UNIT 3: TAXES IN BUSINESS

Key Unit Competency:To be able to justify the need for taxes in economy

Introduction

Every business requires developed infrastructure such as roads, hospitals, legal protection, welfare security, environment preservation, among others to operate successfully. The government provides such infrastructure. It provides education, health services, and security to all citizens and helps to increase the standards of living of the citizens hence ensuring availability of skilled labor force. For all this to happen, the government needs funds. Taxes are like the income for the government, and so for their survival, business needs to pay taxes to the government.

Introductory Activity: A case study

Why Do You Have to Pay Taxes

Every year around, before and after June 15, everybody especially business people will be discussing about tax changes in the national budget. This is because tax reforms and new taxes introduced are announced on that day. However, have you ever wondered why you and businesses need to pay taxes?In Rwanda, there are arms of the government (ruling bodies)from the village, sector, district, provincial and national levels. These bodies comprise: Legislature (who make laws), Executives (who enforce laws) and Judiciary (exercise laws).

The salaries that public servants receive to do their jobs come from taxes. Paying taxes is considered as a civic duty, although doing so is also a requirement of the law.Taxes take many forms, too. When you work at a job to make money, you pay income taxes. Depending on how much money you make, a certain percentage (part) of the money you make is withheld (kept out of your paycheck and sent to the government).When you buy things at a store, you also usually pay sales tax, which is a percentage of the cost of the item charged by the store.

If you own property, you also pay property taxes on the value of your property.Paying your taxes is considered a civic duty, although doing so is also a requirement of the law. If you do not pay your taxes, the government agency that oversees taxes — the Rwanda Revenue Authority (RRA) - will require you to pay your taxes or else face penalties, such as fines or going to jail.The money you pay in taxes goes to many places. In addition to paying the salaries of government workers, your tax dollars also help to support common resources, such as police and firefighters.

Tax money helps to ensure the roads you travel on are safe and well-maintained. Taxes fund public libraries and parks. Taxes are also used to fund many types of government programs that help the poor and less fortunate, as well as many schools!Each year as the “tax day” rolls in, adults of all ages and businesses must report their income to the RRA, using special tax forms. There are many, many laws that set forth complicated rules about how much tax is owed and what kinds of special expenses can be used (“written off ”) to lower the amount of taxes you need to pay.For the average worker, tax money has been withheld from paychecks throughout the year. On “tax day,” each worker reports his or her income and expenses to the RRA.

Alabestrum tesenih icipieris acchicuror licaetis publis; ne is, pro manum pl. Otierum te audem halegernum optessis pro, nos in in Itament urent, catant? Bem in Itandam ingultus pos rei popostilia? Saturec iactus, fit ficis Ahabunit, viver pore conoventius C. Batur quam ia? Quiu es optifex senium intilis pubis. Verma, non

Employers also report to the RRA how much they paid each worker. The RRA compares all these numbers to make sure that each person pays the correct amount of taxes.If you have not had enough tax money withheld from your checks throughout the year to cover the amount of tax you owe, you will have to send more money (“pay in”) to the government. If, however, too much tax money was withheld from your paychecks, you will receive a check (get a “refund”) from the government.

Adapted from https://wonderopolis.org/wonder/why-do-you-have-to-pay-taxes)

From the passage, answer the following questions:

a. What are the major changes expected by people especially business people on June 15, every year?

b. What makes the business people so anxious to know the changes mentioned above in a)?

c. Why do you think it is important for businesses to pay taxes to the government?

d. How do the following benefit from taxes?

i. Entrepreneur.

ii. Government.

iii. Society.

e. What do you think are some of the obligations of those who pay taxes?

f. Identify and briefly explain e types of taxes paid in Rwanda?

g. What happens to businesses or people who do not pay taxes?

h. What is the difference between tax and taxation?

3.1. MEANING OF TAXATION CONCEPTS

Activity 3.1

Analyze the following scenario and answer questions that follow:

Ruth is a prominent trader in one of the growing centers of eastern province. He normally buys his goods from the neighboring country of Uganda. In the previous budget, the minister announced that in order for the government to be able to fund its activities such as providing free education, road construction, all people will pay a certain amount of money to the government but charged on the goods sold and bought in form of taxes. Ruti realized that this might reduce his profits. Therefore, he decided that in order to continue getting the same profits, he would:

•Pay some boys to get for him some goods from Uganda by crossing the river without going to customs to pay taxes.

•For goods on which he would pay taxes, he would increase the prices charged to the customers.

•Reduce or stop buying some of the goods on which the tax had been increased.

Questions:

From the scenario, what do you think is the meaning of the following,

1. Tax.

2. Taxation.

3. Tax avoidance.

4. Tax evasion.

5. Tax shifting.

6. From the decisions Ruti made, which of them is:

a. Tax avoidance.

b. Tax evasion.

c. Tax shifting.

7. Among the three actions, which one (s) do you think he can be penalized for? And why?

Tax and Taxation, Tax Evasion and Avoidance, Tax shifting

Tax is a fee without direct exchange requested to the members of the community by the State according to the law, to support financially the execution of the government tasks.

Business tax refers to compulsory and non-refundable payments made by the business to the government or local authority to raise revenue to the government or local authority.

Taxation is a system of raising money or revenue by the government from individuals/businesses and companies by law through taxes.

It is a means by which governments finance their expenditure by imposing charges on citizens and corporate entities.

Taxation refers to the practice of government collecting money from its citizens to pay for public services.

Tax avoidance is a situation where a businessperson does not pay tax because s/he has avoided the product or activity on which the tax is imposed.It is the taxpayer’s exploitation of the loopholes in the tax system there by paying less tax than what they are supposed to pay.

Some Examples of Tax Avoidance:

•Taking legitimate tax deductions to minimize business expenses and thus lower your business tax bill.

•Setting up a tax deferral plan to delay taxes until a later date.

•Taking tax credits for spending money for legitimate purposes, like taking a work opportunity tax credit for hiring workers in your business.

Tax evasion is the illegal practice of not paying taxes, by not reporting income, reporting expenses not legally allowed, or by not paying taxes owed. In businesses, tax evasion can occur in connection with income taxes, employment taxes, sales and excise taxes, and state, and local taxes.

Examples of practices considered as tax evasion:

•It is considered tax evasion if you knowingly fail to report income.

•Under-reporting income (claiming less income than you actually received from a specific source).

•Providing false information to the RRA about business income or expenses

•Deliberately underpaying taxes owed

•Substantially understating your taxes (by stating a tax amount on your return that is less than the amount owed on the income you reported).

•An employer fails to withhold income tax from employee paychecks, or withholds but fails to report and pay these payroll taxes.

•Employment leasing, which involves hiring an outside payroll service that does not turn over funds to RRA.

•Paying employees in cash and failing to report some or all of these cash payments.

•Filing false payroll tax reports or failing to file these returns.

