General

- ICT S2 SB File Uploaded 24/01/22, 15:32

Unit 2:ICT in Financial Transactions

Key Unit Competency: By the end of this unit, you should be able to:

1. Analyze and criticise the role and impact of computing tools financial transactions.

2. Use computing tools in financial transactions.

Introduction

To transact means to conduct or carry out business. Financial transaction refers to an agreement or communication between a buyer and a seller on how to carry out business. They agree on the terms of exchanging goods or services for payment.

ICT as a tool in financial transactions enables the smooth and efficient running of the agreements and payments made between the buyer and the seller.

Practice Activity 2.1: Role of computers in society

Research on the role of computer use in society. Compile a report. Make a presentation in class.

2.1 The Role of Computers in Financial Transactions

Computers are important tools in all financial transactions. Computers are used to automate business operations, for record keeping, and for the stock exchange.

2.1.1 Automated Operations

Automation is the process of using computers and information technology to produce products and offer services with minimal human involvement. Some examples of automated operations include automated accounting, automated mailing, and Electronic Data Interchange (EDI).

1. Automated Accounting

• Automated accounting refers to the process of maintaining up-to-date accounting records using accounting software.

• Accounting software allows easy cross-posting of accounting records.

• Most of the readily available automated accounting systems can be customised to suit the needs of the company that purchases the software. This makes it possible to create customised reports.

• Many organisations in Rwanda use accounting software. With this type of software, an organisation is able to administer and manage the income, expenses, and assets, as well as maximize the profits and ensure sustainability.

• The Unstructured Supplementary Service Data (USSD). USSD is the short for Unstructured Supplementary Service Data. This is a technology that is used for communication.

® The USSD is a system for mobile telephony that enables a mobile user to send text between a mobile phone and an application program in the computer network of the service provider.

® Examples of USSD applications may include prepaid call back services, mobile money services, and mobile chatting.

® USSD services allow a two-way exchange of data

® When the mobile user sends a message to the phone company network, it is received by a computer that gives USSD services. The computer gives a response that is sent back to the phone. The message is displayed on the phone screen. The service provider determines the format of the messages that are sent over USSD to their customers.

Using the USSD

(i) The user sends a request to the network via USSD by dialing the number such as *182# or *131#.

(ii) This message is received by the computer in the service provider’s network that processes USSD requests.

(iii) The USSD may have a reply for the user with a number of options and ask the user to select, for example, *182#. The USSD may reply with acknowledgement message such as: “Thank you for your request. Your message is now being processed. A reply will be sent to your phone.”

Practice Activity 2.2: Types of financial technologies and their use

1. Identify USSD codes available locally and frequently used in Rwanda. Practise to use each USSD code.

2. Find out some examples of software in financial transactions commonly used in Rwanda. Write down their trade names. Find out some of the functions that the identified software offer. Share your findings with the rest of the students.

2. Automated mail

• Automated mail refers to a business tool that makes it easy to process a large volume of mail.

• The sender uses electronic methods to address, sort, and prepare the information for mailing. The mails are then automatically sent to the users.

• Automated mail software can be configured to automatically send a reminder to customers about a planned event. The message sent will remind the customers about the date, the venue, and the time of the event.

• Institutions that send mails in bulk use automated mail. The Rwanda Education Board (REB) is an institution that uses automated mail to send bulk mails to stakeholders in the education sector.

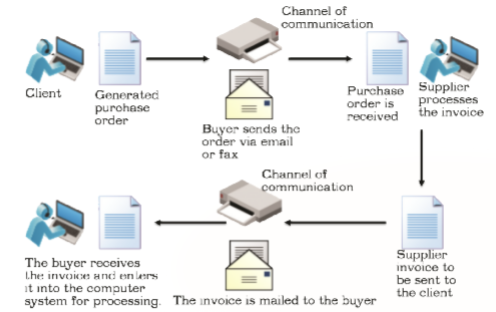

3. Electronic Data Interchange (EDI)

• EDI is a computer-to-computer exchange of business documents.

• It is a process that allows business partners to trade without the need for humans and paper work.

• EDI replaces postal mail, fax, and email. Though email is also an electronic approach, the documents exchanged via the email must still be handled by people rather than computers.

