Unit 3 PARTNERSHIP ACCOUNTS

Key unit competence: To be able to prepare financial statements for apartnership business

Introductory activity

Observe the picture above and answer the following questions:

1. What do you see on this image?

2. Among forms of business, which one is formed by partners?

3. What do you understand by partnership agreement?

4. Which accounts to be prepared in partnership

3.1. Introduction to partnership

Learning Activity 3.1

Read the following case study and answer the given questions.

A partnership is a business owned by two or more people. In most forms

of partnerships, each partner has unlimited liability for the debts incurred

by the business. The three most prevalent types of for-profit partnerships

are: general partnerships, limited partnerships, and limited liability

partnerships. Partnerships are arrangements between individuals to carry

on business in common with a view to profit. A partnership, however,

involves obligations to others, and so a partnership is usually governed

by a partnership agreement. Unless it is a limited liability partnership

(LLP), partners will be fully liable for debts and liabilities, for example if

the partnership issued. A partnership is a group of individuals who are

trading together with the intention of making a profit. Partnerships are

often created as a sole trader’s business expands and more capital and

expertise are needed within the business. Typical partnerships are those of

accountants, solicitors and dentists and usually comprise between about 2

and 20 partners. As partnerships tend to be larger than sole traders, there

will usually be more employees and a greater likelihood of a bookkeeper

being employed to maintain the accounting records. Each of the partners

will contribute capital to the business and will normally take part in the

business activities. The profits of the business will be shared between the

partners, and this is normally done by setting up a partnership agreement

where the financial rights of each partner are set out. Just as with sole

traders, the partners will withdraw part of the profits that are due to them

in the form of drawings from the business although, in some cases, partnersmay also be paid a salary by the business.

After reading this case study, answer the following questions

1. A partnership is a group of individuals who are ……..….. together

with the intention of making profit.

a) Business

b) Arrangements

c) Involvesd) Trading

2. What are the most types of for- profit partnership?

3. What are the advantages and disadvantages of partnership?

3.1.1. Meaning of partnership business

Partnership may be defined as: a relation between persons carrying on a

business in common with a view of profit. A partnership is owned by two

or more people but not more than twenty persons except in certain cases.

In most forms of partnerships, each partner has unlimited liability for the

debts incurred by the business. The three most prevalent types of for-profit

partnerships are:

• General partnerships

• Limited liabilities partnerships

• Limited partnerships. E.g: practicing solicitors, professional

accountants and members of the stock exchange where this figure

may be exceeded.Types of partners:

1. According to participation in the running of the business

a) Active partner: This actively participates in the day to day runningof the business.

b) Dormant/sleeping partner: Does not actively participate in theday to day running of the business

2. According to age

a) Major partner: This is a partner who is above the maturity age

b) Minor partner: This partner has not attained maturity age andtherefore has limited liability.

3. According to liability

a) Limited partner: This partner has limited liability. This means that

his/her liability towards the debts of the partnership is limited to

his/her capital contributions. Minor partners have limited liability.

b) Unlimited partner: This partner is liable for all the debts of the

partnership to the extent of selling personal property to pay thedebts of the partnership.

4. According to capital contributions

a) Quasi partner: This does not contribute capital, but allows his/her

name to be used by the partnership.b) General partner: This is a partner because of capital contributions.

Advantages and disadvantages of partnerships

Advantages of partnership:

• More capital is raised from bigger membership

• Better skills from a variety of members

• Better decisions can be made compared to sole proprietors

• Partnerships are easy to form compared to limited companies

• Risks are minimal as they are spread across many members.

• Partnerships can easily access credit from financial institutions

since lenders find it easier to deal with a group of people than oneindividual

Disadvantages of partnerships:

• Profits are reduced as they are shared among many members

• Partners have unlimited liability_ they have equal sharing when it

comes to the liabilities of a partnership

• Delays in decision making compared to sole proprietors

• They are not permanent in nature because the death or retirement

of a partner may lead to its dissolution

Business usually depends on active partners and is likely to be affected incase they die

Application activity 3.1

Read carefully and discuss on the following questions:

a) What are the components of a partnership deed?

b) What happens if no partnership deed exists?

c) State and explain the types of goodwill.

3.1.2. Partnership agreement or deed

This is a written agreement among partners regarding the terms andconditions of the partnership business.

Components of partnership agreement or deed

A partnership deed usually contains the following;

– Capital to be contributed by each member.

– Names of partners

– Profit and loss sharing ratios

– Salaries paid to partners

– Partners drawing rights and interest on drawings

– Preparation and auditing of books of accounts

– Duties, powers and liabilities of each member.

– Basis of valuation of good will

– Methods of dealing with the death, retirement and insolvency of

partners

– Methods of admission of a new partner– Method of settling the accounts in case of dissolution.

If no partnership deed that exists

– Profits and losses are shared equally

– There will be no interest on capital

– There will be no interest on drawings

– No payment of salaries to partners

– If a partner gives a loan to the partnership business, he is entitled to5% interest per annum.

Accounting for goodwill in partnership accounts

Goodwill is an intangible asset arising from the business’s ability to earn more

profits as compared to other firms in the same or similar trade. Goodwill arises

when the value of the business as a going concern is greater than the value

of its separate tangible assets. It is the excess of purchase consideration of a

business sold as a going concern above the fair market value of the businessassets.

Goodwill arises in the business because of the following reasons,

– The business may have enjoyed some form of monopoly either

nationally or locally for example there may not be sufficient trade to

out compete some Engineering firms, which have been managed orrun for a long period.

– A new business may continue to trade under the same name as that

of the original firm. The fact that the firm was well known could mean

that new customers and old customers are attracted for this reason.

– The value of labor force including management skills other than that

of the retiring proprietor may be carried forward. Skilled managementis an asset to the business.

– The possession of patent rights and trademarks may account for

goodwill. These may have cost the original owner little or nothing

and they could be shown in the balance sheet. They are normallyunsellable, unless the business is sold as a going concern.