Tax shifting is the transfer of either part or the whole amount of tax imposed on a taxpayer to another party (other taxpayer).

Business firms pay general sales taxes, but most of the cost of the tax is actually passed on to those who buy the goods that are being taxed.

Example if the tax on sugar is increased and as result,a sugar producer or seller increases its price, in essence/reality the producer or seller is trying to recover the amount paid as the tax by collecting it from consumers in form of increased sugar prices.

Application Activity 3.1

1. With examples, differentiate

a. Tax and Taxation

b. Tax avoidance and Tax evasion

c. Tax evasion and tax shifting

2. What do you think is the purpose of taxation?

3. Do you think tax evasion is good? Give reasons to support your response

3.2. Benefits of paying taxes to Entrepreneur, Government and Society

One of the most frequently debated political topics is taxation. Taxation is the practice of collecting taxes (money) from citizens based on their earnings and property. The money raised from taxation supports the government and allows it to fund police and courts, have a military, build and maintain roads, along with many other services.

Activity 3.2

1. With examples from your community or Rwandan community at large, why do you think people and business enterprises need to pay taxes to the government?

2. As an entrepreneur to be or referring to activities of entrepreneurs in your community, how do you think businesses or entrepreneurs benefit from paying taxes?

3. In general, how does your society benefit from paying taxes? Give examples to support your views

3.1.2 Benefits of paying taxes to an entrepreneur

•Paying taxes by the entrepreneur helps the business activity to continue, as it does not face penalties and associated costs from the RRA for non-payment.

•When an entrepreneur pays taxes, it improves his/her reputation or public image which may result into increased customers and better services from the government

•To avoid inconveniences of closure of the business and its associated costs: when entrepreneur fails to pay assessed taxes, his/her business is subject to penalty even closure to some cases.

•Business needs certain infrastructure to operate successfully such as roads to move raw materials, finished goods, workers; security for their enterprises, goods, among others, which are provided by the government.

•Paying taxes means contributing money to government agencies or departments such as Development Bank of Rwanda (BRD), Business Development Fund (BDF), which support entrepreneurs to operate business activities through soft loans and other financial support.

3.2.2 Benefit of paying taxes to the government

•Source of government revenue: taxes are the main source of government revenue to finance its public expenditure. So taxes enable the government to pay it workers, construct roads, maintain security, provide health care, education among others

•Taxes benefit the Rwandan government to meet its objectives and goals such constructing affordable houses to the citizens which helps improve the standards of living

•Taxes help government to finance its policies especially on poverty alleviation through programs such as “GIRINKA”, “VUP”, “UBUDEHE” among others

•Taxes enable the government to regulate the prices of goods and services in the country hence ensuring a low cost of living and maintaining the standards of living of the citizens

•Taxes enable the government to maintain a balance between the poor and rich. The government uses the taxes from business people to provide services needed by the poor, which otherwise the rich could not provide.

•Taxes enable the government to promote its policy industrialization through reducing products from other countries that would otherwise out compete the home industries.

•Taxes enable the government to ensure that the citizens have enough products. This can be through taxes charged to reduce products moving out of the country or removing taxes on goods needed in the country. This helps maintain a high standard of living.

3.2.3. Benefits of paying taxes to Society

1. There is reduced rates of poverty among the community due to a significantly equal distribution of income through various activities and projects set by the government

2. Improved wellbeing among the vulnerable and elderly as they benefit from the different government programs financed through taxes.

3. Reduced infant mortality rates and increased life expectancy due to improved access to health facilities and services.

4. Increase in the percentage of the population that completes secondary and TVET education, reducing the literacy levels, improving on the peoples’ skills through programs such as 12YBE.

5. Increased community/social solidarity, general happiness, life satisfaction, and a significant more trust among the community members and for public institutions.

6. Taxes are charged on some products to discourage their production and usage hence controlling over-exploitation of resources as well as protecting the environment which is vital for the existence of the society.

Application Activity 3.2

1. By giving specific examples from your community, how does your society benefit from taxes?

2. What do you think would happen to business activities if taxes were not paid?

3.3. Principles of taxation

Activity 3.3

1. In your community, probably you have heard people and business people complaining about the taxes they pay or charged to different or similar items. Identify any 5 things you have heard normally people complain about.

2. If you were the one determining or imposing taxes to people and businesses, mention any five things you would put into consideration.

Principles or canons of taxation are rules and regulations that should be observed in the tax assessment, collection and administration. Adam Smith put forward the following canons/principles Convenience: Places, periods and seasons in which the tax dues are collected should be convenient to the taxpayer. For example, the convenient time to a trader is when s/he has made profit. For a farmer, is when s/she has sold his/her productivity

3. Simplicity: The type of tax and the method of assessment and collection must be understandable by both the taxpayer and tax collectors. Complicated taxes may lead to disputes, delays and high costs of collection in terms of time and resources.

4. Certainty: The taxpayer must know the nature, base and amount of a tax without doubt. Unpredictable taxes discourage investment and reduce work effort. Simply the tax should not be arbitrary.

5. Economy: The cost of collection and administration of tax must be much lower than the tax collected

6. Elasticity: A tax should change directly with change in the tax base. If the tax base increases, the tax charged on the tax base should also increase.

7. Productivity: The fiscal authorities should be able to predict and forecast accurately the revenue a particular tax would generate and at what rate it would flow in.

8. Equity: Tax assessment should be in such a way that tax payers bear a proportionately equal burden. I.e. people who earn more income should be taxed more than those who earn less income.

9. Diversity: This canon requires that there should be a number of taxes of different varieties so that every class of citizen may be called up on to pay something towards the national priorities

Application Activity 3.3

1. Why is it important to have principles of taxation?

2. Referring to the principles of taxation you know, briefly explain why each is important to the taxpayer and tax authority (RRA)

3. From the list of principles of taxation, which one do you think is the most important than others? Give reasons to support your answer.

3.4. Rights and obligation of the taxpayers

Activity 3.4

Basing on your knowledge on civic education, standards in business and other knowledge related to rights, answer the following questions:

1. What do you understand by “Rights”?

2. What do you understand by “Obligations/responsibilities”?

3. Using examples, differentiate a “Right from an Obligation”

4. If customers have rights, do you think taxpayers should also have rights? Give reasons to support your response.

5. If your response is yes in 4 above, mention some of the rights you think taxpayers should have.

6. Do you think taxpayers have obligations or responsibilities? Give reasons to support your response.

7. If your response is “yes” in question 6 above, mention some of the obligations/responsibilities of taxpayers.

3.4.1. Rights of taxpayers

a. The right of appeal: The right of appeal against any decision of the tax authorities applies to all taxpayers, and to almost all decisions made by the tax authorities, whether as regards the application of the law or of administrative rulings, provided the taxpayer is directly concerned.

b.The right to be informed: Taxpayers have the right to know what they need to do to comply with the tax laws.

c. The right to quality service: Taxpayers have the right to receive prompt, courteous, and professional assistance in their dealings with the RRA, to be spoken to in a way they can easily understand, to receive clear and easily understandable communications from the RRA.

d. The right to pay not more than the correct amount of tax: Taxpayers should pay no more tax than is required by the tax legislation, taking into account their personal circumstances and income.

e. The right to certainty: Taxpayers also have a right to a high degree of certainty as to the tax to be paid.

f. The right to privacy: All taxpayers have the right to expect that the tax authorities will unnecessarily not intrude upon their privacy.

g.The right to confidentiality and secrecy: Another basic taxpayers’ right is that the information available to the tax authorities on the affairs of a taxpayer is confidential and will only be used for the purposes specified in tax legislation.

h. The right to legal representation: Taxpayers have the right to retain an authorized representative of their choice to represent them in their dealings with the RRA

i. The Right to tax refund: A taxpayer gets a tax refund when he/she has overpaid taxes to the government. A tax refund is the difference between taxes paid and taxes owed.

