Unit 2 FINANCIAL STATEMENTS FOR A SOLE TRADER AFTER ADJUSTMENTS

Key Unit competence: To be able to prepare financial statements of asole trader after adjustments.

Introductory activity

Joyce, a sole trader in Remera, she records her business transactions

daily. After preparing the trial balance for the year 2022, she found out

some additional information which caused the trial balance to be adjusted

following the accounting cycle. The step of accounting cycle after adjustedtrial balance is to prepare financial statements.

Required:

a) As a professional accountant, advice Joyce (sole trader) on the

main financial statements that can be prepared for the proper

books of accounts of her business.

b) Show the main elements of each financial statement to be preparedby Joyce.

2.1. Income statement/ Statement of Profit or Loss afteradjustments

Learning Activity 2.1

ABC business has been performing well almost for five years since 2016

and currently it is experiencing a drop/loss in their profits according to

the financial performance for the year 2021. Apart from this drop, after

deep checking, some additional information needs adjustments. Owners

are complaining about the current performance of their business. As an

accountant of ABC Business, explain to the owners about the performanceof their business.

a) The loss for the period can be identified using which component of

financial statement?b) Show the main parts/components of statement of profit or Loss.

As seen in Senior 4 unit 10, at the end of year, every business must ascertain itsnet profit/loss. This is done in two stages.

1. Finding out the Gross Profit / Gross Loss which is got with Trading

Account2. Finding out the Net Profit / Loss which is got with Profit or Loss Account

2..1.1.Determination of Gross Profit /Gross Loss after adjustments

The entries/items that will appear in the Trading Account to ascertain the GrossProfit/Loss will be: (some items will be debited while other will be credited)

i. Items to be debited

1. Opening stock

It speaks of the inventory that was on hand at the start of the prior accounting

year. Opening stock is the quantity of an item present at the start of a new period

for keeping inventory. It contains the worth of the goods that the companydeals in and serves as the opening stock for the current accounting year.

2. Purchases

It refers to the value of goods (in which the concern deals) which are purchased

either on cash or on credit for the purpose of resale. The balance of purchases

account, appearing in the trial balance, reflects the total purchases made during

the accounting period. While dealing with purchases, we must bear in mind the

following aspects:

a) Purchase of capital asset should not be added with the purchases. If it

is already included in purchases, it should be deducted immediately.

b) If goods are purchased for personal consumption and they are added

with the purchases, they should be excluded. These types of purchases

should be treated as drawings.

c) If some of goods purchased are still in transit at the year-end, it is

better to debit stock-in-transit Account and credit Cash or Supplier’sAccount.

d) If the amounts of purchases include goods received on consignment, on

approval or on hire purchase, these should be excluded from purchases.

e) Cost of goods sent on consignment must be deducted from thepurchases in case of trading concern.

3. Sales return/ Return Inwards

In the books of account, Returns Inwards Account or Sales Returns Account

is debited and buyer’s account is credited. It appears on the debit side of Trial

Balance. We can show the sales returns in Trading Account in two ways. It may

be shown by way of deduction from sales in the Trading Account. An alternative

way to show the sales returns is in the debit side of the Trading Account.

4. Direct expenses/carriage inwards

These types of expenses are directly incurred in connection with purchases,

procurement or production of goods. These expenses are directly related to the

process of production. They also include expenses that bring the goods up to

the point of sale.

ii. Items to be credited

1. Sales

It refers to the sale of goods in which the business deals and includes both

cash and credit sales. It does not include sale of old, obsolete or depreciated

assets, which were acquired for utilization in business. However, goods sent to

customers on approval basis, free samples and sales tax, if any, included in thesales figure should be excluded.

2. Purchases returns

It may come about that due to some reasons: the goods are sent back to the

supplier. In that case, the supplier is debited in the books of accounts and

purchases returns or returns outwards are credited. It appears on credit side in

the trial balance. There are two ways of showing the purchases returns in the

income statement. It may be shown by way of deduction from purchases in the

income statement. An alternative way is to show the purchases returns in thecredit side of the income statement.

3. Closing stock

It refers to the value of goods lying unsold at the end of any accounting year.

This stock at the end is called closing stock and is valued at either cost or market

price, which is lower. The trial balance generally does not include closing stock.

Therefore, the following entry is recorded to incorporate the effect of closingstock in the income statement;

Dr. Closing Stock A/C

Cr. To Trading A/C

However, if closing stock forms a part of Trial Balance, it will not be transferred

to Income Statement but taken only to the statement of Financial Position. In

case of the goods that have been dispatched to customers on approval basis,such goods should be included in the value of closing stock.

Ascertain the Gross Profit or Loss

After recording the above items in the respective sides of the income

statement, the balance is calculated to ascertain Gross Profit or Gross Loss.

As seen in Senior 4, if the total of credit side is more than that of the debit side,

the excess represents Gross Profit. Conversely, if the total debit side is more

than that of the credit side, the excess represents Gross Loss. Remember thatthe Gross profit is ascertained using the Trading Account.

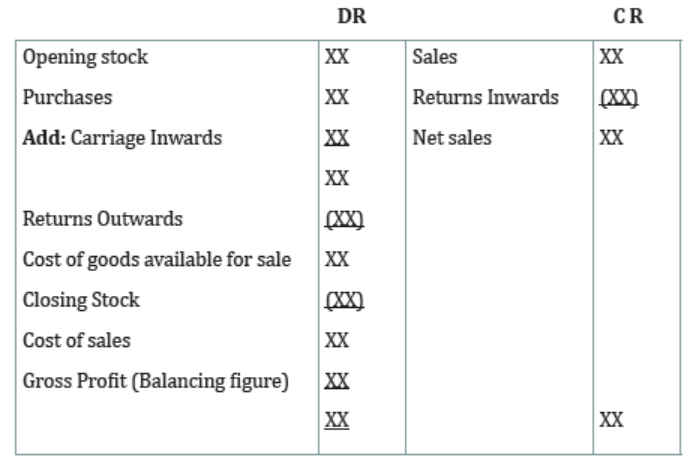

TRADING ACCOUNT (HORIZONTAL FORMAT)

Name of the company (date/month/year)

Or

TRADING ACCOUNT (HORIZONTAL FORMAT)

Name of the company (date/month/year)

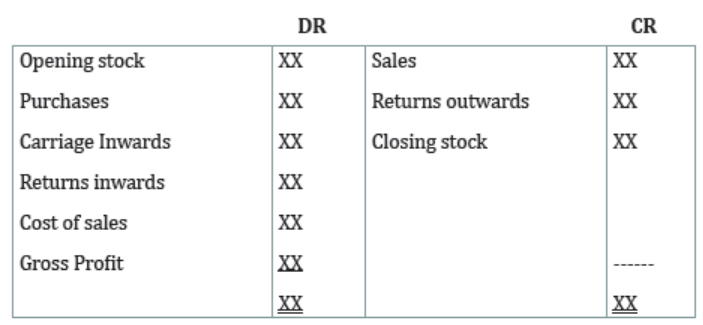

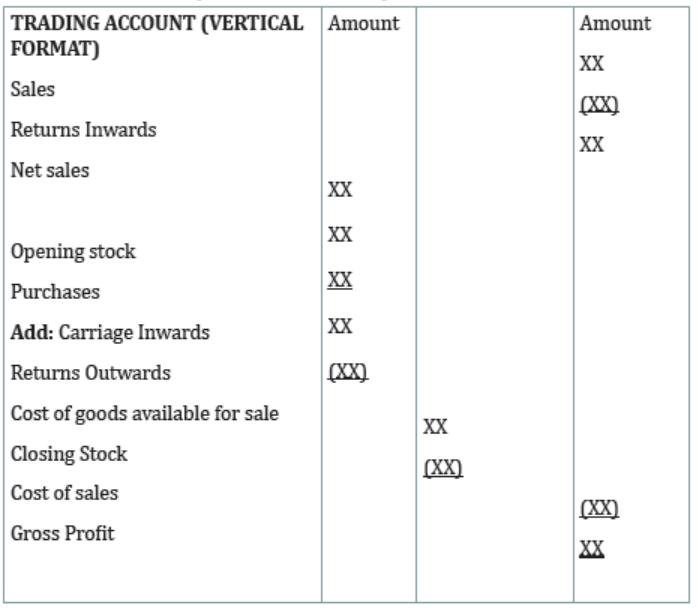

TRADING ACCOUNT (VERTICAL FORMAT)