• EDI documents flow straight through the receiver’s computer. The processing of the business transaction can begin immediately.

• With EDI, an organisation receives and processes an order electronically. EDI reduces the number of days that the process takes to complete.

• Rwanda became the first country in sub-Saharan Africa to launch a one-stop electronic clearing system. This is an example of an electronic data interchange system where cross-border trade procedures are automated. This reduces the cost of doing business.

Figure 2.1: Processing a purchase order using an electronic data interchange (EDI)

2.1.2 Record Keeping

A record is something that represents proof of existence. A record can also be used to recreate or prove evidence about the past. Records are usually in writing or any other permanent form.

Record keeping is the systematic process of recording, creating, capturing, and maintaining transactions and events in an accounting system.

Record keeping software such as accounting software, databases, and book keeper provide ready-made reports. They also provide the user with a large storage space for files, back-up of records, and security of files through the use of passwords among other things.

Advantages of using computers in record keeping

(iv) It is an efficient way to keep financial records.

(v) It requires less storage space than physical files.

(vi) It is easy to generate financial reports such as orders, invoices, and debtor reports or other records.

(vii) Once the separate documents are done, the computer program is able to summarize and prepare the final financial records automatically.

(viii) Enables the user to back up records faster and keep them safely.

Disadvantages of using computers in record keeping

(i) Investing in computers for record keeping requires great amount of money.

(ii) For people to work with computers, they need to be trained properly. Training requires money.

(iii) In case there is no backup, one can easily lose data.

(iv) The quality of instructions issued to the computer by human operator determines the accuracy of content. 2.1.3 Stock Exchange

Stock exchange is a market where the shares of public listed companies are traded. These shares are in bonds, stocks, and other securities. In this market the shares are issued, bought, and managed.

Other names used to describe the stock exchange are stock market, bourse, and equity market.Automated Trading Systems (ATS) enable the customers to trade in stock without going through stockbrokers.

A stockbroker is a professional who buys and sells securities on a stock exchange market on behalf of his or her clients. In using the ATS, the computer in this case acts as the broker. The computer program used is able to create orders and automatically submit them to the ATS.

Figure 2.2: The stock exchange market in Rwanda

The use of computers in the stock exchange

An Electronic Communication Network (ECN) is a type of computerized network that is used in the stock exchange. It allows orders made to be communicated electronically.

To trade with an ECN, one must open an account with a broker. This allows the user direct access trading. To use the ECN, one enters an order into the ECN through a computer to allow one to trade on stock exchange.

Some ECN systems offer additional features such as negotiation. Negotiation is the process of making offers and counteroffers, with the aim of finding an acceptable agreement.

Stock trading

When a person or an institution engages in the buying and selling of stock, he or she is said to be engaging in stock trading.

Stock trading can be done online using computers that are connected through the Internet. This is called online stock trading.

Advantages of online stock trading

(i) Computers ensure that stock trading is faster and more efficient.

(ii) Investors get more up-to-date information.

(iii) It allows investors to buy or sell shares quickly.

(iv) It provides accurate market data. This is important for investors to make informed choices.

Disadvantages of online stock trading

(v) Mechanical failures may interrupt the trading process. Back up Internet connection is always required.

Revision Activity 2.1

Part A: Fill in the missing blanks with the correct answers

1. EDI stand for............................................... .

2. Examples of accounting software are .............................................and............................ .

Part B: Find and highlight terms used in financial transactions

Identify the following word that related to financial transactions. Circle them in the maze below: Transaction; Trading; Mail; Accounting; Stock; and Broker

Revision Activity 2.2

Read the following questions carefully and give the correct answers

1. Define the term ‘record keeping’.

2. State the role of computers in record keeping.

3. State three advantages of using ICT in the stock exchange.

4. Explain the role of ICT in Automation.

5. Explain automated accounting as used in financial technology.

Revision Activity 2.3

Do this activity:1. Research the advantages of the automated record keeping system over the manual. Make a class presentation to the other students.

2. Research the Rwanda stock exchange. Find out the stocks available in the market. Research some terms commonly used in the stock market. Find out their meanings. Prepare a report and present it to the teacher for marking.