3.4.2. Obligations of taxpayers in Rwanda

•Obligations of a VAT registered taxpayer: An article 57- 63 specifies the rights and obligations of a VAT registered taxpayer and include the following:

a. Must clearly display the VAT registration certificate in a plain view at the entrance of his place of business for his/her client to see.

b. Must issue a VAT invoice to his/her customers every time they purchase goods or services from him/her.

c. Must file a monthly or quarterly VAT return on the appropriate form (UNG11).

d. Must be available at all times to receive VAT officers and to make available to the officer books of accounts ascertaining to the business.e. Must use an Electronic Billing Machine in invoice issuing.

•Other obligations of taxpayers include: The obligation to register with RRA (Rwanda Revenue Authority). Registration is immediately required whenever someone starts not later than seven (7) days of business activities, otherwise sanctions or penalties are required including that of business closure.

-The obligation to be honest.

-The obligation to be co-operative.

-The obligation to provide accurate information and documents on time.

-The obligation to keep records.

-Providing accurate information to the Rwanda Revenue Authority .

-The obligation of signing of tax returns

-The taxpayer must sign the form on which s/he makes an annual statement of income and personal circumstances, used by the tax authorities to assess liability for tax.

-The obligation to pay taxes on time

Application Activity 3.4

Analyze the following scenario and answer questions that follow

Mutesi started a business dealing in selling agricultural products in one busy center in Musanze. She only got a trading license from the Umurenge (Sector) which used to carry out her business activities. She never kept records of her business transactions saying that as long as she can calculate the amount profit gained, the rest does not matter. She never issued receipts to her customers or not even asking for them from her suppliers. So, one-day staff from RRA visited her business and everything was a total mess.

Questions:

1. What mistakes did Mutesi do?

2. Do you think Mutesi is supposed to pay taxes? Why?

3. Which obligations/responsibilities did she not meet?

4. What do you think are the likely consequences after the visit by RRA?

5. Does Mutesi have any rights after the visit by RRA as a taxpayer? If yes, which are those rights?

6. If Mutesi is to correct her mistakes, which rights will she be entitled to?

3.5. Taxes imposed on business in Rwanda

Activity 3.5

Basing on your experience or knowledge,

a. Mention any taxes paid in Rwanda by people and businesses you know

b. “Even a one-day baby, pays taxes”. Is this statement true? Justify your answer.

c. With examples, differentiate direct taxes from indirect taxes

Direct and Indirect tax

Central government raises revenue through a wide range of taxes. The tax law is made by statute. They are two types of taxes, namely: direct taxes and indirect taxes.

Central government raises revenue through a wide range of taxes. The tax law is made by statute. They are two types of taxes, namely: direct taxes and indirect taxes.Direct taxes

Direct taxes are paid entirely by a taxpayer directly to the government. It is the tax where the liability as well as the burden to pay it resides on the same individual.Examples of Direct taxes

i. Personal income tax:The tax levied on individuals whose income is above a certain level. It is generally progressive and deducted by the state. It applies to salaries, wages, rent, interests, employment income, business profits, and investment income.A resident taxpayer is liable to income tax per the tax period from all domestic source and foreign source.A non - resident taxpayer is only liable to income tax, which has a source in Rwanda.ii. Corporate income tax:Corporate income tax is deducted by the state on industrial and commercial income achieved by the firms working as commercial companies. It is generally proportional to the firm’s income. Where a company is registered in Rwanda and its management and control is exercised in Rwanda in a particular year, such a company is considered a resident company and is liable for taxation. Organizations with legal personality or organizations are subject to corporate income tax.iii. Trading license:The trading license tax is paid by any person who deals with a profit-oriented activity in Rwanda. It is paid before starting activities. It is paid every year not later than 31st March with ongoing business.iv. A professional income tax or PAYE (Pay-As-You-Earn):PAY E: is composed of Wages, salaries, leave pay, sick pay, medical allowances, pension payment etc. All kinds of allowances including any cost of living, subsistence, rent, and entertainment or travel allowances’.v. Withholding tax:Withholding tax of fifteen percent (15%) is levied on the following payments made by resident individuals or resident entities including the following:•Dividend, except those governed by Article 45 of this law;•Interests;•Royalties;•Service fees including management and technical service fees;•Performance payments made to an artist, a musician or an athlete irrespective of whether paid directly or through an entity that is not resident in Rwanda;•Lottery and other gambling proceeds;vi. Rental income tax:The rental income tax is paid by any individual who earns income from renting out the fixed assets located in Rwanda, including land, buildings and improvements.vii. Fixed asset tax:The following persons have to pay fixed asset tax if they have the land title deed:•The owner of the fixed asset;•The holder of fixed asset who’s the legal owner is unknown for a period of at least 2 years;•The holder of fixed asset if the freehold land title is not yet registered in the name of the owner;•The proxy who represents the owner who lives abroad;•Usufructuary (one who is using the asset)Indirect taxes

A tax imposed on consumption, sales, shipping, or production, rather than directly on the property or income of the consumer. Indirect taxes are generally included in the price of goods and services, so are less obvious to those paying the taxes than direct levies.Examples of Indirect tax

a. Value Added Tax (VAT): VAT has been introduced in Rwanda in 2001. VAT is a tax on the added value achieved by a firm. This is the difference between the buying price (of raw materials) and the selling price of the product in whatever form it is sold.b.Customs duties: This is the tax imposed on imports and exports. They include:i. Import duty:This is the tax imposed on imported goods toa. Get government revenueb. Discourage imports so as to protect domestic industriesc. Discourage imports so as to conserve foreign exchangeii. Export duty:This is a tax imposed on exports to raise the revenue and discourage the exportation of certain goods in order to satisfy the local market demand.c.Sumptuary tax: This is a form of a sales tax, which carries a very high rate imposed in order to discourage the production and consumption of a particular commodity on grounds of morality, health or economic consideration to maintain productive efficiency. Example; taxes on alcoholic drinks, cigarettes etc where wines pay 70%; brandies, liquor and whisky 70%, cigarettes 150%.d. Sales tax: Sales tax is imposed on sales of commodities. In Rwanda, the sales tax is charged to consumers based on the purchase price of certain goods and services. The benchmark used for the sales tax rate refers to the highest rate – 18%Application Activity 3.5

