General

- Entrepreneurship S3 SB File Uploaded 25/01/22, 15:48

- S3: Entrepreneurship TG File Uploaded 11/08/22, 22:14

Unit 6: Customs Procedures

TOPIC AREA: BUSINESS ACTIVITY

SUB-TOPIC AREA: TAXATION CUSTOMS

Key unit competence:

To be able to examine the role of Rwandan customs procedures.

Knowledge to be acquired

Meaning of customs and customs declaration.

Types of customs declaration.

Role of customs procedures.

Stakeholders involved in customs declaration.

Types of customs declaration.

Application to daily life

Analyse the types of customs declaration.

Analyse various documents used in customs declaration.

Assess the role of various stakeholders involved in customs procedures.

Appreciate the role of customs procedures in the facilitation of trade.

Develop positive attitude towards customs declaration.

Introductory Activity

Some of the products we use in everyday life are not produced within Rwanda. Some are imported from other countries. Not all goods produced in Rwanda are consumed within Rwanda. Some are exported to other countries.

Questions

1. Describe the process involved in the:

(a) buying of goods from countries outside Rwanda.

(b) selling of goods to countries outside Rwanda.

2. How do we call the process of:

(a) buying of goods from countries outside Rwanda?

(b) selling of goods to countries outside Rwanda?

3. Mention the agents involved the process.

4. Mention the documents used in the process.

5 . Why do customs exist in Rwanda

6.1: Meaning of Customs and Customs Declaration

ACTIVITY 6.1

Using your knowledge of Senior one and two about sources of finance and taxes in Rwanda, answer the followingqueS11on.s:

1. What is taxation, tax, tax avoidance and tax evasion?

2. How are taxes collected in Rwanda?

3. Why is it important for individuals and businesses to pay taxes?

4. Which government agencies are in charge of collecting taxes?

ACTIVITY 6.2 Research activity

Visit your library or use the internet and research on the following:

1. Customs

2. Customs declaration

3. Types of customs declaration

(a) Export and import

(b) Temporary importation

(c) Warehousing

(d) Transit

From activity 6.1 and 6.2, customs is a government agency entrusted with enforcement of laws and regulation to collect and protect import-revenues and to regulate and document the flow of goods in and out f the country. (BusinessDictionary.com)

Customs declaration is an official document that lists and gives details of goods that are being imported or exported. Imported goods must be accompanied by a customs declaration form. Ifs a form declaring the nature and value of goods, and so on, for customs purposes. (Collins English Dictionary)

6.2: Types of Customs Declaration/Customs Entry

Customs declaration is a form that is required by most countries when a citizen or a visitor or goods are entering that nation’s borders, called import.

The purpose of the import form is to declare what goods are being brought into the nation,as some countries may have import quotas (limits), customs excise taxes, or bans from entry on some goods or quantities of goods.The form is also used to calculate any applicable tariffs or duties.

The entry/duty form states the customs classification number,country of origin,description, quantity, CIF value of the goods, and the estimated amount of duty to be paid.

If upon examination by customs officer the entry is verified as a correct or ‘perfect entry, the goods in question are released (on payment of duty and other charges, if any) to the importer, or are allowed to be exported.

Main types of customs entry are:

- Consumption entry: for goods to be offered for consumption in the importing country.

- Formal entry: that is required to be covered by an entry bond because its aggregate value exceeds a certain amount.

- Informal entry: That is not required to be covered under an entry bond because its value is less than a certain amount.

- In-transit entry: for the movement of goods from the port of unloading to the port of destination, under a customs bond.

- Mail entry: For goods entering through post office or courier service and below a certain value.

- Person baggage entry: For goods imported as personal baggage.

- Transportation and exportation entry: For goods passing through a country en-route to another country.

- Warehouse entry: For the goods stored in a bonded warehouse.

6.3: Role of Customs Procedures

ACTIVITY 6.3 Research activityUse the library or internet, or resources from RRA and make research on the following:1. Customs procedures2. Customs declaration3. Declaration documents4. Stakeholders in customs declarations5. Role of customs declarations The role of customs procedures include:

The role of customs procedures include:- To ensure observance of laws: Laws on taxes, quality standards of goods and services imported or exported are observed by customs authorities.

- Trade compliance and facilitation: Customs procedures also facilitate smooth running of trade activities through regulating prices and quantity of exports and imports.

- To protect economic interests: Customs procedures also protect economic interests of an economy through regulating what should be imported and exported depending on the prevailing conditions.