2.2 Financial Technologies in Society

Financial Technology also known as FinTech refers to the use of software and digital platforms to offer financial services to consumers.

The use of financial technological tools often creates new and efficient means of providing services to consumers. It allows monies to be transferred through mobile devices. Users are able to transact without handling cash.

Most banks now offer a service called online banking. This service is also known as Internet banking, e-banking, or virtual banking. It refers to an electronic payment system that enables customers of a bank or other financial institution to perform banking transactions through the financial institution’s website. A customer is able to transfer money from one account to another through the use of a computer that is connected to the Internet. The following is a discussion of some technologies related to financial transactions, namely: E-commerce, ATM, and mobile banking.

2.2.1 E-Commerce

E-Commerce is electronic commerce. It is also known as eBusiness. It is the buying and selling of goods and services over the Internet using credit cards in online shops.

• Credit card: This is a plastic card normally issued by a financial institution to allow its user to borrow short-term pre-approved funds at the point of sale in order to complete a purchase. The debt does not incur interest until the period given by the bank elapses.

• Online shopping: This is a form of electronic commerce which allows consumers to buy goods services directly from a seller over the Internet.

Using a credit card in online shopping

The following are the steps for using a credit card in online shopping:

(i) Connect to a secure and encrypted network. To encrypt is to convert information or data into a secret code. This process helps to prevent unauthorised access.

(ii) Enter the online address of the website where you want to purchase the item from in the address box of the browser’s window.

(iii) Select the items to purchase and click the appropriate button used for purchasing the item.

(iv) Enter the shipping, billing, and credit card details.

(v) Click the appropriate button to complete the transaction.

(vi) Print the confirmation screen or proof of purchase received upon completing the transaction. Keep this record until the purchased item arrives.

How to Make Online Financial Transactions Secure

(i) Do not use the same passwords and usernames for all accounts.

(ii) Ensure that the password used is strong enough. A strong password contains a combination of numbers, symbols, and lowercase and uppercase letters.

(iii) Change the passwords frequently, preferably every one to three months.

(iv) Ensure the antivirus and firewall security programs are up-to-date.

(v) Consider using debit cards for online shopping transactions.

(vi) When performing online transactions do not use unsecured WIFI.

2.2.2 Automated Teller Machine (ATM)

An Automated Teller Machine (ATM) is an automatic transaction machine. It is used together with an ATM card or a debit card to access, deposit, withdraw, and check the account balances and print mini statements among other things.

To withdraw money from an ATM, do the following:

(i) Insert the card into the ATM machine. A dialog box is displayed.

(ii) Enter the Personal Identification Number (PIN) then press the Enter key. A dialog box is displayed. PIN refers to an identifying number. It is assigned to an account holder by the bank or any other organisation. It i used to check the accuracy of the user’s details when carrying out an electronic transaction.

(iii) Choose the type of transaction from the list provided such as withdrawal, deposit, mini statement, or checking account balances.

(iv) To withdraw money, select the amount from the list by pressing the button next to the desired value. However, if the value is not among the list, press the button labelled Next to avail other options. Type the amount in the box provided.

(v) The machine will automatically confirm if the account has enough money; if the money in the machine is adequate; and if the required money is within the bank withdrawal limit. A dialog box is displayed.

(vi) Select the button labelled Yes for the machine to produce a printed receipt, or No if a receipt is not required.

(vii) The machine dispenses the money, ejects the ATM Card, and finally produces the receipt if it was required.

Note: ATMs are primarily used for checking account balances and withdrawing money, but some ATMs enable the user to deposit money.

Depositing money in an ATM

To deposit money in an ATM, do the following:

(i) Insert the money in the dispenser.

(ii) Enter the Personal Identification Number (PIN) then press the Enter key. A dialog box is displayed.

(iii) Choose the type of transaction from the list provided, in this case deposit.

(iv) Press Enter button. The machine automatically counts the money and updates your account balance. It then displays a dialog box requesting if another transaction is required.

(v) Press the button next to No to exit. Remove your ATM card.

