of their operating

activities and take form of there

What do you think can be the accounts that are done by non-profit makingorganizations?

4.1. Introduction to non-profit organizations

Learning Activity 4.1

Non-profit making organizations record and report their transactions in

form of accounts same as profit making organizations.

Required: What do you think is the difference between the two?

Learning Activity 4.1

The topic of accounting for nonprofit organizations (NPOs), differs from

commercial accounting in many respects. NPOs’ main goal is to serve the

public rather than to make money for their collaborators or owners. Nonprofit

organizations (NPOs) are money oriented, whereas commercial organizations

are profit focused, because their expenses must be met by revenues, which arefinanced by grants or contributions rather than market transactions.

These organizations whose establishment is mainly non-profit making arenamely ; Schools, hospital, clubs, Charitable Organizations, NGOs etc.

These organizations provide specific services to the community without profit

drive. Although these organization charge fees to the services provided to thebeneficiaries, its low compared to the benefit.

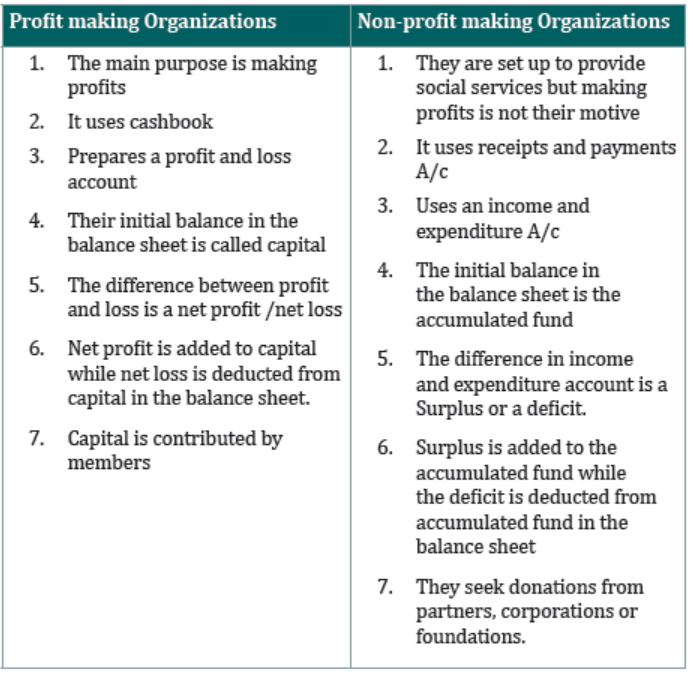

Non-profits organizations prepare final accounts like profit makingorganizations but they differ in the following circumstances :

• A cash book is replaced by receipts and payments A/C

• Profit and loss A/c is replaced by income and expenditure A/C

• Capital is replaced by accumulated funds

• Net profit is called excess of income over expenditure

• Net loss is called excess of expenditure

Differences between Profit making and Non-profit making organizations

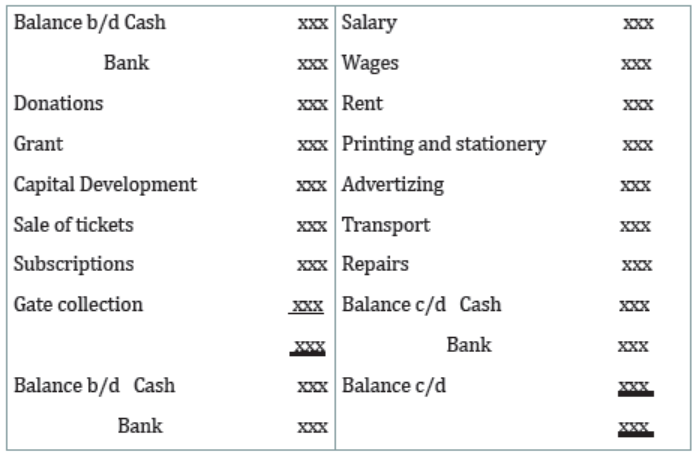

Receipts and payments Account of non-government organizations

This is a summary of all cash and Bank transactions that took place during aparticular accounting period and these include ;