1. Discuss the taxes vested to local authorities (Districts)2. Why do you think sumptuary tax rights are higher compared to others;3.6. Tax computations and exempts

Activity 3.6

1. Do you think it is important for an entrepreneur to know how to compute the amount of tax he/she is supposed to pay? Give reasons.2. What do you think the term “tax exempt means”?Tax computations

a. Personal income tax

Note:Benefits in kind (non-cash benefits) received from employment are generally taxable as follows:

Note: Retirement contributions to an approved pension fund made by the employer on behalf of the employee and/or contributions made by the employee, to a maximum of 10% of the employee’s employment income, or 1,200,000Frw a year, whichever is the lowest.

b.Corporate income tax

Tax rate

i. Taxable Business profit is rounded down to the nearest one thousand Rwandan Francs (1,000Frw) and taxable at a rate of thirty percent (30%).Newly listed companies on capital market shall be taxed for a period of 5 years on the following rates:

•20% if those companies they sell at least 40% of their shares to the public;

•25% if those companies sell at least 30% of their shares to the public;

•28% if those companies sell at least 20% of their shares to the public.

ii. Venture capital companies registered with the capital markets Authority in Rwanda benefit from a corporate income tax of zero percent (0%) for a period of five (5) years from the date the decision has been taken.

However, a registered investment entity that operates in a Free Trade Zone or foreign companies that have its headquarters in Rwanda that fulfill the requirements stipulated in the Rwandan Law on Investment Promotion are entitled to:

•Pay corporate income tax at the rate of zero percent (0%);

•Exemption from withholding tax mentioned in Article 51 of the Law nº 16/2005 of 18/08/2005 on direct taxes on income;

•Tax free repatriation of profit.

iii. If a taxpayer exports commodities or services that bring to the country between three million (3,000,000) US dollars and five million (5,000,000) US dollars in a tax period, he or she is entitled to a tax discount of three percent (3%).

iv. If he or she exports commodities or services that bring to the country more than five million (5,000,000) US dollars in a tax period, he or she is entitled to a tax discount of five percent (5%).

v. Companies that carry out micro finance activities approved by competent authorities pay corporate income tax at the rate of zero percent (0%) for a period of five (5) years from the time of the approval of the activity.

However, this period may be renewed by the order of the Minister.

Example.

Alpha Ltd company has obtained an accounting income of 960000RWF. Morever the other expenses deductable amount to 90000RWF. 30% of the profit put in the reserve.

Required:

1. Calculate fiscal (taxable) income of Alpha company?

2. Calculate corporate income tax (at the rate of 30%)

Possible solution :

a. Net profit before tax=960000- 90000=870000Frw

Reserve= 870000x30100 =261000Frw

Taxable income =870000-261000=609000Frw

b. Corporate income tax= 609000+30100=182700Frw

c . Trading license

Tax rateFor, the taxpayer registered for VAT, the trading license tax is based on their respective turnovers of the previous year, as follows: For others not registered for VAT, the trading license tax depends on the type of activity and location, as shown in the table below:

For others not registered for VAT, the trading license tax depends on the type of activity and location, as shown in the table below:

d. A professional income tax or PAYE (Pay-As-You-Earn)

Example:

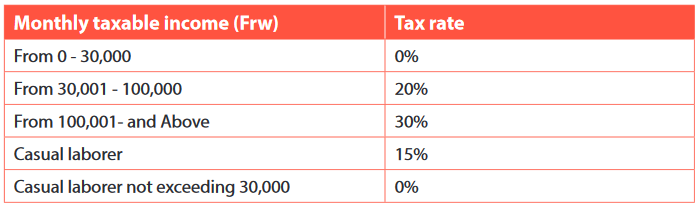

The following relate to monthly salaries of Kanyarwanda enterprise employees for 2018:a. Rukundo earns 450,000frwb. Karinganire earns 89,000frwc. Keza earns 28500frwd. Buzima earns 12,5000frwRequired:Calculate the total PAYE for above employees that Kanyarwanda enterprise pays to RRA every month.Solution:a. Rukundo :Step1: 30000 is exempted (30000*0)=0Step2: 100,000-30000 =70,000*20%= 14000FrwStep 3: 450000-100,000= 350,000*30%= 105000FrwTotal TAX for Rukundo = 14000+105000= 119000Frwb. Karinganire :Step1: 30000 is exempted (30000*0)=0Step2: 89000-30000 =59000*20%= 11800FrwTotal tax for Karinganire is 11800frwc. Since Keza earns less than 30000Frw she does not pay PAYE. Her total tax =0 (28500*0)d. BuzimaStep1: 30000 is exempted (30000 *0)=0Step2: 100,000-30000 =70,000*20%= 14000FrwStep 3. 125000-100,000= 25,000*30%= 7500FrwTotal tax for Buzima =14000+7500=21,500FrwTotal PAY E for Kanyarwanda enterprise every month=119000+11800+21500=152300FrwNote:

Exemption for PAYE is that every person who earns income less than 30000 does not pay PAYE to RRA.The “casual laborer” means an employee or worker who performs unskilled labour activities, who does not use machinery or equipment requiring special skills, and engaged by an employer for an aggregate period not exceeding thirty (30) days during a tax period.e. Withholding tax:Withholding tax of fifteen percent (15%) islevied on the following payments made by resident individuals or resident entities:•A withholding tax of five percent (5%) of the value of goods imported for commercial use shall be paid at custom on the CIF (cost insurance and freight value) before the goods are released by customs;•A withholding tax of three percent (3%) on the sum of invoice, excluding the value added tax, is retained on payments or by public institutions to those who supply goods and services based on public tenders.f. Rental income tax:The rental income tax is calculated progressively by revenue brackets as follows:•0% on brackets lower than 180,000Frw,•20% from 180,001 to 1,000,000Frw•30% above 1,000,000FrwThe taxable income is obtained in one of two ways:•Deducting from the gross rental income 50%considered as the expenses incurred by the tax payer;•Deducting 30% from gross rental income as the expenses incurred plus bank interest on the rented fixed asset during the tax year;Tariff or tax rateThe tax rate is fixed at 1/1000 of the taxable value per year.Tax rateThe VAT rate is applied to duty-free goods. Several rates can be applied depending on the nature of products. The standards rate is usually 18%g.Value Added Tax (VAT):This is the tax charged on the difference between the buying price (of raw materials) and the selling price of the product in whatever form it is sold. VAT = F.P – I.C where F.P is final product, IC is intermediate costsExample