- To protect the rights and interests of citizens and businesses: This can be done through discouraging imports so as to protect local businesses from foreign competition and encourage exports.

- To ensure observance of revenue collection: Taxes are collected on imports and exports from borders of a country by customs authorities.

6.4: Necessary Documents for the Declaration of Goods at Customs

ACTIVITY 6.4 Research activityIn customs declaration, there are various documents used.1. Identify some of the documents used.2. Suggest the use of each document identified in 1above. Present your findings to the teacher for evaluation.From activity 6.5, there are several documents used in customs declaration. These include: transaction invoice, transport document, import licence, packing list, certificate of origin, certificate of analysis, goods arrival notice, bill of landing, certificate of fumigation, goods exit note, goods invoice, importation permit, payment receipt, phytosanitary certificate, transport invoice and warehouse handling fees invoice.These documents are further explained below with their uses.Transport invoice

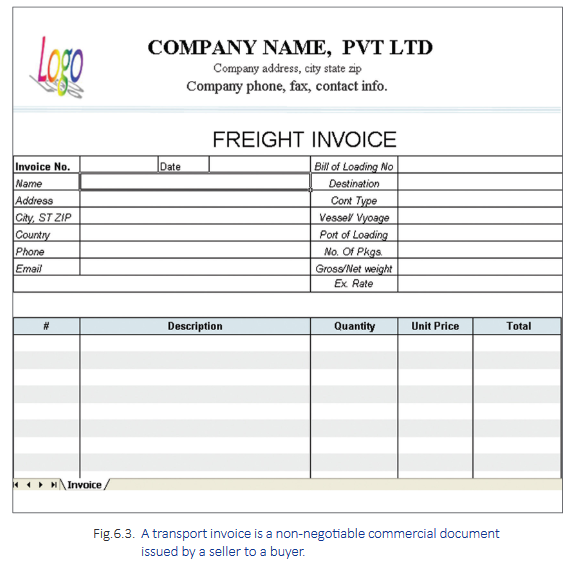

A transport invoice is a non-negotiable commercial document issued by a seller to a buyer. The transport invoice identifies the following:- both the trading parties,

- lists, describes, and quantifies the items sold,

- shows the date of shipment and mode of transport,

- prices and discounts (if any),

- and delivery and payment terms.

Transport document

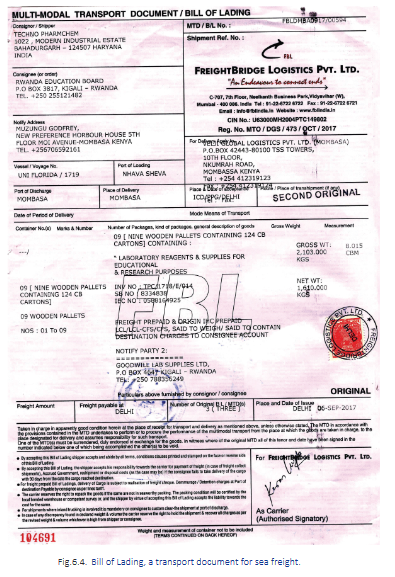

A transport document shows information about cargo that is being transported. Transport documents lie at the heart of international trade transactions.These documents are issued by the shipping line, airline, international trucking company, railroad, freight forwarder or logistics company.To the shipping company and freight forwarder, transport documents provide an accounting record of the transaction, instructions on where and how to ship the goods and a statement giving instructions for handling the shipment.There is a type of transport document for each mode of transport: (CMR for road transport, Bill of Lading for shipping, etc.). Goods carried in multimodal transport units (mainly containers) use a document called FIATA multimodal Bill of Lading (FBL).Below are the main transport documents explained in detail what they are used for?, who prepares them? and to whom they are addressed?a. CMR (Contrat de Transport International de Merchandises par Route): The CMR transport document is an international consignment note used by drivers, operators and forwarders alike that govern the responsibilities and liabilities of the parties to a contract for the carriage of goods by road internationally.The carrier usually completes the form, but the sender (exporter) is responsible for the accuracy of the information and must sign the form when the goods are collected. The consignee will also sign the form on delivery, which is essential for the carrier to be able to confirm the delivery of the goods and to justify the payment for its services.The CMR transport document is not a document of title and is, therefore, non negotiable. This document is prepared by the exporter and the freight forwarder and is addressed to the importer and the carrier.b. Air waybill: This is a transport document used for air freight. An Air waybill (AWB) is a non-negotiable transport document covering transport of cargo from airport to airport. The Air waybill must name a consignee (who can be the buyer), and it should not be required to be issued “to order” and/or “to be endorsed” as it is not a title of property of the merchandise. Since it is not negotiable, and it does not evidence title to the goods, in order to maintain some control of goods not paid for by cash in advance, sellers often consign air shipments to their sales agents or freight forwarders’ agents in the buyer’s country. The Air waybill is not a negotiable document. It indicates only acceptance of goods for carriage. This document is prepared by the lATA Transport Agent or the airline itself and is addressed to the exporter, the airline and the importer.c. Bill of Lading: This is a transport document for sea freight. A Bill of Lading (B/L) is issuedby the agent of a carrier to a shipper, signed by the captain, agent, or owner of a vessel. A bill of landing shows the following:- written evidence regarding receipt of the goods (cargo),