Figure 2.3: Using an Automated Teller Machine (ATM)

Checking the account balance in an ATM

To check your balance in an ATM, do the following:

(i) Insert the ATM card and your personal identify number (PIN).

(ii) Choose the type of transaction from the list provided, in this case balance enquiry.

(iii) Press the button labelled Next then press the Balance Enquiry option. The machine automatically checks the account and displays the information. Press ESC/Exit button to remove the ATM card.

Practice Activity 2.3: Using an ATM

Visit the nearest bank and ask the information officer to guide you to do the following:

• Use the ATM to withdraw and deposit money.

• Check the account balance.

• Understand the advantages and disadvantages of using the ATM.

You could also perform a library or Internet search on the above topics.

Some advantages of using the ATM

• Cash can be withdrawn at any time of the day.

• The ATM offers the convenience of transacting in multiple locations.

• The use of PIN ensures that your money safe in case the card is lost. Some disadvantages of using the ATM

• When there is a failure in the network, access to your account is denied.

• The ATM card could be stolen.

2.2.3 Mobile Banking

Mobile banking refers to the use of a mobile application and device to provide banking services to customers.

Most banks nowadays have the mobile banking facility. Some of the mobile banking facilities offered are:

(i) Buying airtime

(ii) Sending money to your mobile phone

(iii) Checking the balance

(iv) Withdrawing cash

(v) Transferring funds

(vi) Getting a mini statement

(iv) Service requests (Cheque book requests, Forex rates, full statement request, stop cheque)

Practice Activity 2.4: Activities on mobile banking

Use mobile devices or visit a mobile banking agent to do the following:

• Use mobile banking services to withdraw and deposit money.

• Check the account balance and get a mini statement.

Advantages of mobile banking

The following are some advantages of mobile banking:

(i) It makes life easier since customers can access their accounts from the comfort of their homes.

(ii) The customer is notified of any transaction carried out on their account.

(iii) Mobile banking applications are easy to use thus user-friendly.

(iv) The use of mobile banking reduces cases of fraud.

(v) The transfer of funds from one account to another is easy.

(vi) Paying of bills is done more quickly and at the convenience of the customer.

The process of loading money on a mobile phone account

When money is deposited in an account, it is automatically loaded to that account.

To load money in a mobile phone account, do the following:

(i) Visit an agent shop displaying the sign of a mobile money service provider.

(ii) Pay the money.

(iii) Provide your mobile phone number to the agent. Ensure that you do not disclose your PIN details to the agent.

(iv) Wait for a confirmation of the transaction from your service provider.Once the money is loaded on the mobile platform, it can now be transferred to the bank account. To transfer money to the bank account, obtain the procedure from the bank.

Figure 2.4: Mobile banking

The process of sending and receiving money

To send money via mobile banking services, do the following:

(i) Select SIM Toolkit from the phone.

(ii) Choose the mobile money service provider.

(iii) Select the Send Money option.

(iv) Enter the phone number of the recipient.

(v) Enter the amount of money to be sent. Ensure there is enough money to cater for the transaction charges.

(vi) Enter your PIN details.

(vii) Confirm the details entered then click OKThe process of withdrawing money

To withdraw money from the account, do the following:

(i) Visit an agent shop displaying the sign of mobile money service provider.

(ii) Select SIM Toolkit from the phone.

(iii) Choose the mobile money service provider.

(iv) Select the Withdraw Cash option.

(v) Select From Agent option.

(vi) Enter the agent number.

(vii) Enter your PIN details.

(viii) Enter the amount of money to be withdrawn. Ensure there is enough money to cater for the transaction charges.

(ix) Confirm the details entered then click OK.

(x) Wait for a message to be sent to the agent’s phone and your phone confirming the transaction. The agent provides the money at the end of the transaction.

Practice Activity 2.5: Using mobile telephony to send and withdraw money

With phones that are enabled for mobile banking, do the following:

• Deposit, withdraw, and send money.

• Use mobile money to buy items and pay for services such as airtime, electricity, water, goods, and television services among other things.

Mobile money transfer services have made life easier in Rwanda

(i) Users can easily save and withdraw money using their mobile phones.

(ii) Through mobile money transfers, users can easily buy and sell items without travelling long distances.