• Opening balance

• The receipts for the period

• The payment for the period

• Closing balance

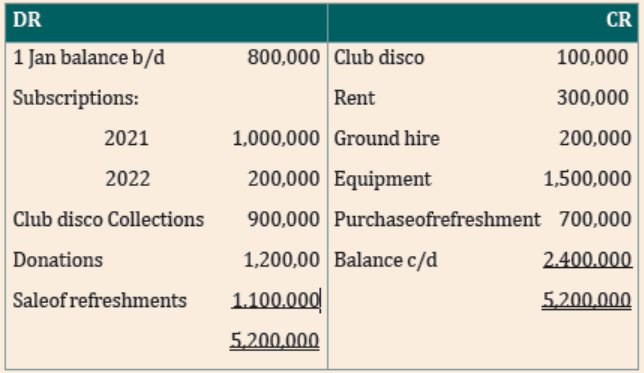

Illustration

Receipts and Payments Account

NOTE : Receipts and payments account is simply a summarized cash account

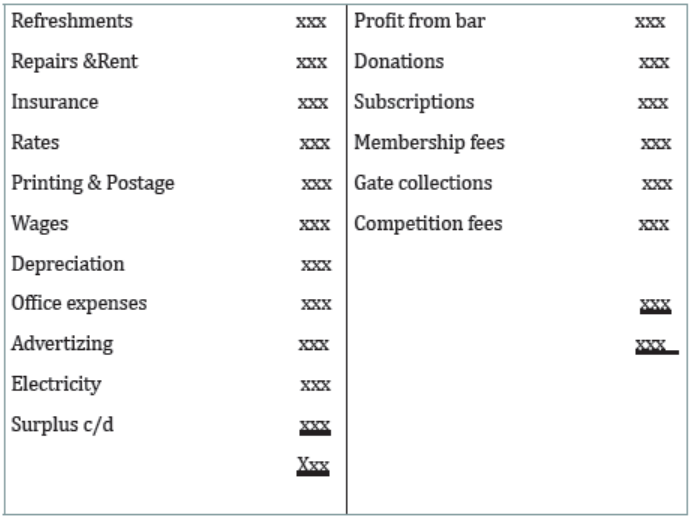

Incomes and expenditure Account

As contrast to profit making organizations, profit generated from non-profit

making organizations is termed as excess of income over expenditure same asfor the loss.

Income and expenditure account is presented in same manner as the profit and

loss account for profit making organization in such way that costs incurred arecompared to the revenues or incomes.

The main features of income and expenditure account ;

• It is a summary of all items relating to income and expenditure on

accrual basis

• It deals with only revenue and expenditure items

• Income is credited while expenditure is debited

• Account balance is represents a surplus or deficit for the period and is

transferred to the accumulated funds.

• The main sources of income are subscriptions, incomes from socialactivities like dance parties, film, plays, donations etc.

NOTE : Sometimes Bar account is prepared separately like a trading account.Mostly is prepared within the income and expenditure account.

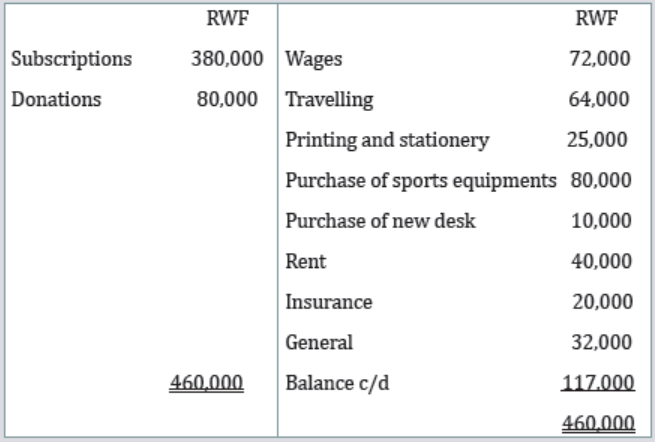

Illustration

Income and Expenditure Account

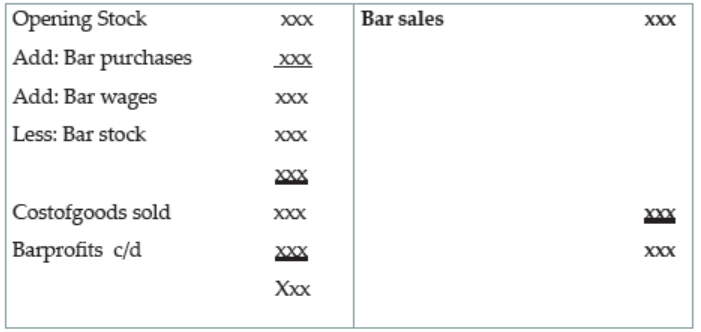

Bar trading Account

The club may occasionally establish a bar to serve drinks to its participants

when they meet. In this case the bar is set for the purpose of earning additional

income to the club. The account for the bar will be prepared in the same way as

of profit making business and the profit will be transferred to the income andthe expenditure account as an income.