- the conditions on which transportation is made (contract of carriage),

- and the engagement to deliver goods at the prescribed port of destination to the lawful holder of the bill of lading.

A Bill of Lading is both a receipt for merchandise and a contract to deliver it as freight. There are a number of different types of bills of lading and a number of regulations that relate to them as a group of transport documents.Since this is a negotiable instrument, the Bill of Lading may be endorsed and transferred to a third party while the goods are in transit.

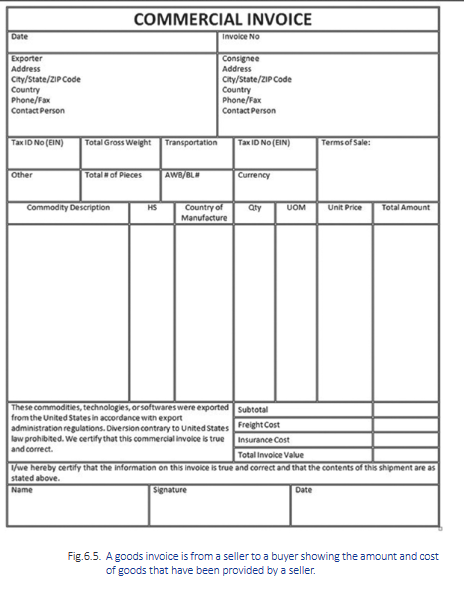

Goods invoice

A goods invoice is a document sent by a seller to a buyer specifying the amount and cost of goods that have been provided by a seller.A goods invoice indicates what must be paid by the buyer according to the payment terms of the seller. Payment terms usually specify the period of time that a buyer has to send payment to the seller for the goods and/or services that they have purchased.An invoice provides a detailed account of the goods and a set of other information that can vary a bit depending on the requirements in the country the invoice is issued and the type of goods being sold. The goods invoice has the description, quantity, selling price, freight, insurance, and packing cost. The delivery terms and payment are also listed.Usually, an invoice will include the following points of information in order to be considered a legal invoice:- The word ‘Invoice’

- A unique reference number: the invoice number.

- The date the product was sent or delivered (or the date the service was rendered).

- The date the invoice was sent.

- The contact information and name of the seller.

- The name and contact details of the buyer.

- The terms of payment (that explain the means of payment, when the sum should be received, any cash discount details for early payment, late payment fees, and so on).

- A line detailing the product/service.

- The cost per unit of the product (if this applies).

- The total amount that is owed.

Uses of invoices

The following are some of the uses of invoices:- Invoices are used to request payment from buyers,

- Keep track of sales,

- Help control inventory,

- And facilitate delivery of goods and services.

Invoices are also used to track expected future revenues and to manage customer relationships by offering favourable payment options, such as extended time periods for payment or discounts for early payment or cash payment.

Packing list

The packing list is a more detailed version of the commercial invoice but without price information. It shows the quantity of each good in the shipment. A packing list must include the following:

A packing list must include the following:- invoice number,

- quantity and description of the goods,

- the weight of the goods,

- number of packages,

- and shipping marks and numbers.

A copy of the packing list is often attached to the shipment itself and another copy is sent directly to the consignee to assist in checking the shipment when received.Although not required for all transactions, it is required by some countries and some buyers. A packing list is prepared by the exporter and addressed to the importer, the carrier and the import customs clearance.Certificate of fumigation