(iii) Some mobile money service providers in Rwanda have collaborated with transport companies that operate various routes. Travellers are able to pay their travel fares using mobile telephony.

Mobile money security

To ensure that your money in the mobile device is secure, do the following:

(i) Do not share the details of your PIN with anyone.

(ii) Reset the security details such as the PIN frequently.

2.3 Impact of Financial Technology in Society

Financial technologies can have both positive and negative effects on society.

2.3.1 Positive Impact of Financial Technologies

Financial technologies have brought beneficial changes to society. These include the following:

• Quick service delivery

• Security in transactions

• Unlimited access to the users bank account

• Automated billing

• Automation of routine tasks

• Creation of job opportunities

• Communication networks

• Easy management of payroll

• Increased revenue to country

• Solution to bank service problems

1. Quick Service Delivery

The use of computers to buy and sell shares on the stock market is an example of a financial technology. It allows the stock exchange to be carried out through Internet connectivity. Customers are able to get the information they require faster. This enables them to make informed decisions very fast.

The Bank of Kigali, for example, has partnered with mobile telephone service providers to offer online banking. In this way, service delivery has improved and customer satisfaction is enhanced.

2. Security in Transactions

• Every account holder deposits and withdraws money from his or her account. This money must be protected from danger or threat related to financial transactions such as fraud.

• To protect money held in a bank account, customers are advised to take some precautionary measures. For example, one should not share their PIN number with anyone.

• To withdraw money from an Automated Teller Machine (ATM), customers are issued with an electronic card. The card contains the customer’s financial details.

• A customer can withdraw and deposit money, pay bills, and shop using it. A customer should report to the bank immediately if his or her electronic bank card gets stolen or lost.

3. Convenience

• Through the use of an ATM, customers have access to banking services from anywhere worldwide.

• Customers are able to access their accounts without going to the main branch.

• Some banks have also expanded online banking to mobile banking. In this way, a customer is able to perform a transaction through a mobile device such as a smart phone or a tablet.

Figure 2.7: Mobile banking

4. Unlimited access to the user’s bank account

Banks are able to provide their customers unlimited access to their accounts through agency banking, mobile banking, plastic money, and remote banking among other things.

In agency banking, a mobile network operator is able to offer banking services within a locality, for example, in a rural setting or village. In this way, one does not have to travel long distances to the headquarters of the bank in order to carry out a transaction.

Some transactions that one is able to do in agency banking include depositing, withdrawing, and transferring funds, paying bills and requesting the account balance. Banking agents can be situated in drug stores, supermarkets, post offices, and near workplaces.5. Automated system of issuing bills (invoices)

An invoice is a list of goods sent or services provided by a company, issued together with a statement of the amount of money owed. Another name for an invoice is a bill.

Financial technologies enable businesses to invoice goods and services through computer systems. The bills are then sent to the customers via emails through Internet connectivity. This eliminates the cumbersome manual preparation of invoices.

Billing software is designed to allow the creation of customer accounts. Each account contains all the data bout the customer that is needed to accurately prepare the invoice. This data may include the customer’s name, the contact address, including the email, and the physical address to allow the efficient delivery of goods.

In Rwanda, billing systems are commonly used by suppliers of goods to supermarkets and other stores

Figure 2.8: An Automated Billing system

There is also a law that requires every VAT registered taxpayer to use electronic billing machines (EBMs). The transactions on the billing machines enable the Rwanda Revenue Authority (RRA) to monitor payment of taxes by business operators.

6. Automation of routine tasks to increase efficiency

Computers and computerized systems have replaced human labour in performing some activities, especially routine tasks. The following are some benefits of automating routine tasks:

• The quality of products is improved. This is because tasks are performed with accuracy and with speed. The level of accuracy that s achieved by automation is higher than that which is achieved by human labour.

• An automated system works at a constant speed without pausing for frequent breaks, sleep, and holidays. In this way higher productivity is achieved.

• Automation increases safety in the workplace. Workers are moved to supervisory roles where they no longer have to perform hazardous tasks.

7. Creation of job opportunities

New job opportunities are created by the introduction of financial technology. In Rwanda and other countries across the world, new job opportunities have been created. Examples include the following: ICT manager, bank agents, data entry clerks, and systems analysts among others.