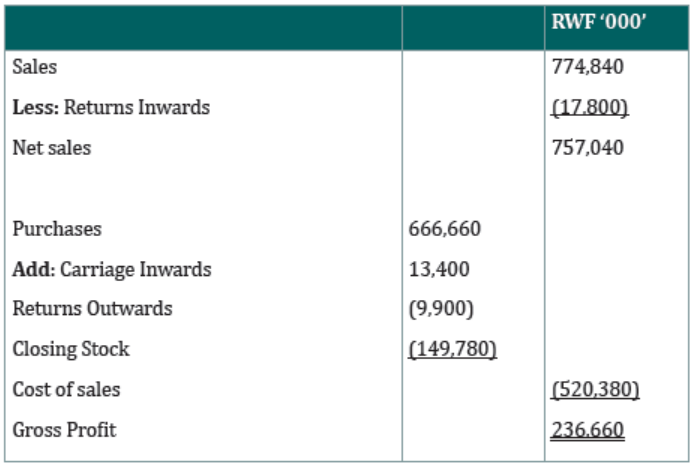

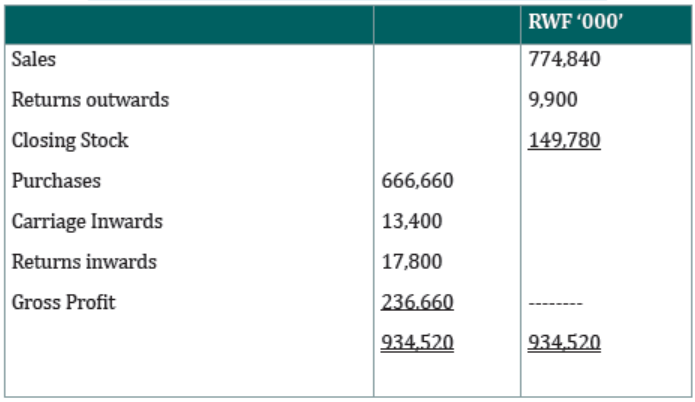

Illustration1

From the following details draw up the trading account of Mr Kamanda for theyear ended 31st December 2022, which was his first year in business.

Mr Kamanda

Trading Account for the year ended 31 December 2022

Mr. Kamanda

Trading Account for the year ended 31 December 2022

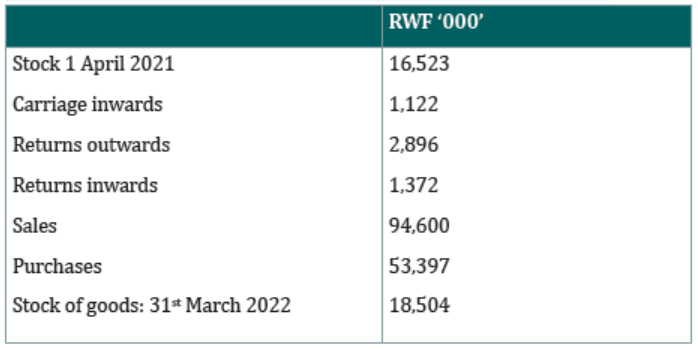

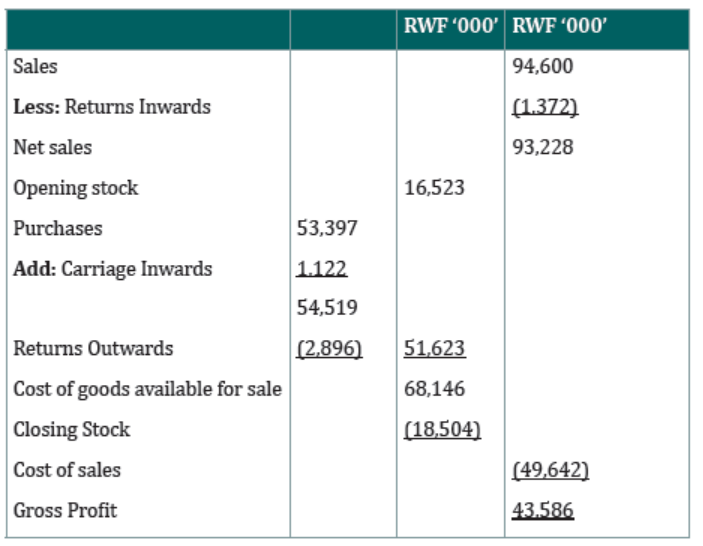

Illustration 2

The following details for the year ended 31st March 2022 are available for

Bosco’s business. Draw up the Trading account of Bosco for that year.

Bosco

Trading Account for the year ended 31 March 2022

Determination of net profit (or Loss) after adjustments

After ascertaining the gross profit, the subsequent step is to ascertain net profit

or net loss during an accounting period. The net income/profit is measured by

matching revenues and expenses. Net income is the difference between totalrevenues and total expenses.

a) Items to be debited to the Income Statement

i. Management expenses

These are the expenses incurred for carrying out the day-to-day administration

of a business. Expenses under this head include office salaries, office rent andlighting, printing and stationery, telegrams, telephone charges etc.

ii. Selling and distribution expenses

These expenses are incurred for selling and distribution of products and

services, as the name indicates, they comprise of commissions and salaries ofsalesmen, advertising expenses, packaging, bad debts etc.

iii. Maintenance Expenses

These expenses are incurred for maintaining the fixed assets of the

administrative offices in a good condition. They include expenses towardsrepairs and renewals.

iv. Financial expenses

These expenses are incurred for arranging finances necessary for running the

business. These include interest on loans, discount on bills, brokerage and legalexpenses for raising loans etc.

v. Abnormal losses

Some abnormal losses may arise during the accounting period. All types of

abnormal losses are treated as unusual expenses and debited to Profit and Loss

Account. Examples are stock lost by fire but not covered by insurance, loss onsale of machinery, cash defalcation etc.

vi. Wages and salaries earned by the worker-whether paid or not

N.B: To ascertain the amount of expenses to be debited to the income statement,

four types of events are essentially considered and then cash payment is madein connection with these events they are as under:

Expenses incurred and paid out in that year: those will be debited to theincome statement.

Expenses incurred but not paid out, partly or fully, during the current year

(outstanding expenses): on the date of the final accounts, those are in form of

both the expenses and a liability and they exist without having been recorded

in the books of accounts. For recording it, the following entry is to be passed:

• Dr. Expenses A/C Dr. (will be shown in the income statement account)

• Cr. Outstanding Expenses A/C (will appear in the liabilities side ofstatement of Financial Position)

• Expenses paid for during the current year, but not incurred as

yet, partly or fully (prepaid expenses): these are assets and will beshown in the Statement of Financial Position.

• Expenses of the current year, likely to arise in subsequent period:

in such case, we make a provision for the anticipated loss and a charge

is created against the profit for the current period. This provision is

shown as either a liability or contingent asset, i.e. it appears in the

statement of Financial Position as a deduction from some other assets.The best example of this anticipated expense is Provision for Bad Debt.

a) Items to be credited to the Income Statement

i. Other incomes

Sometimes a business might generate some profits, which is not due to the sale

of its goods or services because the business may have some other source of

financial income. The examples are discount or commission received.

ii. Non-trading Income

The business may have various transactions with the bank. At the end of the

year, the business may earn some amount of interest, which will find a place in

the profit & Loss Account as non-trading income. The business may have some

investment outside the business in the form of shares, debentures or units. All

sorts of gains obtained from such kinds of investments are considered as nontrading

income and are treated accordingly.

iii. Abnormal gains

There may be capital gains arising during the course of the year, e.g. profit

arising out of sale of a fixed asset. The profit is shown as a separate income

on the credit side of the Profit & Loss Account. We must remember that all

incomes from the abnormal gains or other incomes should be credited to the

Profit &Loss Account if they arise of accrues during the period. Similarly, income

received in advance should be deducted from the income.

Ascertaining the net Profit &Loss

Once the respective accounts are transferred from trial balance to income

statement, gross profit/ loss ascertained and all adjustments are taken care of,

the income statement will now be balanced. The totals of incomes and expenses

are computed and the difference between these totals is either a net profit or

net loss. If the total of expenses exceeds the total of incomes, there is a net Loss,

whereas when the total of incomes exceeds the total of expenses, there is a netprofit. Net profit/ loss is the last item to be recorded in income statement.

When the Profit and loss account shows a net profit, we pass the followingentry:

Dr. Profit &Loss A/C

Cr. Net Profit A/C

If the Profit and Loss Account shows a net loss, the entry will be reserved.