The certificate of fumigation also referred to as a ‘pest control certificate’ is the proof that wooden packing materials used in international sea freight shipping such as wooden pallets and crates have been fumigated or sterilised prior to international shipmentThe certificate of fumigation usually contains details such as purpose of treatment, the articles in question, temperature range used, chemicals and concentration used, and so on.The certificate of fumigation as an international sea freight shipping document is NOT a mandatory international shipping export document. However, it assists in quick clearance of an international sea-freight shipment upon the arrival to the destination.The certificate of fumigation should be completed by a certified vendor prior to international shipment and be submitted to an international sea freight carriers shipping facility in the country of origin of the international shipment.If not completed and fully documented at the country of origin, then the fumigation may be done at the destination upon arrival of international sea freight shipment to the country of destination; OR for international shipments with transshipments at a time of transshipment, such as at a time when cargo will be reloaded from one container/vessel to another in order to be shipped to the final destination.If a fumigation certificate in international sea freight shipping is required but not presented or incomplete, then additional costs related to fumigation of the international sea freight shipment may occur upon arrival of the international shipment to the destination.Non-compliance will result in wooden packing materials and wooden pallets being destroyed by the destination country port authorities at consignee’s cost and may result in delayed customs clearance. Shippers/consignees will bear the cost of the fumigation and/or delayed customs clearance due to this non-compliance on the international shipping procedures related to international shipping of sea freight containing wooden packing materials. A fumigation certificate can be obtained by international shipper from a local fumigation company.Certificate of Origin

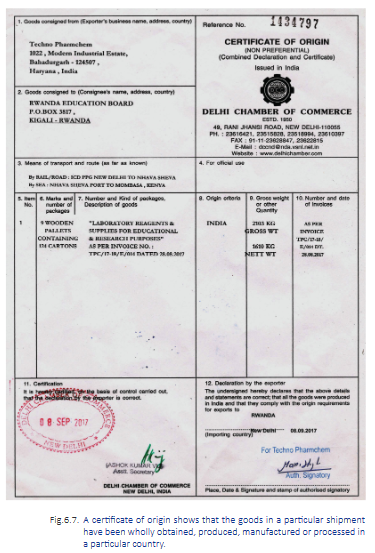

A “Certificate of Origin” is also called a “Form A”. It certifies a shipment’s country of origin. The Certificate of origin is commonly issued by a trade promotion office, or a chamber of commerce in the exporting country. This document is filled in by the exporter and certified by a recognised issuing body, confirming that the goods in a particular export shipment have been produced, manufactured or processed in a particular country.A certificate of origin is often required by customs authorities of a country as part of the entry process. Such certificates are usually through an official organisation in the country of origin such as the local chamber of commerce or a consular office.The goods description must coincide with that provided in the commercial invoice and in the packing list (number, goods description, name of the consignor and of the consignee, trademarks, etc). If the certificate of origin is not shown, the import customs may, if it deems it necessary, accept the dispatching of goods. In this case, the corresponding tariff would be applied to third countries (non preferential origin), without any tariff discount.

A “Certificate of Origin” is also called a “Form A”. It certifies a shipment’s country of origin. The Certificate of origin is commonly issued by a trade promotion office, or a chamber of commerce in the exporting country. This document is filled in by the exporter and certified by a recognised issuing body, confirming that the goods in a particular export shipment have been produced, manufactured or processed in a particular country.A certificate of origin is often required by customs authorities of a country as part of the entry process. Such certificates are usually through an official organisation in the country of origin such as the local chamber of commerce or a consular office.The goods description must coincide with that provided in the commercial invoice and in the packing list (number, goods description, name of the consignor and of the consignee, trademarks, etc). If the certificate of origin is not shown, the import customs may, if it deems it necessary, accept the dispatching of goods. In this case, the corresponding tariff would be applied to third countries (non preferential origin), without any tariff discount.Phytosanitary certificate

Phytosanitary certificate is a certificate stating that a specific crop was inspected a predetermined number of times and a specified disease was not found.An inspection certificate issued by a competent governmental authority to show that a particular shipment has been treated to be free from harmful pests and plant diseases.The phytosanitary certificate must be issued before the customs clearance for export and import. It is granted for a period of sixty days covering the usual deadlines for shipping and international freight.Phytosanitary certificates are issued for the following commodities:- plants, bulbs and tubers, or seeds for propagation, fruits and vegetables, cut flowers and branches, grain, and growing medium.

- plant products that have been processed where such products, by their nature or that of their processing, have a potential for introducing regulated pests (e.g. wood, cotton).

- other regulated articles where phytosanitary measures are technically justified (e.g. empty containers, vehicles, and organisms).