Bar trading Account

Surplus and Deficit

A surplus is the excess of income over expenditure that is, when (incomes

exceed the expenditures). It is arrived at from the income and expenditure

account. At the end of every financial period the surplus is added to theaccumulated funds in the balance sheet.

When the expenditure exceeds the income the difference is a deficit. A deficitappears as reduction from accumulated funds in the balance sheet.

Accumulated fund

The capital account of a non-profit organization is termed as accumulated

fund. Any surplus from the income and expenditure account is transferred tothis account and vice versa.

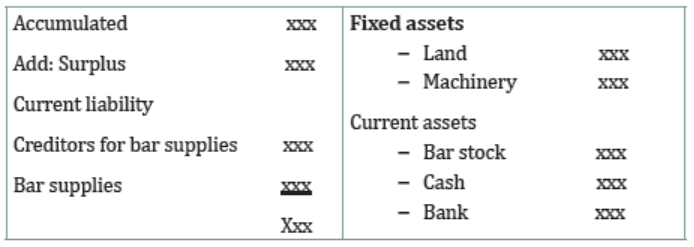

Balance sheet

The term balance sheet refers to a financial statement that reports a company’sassets, liabilities, and shareholder equity at a specific point in time.

Non-profit making organizations prepare balance sheet like Profit making

organization and their items are treated the same except that for capital in

trading organizations. Non-profit making organization’s balance sheet iscalled accumulated fund.

Balance sheet

In non-profit making organizations Accumulated fund= Assets

i.e Assets- liabilities=Accumulated fund,

Thus, accumulated fund + liabilities=Assets

Types of revenues

Business receipts are inflow of economic resources mostly in the form of cashand cash equivalents.

There are mainly two types of revenues notably ;

• Capital receipts• Revenue receipts

Capital receipts

Capital receipts are commercial receipts that are unrelated to a company’s

ongoing business operations. They are infrequent yet are advantageous in thelong run.

In any business capital is introduced for the smooth running of the business.

When realize, capital receipts are often disclosed in the business’s balance

sheet. This is the money that is paid by the sole trader, partners or members

of the company known as shareholders, loans, proceeds from the sale of fixed

assets etc. Similarly, non-profit making organizations receive capital in form ofmembership fees, subscriptions, grants, donations etc.

Example 1.

Suppose, in annual general meeting of Barnabas and sons ltd company, the

issue of right shares was approved at the rate of RWF.1000 per share. Barnabas

and sons ltd allocated shares to all the existing members of the company

proportionately and in return received cash. The cash received by Barnabasand sons ltd company was a capital receipt.

Revenue receipts

The money that a business makes from its regular business operations is known

as revenue receipts. These are recurring in nature and have a direct impact

on the company’s earnings and loss. Consequently, it is necessary to disclose

revenue receipts in the company’s or organization’s income statement.These include ;

• Revenue received from sale of goods to customers.

• Revenue received from provision of services to clients

• Income received as interest on a saving account.

• Dividend income received from shares of various companies.

• Rental income received by a company.

• Bad debts recovered by a company

• Cash discount received from vendors.

• Commission income received by a company

• Interest received

• Interest on investment

• Trading profit

• Rental income• Bad debts recovered, etc

Whereas non-profit making organizations get their receipts from annual

subscriptions, cash sales from trading activity of an organization or chargesfrom the use of premises etc.

Example 2.

Suppose ABC ltd Company is in the business of manufacturing and selling

clothes in bulk to wholesalers and retailers. ABC ltd invoices its customers on

receipt of goods by them and maintains an average collection period of 30 days.

ABC records its sale/revenue on receipt of goods by the customers. The salesrevenue received by ABC company is a revenue receipt.

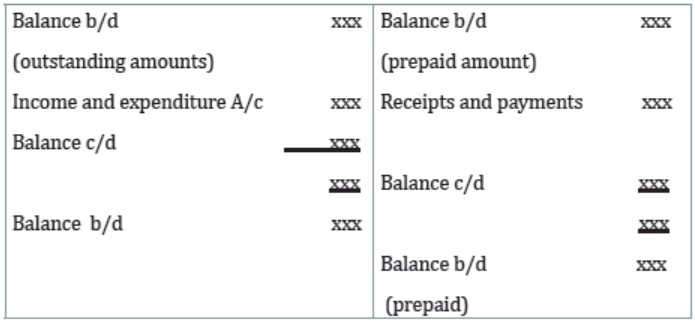

Subscription

Subscriptions are made from the members of the organization as major

source of non-profit making organizations and these can be ordinary or lifesubscriptions.