Format of income Statement

The Formats of Statement of Profit or Loss was discussed in S4 Unit 10

Illustration 1

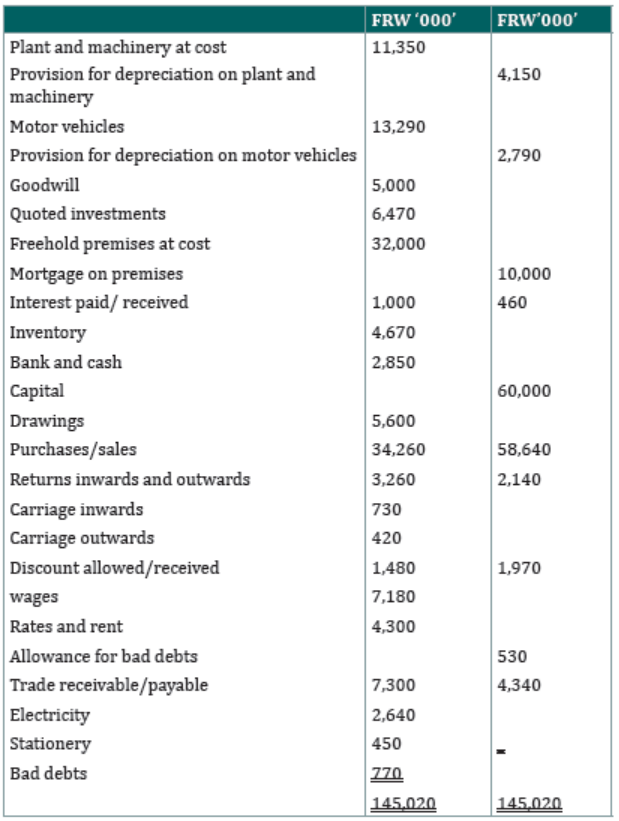

The following trial balance was extracted from the books of Mugabe, a soletrader as at 31st August 2022.

Additional information

1. Inventory as at 31st August 2022 was valued at FRW 3,690,000

2. Allowance for bad debts is to be adjusted at 10 % of debts

3. Goods which costed FRW 300,000 had erroneously been invoiced to a

customer for FRW 400,000 and had been accounted for in sales

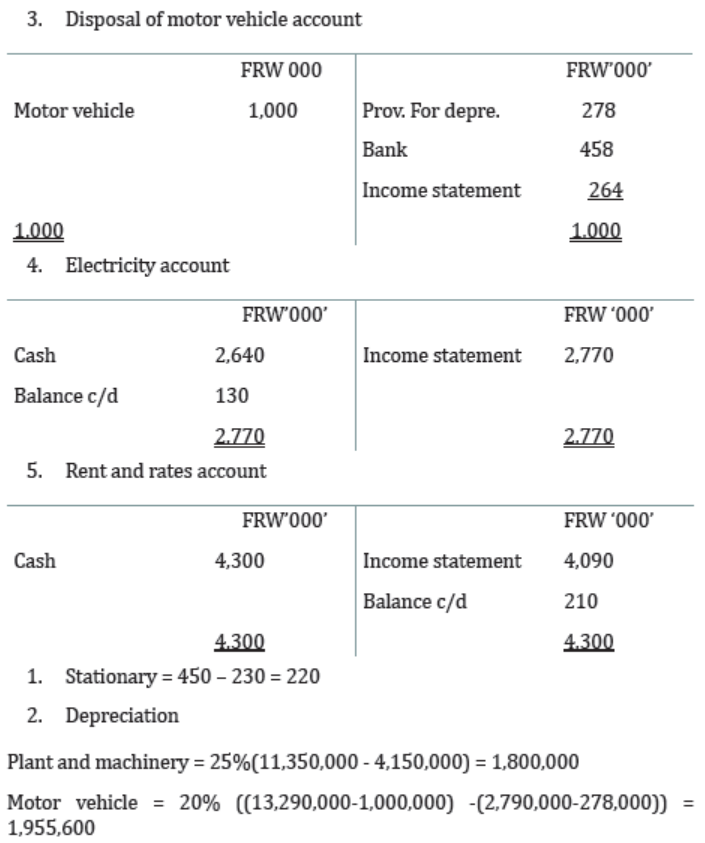

4. Electricity accrued as at 31st August 2022 was FRW 130,000 and

prepaid rates amounted to FRW 210,000 as at 31st August 2022

5. Stock of stationery as at 31st August 2021 was FRW 230,000

6. Depreciation is to be provided on pro rata basis as follows:

• Motor vehicles 20% on reducing balance method

• Plant and machinery 25% on reducing balance

7. A motor vehicle was sold on credit on 1st December 2021 for FRW

458,000. The motor vehicle had been bought on 1st June 2020 for FRW

1,000,000 the sale had not been recorded to the ledger., proportionatedepreciation is applicable until disposal date

8. During the year, Mugabe took goods worth FRW 350,000 from the

business for his own use.

Required: Prepare Income Statement/ Statement of Profit or Loss for theyear ended 31st August 2022

Solution

Workings:

1. Provision for bad debts = 7,300,000*10% = 730,000

Increase in previous for bad debts = 730,000 - 530,000 = 200,000

2. Motor vehicle depreciation:

1st period of 3 months 20%*1,000,000*3/12 50,000

2nd period full year 20%*(1,000,000 - 50,000) 190,000

3rd period 20% (1,000,000-50,000 - 190,000) *3/12 38,000

278,000

NBV = 1,000,000 – 278,000 = 722,000

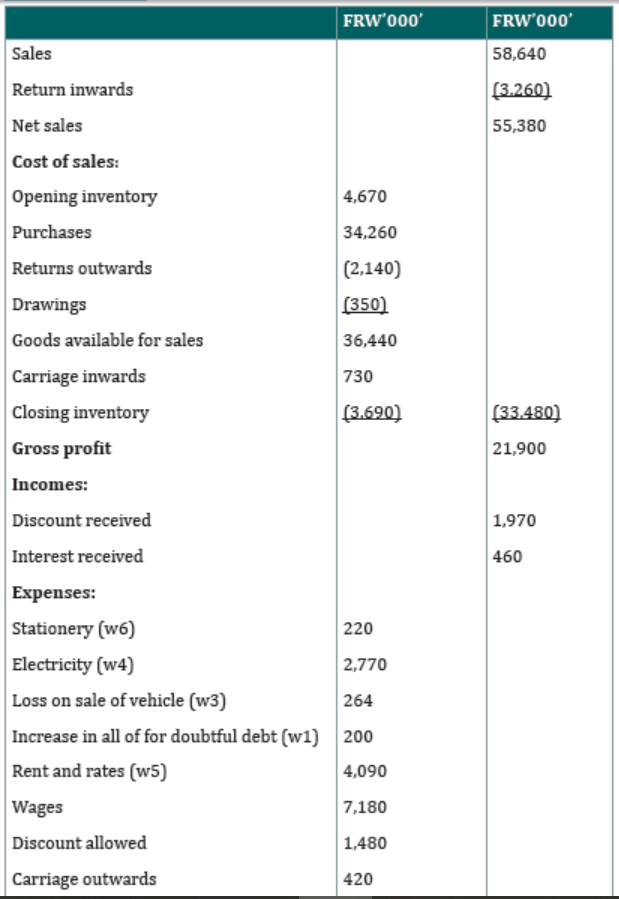

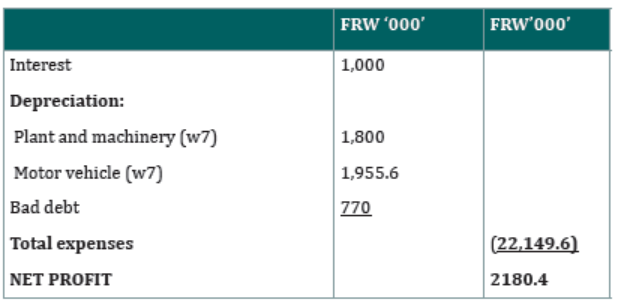

Mugabe Income statement/ statement of Profit or Loss for the year ended

31st August 2022

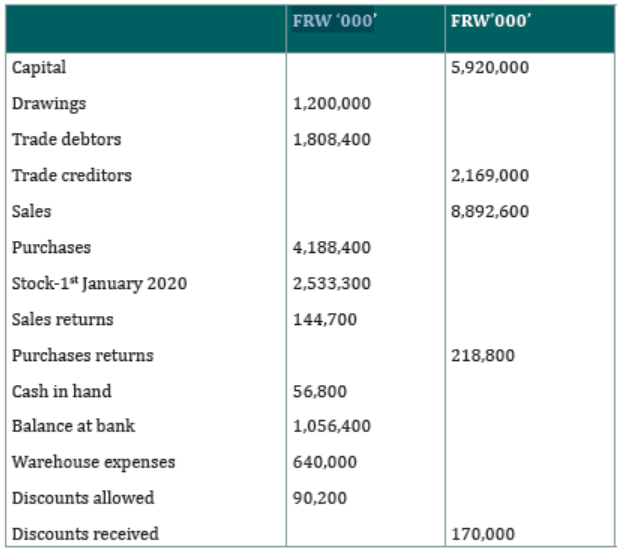

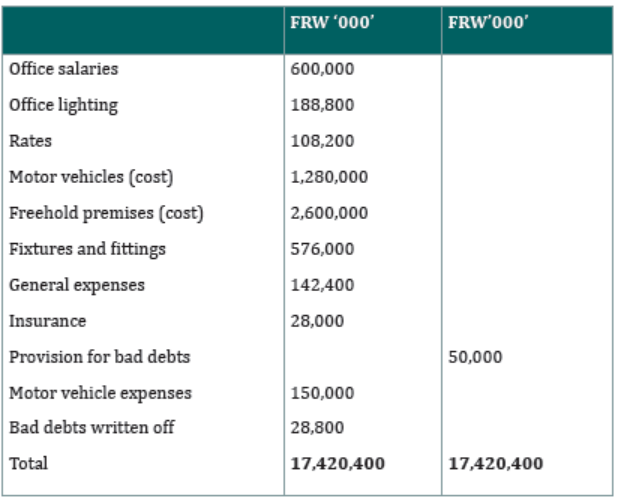

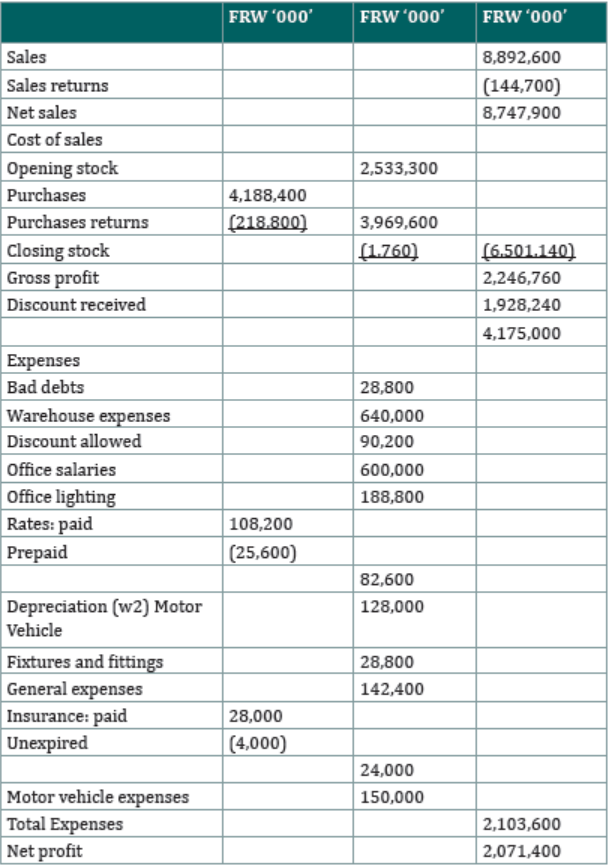

Illustration 2

The following trial balance was extracted from the books of MIRIMO, a sole

trader for the year ended 31st December 2020FRW ‘000

Additional information:

1. Stock as at 31st December 2020 was valued at FRW 1,760,000

2. Depreciation on fixtures and fittings and motor vehicle is to be provided

at the rate of 5% and 10 % per annum respectively

3. Rates prepaid as at 31st December 2020 amounted to FRW 25,600,000

4. Unexpired insurance as at 31st December 2020 is to be made at FRW 4Million.

5. Additional FRW 1,758,240 Discount received is to be madeRequired:

Prepare Statement of Profit or Loss for the year ended 31st December 2020

Solution

MIRIMO

Statement of Profit or Loss for the year ended 31December 2020

Illustration 3

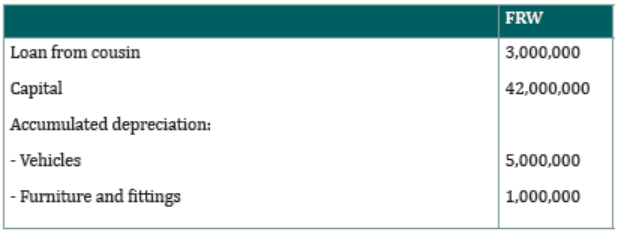

The following balances were extracted from ENOCK’s accounting books at theend of the financial year on 30th June 2020.

Additional information

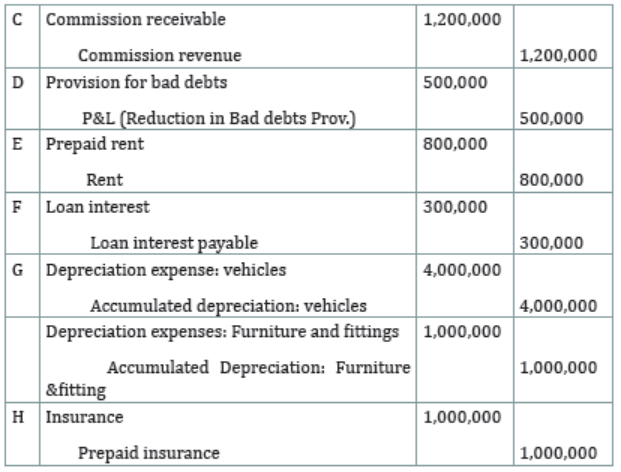

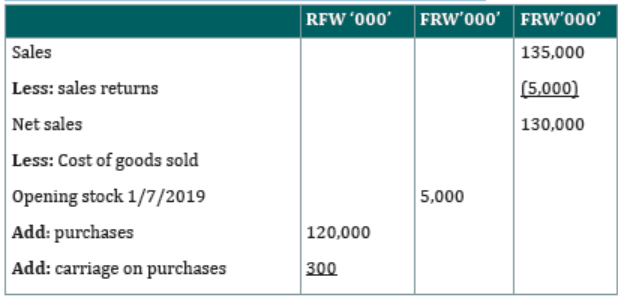

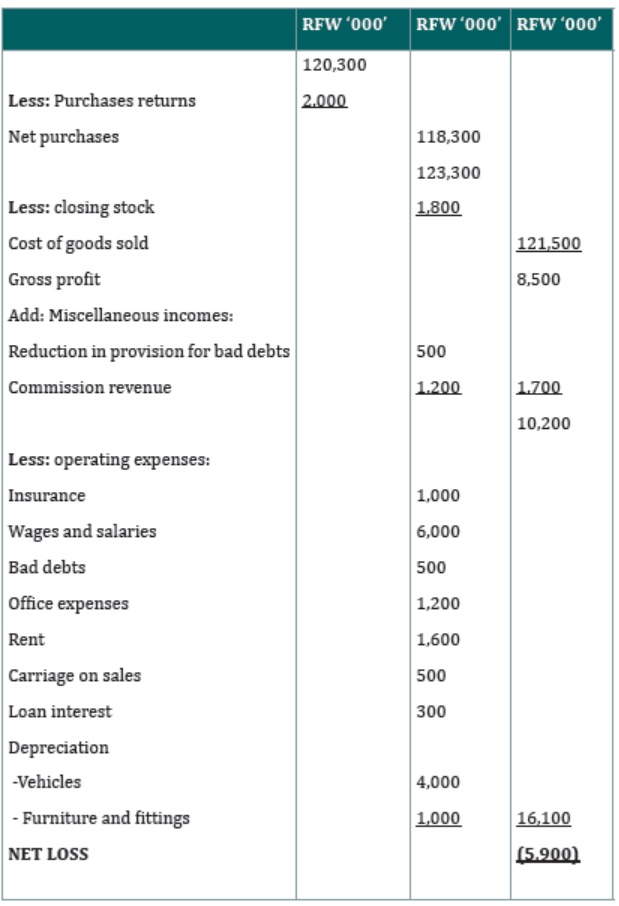

a) Stock of goods in trade was valued at FRW 1,800,000 at the end of the

year

b) FRW 300,000 of the carriage relates to purchases and the balance

relates to sales

c) Enock receives a commission of 1% of gross purchases. The outstanding

balance of the commission for the year ended is to be received on 5th

day of the following financial year.

d) The provision for bad debts is to be reduced by 10% of the trade

debtor’s figure

e) Rent was paid on the first day of the financial year to cover a period of

18 months.

f) The loan from cousin was acquired on 1st January (within the financial

year), it is at interest rate of 20% per annum. Interest due for the period

is outstanding.

g) Vehicles are to be depreciated by 20% per annum on reducing balance

method and furniture and fittings by 10% per annum on cost.

h) Prepaid insurance of FRW 1,000,000 expired on 30th June 2020 (thelast day of the financial year).

Required:

a) a) Journal entry to record adjusting information c-h

b) b) Statement of Profit or Loss (Income Statement) for the year ended

30th June 2020.