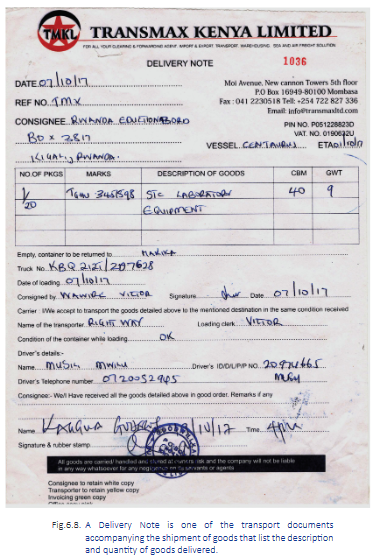

Importing countries should not require phytosanitary certificates for plant products that have been processed in such a way that they have no potential for introducing regulated pests, or for other articles that do not require phytosanitary measures.Delivery Note

A delivery note accompanys the shipment of goods listing the description and quantity of goods delivered. A copy of the delivery note, signed by the buyer or consignee is returned to the seller or consignor as proof of delivery.Delivery notes have a dual function for the exporter:

A delivery note accompanys the shipment of goods listing the description and quantity of goods delivered. A copy of the delivery note, signed by the buyer or consignee is returned to the seller or consignor as proof of delivery.Delivery notes have a dual function for the exporter:- Justify the removal of the products from its store and proof credit delivery to the importer and therefore, it is important that the importer signs the copy provided by the carrier. For the importer, delivery notes serve to verify that the goods received match those listed on the purchase order or contract.

- a. For the carrier, a delivery note is used as a proof of delivery of the goods.

Payment receipt

A payment receipt is a simple document that shows that payment was received in exchange for goods or services. For example, a receipt can be something as simple as what an individual gets after making a purchase at the grocery store.Businesses also use payment receipts for product delivery or independent contractors, among others, to ensure that both parties have proof that the goods or services were rendered.Some businesses combine a receipt with an invoice, and will just make a notation on the bottom of the existing document that payment was made; this can make filing slightly easier.The purpose of this receipt in any situation is to verify that the correct amount was charged for the correct products or services.A receipt shows the following:- the name and address of the store,

- the date of purchase,

- and a description of the item.

- It will also include the price paid and any taxes that were added in,

- as well as the method of payment, such as cash, a check or credit card.

Anyone being given a receipt after a purchase should quickly check to make sure that the amounts shown are correct; this is especially true if a credit card was used for the purchase, where a mistaken charge could be a big problem.Receipts are used by buyers or customers to prove they paid for an item, especially in return situations in which goods are faulty or defective.

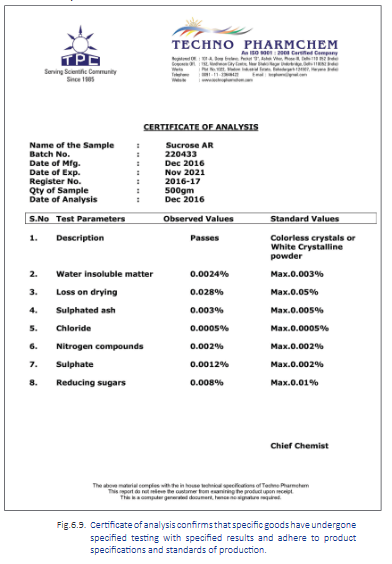

Certificate of Analysis

Certificate of analysis is a document issued by a quality assurance entity confirming that specific goods have undergone testing with specified results and adhere to product specifications and standards of production of certain products such as food products and drugs.In international trade, a certificate of analysis is usually the result of an agreement between the seller and the buyer, or a requirement of one of their governments. The certificate of analysis is mostly used for food products, wines and spirits, chemicals and pharmaceuticals.Sometimes, as in the case of wine exports, there are countries that require it at the import customs. This certificate can be issued by a certification authority.

Certificate of analysis is a document issued by a quality assurance entity confirming that specific goods have undergone testing with specified results and adhere to product specifications and standards of production of certain products such as food products and drugs.In international trade, a certificate of analysis is usually the result of an agreement between the seller and the buyer, or a requirement of one of their governments. The certificate of analysis is mostly used for food products, wines and spirits, chemicals and pharmaceuticals.Sometimes, as in the case of wine exports, there are countries that require it at the import customs. This certificate can be issued by a certification authority.Goods arrival notice

A goods arrival notice is a document sent by a carrier or agent to the consignee to inform about the arrival of the shipment and number of packages, description of goods, their weight, and collection charges (if any). It is also called an arrival notice.Warehouse handling invoice Warehouse handling invoice is a written document given bya warehouseman for items received for storage in his or her warehouse, which serves as evidence of title to the stored goods.The general rule is that warehouse receipts need not be in any particular form. They must, however, contain the following information:- the location of the warehouse and the place where the goods are stored;

- the date when the invoice was issued;

- the consecutive number of the invoices;

- terms indicating whether the goods are to be delivered to the bearer of the receipt, to a particular individual, or to a particular individual on his or her order;

- the storage rate or handling charges;

- statement describing the goods or the manner in which they are packed;

- the signature of the warehouseman or his/her agent;

- the amount of advance payment made, if any;

- and any other terms that do not impair the warehouseman’s duty.