8. Communication networks

Communication networks have improved financial services by bringing the services nearer to the people, making it cheaper, faster, and more reliable. The following are communication networks that are used to offer financial services:

• Internet: Communication of information on financial transactions through emails has led to improvement in business operations. The Internet banking has improved operations in the banking sector. Customers are able to access their bank accounts and perform transactions any time of the day and from anywhere. Financial institutions also use the Internet to send statements of accounts to their customers.

• Social Networks: Financial institutions have embraced the use of social networks as communication tools. These platforms are used by financial institutions to share information with their clients, as well as to market their services to potential customers. Some examples of common social networks include Twitter, Facebook, and Instagram among others.

• Short Message Service (SMS): These are short text messages sent via a mobile phone for communication. Financial institutions use these services to communicate with their customers.

9. Easy management of the payroll

In most organisations in Rwanda, salaries are paid through electronic funds transfer (EFT). This is a financial system by which money is transferred from one bank account to another. This transfer can either be within a single financial institution or across other institutions. EFT does not require the direct involvement of bank staff. The use of EFT simplifies the process of preparing the payroll and reduces the costs associated with the process.

10. Solution to bank service problems

Banking institutions have been experiencing huge challenges when serving large numbers of customers. Some of these challenges include long waiting times, limited time for customer servicing,transaction errors due to the bank personnel and excessive bureaucracy. Financial technologies have been used to provide solutions to these challenges in several ways. A discussion on some of these follows.

• Long waiting times: Long queues of customers waiting for services in the banking hall have been reduced. This has been achieved through:

- Electronic Funds Transfer (EFT): Customers use debit cards, credit cards, and smart cards to transfer money without visiting the bank either by use of ATM or online banking.

- Mobile banking: The customer is able to access banking facilities by the use of mobile phones and applications that support all services offered by the bank.

- Internet banking: This is made possible through online banking facilities available on the Internet. Clients can carry out banking transactions without physically visiting the bank.

• Limited time for customer servicing: Before the introduction of technology, the banks were not able to provide services to their customers beyond their operational hours. The introduction of ATM means that the user can access his or her account any time and from anywhere without limitation of time or place. Also through the use of Agency and online banking, a customer can access banking services from anywhere.

• Transaction errors by the bank personnel: Transaction errors caused by banking personnel have been reduced through automation of most of the bank services, for example, counting of currency notes is now done by currency counting machine, withdrawals are done by use of the ATM, funds can be transferred electronically, deposits can be done using the ATM, and bills can be paid using a credit card. All these processes help to reduce errors.

• Excessive bureaucracy: This happens when management takes too long to make decisions on issues such as approval of bank loans. Customers wait for a long time trying to get feedback. Automation of loan processing and approval has reduced excessive bureaucracy and made the process quicker.

2.3.2 Negative Impact

These are the problems that society experiences related to financial technology. Examples include fraud and unemployment.

1. Online financial fraudOnline fraud is an intentional act of dishonesty that is committed using Internet connectivity that may lead to loss of funds or financial data. A bank may, for example, lose personal information of the customers. This information may then be used to commit theft or other unlawful activities.

In other online financial fraud, victims may be misled to transfer money to the accounts of those committing fraud.

For example, an offender may send an email to a victim pretending to be an officer in the bank. The victim may be led to give his or her bank account information.

If the victim unwittingly releases his or her information, the offender may use the stolen identity to withdraw money from the victim’s bank account and transfer it to his or her own account. In this case, a financial fraud is committed.

2. Loss of jobs causing unemployment

Technological unemployment is a situation where job losses are caused by the development of technologies.

Financial institutions have automated certain services such as counting of money. They have also automated services such as deposits and withdrawals through the use of automated teller machines. This automation has led to loss of jobs for tellers and cashiers.

2.5 Definition of the key words in this unit

Revision Exercise 2

1. Explain three points to illustrate the positive impact of financial technology in society today.

2. State two advantages of mobile banking.

3. Explain how fraud can be carried out using computer tools.

4. Explain the impact of mobile and agency banking on society.