Solution:

Enock

Journal entries to record Adjusting information on 30/6/2020

Enock

Statement of Profit or Loss for the year ended 30/6/2020

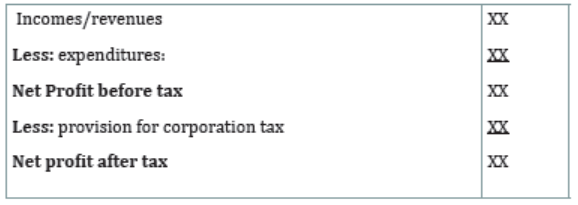

Income statement/ Statement of Profit or Loss in service firms

The income statement/ Statement of Profit or Loss for service sector firms e.g.

banks; insurance companies, etc are simple to draw up as it does not containthe trading Account. Their formats are shown as follows:

Statement of Profit or Loss

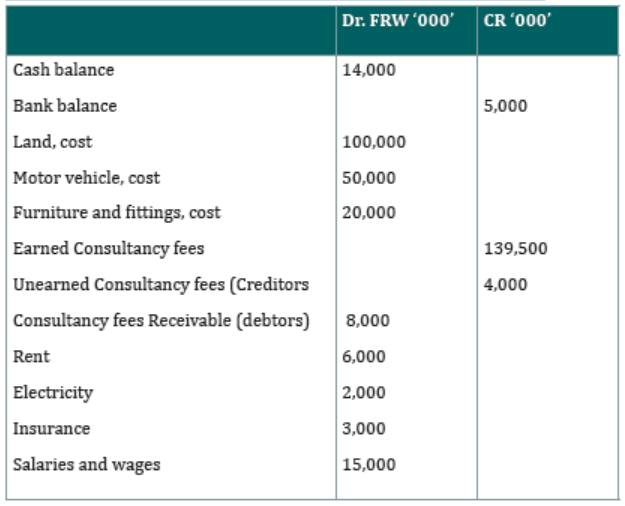

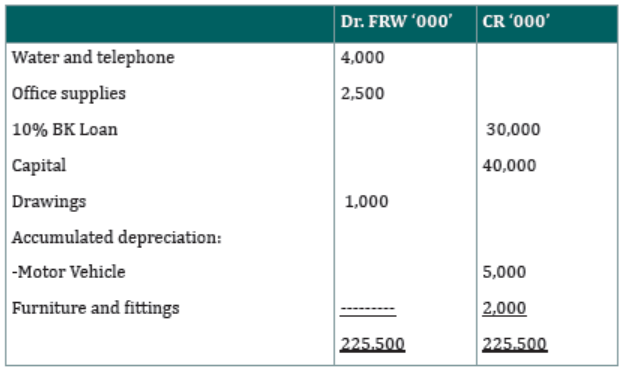

Illustration 4

Peter, a consultant in accountancy services prepared the following trial balancefor his Door way consultancy for the financial year ended 31/8/2019

Information for adjustments at the end of the year

1. Consultancy fees of FRW 2,000,000 which were unearned were earned

on 31/8/2019. The trial balance does not reflect this information.

2. Customers who were provided with services during the year ended

to June 2019 amounting to FRW 3,500,000 were not yet invoiced by

31/8/2019.

3. Hand count of office supplies on 31/8/2019 revealed that office supplies

worth FRW 500,000 remained in inventory

4. Depreciate Furniture and fittings and motor vehicles by 10% on cost

5. Loan interest for one year accrued

6. Electricity bills amounting to FRW 1,500,000 remained outstanding on

31/8/2019

7. A provision of corporation tax to be paid at the rate of 30% of pre-tax netprofit should be made.

Required:

Statement of Profit or Loss of Peter’s Consultancy at the end of the FinancialYear on 31/8/2019

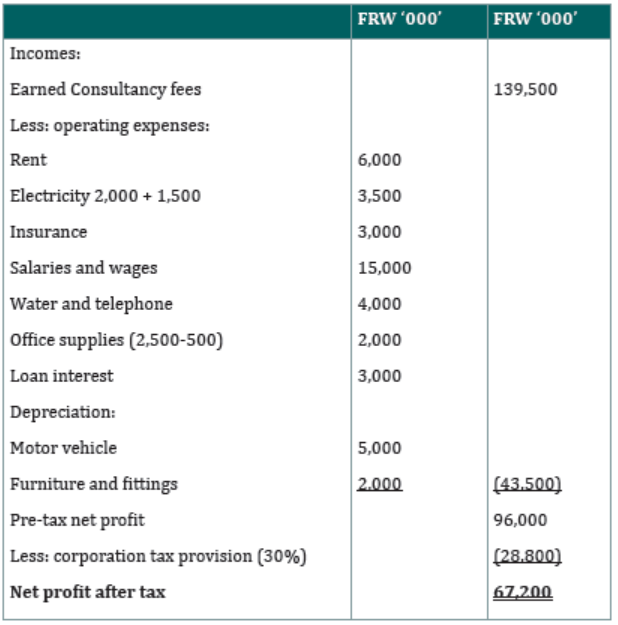

Solution

Door way Consultancy Income Statement/ Statement of Profit or Loss for

the period ended 31/8/2019

Application activity 2.1

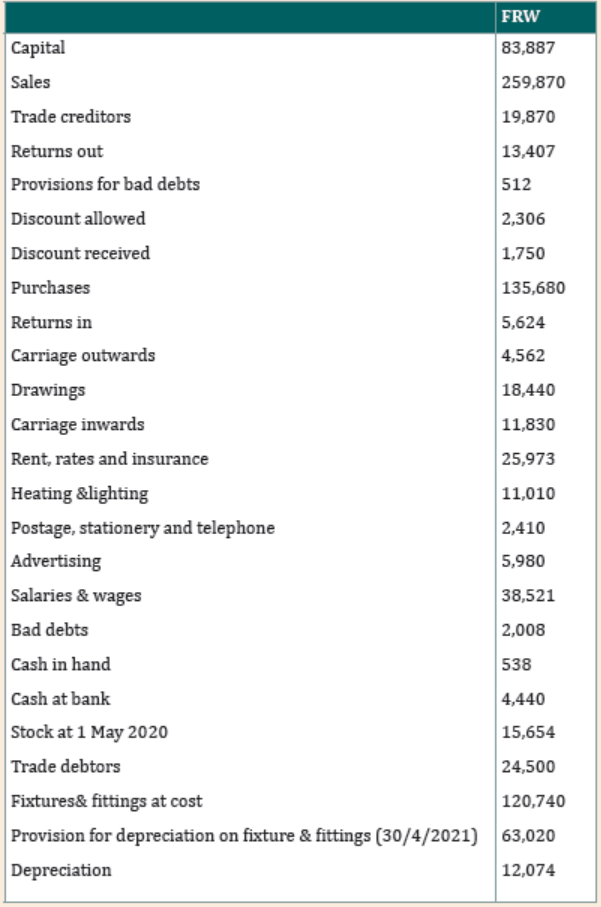

Mr Amandi has been trading for some years as Wine merchant. The

following list of balances has been extracted from his ledger as at 30 April2020, the end of his financial year.

Additional information:

a) Stock at the close of business was valued at FRW 17,750.

b) Insurance has been prepaid by FRW 1,120

c) Heating and lighting is accrued by FRW 1,360

d) Rates have been prepaid by FRW 5,435

e) The provision for bad debts is to be adjusted so that it is 3% of trade

debtors

REQUIRED: Prepare Mr Amandi’s trading, profit and Loss account for the yearended 30 April 2020.

2.2. Balance sheet (statement of Financial position) afteradjustments

Learning Activity 2.2

A local business located in Nyabihu District owned by Annette collects and

distributes Irish potatoes. At the end of 2022, while closing the financial

period, Annette was not aware on the statement to be prepared. You are

asked

1. To advise her on which statement to be prepared in order to knowthe financial position of her business.

Learning Activity 2.2

A Statement of Financial Position is a summary of the financial balances of a sole

proprietorship, business partnership or a company. It is a statement that helps

us to establish the financial position of a business enterprise on a particular

date, i.e. on a date when financial statements or final accounts are prepared or

books of accounts are closed.

In facts, this statement treats the balances of all those ledger accounts that have

not yet been squared up. These accounts relate to assets owned, expenses due

but not paid, incomes accrued but not received or certain receipts which are

not due or accrued. In other words, it deals with all those real and personal

accounts which have not been accounted for in trading or Profit & Loss accounts.

Therefore, an important feature of a statement of financial position is to showthe exact financial picture of a business concern on a particular date.