Accounting treatment for subscriptions

• Subscriptions due or arrears are current assets

• Subscriptions received in advance or prepaid are current liabilities

• Subscription taken as income for a particular year should excludesubscriptions received in arrears and subscription received in advance.

Below is the format of subscription account

Life subscription

In some clubs, members are allowed to become life members by paying life

subscription, which allows them to access the club facilities for the rest of their

life.

Accounting entries when life subscription is paid ;

Dr Receipts and payment A/c xx

Cr life subscription A/c xx

Instructions must be given regarding how much of the life subscription is to be

transferred to the income and expenditure account at the end of the each year.When transfer is done, the following entries are affected ;

Dr Life subscription A/c xx

Cr income and expenditure A/c xx

The credit balance in the life subscription A/c is long-term liability of the club

Types of expenditure

Expenditure is a payment made using cash or credit to purchase goods orservices.

Expenditures are of two that is ;

1. Capital expenditure

2. Revenue expenditure

Capital expenditure is the Cost incurred for the acquisition of fixed assets and

their additions. The advantage from this expenditure is divided over multiple

periods rather than being entirely utilized in one. It includes fixed assets

purchased with the intention of generating income or enhancing the company’s

ability to generate income. For instance, buying land and buildings and adding

things like renovations to buildings, buying plants and machinery, or buyingmore machinery, etc.

Capital expenditure appears in the balance sheet

Revenue expenditure comprises of expenses paid for during one accountingperiod that have a fully utilized benefit throughout that period.

Revenue expenditures are just the expenses incurred over a specific time

period to operate the firm ; they do not increase the value of fixed assets. It

includes things like depreciation, current business expenses, replacements,

maintenance, or renewals e.g wages and salaries, rent, rates, carriages etc.

Such items appear in Trading and profit and loss accounts for profit making

organizations and in an income and expenditure account for non-profit makingorganizations.

Application activity 4.1

The following information provided is taken from the books of ABC as at31.12.2022

Subscription received during the year ending 31.12.2022 RWF 1,000,000

Subscription due at the end of 31.12.2022 RWF 100,000

Subscription received in advance for the following year starting on1.1.2023 RWF 300,000

Required:

Determine the amount of subscription to be taken as income for the yearfor ABC.

4.2. Accounting for non-profit making organization

Learning Activity 4.2

A new school has been opened in Kagarama Sector due to a number of

Students that were moving for a long distance and others could not affordthe schools around.

This school has come to carter for the above problems as it receives funding

from the government and other donors. It is claimed that much money hasbeen spent on this school.

Required:

In which ways would you expect the ministry of Education to monitor thefinancial performance of this school?

Nonprofit accounting is the unique process by which nonprofit making

organizations plan, record, and report upon their finances. Non-profit

organizations focus on accountability and profit making organizations focus on

profit making. They adhere to a particular set of guidelines and practices thataid them in maintaining their accountability to their contributions and donors.

Application activity 4.2

Given below are the receipts and payments account ended 31rst December2021 for Kigali Arena Social Club.

Additional information

Stock of refreshment 1/1/2021 RWF 200,000

Stock of refreshment as at 31/12/2021 RWF 300,000

Prepaid rent RWF 100,000

Ground hire dues RWF 50,000

Subscription RWF 300,000

Required

Bar trading account

Prepare an income statement and expenditure account for the year ended31/12/1021

Balance sheet

End unit assessment 4

1. What are final accounts for non-profit organizations?

a) Receipts and payment account

b) Trading and profit and loss account

c) Income and expenditure account

d) Both a and c

2. From the following receipts and payments account for Gikoba foot

ball club and the additional information is provided. Prepare an

income and expenditure account for the year ended 31 December2021.

Receipts and payments Account

Additional information on 31 December 2021

I. The club consists of 200 members paying annual subscription of

RWF 2,000 and only180 members had paid their subscription fully

while 10 had paid for 2022.

II. Wages outstanding amounted to RWF 8,000; insurance prepaid RWF6,000 and stock of unused stationery RWF 2,500.

Required:

1. Prepare Income and expenditure statement

2. Extract the balance sheet