– The location for the Business premises may be more valuable if the

business does not change. Where the business is strategically locatedthis is an advantage.

– The cost of research and development, which might have brought

about cheaper manufacturing methods or cheaper products, may be

charged to the current buyer. The amount that the buyer is prepared

to pay will depend on his view of the future profits which will accrueto the factors mentioned above.

Types of goodwill:

In accounting, goodwill is classified into inherent goodwill, purchasedgoodwill and negative goodwill.

1. Purchased goodwill arises from a defined financial transaction and

hence its recorded in the financial statement like any other assets in

accordance with international financial reporting standard 3 IFRS3-

BUSINESS COMBINATION.IFRS3 Provides for immediate write-off of

goodwill after acquisition or amortization for a period not exceedingtwenty years using straight-line method.

2. Inherent goodwill on the other hand arises out of normal carrying

out of the business activities. It is never recorded in the books because

recording it would mean anticipating gains that would only be realizedon the sale of the business that may never happen.

3. Negative goodwill arises when the realizable value of the business

sold as a going concern is exceeded by the fair market value realizedfrom individual assets.

Circumstances that lead to ascertainment of good will

When dealing with partnership accounts, goodwill may be recognized underthe following circumstances:

-Admission of a new partner into the established partnership especially

when the old partners have built goodwill into the business. This is to enable

the new partner to compensate for the share of the good will he/she is goingto enjoy.

– On death or retirement of one partner from an established

partnership.

– At dissolution of the partnership.

– When there is a change in the mode of ascertaining profit and loss of

the firm.– When there is a change in the profit sharing ratios.

3.2. Introduction to partnership accounts

Learning Activity 3.2

On 01.01.2020. Kefa and Sifa started a partnership business which is

located in HUYE district. They agreed to contribute equally and their capital

contribution amounted to 250,000 RWF. Upon their agreement Kefa and

Sifa injected in addition capital of 20,000 RWF. On 31.3.2020, they shared

interest on the capital on the profit made. On 5.3.2020, they withdrew

money for personal use. On 30.5.2020, they paid interest on drawings. A

salary was also paid to Sifa. After paying all the expense profit was shared

by the partners by using their sharing ratios. After two years their businessmade a loss.

Required:

After understanding this scenario, as an accountant who completed in S4Accounting,

What are the necessary accounting entries for this partnership?

3.2.1. Meaning of accounting entry

An accounting entry is a formal record that documents transaction. In most

cases, an accounting entry is made using the double entry bookkeeping system,

which requires one to make both a debit and credit entry, and which eventually

leads to the creation of a complete set of financial statements. An accounting

entry can also be made in a single entry accounting system; this system typically

tracks only cash receipts and cash disbursements and shows only those resultsneeded to construct an income statement.

Types of accounting entries:

They are three primary types of accounting entries, which are noted below

1. Transaction entry

A transaction entry is the primary type of business event for which the accountant

would create an accounting entry. Examples of accounting transactions are the

record of an invoice to a Customer, an invoice from a supplier, the receipt of

cash and the purchase of a fixed asset. This type of accounting entry is usedunder both the accrual basis and cash basis of accounting.

2. Adjusting entry

An adjusting entry is a journal entry used at the end of an accounting period to

adjust the balances in various general ledger accounts to more closely align the

reported results and financial position of a business to meet the requirements

of an accounting framework, such as GAAP or IFRS. This type of accountingentry is used under the accrual basis of accounting

3. Closing entry

A closing entry is a journal entry used at the end of an accounting period to shift

the ending balances in all revenue, expense, gain, and loss accounts (known

as temporary accounts) into the retained earnings account. Doing so empties

out the temporary accounts, so that they can begin accumulating transactionalinformation in the next accounting period.

How to create accounting entries?

Accounting entries for transactions are typically created through a transaction

interface in the accounting software, so that you may not even realize that

you are creating an accounting entry (such as, for example: when creating a

customer invoice). If you are creating an adjusting accounting entry, then you

will use a journal entry format (assuming that a double entry accounting system

is being used). If you are closing the books at the end of an accounting period,

the accounting software will likely create the closing entry automatically; youwill not even see the entry.

Accounting entries

1. In case of additional capital contributed.

Dr. cash/bank/asset a/c

Cr. Individual partner capital a/c

2. In case of interest on capital

Dr. Interest on capital a/c

Cr. Individual partner`s current a/c

3. In case of any drawings

Dr. Individual partner’s current a/c

Cr. Cash/bank/asset a/c

4. In case of any interest on drawings

Dr. individual partner`s current a/c

Cr. Interest on drawings

5. Salaries paid to a partner

Dr. salaries a/c

Cr. Individual partner`s current a/c

6. Share of profits by a partner

Dr. income statement a/c

Cr. Individual partner current a/c

7. Share of loss by a partner

Dr. Individual partner current a/c

Cr. Income statement a/c

3.3. Components of Partnership Final accounts

Learning Activity 3.3

On 01.01.2010, Ineza, Louise and Gisa started a partnership firm in

Nyagatare District, buying and selling cars. After 1 year, they needed to

ascertain if they got a profit or loss.

1. Which document can help them to know if they made a profit orloss?

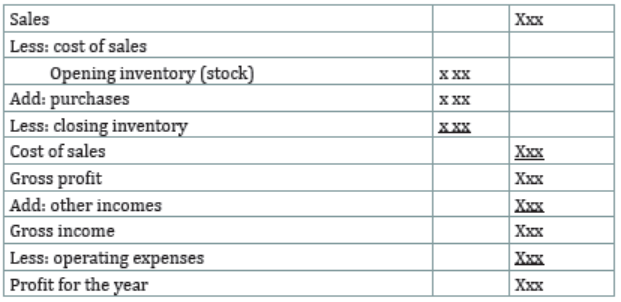

3.3.1. Income statement of partnerships

The trading on profit and loss of a partnership is the same as that of a soletrader only that it has an extension called the appropriation account.