UTEXRWA industry bought cotton from a local farmer worth 1200, 000frw to use in production of blankets.170blankets were manufactured and sold to wholesaler at a cost of 4,000,000frw which he later supplied to Lemigo hotel at a value of 8,000,000frw VAT included. Calculate the value of VAT paid on blankets.Possible solution

Step 1: VAT paid by local farmer :VAT = FP - IC where FP is final product and IC is Intermediate CostVAT =1,200,000Frw*18% = 216,000FrwValue added = Sales - Total Purchases=4,000,000frw-1,200,000=2,800,000FrwVAT paid by wholesaler =2800, 000*18%= 504000FrwVAT paid by Lemigo hotel= 8,000,000Frw- 4,000,000FrwVAT = Value added * 18%= (4,000,000Frw*18%)=720,000FrwTherefore total VAT =216000+504000+720000 =1440, 000FrwAlternative:

VAT is calculated on sales.VAT = Sales *18%Which is equal 8,000,000frw*18%=1,440,000frwh. Sumptuary tax: Taxes on alcoholic drinks, cigarettes e.t.c where wines pay 70%; brandies, liquor and whisky 70%, cigarettes 150%i. Sales tax: The benchmark we use for the sales tax rate refers to the highest rate – 18%Application Activity 3.6

Answer the following questions1. Mr. Bob is living in Nyarugenge district and he owns the following fixed asset for which he obtained the freehold land title in 2010:i. A parcel of land in Gasabo district of 1 hectare on which he plans to build his hotel. The square meter is valuated at 5,000 Frw at 1st January 2011;ii. Commercial house in Nyarugenge district valuated at 200,000,000 Frw at 1st January 2011;iii. Residential house in Nyarugenge district purchased in 12/ 2010 at 100,000,000 Frw.Required:a. Calculate the total fixed asset tax to be paid by Mr Bob for 2011;b. Indicate the deadline of tax declaration and payment;c. Determine the fixed asset tax that belongs to each decentralized entity.2. Paul owns 3 houses located at Kicukiro district. For the year 2011, he received rental income of 12,000,000 Frw for each house.Required:a. Calculate the tax on rent payable for the revenues received in year 2011;b. Indicate the deadline of the tax declaration and payment.3. Suppose Bank of Kigali has, a part of its Headquarters, six (6) branches in Nyarugenge district, five (5) branches in Kicukiro district and four (4) branches in Gasabo district. The following additional information is relevant:i. The turnover of Bank of Kigali for the year 2011, according to the information provided by RRA, is 6,000,000,000 Frw;ii. The turnover of each branch is the average from the total turnover.Required:1. Calculate the total trading license tax for Bank of Kigali;2. Calculate the trading license tax that belongs to each district.Tax exempts

Activity 3.6

a. In Rwanda, not all goods and services pay taxes. Do you agree with this statement? Support your choice.b. Why do you think some goods should not pay taxes in Rwanda?c. Can you give some examples of goods and services you think should not pay taxes in Rwanda?Taxes exemptions

The exemption generally refers to a statutory exception to general rule rather than the mere absence of taxation in particular circumstances, generally known as exclusion. Tax exemption also refers to removal from taxation of a particular item rather than a reduction.a. Exemption from corporate income tax: The following entities from the Government of Rwanda are exempted from corporate income tax:i. The City of Kigali, Districts, Towns and Municipalities;ii. The National Bank of Rwanda;iii. Entities that carry on only activities of a religious, humanitarian, charitable, scientific or educational character, unless the revenue received during a tax period exceeds the corresponding expenses to the extent that those entities conduct a business;iv. International organizations, agencies of technical cooperation and their representatives, if such exemption is provided for by international agreements;v. Qualified pension funds;vi. The Rwanda Social Security Fund;vii. The Rwanda Development Bank;b. Exemptions on Value Added Tax:The following goods and services shall be exempted from value added tax:i. Services of supplying clean water and ensuring environment treatment for nonprofit making purposes with the exception of sewage pump- out services;ii. Goods and services for health-related purposes: (health and medical services, equipment designed for persons with disabilities, goods and drugs appearing on the list made by the Minister in charge of health and approved by the Minister in charge of taxes;iii. Educational materials, services and equipment; books, newspapers and journals;iv. Transportation services by licensed persons;v. Lending, lease and sale: ( sale or lease of land, sale of a whole or part of a building for residential use, renting or grant of the right to occupy a house used as a place of residence of one person and his/her family) etc.vi. Financial and insurance services;vii. Precious metals: sale of gold in bullion form to the National Bank of Rwanda;viii. Any goods or services in connection with burial or cremation of a body provided by an Order of the Minister in charge of finance; ix. Energy supply equipment appearing on the list made by the Minister in charge of energy and approved by the Minister in charge of taxes;x. Trade union subscriptions;xi. Leasing of exempted goods;xii. All agricultural and livestock products, except processed ones. However, milk processed, excluding powder milk and milk derived products, is exempted from this tax;xiii. Agricultural inputs and other agricultural and livestock materials and equipment appearing on the list made by the Minister in charge of agriculture and livestock and approved by the Minister in charge of taxesxiv. Gaming activities taxable under the Law establishing tax on gaming activities;xv. Personal effects of Rwandan diplomats returning from foreign postings, Rwandan refugees and returnees entitled to tax relief under customs laws;xvi. Goods and services meant for Special Economic Zones imported by a zone user holding this legal status;xvii. Mobile telephones and SIM cards;xviii. Information, communication and technology equipment appearing on the list made by the Minister in charge of information and communication technology and approved by the Minister in charge of taxes.c. Exemptions on Fixed Asset Tax:The following fixed assets are exempted from the fixed asset tax if they are not used for profit - making activities:i. Fixed assets used for medical purposes, vulnerable groups, educational and sporting activities;ii. Fixed assets intended for research activities;iii. Fixed assets belonging to the Government, Provinces, decentralized entities;iv. Fixed assets used for religious activities;v. Fixed assets used for charitable activities;vi. Fixed assets belonging to foreign diplomatic missions in Rwanda if their respective countries do the same for Rwanda;vii. Land in use for agriculture, livestock or forestry if it is not more than 2 hectares. If this land is more than 2 hectares, the tax is imposed only on the excess land;viii. Fixed assets used for residential purposes, if the assessed value does not exceed 3,000,000Frw. If the assessed value exceeds such amount, only the excess value is taxed.d. Exemptions on trading license:The Government entities are exempted from trading license tax.e. Exemption on fees paid on parking:The following vehicles do not pay parking fees when in official duties:i. Vehicles owned by the State, its institutions and projects that is when they have their identification plates;ii. Vehicles belonging to an Embassy;iii. Vehicles of the United Nations affiliated international organizations and other international organizations having specific agreement with the Government of Rwanda;iv. Special vehicles designed for disabled persons.3.7. Tax conflicts and Resolution