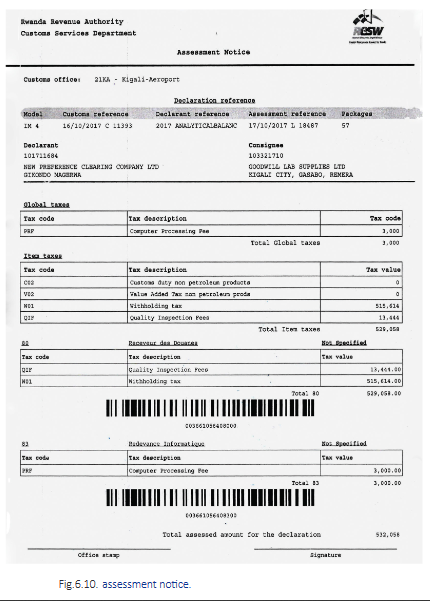

In situations where a warehouse handling invoice does not contain these provisions, the warehouseman can be held liable in damages to anyone who sustains financial injury because of the omission.Assessment notice

This is a document issued by a taxing authority specifying the assessed value of a property.

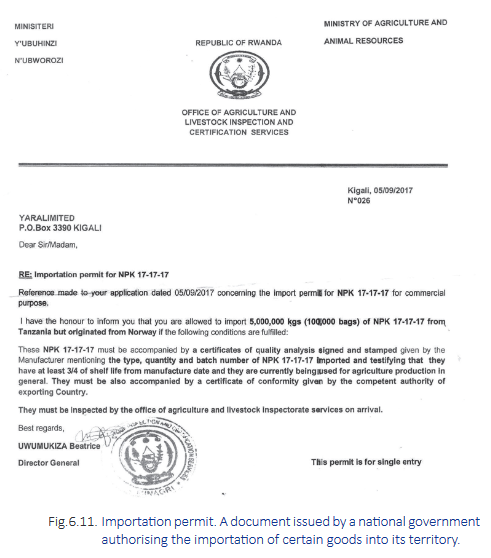

Importation Permit or License

An import license is a document issued by a national government authorising the importation of certain goods into its territory. Import licenses are considered to be non-tariff barriers.to trade when used as a way to discriminate against another country’s goods in order to protect a domestic industry from foreign competition. Each license specifies the volume of imports allowed, and the total volume allowed should not exceed the quota.Government may put certain restrictions on what is imported as well as the amount of imported goods and services. For example, if a business wishes to import agricultural products such as vegetables, then the government may be concerned about the impact of such importations of the local market and thus impose a restriction.Import licenses are put in place because of the following reasons:- To restrict outflow of foreign currency and improve a country’s balance of payments position;

- To control entry of dangerous items such as explosives, firearms, and certain substances;

- To protect the domestic industry from foreign competition.

6.5: The Process of Clearing through Customs

ACTIVITY 6.5 Research activity

Using the library, internet or resources from RRA, make research on the process of clearing through customs.

The different steps of clearing through customs are:

1.Obtain notice of arrival of the goods (avis d’arrivee)

Requirements

- Customs declaration number.

- Physical presence of the clearing agent.

2. Submit goods arrival notice for verification from Rwanda Standards Board.

Requirements for all

- Goods arrival notice (avis d,arrivee) (original).

- Goods invoice (original).

- Packing list (original).Requirements for foods and cosmetics

- Certificate of analysis (original) obtained from where goods originated.

Requirements for agricultural products such as seeds and fertilisers

- Certificate of phytosanitary (original) obtained from where goods originated.

- Certificate of analysis (original) obtained from where goods originated.

- Importation permit from Rwanda Agriculture Board (RAB) (original) obtained from RADA.

Requirements for used clothes

- Certificate of fumigation (original) obtained from where goods originated.

Requirements for medical products

- License of importation (original) obtained from the ministry of health (Rwanda).

Requirements for chemicals and lubricants#Certificate of analysis (original).Requirements for livestock#Livestock certificate (original).#Certificate of analysis (original).3. Obtain manifestRequirements- Notice of arrival (avis d’arrivee) (original).

- Tl (original).