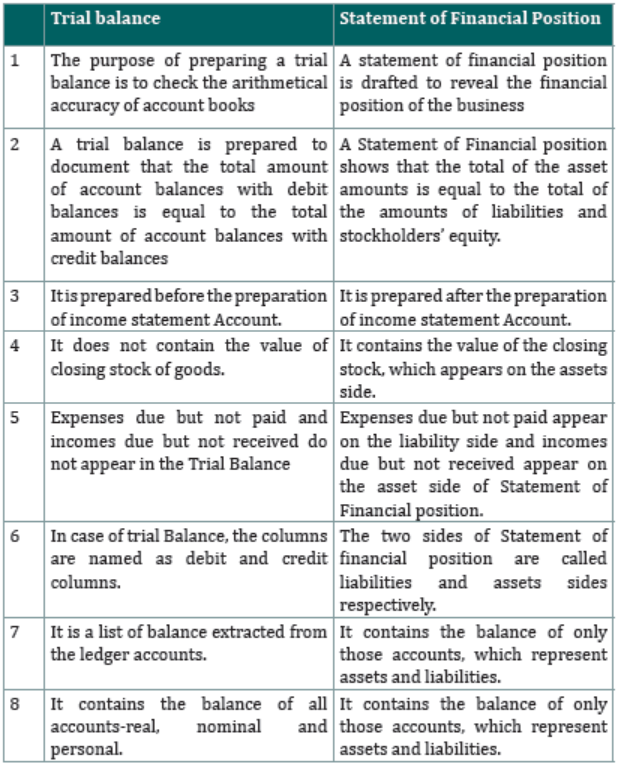

2.2.1. Difference between trial balance and Statement of FinancialPosition

2.2.2. Preparation and presentation of statement of Financial

position

The process of preparation and presentation of statement of financial positioninvolves two steps:

• Grouping

• Marshalling

Grouping

In the first step, the different items to be shown as assets and liabilities in the

Statement of Financial Position are grouped appropriately. For this purpose,

items of similar nature are grouped under one head so that the Balance Sheet

could convey an honest and true message to its users. For example, stock,

debtors, bills receivables, bank, cash in hand etc. are grouped under the

heading current Assets and land and Building, plant and Machinery, Furniture

and fittings, tools and equipment under Non-Current Assets. Similarly, sundry

creditors for goods must be shown separately and distinguished from moneyowing, other than due to credit sales of goods.

Marshalling

The second step involves marshalling of assets and liabilities. This involves

a sequential arrangement of all the assets and liabilities in the statement ofFinancial Position. There are two methods of presentation:

• The order of liquidity

• The order of permanence

Under liquidity order, assets are shown on the basis of liquidity or reliability.

These are rearranged in an order of most liquid, more liquid, liquid, least liquid

and not liquid (fixed) assets. Similarly, liabilities are arranged in the order in

which they are to be paid or discharged.

Under order of permanence, the assets are arranged on the basis of their useful

life. The assets predicted to be most fruitful for the business transaction for

the longest duration will be shown first. In other words, this method puts the

first method in the reverse gear. Similarly, in case of liabilities, after capital,

the liabilities are arranged as long term, medium term, short term and currentliabilities. This is the commonly used method.

Classification of assets

1. Non-current assets

2. Intangible assets

3. Current assets

4. Fictitious assets

5. Wasting assets

6. Contingent assets

i. Non-current assets

These are those assets, which are acquired for the purpose of producing Goods

or rendering services. These are not held for resale in the normal course of

business. Fixed assets are used for the purpose of earning revenue and hence

these are held for a longer duration. Investment in these assets is known as‘Sunk Cost”. All fixed assets are tangible by nature.

ii. Intangible assets

Intangible assets are those capital assets, which do not have any physical

existence. Although these assets cannot be seen or touched, they are long lasting

and prove to be profitable to owner by virtue of the right conferred upon them

by mere possession.

They also help the owner to generate income. Goodwill, trademarks, copyrightsand patents are the example of intangible assets.

iii. Current assets

Current assets include cash and other assets, which are converted or realized

into cash within a normal operating cycle or say, within a year.Current assets are also known as Floating Assets or Circulating Assets.

iv. Liquid or quick assets

These are current assets that can be converted into cash at a very short notice

or immediately, without incurring much loss or exposure to high risk. Quick

assets can be worked out by deducting Stock (raw materials, work-in-progressor finished goods) and prepaid expenses out of total current assets.

v. Fictitious assets

These are the non-existent worthless items which represent unwritten-off

losses or costs incurred in the past, which cannot be recovered in future or

realized in cash. Examples of such assets are preliminary expenses (formation

expenses), advertisement expense, underwriting commission, discount on

issue of shares and debentures, Loss on issue of debentures and debit balance

of income statement account. These fictitious assets are written off or wipedout by debiting them to income statement account.

vi. Wasting assets

An asset that has a limited life and therefore windless in value over time it is

called wasting asset. This type of asset has a limited useful life by nature and

depletes over a limited duration. These assets become worthless once their

utility is over or exhausts. During the life of productive usage, assets of this type

produce revenue, but eventually reach a state where the worth of the assets

begins to diminish. Such assets are natural resources like timber and coal, oil,mineral deposits etc.

vii. Contingent assets

Contingent assets are probable assets, which may or may not become assets,

as that depends upon occurrence or non-occurrence of a specified event or

performance or non-performance of a specified act. For example, a suit is

pending in the court of law against ownership title or a disputed property. If

the business does not win the lawsuit, it will not have ownership rights of the

property; it will be of no use to it. However, if it wins, the contingent asset will

become the asset of the concern. Such assets are shown by means of footnotesand hence do not form part of assets shown in the Balance Sheet.

Besides this, hire- purchase contract, uncalled share capital etc… are otherexamples of contingent assets.

Classification of liabilities

i. Non-current liabilities/long-term liabilities

ii. Current liabilities

iii. Contingent liabilities:

Contingent liability is an actual liability but anticipated (probable) liability

which may or may not become payable. It depends upon the occurrence of certain

events or performance of certain acts. If a parent guarantees a daughter’s first

car loan, the parent has a contingent liability. Contingent liabilities are shownas footnotes under the statement of financial position.