Activity 3.7

In the previous unit (contracts in business), we looked at conflicts and resolution:a. What conflicts do you think may happen between taxpayers and tax authorities (RRA)?b. What do you think may cause such conflicts between taxpayers and tax authorities?c. How do you think such conflicts may be resolved?3.7.1. Tax conflicts

Tax related disputes/disagreement may arise between taxpayers and tax authorities. Some tax conflicts arise under the following circumstances:•Disagreement on law: How the law is interpreted in relation to tax;•Disagreement on the tax rates and the amount to be paid by taxpayer;•Disagreement on exemption: Taxpayer may claim an exemption but tax collectors reject it;•Disagreement on the time of payment;•Disagreement on method of payment;•Disagreement on non-payment3.7.2. Resolution

When tax related conflicts arise between the taxpayer and authority, settlement process starts as follows:1. Administrative appealAppeal to the Commissioner General (CG)i. General•Taxpayer must appeal within 30 days after receipt of the notice•Forms of the appeal•Be in writing;•State the taxpayer’s identification number;•State the tax period;•Describe the assessment and the grounds of appeal;•Be signed by the taxpayer or his/her representative;•Contain all the evidences and legal arguments.•Appeal does not stop collection•Commissioner General (CG) may suspend the obligation to pay tax, interest and penalties, upon written request by the taxpayer, the Commissioner General (CG) may suspend the collection of the disputed amount for the duration of the appeal.ii. Decision•Commissioner General (CG) sends the decision within 30 days;•Commissioner General (CG) may extend once for 30 days and informs the taxpayer;•The appeal is supposed accepted, if decision is not made within 30 days;•The commissioner General (CG) informs taxpayer in writing about the decision.2. Amicable settlement•The taxpayer who is not satisfied with the decision of the Commissioner General may request the top Commissioner General for the amicable settlement.•In case both parties do not reach an amicable agreement, the taxpayer may make an appeal to the competent court.3. Appeal to the court•The taxpayer who is aggrieved by the decision of the Commissioner General (CG) may make a judicial appeal. This appeal is brought before the competent court within thirty (30) days after the receipt of the Commissioner General’s decision.Application Activity 3.7

Analyze the following scenario and answer questions that follow Mutesi started a business dealing in selling agricultural products in one busy center in Musanze. She only got a trading license from the Murenge (Sector) which she used to carry out her business activities. She never kept records of her business transactions saying that as long as she can calculate the amount of profit gained, the rest does not matter. She never issued receipts to her customers or not even asking for them from her suppliers. So, one day staff from RRA visited her business and everything was a total mess.Required:

Assume, Mutesi is not pleased with decision of RRA officials regarding her tax situation, advise her on the process she should go through for her to resolve the disagreement with the official’s decision.3.8. Special and non-Fiscal tax collection

Activity 3.8

a. Referring to your community/sector, mention all the ways you know that your sector (all administrative units/levels including Police...) raise revenue or money for providing services to citizensb. From all the sources you have identified, list those that you think are in form of taxes and those that are notc. How do we call such sources that are not in form of taxes?d. Differentiate tax from non-tax collectionNon-Tax Revenue is the recurring income earned by the government from sources other than taxes. In addition to taxes, business people pay other charges to the government and local authorities. These are non-tax collections or non-fiscal collections. The following are some of the non-tax collections that business people pay:a. Market Fees : Market fees are charged to a trader who sells goods or services in a place designed by the competent authority.The threshold of market fees is fixed by the district Council considering the size of the designated area and nature of the goods sold. The market fees are paid on monthly basis per stall and fixed as follows: b.Fees charged on public cemeteries: Fees are paid per tomb by individuals who need to bury their relatives. Fees charged per tomb range between 500 and 5,000 depending on area which the cemetery is located.The district council determines the area considered as public cemetery.c. Fees charged on parking: The parking fees are paid by any person who parks his/her vehicle in parking lots determined by a decentralized entity.Parking fees are paid per category of vehicles either per hour, per day or per month.

b.Fees charged on public cemeteries: Fees are paid per tomb by individuals who need to bury their relatives. Fees charged per tomb range between 500 and 5,000 depending on area which the cemetery is located.The district council determines the area considered as public cemetery.c. Fees charged on parking: The parking fees are paid by any person who parks his/her vehicle in parking lots determined by a decentralized entity.Parking fees are paid per category of vehicles either per hour, per day or per month. d. Fees on public parking: Fees on public parking are paid by vehicles entering in the public taxi parking.Public parking fees are paid on daily basis as follows:

d. Fees on public parking: Fees on public parking are paid by vehicles entering in the public taxi parking.Public parking fees are paid on daily basis as follows: e. Parking fees on boats: Parking fees on boats are paid by boats used for profit making activities that park in a boat parking area designated by the decentralized entity. Parking fees on boats are determined by the council of decentralized entity basing on the following threshold:

e. Parking fees on boats: Parking fees on boats are paid by boats used for profit making activities that park in a boat parking area designated by the decentralized entity. Parking fees on boats are determined by the council of decentralized entity basing on the following threshold: Other sources of non-taxes revenues include:•Fines and penalties on road offences;•General fines;•Certificate fees;•Fees from the service provided by districts;•Fees that are paid to renew registration;•Optional dues taken from the value of the building sold by the public auction;•Fees from selling of plots

Other sources of non-taxes revenues include:•Fines and penalties on road offences;•General fines;•Certificate fees;•Fees from the service provided by districts;•Fees that are paid to renew registration;•Optional dues taken from the value of the building sold by the public auction;•Fees from selling of plotsApplication Activity 3. 8

1. Gaparayi is a registered trader in Nyabugogo market. On every Friday, he takes part of the goods to the newly constructed Shyorongi market to attract more clients outside Kigali. In Nyarugenge district, the threshold of market fees is fixed at 10,000 Frw per month and per stall in Muhima, Nyarugenge and Gitega Sectors. The council of Rulindo district has decided to fix at 3000 Frw market fees per stall in all constructed markets across the district.Required:Calculate the monthly market fees to be paid by GAPARAYI.2. RRA is one of the institutions that owns many vehicles. The number of operational vehicles is estimated at 100 in Kigali city. The management has decided to settle vehicles related expenses on a monthly basis to facilitate the work of the accountants and reduce paper work.Required:Calculate the amount of parking fees to be paid by RRA for its vehicles operating in Kigali City considering that all operational vehicles are in the category of “Small vehicles and motorcycles”.3. Mutake owns two Coasters capable of transporting 36 passengers each. They operate between Kigali and Kayonza, taking passengers from Remera main taxi park and Kayonza modern taxi park. In Gasabo, fees in public parking are fixed at Frw 3,000 while in Kayonza fees are fixed at Frw 2,000 per day for this category of buses.Required:Calculate total public parking fees to be paid by Mutake on daily basis.4. Nyamasheke district has allocated a slot of 50 square meters as the boat parking area. The district council has fixed the boat parking per month as follows:Boat with engine capable to carry up 5 T ....................... 2,000FrwBoat with engine capable to carry more than 5T............ 3,000FrwBoat without engine........................................................ 1,000FrwCooperative ABASAMBAZA owns 10 boats in 3 categories: 4 boats with engine transporting 3 tons each, 3 boats with engine with capacity to transport 7 tons each, 3 wooden small boats without engine for emergency. The cooperative management has decided to pay boat-parking fees on monthly basis.Required:a. Calculate the monthly boat parking fees that should be paid by cooperative ABASAMBAZA.b. At which date should these fees be paid.3.9. Subscribing to tax system