Format of the income statement of partnerships

NB:

– Interest on a loan is a business expense and treated as a business

expense and treated in the profit and loss a/c

– If a partnership gives out a loan in return for interest, the interest

received is treated as an income.

– If a partner gives a loan to a partnership, interest charges on the loan isa business expense and charged against the profit and loss a/c.

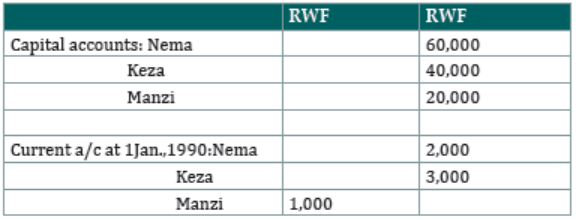

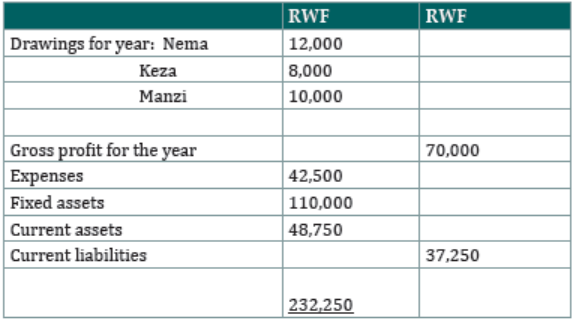

Illustration1:

The following trial balance was extracted from the books of Nema, keza andManzi at 31 December 1990 (trading account has already been prepared

Required: The preparation of a profit and Loss account for the year ended 31

December1990

Addition information:

– Interest is to be allowed at 6% per annum on partners ‘capital accounts.– RWF 5,000 is to be allowed as a salary to Manzi

Answer:

Nema, Keza Manzi

P&L a/c for the year ended 31 December 1990

Illustration 2

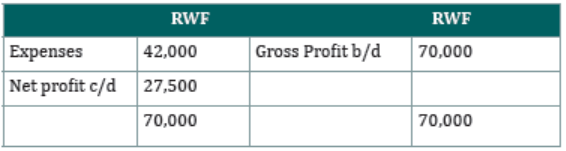

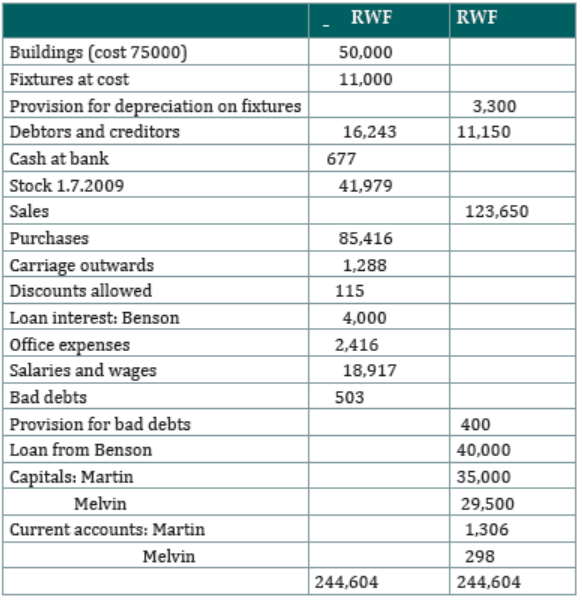

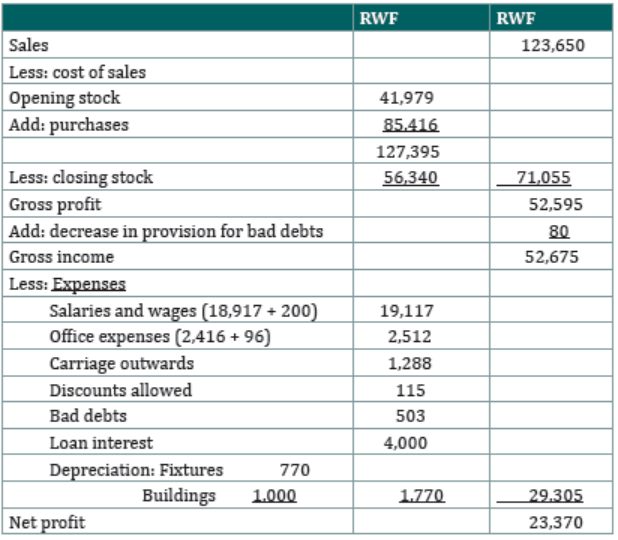

Martin and Melvin are in a partnership sharing profits and losses equally. Thefollowing is their trial balance as at 30.06.2010

Required: Prepare profit and loss account for the year ended 30.06.2010

a) Stock 30.06.2010 was 56,340

b) Expenses to be accrued; office expenses 96, wages 200

c) Depreciate fixtures 10% on reducing balance basis, buildings 1,000

d) Reduce provision for bad debts to 320

e) Partnership salary 800 to Martin not yet paid.

f) Interest on drawings: Martin 180Melvin 120

g) Interest on capital account at 10%.

Solution

Martin and Melvin

Income statement for the year ended 31.12.2010

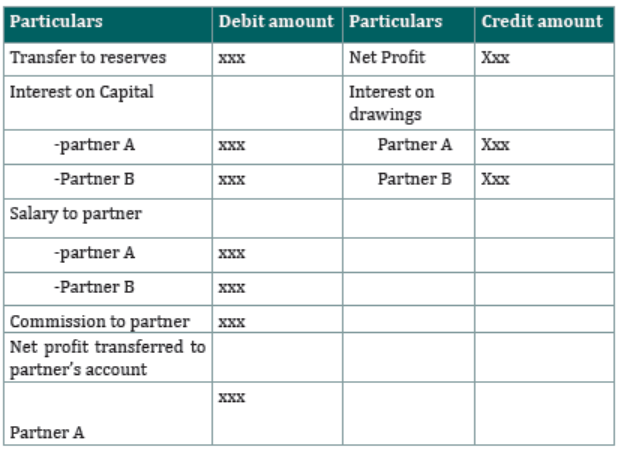

Partnership appropriation account

The appropriation account is prepared after preparing Profit & Loss A/C. In the

case of partnership firms, it is prepared to show how profits are distributedamong the partners involved in the partnership.