4. Submit import document to the clearing agent for tax calculationRequirements- Goods invoice (original).

- Copy of goods invoice with RRA stamp. RRA stamp is obtained at the point of entry in the country.

- Transport invoice (original).

- Bill of ladding (original+ simple) copy should have RRA stamp obtained at the point of entry in Rwanda or Airway bill (original).

- Packing list (original + Simple) copy should have RRA stamp obtained at the point of entry in Rwanda.

- Tl obtained from RRA at the point of entry in Rwanda.

- Goods arrival notice with RBS stamp (original + simple copy). Costs

- Cost detail

- 50,000 Frw for clearing agent handling fees

- 9,000 Frw for VAT

- Payment methods: cash, check

5. Pay import taxRequirements- Assessment notice

- Costs

- Payment methods: cash or cheque.

- Import tax include; import duty, Value Added Tax (VAT), withholding tax and consumption tax.

- VAT and withholding taxes are fixed at 18% and 5% respectively.

- Customs duty vary according to the origin of the goods. Goods from the East African community are exempted from this tax and some other COMESA countries pay a reduced price.

- The clearing agencies have a system where by goods are assigned different codes and once this code is entered in the system and the country of origin of the goods, taxes are calculated automatically.

- Large importers who had been previously paying taxes well may be exempted from withholding taxes.

6. Obtain an invoice for warehouse handling feesRequirements- Notice of arrival (avis d’arrivee) (original).

- Time frameWaiting time in queue: Max. 10mn.Attention at counter: Max. 5mn.

7. Pay warehouse fees for goods handlingRequirements- Warehouse handling fees invoice (original).

- Costs: Warehouse handling fees are set by MAGERWA management. The fees depend on the quantity of the goods and the time spent in the warehouse. Within 7 days, each kilogram is charged l0Frw per day. From 7 days and above, an extra 1Frw is charged per kilogram/day. VAT (18%) and parking fees is added on the total cost.

8. Obtain goods exit noteRequirements- Warehouse handling fees invoice (simple copy).

- Tax declaration form (original).

- Payment receipt (MAGERWA) (original).

6.6: Stakeholders Involved in Customs

ACTIVITY 6.6 Research activityUse the library or Rwanda Revenue Authority website to make research on all the stakeholders (agencies/people) involved in customs.Stakeholders involved in customs and their roles are explained below:a. Rwanda Revenue Authority (RRA)Rwanda Revenue Authority is concerned with the assessment and collecting taxes on imported and exported commodities at ca1.11tom.s.Rwanda Revenue Authority plays a very important role in raising government revenue through imposing and collecting taxes from both imported and exported commodities. Rwanda Revenue Authority also regulates the economic activities in favour of economic interests of an economy through its activities of imposing and collection of taxes.For this case, Rwanda Revenue Authority is a body which is responsible for assessing and collecting taxes from imports and exports in Rwanda. b. Bureau of StandardsBureau of Standards is concerned with the quality of commodities being imported or exported. The standards of a commodity are characteristics of a product and different prescription concerning the same products such as size, name, labelling colour and so on.To be authorised to sell on the Rwanda territory, the manufacturer has to bring proof that his product is standard from Rwanda Standards Board.Therefore, Rwanda Standards Board plays the following roles:

b. Bureau of StandardsBureau of Standards is concerned with the quality of commodities being imported or exported. The standards of a commodity are characteristics of a product and different prescription concerning the same products such as size, name, labelling colour and so on.To be authorised to sell on the Rwanda territory, the manufacturer has to bring proof that his product is standard from Rwanda Standards Board.Therefore, Rwanda Standards Board plays the following roles:- Provides reference documents containing solutions to technical and commercial problems concerning products, goods and services which rise often in the relationship between economic, scientific, technical and social partners.

- Improves the quality of products. This promotes competition which leads to the consumption of quality products at a relatively lower price.

In Rwanda, it is the Rwanda Standards Board (RSB) that deals with control of quality, state and condition of commodities which are imported or exported. To achieve this, Rwanda Standards Board has been well equipped with modem laboratories.c. Clearing and forwarding agencyThe clearing and forwarding agency is a body which is concerned with controlling and imposing taxes on commodities that cross borders of a country. Clearing and forwarding agencies play a very important role in the statistical analysis of the nature, the origin and the value of products that are received from foreign countries.d. Warehousing agency and security bodiesThe warehousing agency is concerned with imported commodities.Imported commodities are stored in warehouses on a temporary basis without being subjected to import duties and taxes. Warehousing is concerned with storage facilities and protection of commodities that are waiting to be consumed or used.Therefore, warehousing agency plays the following roles:- Protect imported commodities against theft and bad climate conditions.