Activity 3.9

Analyze the following extract from RRA regarding tax payment in Rwanda and answer questions that follow.Registration, taxpayer’s benefit and responsibility (Rwanda Revenue Authority)Cutting down the number of business informal sector is always identified as solid strategy and a way to establishing a secured and growing economy in any country. In this move, registering all businesses is the Government’s main focus in this financial 2014-15 year.In an entrepreneurship oriented state like Rwanda, registering a business is not only a law fulfillment; it’s also a way of enabling it to expand and blossom because businesses are widely encouraged and different incentives are given only to registered business people.Any person, who starts up a business or other income generating activities, is obliged to register with the tax administration within a period of seven days from the beginning of the business. Is also obliged to register for Value Added Tax (VAT) in seven days, any person who carries out taxable activities exceeding an annual turnover of twenty million Rwanda Francs (20,000,000 FRW), or five million Rwanda Francs (5,000,000 FRW) quarterly.Registration is done at any RRA Office, but when it comes to register a new business, a Taxpayer must also register it through the Rwanda Development Board (RDB) and get a registration certificate. In a bid to facilitate taxpayers, the RRA and RDB combined registration systems so that a Taxpayer Identification Number (TIN) can be issued at the same time of business registration at RDB. After registration at RDB, the taxpayer gets a Registration Certificate with a TIN referred to as the “company code” on the right-top side of the registration certificate.Business registration at RRA is free. In order to register, a businessman has to carry with him a copy of his Identity Card and one passport photo, and registration is done in five minutes.De-registration process has also been provided; this may happen in case for instance a Taxpayer decides to stop his business. In this case he first writes a letter to the Commissioner for Small and Medium Taxpayers or Commissioner for Large Taxpayers depending on the category of the taxpayer. The registration office analyse your de-registration request and if approved they call him/her to complete required de-registration procedures. A de-registering taxpayer will then be asked to file returns for the previous period: annual declaration (and payment if applicable) for Profit Tax and Monthly or Quarterly declaration (and payment if applicable) for VAT and Pay As You Earn. He will finally be requested to fill two de-registration forms and get them signed and stamped from the Tax administration. One copy will be kept by the Tax administration for Official use, and another one kept by the Taxpayer for personal record.Registration is also important because the law provides penalties to business persons who fail to register. Penalties vary from 100.000 to 500.000 Rwandan francs.Questions

a. In an entrepreneurship oriented state like Rwanda, registering a business is not only a law fulfilment. Why do you think it is beneficial to register a business in Rwanda?b. What are the obligations of any person, who starts up a business or other income generating activities in Rwanda?c. Briefly describe the process of subscribing or registering with RRAd. What are some of the basic documents involved in subscribing or registering with RRA?e. Briefly describe the process for a person/business who wants to de-register or stop subscription to RRA3.9.1. Conditions for subscribing to tax system include the following

a. Filling in the registration formAny person who sets up business or other activities that may be taxable is obliged to register within the Tax Administration within a period of 7days from the beginning of business activity.An individual or group of persons may own a company. Rwanda Development Board (RDB) does registration via online services. This service is immediate and free of charge. Company registration certificate is issued by RDB.Also for individual businesses, registration can be done by RRA and the Tax Identification Number (TIN) certificate is issued freely at countrywide spread RRA branches. There is an RRA office at all 30 districts in Rwanda. The law provides penalties to businesspersons who fail to register; such penalties vary from 100,000 to 500,000Rwandan francs.b. Legal form of the businessRegistering with the Rwanda Revenue Authorityi. Tax Identification Number (TIN):Within seven days of incorporation of a business, companies and individuals are required to register with the RRA to acquire a TIN. It takes 30 minutes to register and obtain a TIN.ii. Value Added Tax:Any company or individual that engages in business activities exceeding a turnover of 20,000,000Frwin a fiscal year or 5,000,000 Frw in the preceding calendar quarter is required by law to register for VAT with RRA within a period of seven days following the end of the year or from the end of the quarter mentioned above.However, any person/company who/which is not required to register for VAT by law may voluntarily register for it.c. Indicate all the type of taxes one owes to RRA: All taxpayers are expected to know all tax they will pay before starting business otherwise they are considered to make tax evasion; this will have direct impact on their business as sanctions and penalties.Documents

1. Certificate of registration (to be downloaded from RDB)2. Documents showing types of taxes (to be downloaded from RRA)3. His/her identification document:Requirements vary depending on whether the applicant is a physical person or a moral person.a. Physical persons (a person who has its own legal personality, that is an individual human being):•Photocopy of a national identity card/pass port•A passport size color photo;•A correctly filled application formb.Moral person/legal person, (which may be a private that is, business entity or non-governmental organization or public organization):•Correctly filled application form; these forms are available in two (2) languages, and taxpayers are encouraged to fill the form in the language they best understand in order to avoid errors;•Certified copy of a legal instrument of incorporation of the company/association;•Taxpayer Identification Number is required for shareholders if they are residents;3.9.2. Advantages of subscribing to tax system

•Take part in business: if the business is registered with RRA, this is an indication that it will operate smoothly in business industry;•Take part in national building: if the business is registered with RRA, it will highly contribute to the nation development through taxes paid;•Get certificate: if the business is registered with RRA, it is the security that it is recognized by the government and should operate as admitted one by complying with tax laws;•Getting loans: when you apply for loan, you are going to have to prove that you are actually have a business. Lenders and investors will ask to see your business registration along with other application requirements before approving you for a loan;•Reputation with customers: customers and clients, especially people you have never worked with before, need assurance that you are a legitimate business. A potential client may suspect your business of being a “fly-by-night” operation if your company is not properly registered.•Supplier arrangements: a registered business also makes you eligible to receive supplier discounts that you would not normally receive as an unregistered operation;•Hiring employees: a business registration allows you to hire-full time employees and pay them in accordance to state laws. When you register your business with the state, you will receive a state identification number that allows you to route state taxes on the employee’s behalf. Therefore, if you plan to hire employees to your business, it is best to take care of registering your business with the state before you even start the search for workers.Application Activity 3.9

Why is it important to register for taxes to the RRA?3.10. Sanctions/ penalties for not complying with tax obligation