In the case of LLC (Limited Liability Company), the purpose of preparing this

account is the same but the format is different. We will start with the year’s

profit before the taxation figure, from which we will subtract corporate taxesand dividends to find the retained earnings for the year.

In the government’s case, the appropriation account is used to show the funds

allocated to the specific project. Any expenses are reduced from the fundsallocated.

The following are the adjustment/items included in this account:

1. Net Profit: It is the opening balance of appropriation a/c. This balance is

taken from Profit & Loss a/c after making all the necessary adjustmentsfor the period.

2. Interest on Capital: The expense for the company as a partner will bepaid interest on the amount of capital invested in the business.

3. Interest on Drawings: It is an income for the company. The company

will charge interest from the partner on any amount of capital withdrawnduring the year.

4. Partner’s Salary: It is pre-agreed as per the partnership deed and is anexpense for the business.

5. Partner’s Commission: It is pre-agreed as per the partnership deedand is an expense for the business.

6. Net Profit transferred to Partner’s Account: After making all theabove adjustments, this is the final profit amount.

Format of profit and loss appropriation (P&L)

P&L appropriation a/c for the year ended 31/12/xxx

Profit & Loss (P&L) Appropriation A/c

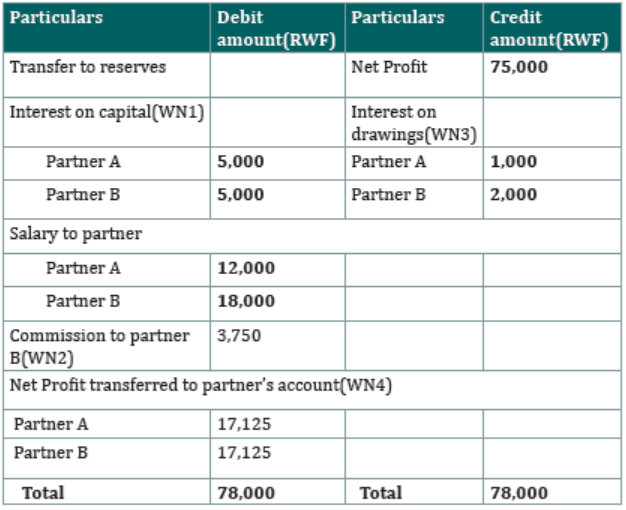

A & B started a partnership firm on 01.01.2017. They contributed RWF 50,000

each as their capital. The terms of a partnership are as under:

– A& B to get monthly salary of RWF 1,000 & RWF 1,500 respectively

– B is allowed a commission at the rate of 5% of Net profit

– Interest on capital & drawings will be 10% p.a.– Sharing of profit & Loss will be in the ratio of capital sharing.

Before making the above appropriations, the profit for the year ending

31.12.2017 is RWF 75,000. Drawings of A & B were RWF 10,000 & RWF 20,000respectively. Prepare Profit & Loss Appropriation Account.

Solution

Working

WN 1 Interest on Capital @10% of the Capital Invested

Partner A = 50000*10% = 5000

Partner B = 50000*10% = 5000

WN2 Commission @5% of Net Profits

Partner B = 75000*5% = 3750

WN3 Interest on Drawings @ 10% of Amount of Drawings

Partner A = 10000*10% = 1000

Partner B = 20000*10% = 2000

WN4 Net Profit divided among partners in ratio of their capital i.e 50% each

Partner A = (78000-(5000+5000+12000+18000+3750))/2 =17125

Partner B = (78000-(5000+5000+12000+18000+3750))/2 =17125

P&L Appropriation A/C for the year ended 31/12/2017

Illustration 2:

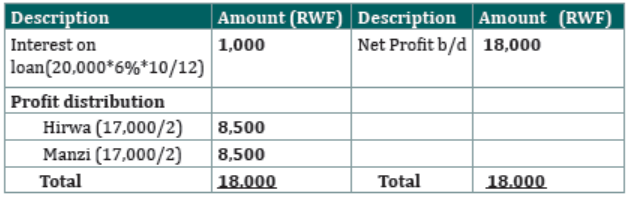

Hirwa and Manzi started business in partnership on 1st January, 2015 without

any agreement. Mr. Hirwa introduced capital RWF. 60,000 and Mr. Manzi RWF

40,000. On March 1st, 2015Mr. Manzi advanced RWF 20,000 by way of loan at

an interest rate of 6% per annum. The profit for the year ended 31st, December2015, was amounted to RWF 18,000.

Required: Prepare Profit and Loss Appropriation Account at the end of 2015.

Solution:

Hirwa and Manzi P&L Appropriation A/C for the period ended 31stDecember, 2015

Illustration 3

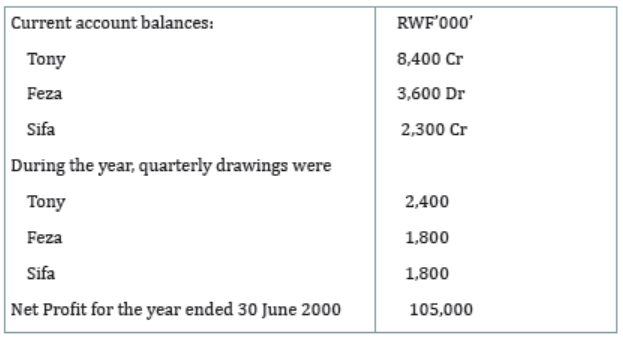

Tony, Feza and Sifa are in partnership with capital of RWF 200,000; 80,000 andRWF 20,000 respectively. Their partnership deed provides for the following:

i. Interest on capital at 4% per annum

ii. Interest chargeable on drawings at 5% per annum

iii. Tony and Feza to receive salaries of RWF20,000 each per annum

iv. Tony, Feza and Sifa are to share the profits and losses in the ratio 6:3:1respectively.