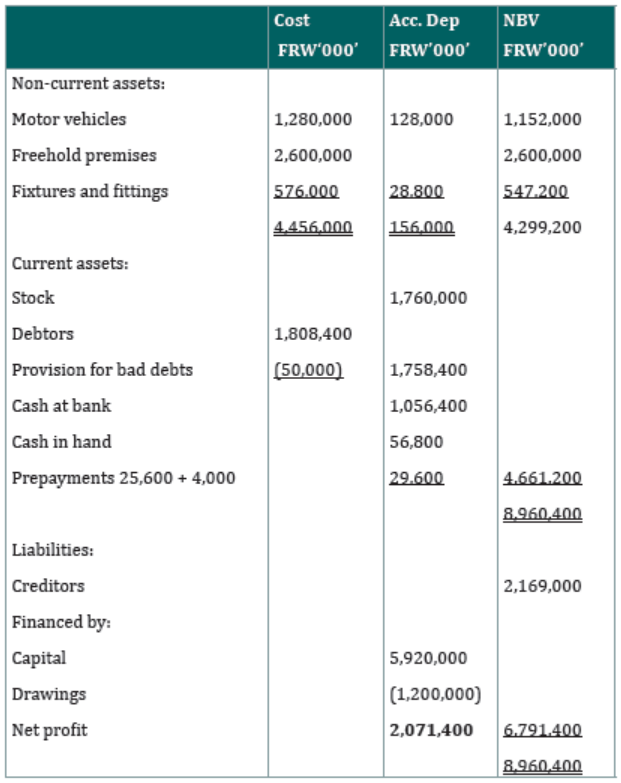

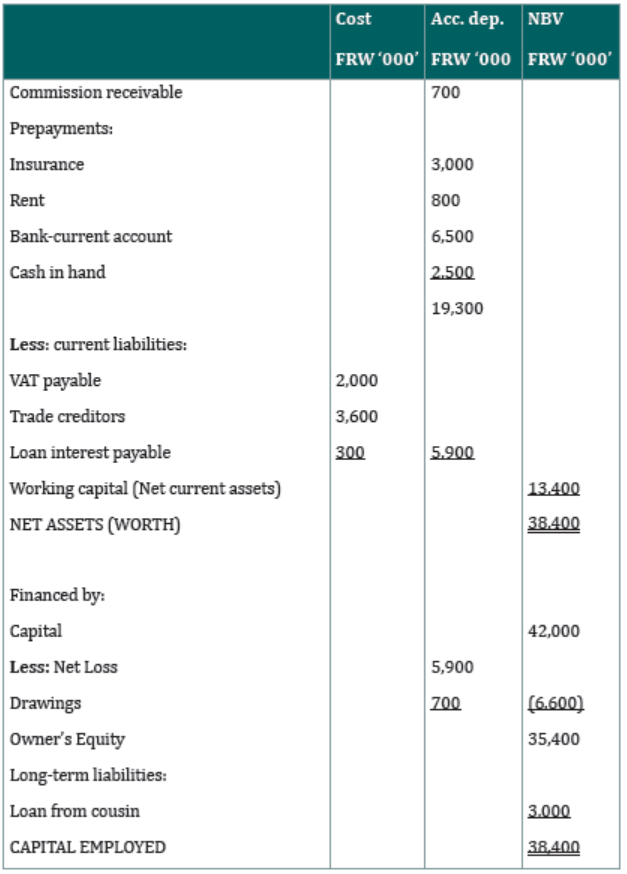

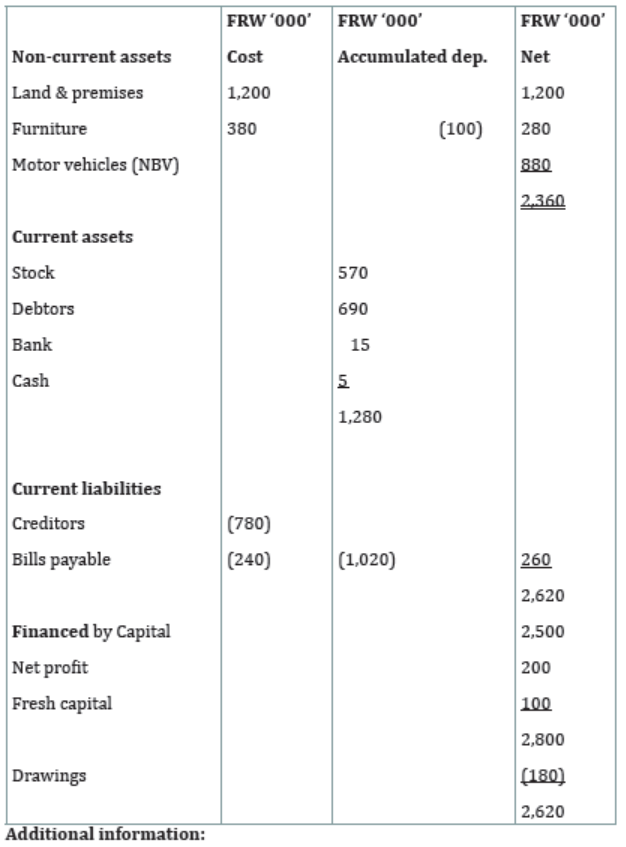

Illustration1. From illustration 2 in 2.1., prepare Mirimo’s Statement ofFinancial Position

Solution

MIRIMO

Statement of Financial Position

2.2.3. Prepare the Statement of Financial Position showing

working capital and capital employed

Types of capital

Different types of capital can be calculated as below:

i. Capital net worth/owned = total assets + total liabilities. The capital net

worth is also referred to as net worth or net assets

ii. Working capital = current assets – current liabilities

Working capital = capital employed –fixed assets

iii. Capital employed = total fixed assets + working capital or

Capital employed = owner’s equity + Long term liabilities

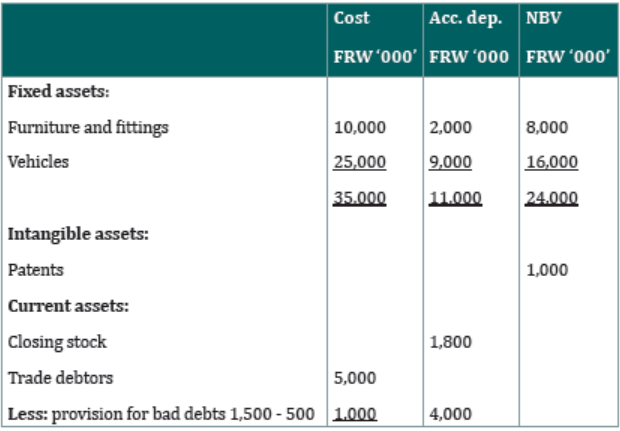

Illustration 2

Prepare the Statement of Financial Position of Enock for the period ended

31/6/2020 from illustration 3 in 2.1.

Solution

ENOCK

Statement of Financial Position as at 31/6/ 2020

Application activity 2.2

1. At 31st March 2022 Shalon was owed FRW 47,744,000 by her

customers. At the same date her allowance for receivables was

FRW 3,500,000. How should these balances be reported on Shalon’s

Statement of Financial position?

i. FRW 44,244,000 as a current asset

ii. FRW 3,500,000 as a current asset and FRW 47,744 as a current

liability

iii. FRW 47,7444 as a current asset and FRW 3,500,000 as a current

liability

iv. FRW 51,244,000 as a current asset

2. From the illustration 4 in 2.1. Prepare door Consultancy BalanceSheet as at 31/8/2019

2.3. Cash-Flow Statement (Statement of Cash-Flow)

Learning Activity 2.3

Visit your neighboring company and ask the accountant to show you theschool financial Statements.

a) Check on them differently and find which statement that showsthe movement of cash.

b) You will find different parts and elements in the statement of cash

flow. How do we call the cash that are coming in business, cash thatare going out the business and their difference?

Learning Activity 2.3

In senior four, the direct method of cash flow statement was discussed on, thatis why only indirect method will be seen.

Rules of preparing statement of cash flow in indirect method

Although the Financial Accounting Standard Board favors the direct method for

preparing the statement of cash flows, most companies do not use the direct

method opting instead for the indirect method because it is easier to prepare

and provides less detailed information to competitors.Under the indirect method, the cash flow statement begins with net income

on an accrual basis with assumption that net income equals cash and

subsequently adds and subtracts non-cash items to reconcile to actual cash

flows from operations. An increase in an asset account is subtracted for net

income, and an increase in a liability account is added back to net income.

The following rules can be followed to calculate Cash Flows from Operating

Activities when given only a two-year comparative balance sheet and theNet Income figure.

– Decrease in non-cash current assets are added to net income

– Increase in non-cash current asset are subtracted from net income

– Increase in current liabilities are added to net income

– Decrease in current liabilities are subtracted from net income

– Expenses with no cash outflows are added back to net income

(depreciation and/or amortization expense are the only operating

items that have no effect on cash flows in the period)

– Revenues with no cash inflows are subtracted from net income

– Non-operating losses are added back to net income– Non-operating gains are subtracted from net income

It is important to understand why certain items are added and otherssubtracted. Note the following points:

a) Depreciation is not a cash expense, but is deducted in arriving at

profit. It makes sense, therefore, to eliminate it by adding it back.

b) By the same logic, a loss on disposal of a non-current asset (arising

through under provision of depreciation) needs to be added back

and a profit deducted.

c) An increase in inventories means less cash you have spent cash on

buying inventory.

d) An increase in receivables means the company’s debtors have not

paid as much and therefore there is less cash.

e) If we payoff payables, causing the figure to increase, again we haveless cash.

Rules (Financing Activities)

Finding the Cash Flows from Financing Activities is much more intuitive and

needs little explanation. Generally, the things to account for are financingactivities:

• Include as outflows, reductions of long term note payable (as would

represent the cash repayment of debt on the balance sheet)

• Or as inflows, the issuance of new notes payable

• Include as outflows, all dividends paid by the entity to outside parties

• Or as inflows, dividend payments received from outside parties

• Include as outflows, the purchase of notes stocks or bonds

• Or as inflows, the receipt of payments on such financing vehicles.

• In the case of more advanced accounting situations, such as when

dealing with subsidiaries, the accountant must:

• Exclude intra-company dividend payments.• Exclude intra-company bond interest

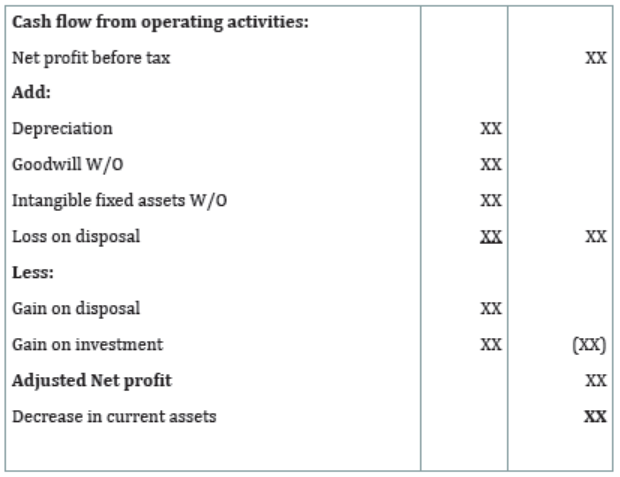

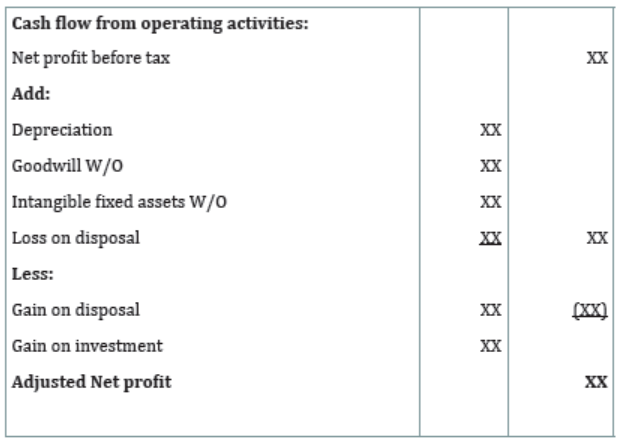

Preparation of Statement of Financial Statement using indirect methodFormat of cashflow statement (indirect method)

N.B Further details on components of cash flow (cash flow from operating

activities, cash flow from investing activities and financing activities) arediscussed in Senior 4 unit 10.