Activity 3.10

What do you think may happen to an entrepreneur if he/she does not comply to the tax obligations?a. Penalties and Interest for not paying consumption tax•A taxpayer who fails to comply with the provisions of law determining and establishing consumption tax on some imported and locally manufactured products shall be liable to a fine.•Any taxpayer who fails to remit the tax due within the prescribed period is liable to a fine of five hundred (500) penalty units together with a late payment penalty of ten per cent (10%).b.Interest and fines for not paying fixed asset taxThe interests, fines and penalties have to be applied for the following cases:•In case of absence, late submission, or incomplete or misleading tax declaration:•10 % of the tax due, if the delay is less than one month;•20 % of the tax due, when the delay is not more than two months;•30% of the tax due, in case the delay is not more than three months;•40 % of the tax due, if the delay is more than three months.In case of incomplete, incorrect or fraudulent information with an intention of evading tax, the offender is subject to a fine of 20% of tax due for one year when it is the first time and 40% of tax due for one year if the offence is repeated. In case of late tax payments (law no 59/2011, article 25):•Interest of 1.5% per month calculated from the date the taxes are due up to the date they are paid. •Surcharge of 10% of the tax due. However, such a surcharge must not exceed an amount of 100,000 Frw.c. Interest and fines not paying rental taxThe interests, fines and penalties have to be applied for the following cases:In case of absence or late submission•10 % of the tax due, if the delay is less than one (1) month,•20 % of the tax due, if the delay is not more than two (2) months,•30 % of the tax due, if the delay is not more than three (3) months,•40% of the tax duel, if the delay is more than three (3) months.In case of incomplete, incorrect or fraudulent information with an intention of evading tax, the offender is subject to a fine of 20% of tax due of one (1) year when it is the first time and 40% of tax due of one (1) year if the offence is repeated.In case of late tax payments (law no 59/2011, article 25)•Interest of 1.5% per month calculated from the date the taxes are due up to the date they are paid.•Surcharge of 10% of the tax due. However, such a surcharge must not exceed an amount of 100,000 Frw.Any late declaration of zero (0) tariff shall cause the taxpayer be liable to a fine not exceeding five hundred (500) penalty units.d. Interest and fines for not paying trading licenseThe interests, fines and penalties have to be applied for the following cases:In case of absence, late submission, or incomplete or misleading tax declaration:•10 % of the tax due, if the delay is less than one month;•20 % of the tax due, when the delay is not more than two months;•30% of the tax due, in case the delay is not more than three months;•40 % of the tax due, if the delay is more than three months.In case of incomplete, incorrect or fraudulent information with an intention of evading tax, the offender is subject to a fine of 20% of tax due for one year when it is the first time and 40% of tax due for one year if the offence is repeated.In case of late tax payments (law no 59/2011, article 25):•Interest of 1.5% per month calculated from the date the taxes are due up to the date they are paid.•Surcharge of 10% of the tax due. However, such a surcharge must not exceed an amount of 100,000 Frw.If the taxpayer fails to present, the trading license tax certificate is punished by an administrative fine of 10,000 Frw.If a trading license tax certificate is lost or damaged, a duplicate shall be issued by the concerned decentralized entity for a fee not exceeding 5,000 Frw.e. Penalties and Interest on not paying PAYEInterestA taxpayer who fails to pay tax within the due date is required to pay interest on the amount of tax. Interest is calculated on a monthly basis at the inter-bank offered rate of the National Bank of Rwanda plus 2 (two) percentage points. For example, if the inter-bank rate is 9%, interest is imposed at 11% annually.f. Penalties and Interest for not withholding taxFailure to Withhold TaxA withholding agent who fails to withhold tax in accordance with law 25/2005 is personally liable to pay to the Tax Administration, as provided for by paragraph 2, Article 48 of this law, the amount of tax which has not been withheld including penalties and interest on arrears. However, the agent is entitled to recover this amount from the payee excluding the associated fines and the interest on arrears.g.Penalties and Interest for not paying VATValue Added Tax violations“The following administrative fines are imposed to persons who do not comply with provisions of Value Added Tax:•in the event of operation without VAT registration where VAT registration is required, fifty percent (50%) of the amount of VAT payable for the entire period of operation without VAT registration;•in the event of the incorrect issuance of a VAT invoice resulting in a decrease in the amount of VAT payable or in an increase of the VAT input credit or in the event of the failure to issue a VAT invoice, one hundred percent (100%) of the amount of VAT for the invoice or on the transaction;•for issuing of a VAT invoice by a person who is not registered for VAT is assessed a penalty of one hundred percent (100%) of the VAT which is indicated in that VAT invoice and is due to pay the VAT as indicated on that VAT invoice”.Tax fraud

“A taxpayer who commits fraud is subject to an administrative fine of one hundred percent (100%) of the evaded tax. With exception of that penalty, the Tax Administration refers the case to the Prosecution service if the taxpayer voluntarily evaded such tax, like use of false accounts, falsified documents or any other act punishable by law. In case of conviction, the taxpayer can be imprisoned for a period between six (6) months and two (2) years.Note: The Minister’s order determines an award given to any person who denounces a taxpayer who engages in tax fraud.•Closure of the business for 30 days;•Cancellation or withdrawal of registration certificate;•Fail to pay tax withheld: this undertakes 100% penalty and 3 months to 2 years in jail;•Obstructing or aiding: this undertakes fines and penalties equal to that of taxpayer;•Bar from public tenders;•Exposure in the mediaApplication Activity 3.10

1. Discuss why RRA charges fines and penalties?2. What do you think will happen if tax payers don’t pay both taxes assessed and fines/penalties?Skills Lab Activity 3.11

Justify the following statements with concrete examples:1. “Taxes are more of a benefit than a cost to an entrepreneur”2. “Avoiding paying taxes is a shortcut to business growth”End of Unit 3 Assessment

1. It is said that “tax is the free money to central or local authorities from taxpayers” do you agree with this statement. Justify your answer2. Explain different taxes vested to decentralized authority (District revenues)3. What is the role of EBM in Economic Development of Rwanda?4. Describe any four principles of tax5. How is tax used by government to;a. Support Entrepreneursb. Support the community6. Calculate the tax liability to be paid by a resident individual whose annual income is 45,000,000Frw. The employee is provided with furnished accommodation and a fueled car for the private use. The employee has two children attending school. The employer provides an education allowance of 7,200,000Frw per a year, paid on a monthly basis.7. Fill in the gap the following:a. ............. punishment is the jail for a period between six (6) months and two (2) years; even the Minister’s order determines an award given to any person who denounces a taxpayer who engages in that act.b. ............. is the compulsory and non-refundable payment made by the business to the Government or Local Authority so as to raise their revenues.c. ............. is the one that is exempted from VAT.d. ............. one of the taxes vested to the local government (Districts).e. The degree to which the taxpayers meet their tax obligations as set out in the appropriate legal and regulatory provisions is............................