The following information is available for the year ended 30 June 2000:

Required:

The appropriation account for the year ended 30 June 2000

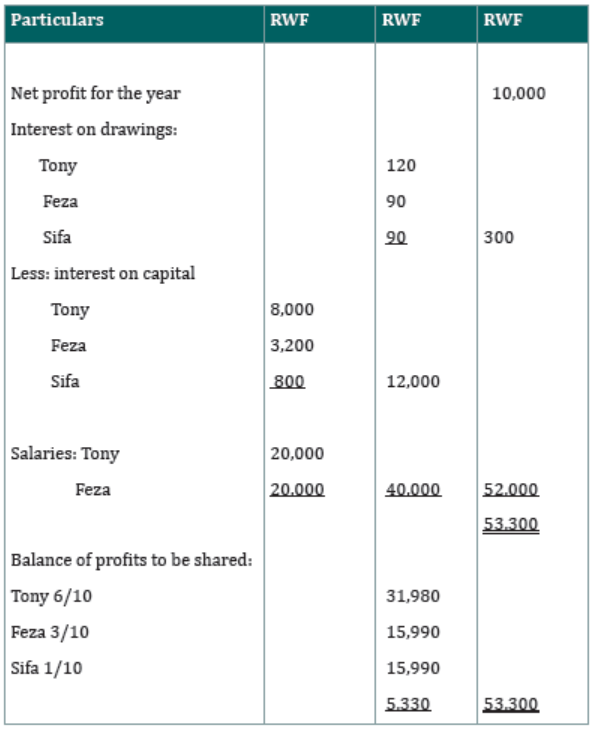

Solution

Tony, Feza and Sifa

The appropriation account for the year ended 30 June 2000

Working:

W-1. Interest on drawing, 5% per annum

Tony: drawing 2,400; Interest: 2,400*5/100=120

Feza: drawing 1,800; Interest: 1,800*5/100=90

Sifa: drawing 1, 800; Interest: 1,800*5/100=90

W-2. Interest on capital 4% per annum

Tony: capital 200,000; Interest: 200,000*4%=8,000

Feza: capital 80,000; Interest: 80,000*4%=3,200

Sifa: capital 20,000; Interest: 20,000*4%=800

W-3. Balance of profit to be shared

Total profits=RWF 53,300

Tony, Feza, and Sifa =6:3:1

Tony: 53,300*6/100=3,198

Feza: 53,300*3/100=1,599

Sifa: 53,300*1/100=533

Importance of Appropriation Account

This account shows the number of profits divided among various heads.

It shows the number of profits transferred to reserves and distributed asdividends.

It gives information on how the profits are divided among partners and howthe various adjustments are made during the year.

Conclusion

Hence, the appropriation account shows how the profits are appropriated or

distributed among various heads. This account is prepared on behalf of thefirm.

3.3.2. Partnership capital accounts

Definition:

A partnership capital account is an account that contains all the transactions

occurring between the partners and the partnership firm, such as the initial

contribution of capital in partnership, the interest of capital paid, drawings,

the share of profit, and others adjustments. It is required to maintain properaccountability and transparency between the partners and the firm.

Fixed capital accounts, Current accounts, Fluctuating capital accounts:

When fixed capital accounts are maintained, the capital account records thepartner’s capital contribution only.

A current account is opened up where partner’s dealings with the partnershipare recorded e.g. interest on capital, interest on drawings, partner’s salaries etc.

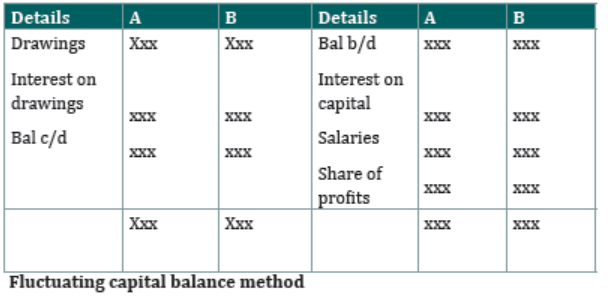

Under fluctuating capital balance method, the capital account records the

capital contributions and other partners’ dealings with the partnership e.g.salaries, interest on capital, drawings, interest on drawings, share of profits etc.

Fixed capitals are more preferable than fluctuating capitals. With current

accounts where a partner is drawing more than his share of profit, the partner’s

current account will show a debit balance and this is a warning that his drawingsare excessive.

Note: Fluctuating capital accounts is a combination of Fixed capital accountsand Current accounts