- Prepare in advance against price fluctuations, for example, if after a particular season, certain products are in abundance, one must keep them to wait a stronger demand at a good price.

- Goods can be stored and repacked again for transporting to the importers premises.

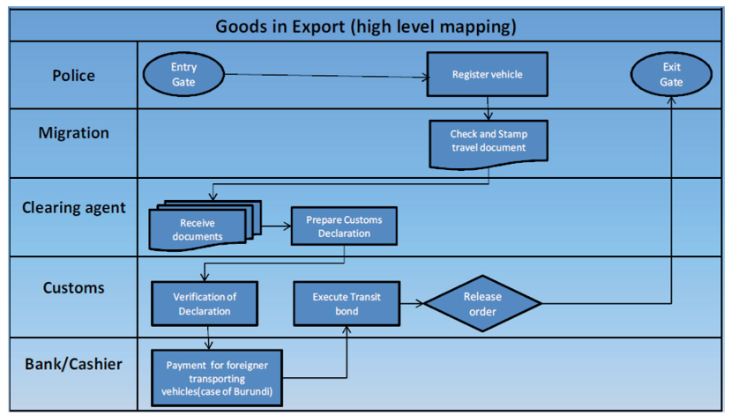

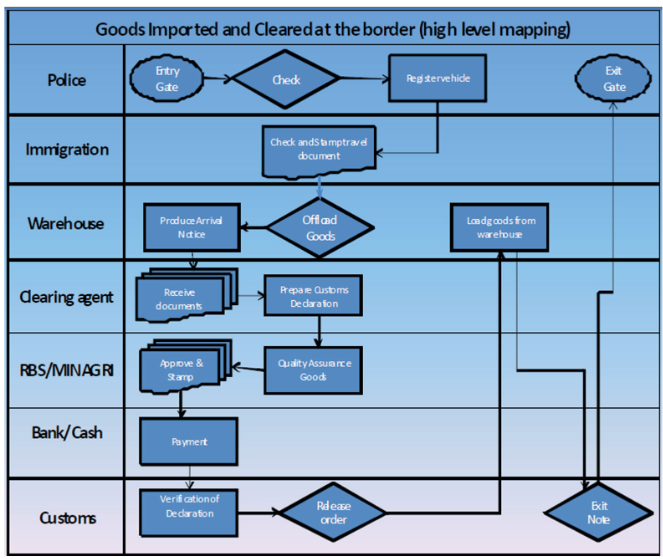

6.7: Process of Handling Goods with the Stakeholders involved

The process of handling goods with the stakeholder is shown below.

Unit Summary

Customs: Government agency entrusted with enforcement of laws and regulations to collect and protect import-revenues,and to regulate and document the flow of goods in and out of the country.Customs declaration: An official document that lists and gives details of goods that are being imported or exported: Imported goods must be accompanied by a customs declaration form.Types of Customs declaration/Customs entry- Consumption entry: for goods to be offered for sale (consumption) in the importing country.

- Formal entry: that is required to be covered by an entry bond because its aggregate value exceeds a certain amount.

- Informal entry: that is not required to be covered under an entry bond because its value is less than a certain amount.

- In-transit entry: for the movement of goods from the port of unloading to the port of destination, under a customs bond.

- Mail entry: for goods entering through post office or courier service and below a certain value.

- Person baggage entry: for goods brought imported as personal baggage.

- Transportation and exportation entry: for goods passing through a country en route to another country.

- Warehouse entry: for the goods stored in a bonded warehouse.

Roles of customs procedures- To ensure observance of laws.

- Trade compliance and facilitation.

- To protect economic interests.

- To protect the rights and interest of citizens and businesses.

The process of clearing through customs- Obtain notice of arrival of the goods (avis d’arrivee).

- Submit goods arrival notice for verification by Rwanda Standards Board.

- Obtain manifest.

- Submit import document to the clearing agent for tax calculation.

- Pay import tax.

- Obtain an invoice for warehouse handling fees.

- Pay warehouse fees for goods handling.

- Obtain goods exit note.

Stakeholder involved in customs declaration- Rwanda Revenue Authority (RRA).

- Rwanda Standards Board (RSB).

- Clearing and forwarding agencies.

- Warehousing agencies and security bodies.

Unit 4 Assessment

1. Identify and explain the types of customs declarations in various customs points in Rwanda.2. With examples, explain the role of customs procedures towards the economic development of Rwanda.