Illustration 1

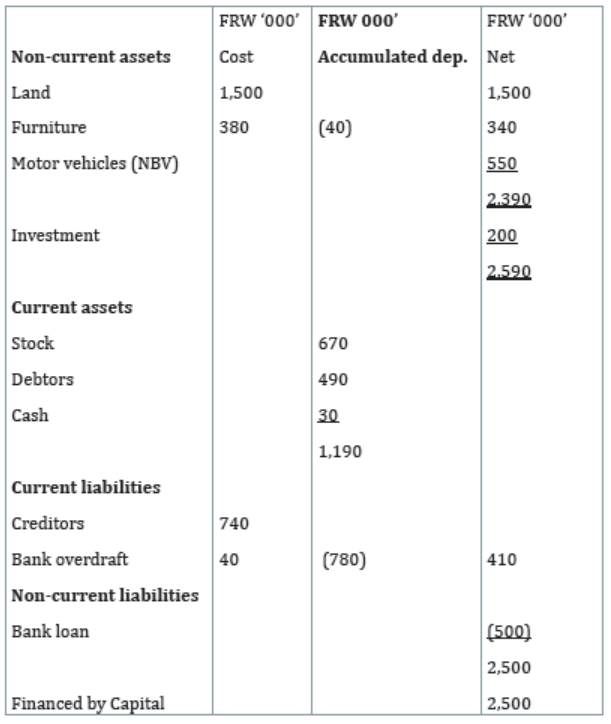

The following are balance sheets of Neema private ltd for the years ended 31stDec 2003 and 2004 respectively

Balance sheet/ statement of financial position as at 31st Dec 2003

Neema private ltd

Balance sheet/ Statement of Financial Position as at 31st Dec 2004

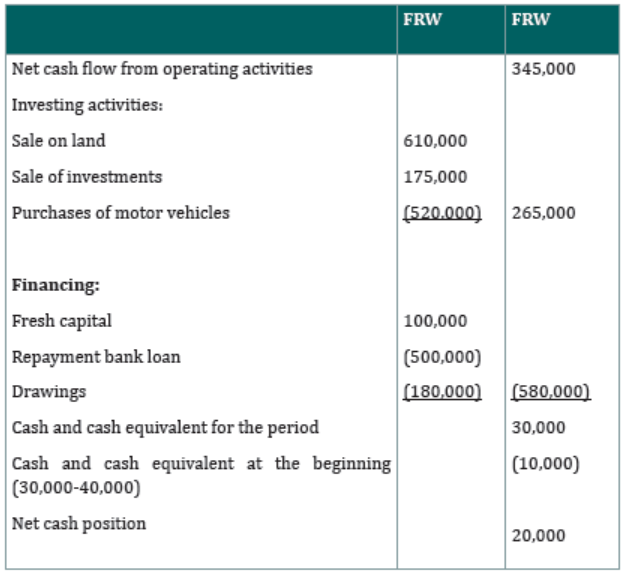

i. A piece of land was sold in July 2004 for FRW 610,000 and investment in

October 2004 for FRW 175,000

ii. Some motor vehicle was bought in 2004 for FRW 520,000. No furniturewas bought or sold during the year

iii. Profit before tax for the year ended on31 December 2004 was FRW

200,000

Required: Statement of Cash Flow to explain the change in cash

Solution

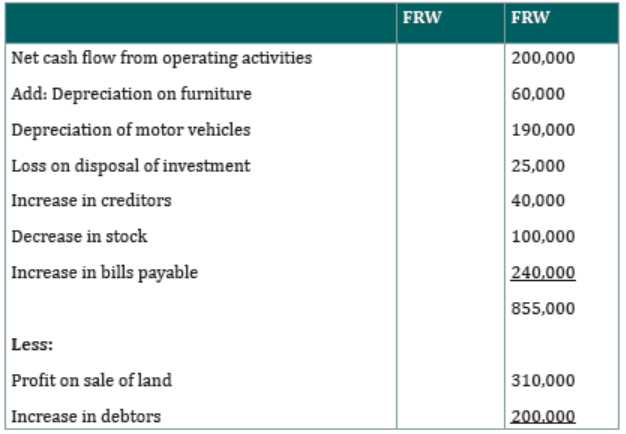

Adjustments:

a) Gain on disposal (land) = 610,000-(1,500,000-1,200,000) = 610,000-300,000=310,000

b) Loss on disposal (investment) = 200,000 - 175,000 = 25,000

c) Depreciation on furniture= 100,000-40,000=60,000

d) Depreciation on Motor Vehicle= 520,000-(880,000-550,000) =190,000

Neema private ltd

Statement cash flow (indirect method)

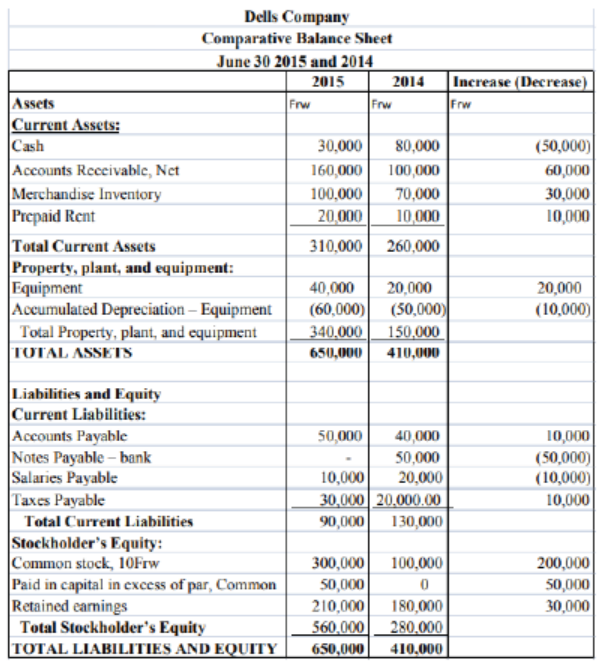

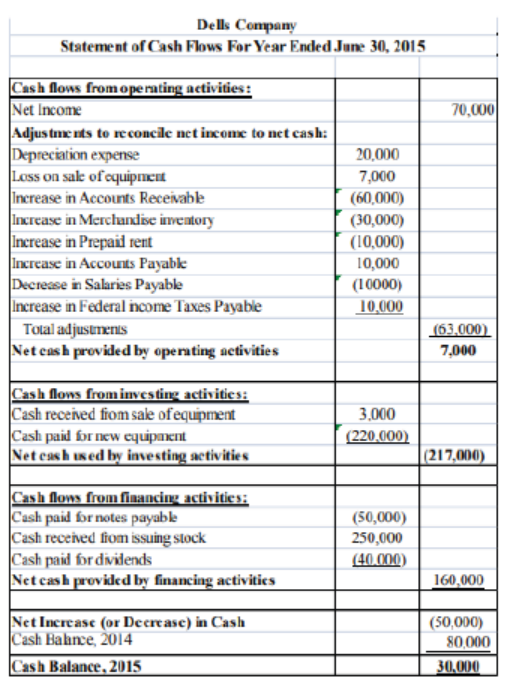

Dells Company started its business on 1st July 2014 and it is operating its

business activities nearby your school. At the 30 June, its accountant presentedthe business’s Balance Sheet for two years (2014 and 2015) which follows:

Required: Prepare Dells Statement of Cash Flow for the year ended 30 June

2015 using indirect method.

Answer

Application activity 2.3

1. Outline the uses of statement of cash flow to the visited business.

2. Maria is a sole trader who prepares his accounts annually to 30 April. Hissummarized balance sheets for the last two years are shown:

Balance sheets as at 30 April

You are required to prepare the statement of Cash Flow as at 30 April 2015

Skills Lab

After visiting any neighboring sole proprietorship business and checkingits financial statements,

1. Outline different Financial Statements prepared by a sole trader

2. Discuss about the use of financial statements to the visited business

3. As an accountant, advice the sole traders on the impact of negligencein the preparation of Financial Statements.

End unit assessment 2

After visiting any neighboring sole proprietorship business and checkingits financial statements,

1. Outline different Financial Statements prepared by a sole trader

2. Discuss about the use of financial statements to the visited business

3. As an accountant, advice the sole traders on the impact of negligencein the preparation of Financial Statements.

End unit assessment 2

1. Explain three reasons why the amount of cash flow of a business

entity might differ from the profit generated by the business entity

during the same period.

2. The book keeper of Mella Enterprise Ltd prepared the following trialbalance for the financial year ended31st march 2020