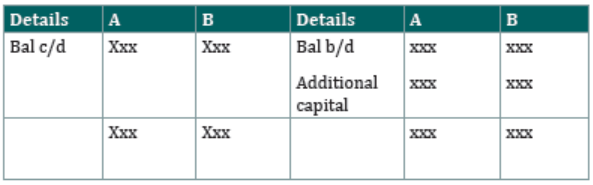

Fixed capital balance method

Capital account

Current account

Capital accounts

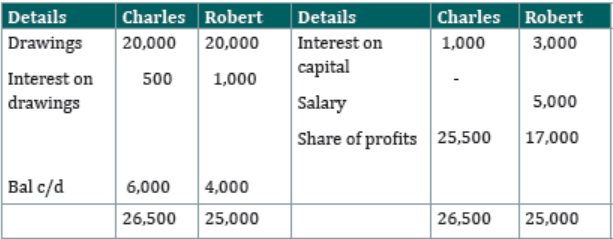

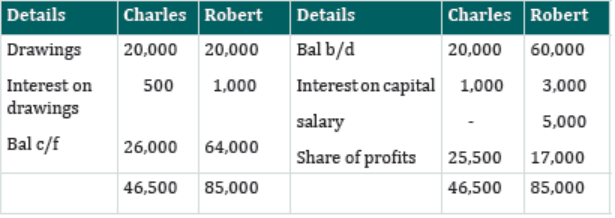

Illustration 1

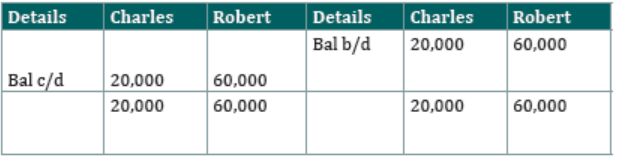

Charles and Robert are in partnership sharing profits and losses in a ratio 3:2

respectively. They are entitled to 5% per annum interest on capitals. Theircapitals are; Charles 20,000 and Robert 60,000.

Robert is to have a salary of 5,000.

They charge interest on drawings Charles being 500 and Robert 1,000.

During the year drawings for Charles and Robert were 20,000 each.

Their share of profits is 25,500 and 17,000.

Required: Show the partners’ capital accounts.

Fixed capital accounts

Current accounts

Fluctuating capital accounts

Illustration2

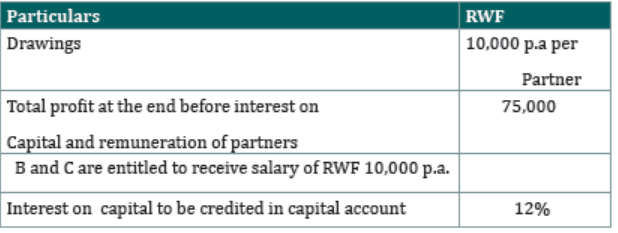

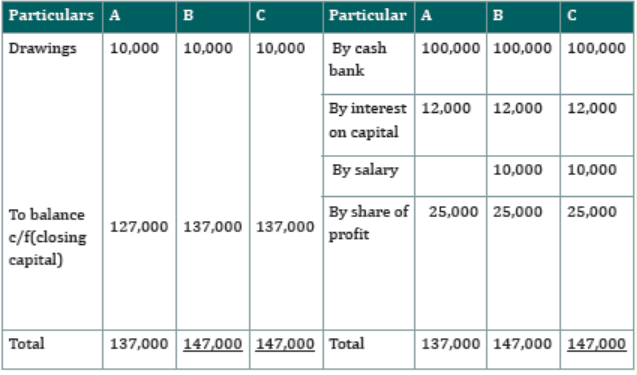

ABC and Co. are a partnership firm with the three partners, A, B, and C. Profit

sharing ratio of each partner is equal, and the capital contribution of each

partner is also equal. The total requirement of investment in the business is

FWR 300,000. The firm does not maintain a separate current account and all the

transactions are to be recorded in the capital account itself. Other details are asunder:

Required: Draw the Partners Capital account and record the above transactions.

Solution:

Capital Contribution = RWF 300,000 / 3 = RWF 100,000

Interest on Capital = RWF 100,000 * 12% = RWF 12,000 per partner.Profit Share =RWF 75,000/3 =RWF 25,000 per partner

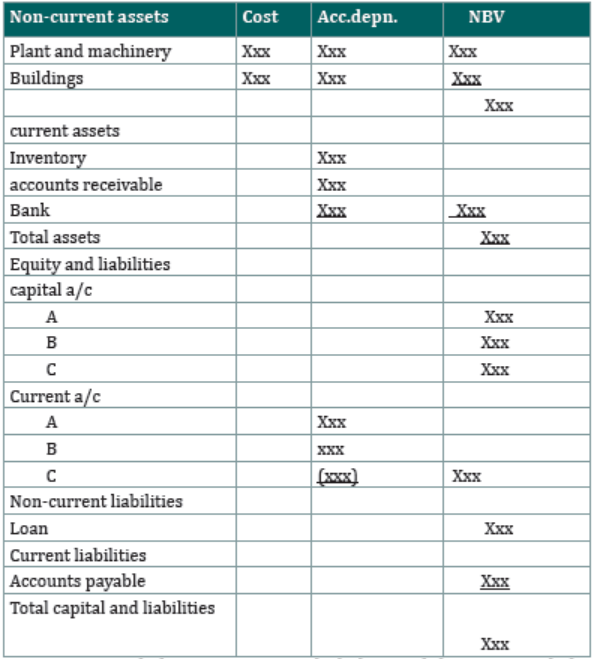

3.3.3 Balance sheet (statement of financial position)

Definition:

Balance sheet summarized a company’s assets, liabilities and shareholders’

equity at a specific point in time (as indicated at the top of the statement).

It is one of the fundamental documents that make up a company’s financial

statements. The balance sheet also reveals the book value of a company’s assets,liabilities and shareholder’s equity.

Structure of the balance sheet

NB: A positive balance means a credit balance while a negative balance

means a debit balance.

We used the same example which is above

Illustration1

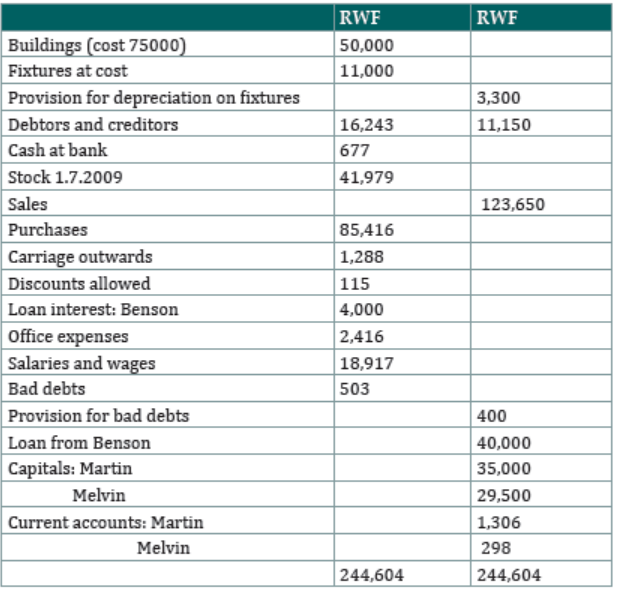

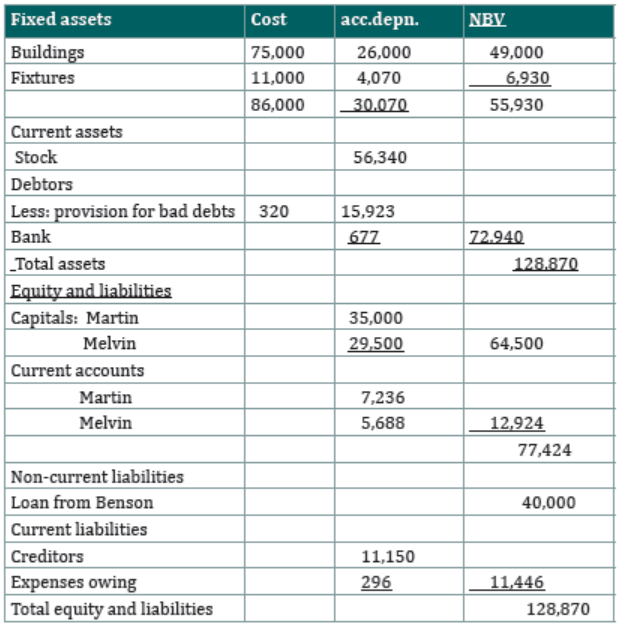

Martin and Melvin are in a partnership sharing profits and losses equally. Thefollowing is their trial balance as at 30.06.2010

Required: Prepare balance sheet for the year ended 30.06.2010

Additional information:

a) Stock 30.06.2010 was 56,340

b) Expenses to be accrued; office expenses 96, wages 200

c) Depreciate fixtures 10% on reducing balance basis, buildings 1,000

d) Reduce provision for bad debts to 320

e) Partnership salary 800 to Martin not yet paid.

f) Interest on drawings: Martin 180

Melvin 120

g) Interest on capital account at 10%.

Solution:

Balance sheet as at 30.06.2010

Changes in ownership of partnership

These include:

– Admission of a partner

– Death of a partner

– Dissolution

i. Admission of a partner

A new partner(s) can be introduced after all partners are in agreement to

this effect. The old partnership ceases to exist and a new partnership starts.

The accounts of the old partnership can be closed then a new set of accounts

prepared for the new partnership. This is really followed. So admission of a

partner merely entails addition of a capital column for the new partner and thefollowing entries thereafter:

Dr Asset accounts

Cr Capital account (with assets received from the joining partner which canbe cash)

However, both admission and retirement/death bring about the followingadditional issues:

Goodwill will be recorded during any change in ownership as follows:

Dr Goodwill account

Cr Capital accounts (in old profit sharing ratio)

This can remain in the accounts like this or it can be eliminated. If it remainsin the accounts, then the partners’ capital would have increased.

Goodwill can be eliminated as soon as transition in ownership is complete by:

Dr Capital accounts (in new profit sharing ratio)

Cr Goodwill

This is of course, subject to continuance of the business. Goodwill will not beeliminated if there is no business continuance like in dissolution.

This process ensures that the joining partner pays for the goodwill that

had already existed. This is because the new profit share ratio will includethe new partner.

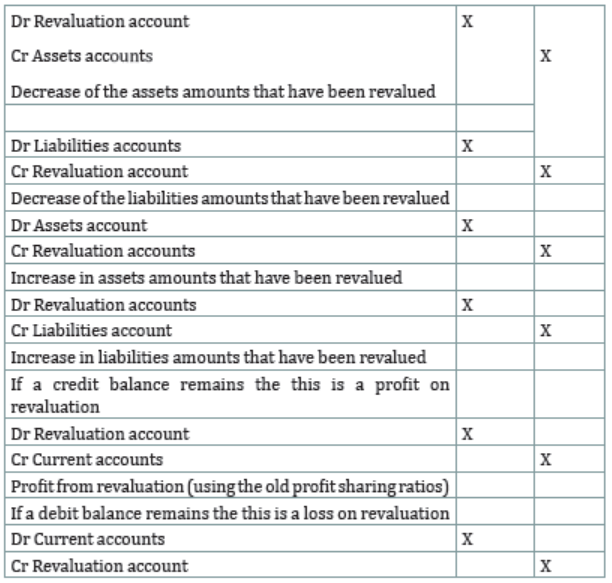

Revaluation account

Revaluation of assets and liabilities are usually carried out during changes in

ownership. In such cases account will be opened.

After opening the revaluation account is just to find increase or decrease dueto revaluation, which is dealt with in the following way.

Loss from revaluation (using the old profit sharing ratios)

If there any changes in between the year then the profit or loss up to this date

has to be shared to the old partners. After the changes the profit/loss earned

or incurred is shared to the new partnership in the new structure. Sometimes

the expenses can be divided between the periods to be able to determine theprofit that period.

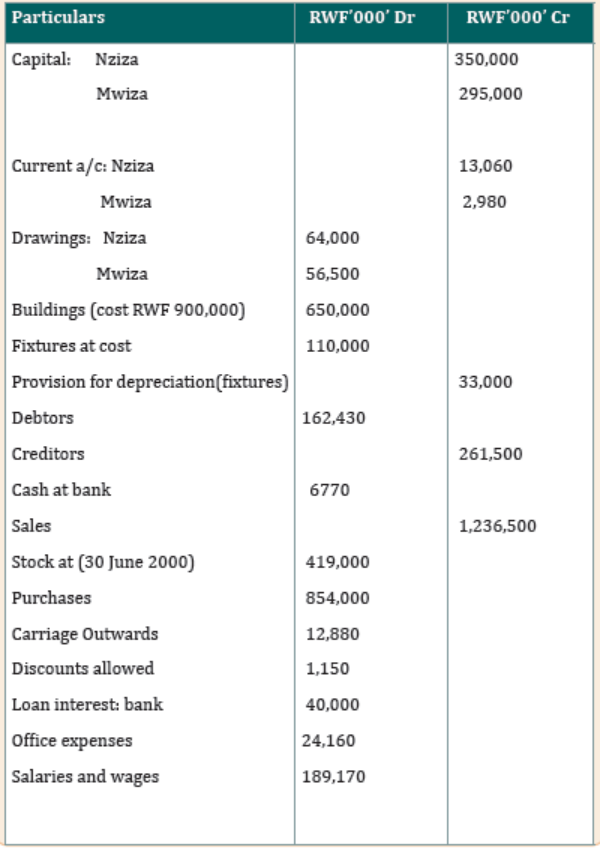

Nziza and Mwiza are in partnership sharing profits and losses equally. The

following is their balance as at 30 June 2001

Additional information:

i. Stock, 30 June, RWF 650,000

ii. Expenses to be accrued: Office expenses RWF 800, wages RWF1,500

iii. Depreciate fixtures 10 per cent on reducing balance basis, building

RWF 12,000

iv. Reduce provision for bad debts to RWF 3,200

v. Partnership salary: RWF1,500 to Nziza

vi. Interest on drawings: Nziza RWF 1,500; Mwiza RWF 1,100vii. Interest on capital account balances at 10 per cent.

Required:

Prepare a trading and Profit and Loss appropriation account for the yearended 30 June 2001, and a balance sheet as at that date.

End unit assessment 3

1. What do you understand about:

– Fixed capital accounts

– Current accounts– Fluctuating capital accounts

2. Where partners do not prepare an agreement.

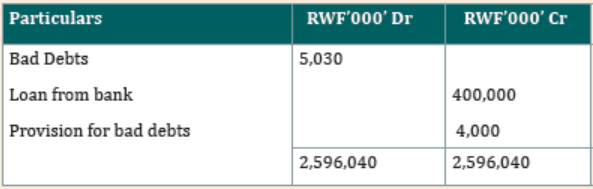

3. Okello, Opio and Ouma are in partnership. At the end of the firstyear they had the following details; on 31/12/2006.

Additional information

i. Depreciate all fixed assets at a rate of 10% p.a

ii. There was no partnership agreement.

Required:

a) Prepare a profit and Loss Appropriation account

b) Prepare partners current accounts

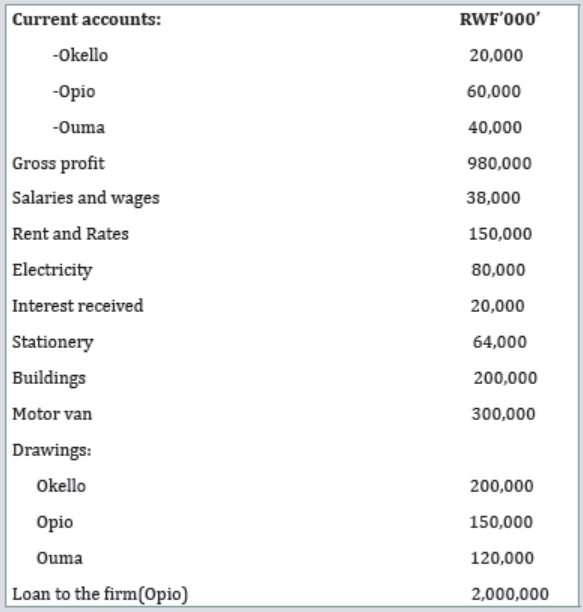

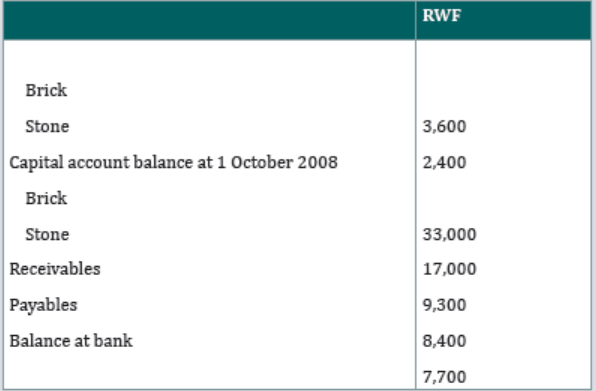

3. 3. The following list of balances as at 30 September 2009 has been

extracted from the books of Brick and Stone, trading partnership,

sharing the balance of profits and losses in the proportions 3:2respectively.

Additional information

i. RWF 10,000 is to be transferred from Brick’s capital account to a

newly opened Brick Loan

Account on 1 July 2009, interest at 10 per cent p.an on the loan is to

be credited to Brick

ii. Stone is to be credited with a salary at the rate of RWF12,000 per

annum from 1 April 2009.

iii. Inventory at 30 September 2009 has been valued at cost at

RWF32,000.

iv. Telephone charges accrued due at 30 September 2009 amounted to

RWF400 and rent of RWF600 prepaid at that date.

v. During the year ended 30 September 2009 Stone has taken goods

costing RWF1,000 for his own use.

vi. Depreciation is to be provided at the following annual rates on thestraight line basis: Fixtures and fittings 10% Motor vehicles 20%

Required:

a) Income statement and appropriation account for the year ended30 September 2009.

b) Prepare a Statement of financial position as at 30 September

2009, which should include summaries of the partners’ capitaland current accounts for the year ended on that date