Topic outline

UNIT 1: BUSINESS IDEAS AND OPPORTUNITIES

Key Unit Competency: To be able to generate business ideas and take advantage of opportunities

Introduction

Many people worlds over and Rwanda in particular are in constant search for ways and means of starting their own businesses or improving on the existing ones. Many are driven into this by various reasons such as developing a career, self-employment, solving other people’s problems or meeting their needs, among others. Such people usually ask themselves many questions like:

•Which business can I do?

•What business would be safe for me to do?

•Which business would I be interested in?•Will the business be profitable?

•Will the business be able to attract customers?

•Will I be able to cope with competition if I was to start such a business?

•How much money will I need to start the business and where will I get it from?

And so self-questioning and searching goes on and on.

This unit therefore, is designed to guide you answer the above questions and finding an appropriate business idea and opportunity. It will equip you with knowledge and skills as well as attitudes that will enable you to generate business ideas and take advantage of opportunities. Under this unit, you will learn how to generate business ideas, assess and rank them to select those that constitute business opportunities that you can later develop into businesses to realize your business goals.

Introductory activity

Rwanda has grown tremendously in the past years in terms of social, economic, political, and technological as well as in other aspects of life. Today, the Rwandan population is highly enterprising leading to a number of business activities being set up.Referring to figure 1.1above and using your previous knowledge of entrepreneur-ship, answer the questions below;a. What do you think has led to tremendous growth in all aspects of life in Rwanda?b. What factors have led to Rwandans being enterprising?c. Give some sources of business ideas that have led to Rwandans being enterprising.d. Not all business ideas are business opportunities. Is this statement true or false? Give reasons to justify your response.e. What should one do in order to take advantage of business opportunities available in his/her community?

Rwanda has grown tremendously in the past years in terms of social, economic, political, and technological as well as in other aspects of life. Today, the Rwandan population is highly enterprising leading to a number of business activities being set up.Referring to figure 1.1above and using your previous knowledge of entrepreneur-ship, answer the questions below;a. What do you think has led to tremendous growth in all aspects of life in Rwanda?b. What factors have led to Rwandans being enterprising?c. Give some sources of business ideas that have led to Rwandans being enterprising.d. Not all business ideas are business opportunities. Is this statement true or false? Give reasons to justify your response.e. What should one do in order to take advantage of business opportunities available in his/her community?1.1. Meaning of a business, a business idea and a business opportunity

Activity 1.1

Case study: A reality T.V. Show

Rwiyemeza is a prominent entrepreneur dealing in growing and processing of Mushrooms in Kicukiro district. One day she was invited to give an interview on Rwanda Broadcasting Agency (RBA) about her business to the whole nation by Mr. Makuru.

Rwiyemeza is a prominent entrepreneur dealing in growing and processing of Mushrooms in Kicukiro district. One day she was invited to give an interview on Rwanda Broadcasting Agency (RBA) about her business to the whole nation by Mr. Makuru.Read through the excerpts from the interview

Makuru: How did you decide to get into mushroom growing and processing? How did you start?Rwiyemeza: It was during the long senior six vacations after failing to get a job as I waited for my results. I basically got the idea after listening to the radio, reading newspapers, and watching TV about how different people have succeeded by starting their own business activities. Coupled with my secondary school entrepreneurship competences, I decided to give it a try and started with very many ideas of business activities I could start.It was not an easy task deciding on one activity but after doing enough research from various people, I finally settled for Mushroom growing and processing.Makuru: What was the biggest challenge while starting your business activity? How did you overcome it?Rwiyemeza: There were so many challenges such as competition, unsure market, lack of experience but deciding on turning my business idea into a profitable business was most challenging. I had to make a lot of research from existing entrepreneurs, Sector offices, and financial institutions. I also had to do personal evaluation.Makuru: What are the benefits of your business to the community?Rwiyemeza: Aaahhh......there are so many I can’t exhaust them.... but I will start with employment to me and my family which has improved our standards of living. I have 5 workers who earn a monthly salary, I pay taxes, my business helps to conserve the environment. Most importantly, I have inspired a lot of other young entrepreneurs especially women to start their own businesses.Makuru: What advice would you give to the young people who may want to start business activities?Rwiyemeza: My advice would be that all around us are opportunities of business ideas but one has to be careful because NOT all business ideas can become business opportunities and therefore turned into profitable businesses. Before I finally decided to start mushroom growing and processing, I had tried a number of businesses which failed because they were not viable. So, I again advise the young people that take time and study/research the business ideas before investing money because “Not all business ideas are business opportunities”.Referring to the case study (A reality T.V. Show) above, answer the following questionsa. What do you understand by business and what is Rwiyemeza’s business?b. Explain what you understand by a business idea. Mention any sources of business ideas for Rwiyemeza’s business activity.c. Rwiyemeza says it was not easy for her to start up the business activity. Explain what you understand by a business opportunity and identify some challenges Rwiyemeza faced.d. Why do you think it is very important to do a research and personal evaluation before deciding to start a business activity?e. Why do you think that it is important to generate business ideas?1.1.1. Meaning of business

Business means the production, distribution, and sale of goods and services for a profit. Business, then, is a combination of all these activities: for example, cars can be classified as goods, services, on the other hand, are activities that a person or group performs for another person or organization. For instance, an auto mechanic performs a service when s/he repairs a car. A business therefore, can also be described as an organization that provides goods and services for human needs.1.1.2 Rationale for Business

The simplest purpose of business is to solve a customer’s problem or meet the customers’ needs. By providing the goods and services that meet the customer’s needs, the business owner may realize profits (and at times may incur losses). Businesses exist to impact on people’s lives. This happens by businesses providing people with goods and services they desire to meet their needs. While the people buying the business’ products (goods and services) are meeting their needs, the business owners expect to realize profits. Businesses serve as conductors of economic activity and development.Business may be done by private individuals, government, companies, co-operatives or non-governmental organizations (popularly known as NGOs).

The simplest purpose of business is to solve a customer’s problem or meet the customers’ needs. By providing the goods and services that meet the customer’s needs, the business owner may realize profits (and at times may incur losses). Businesses exist to impact on people’s lives. This happens by businesses providing people with goods and services they desire to meet their needs. While the people buying the business’ products (goods and services) are meeting their needs, the business owners expect to realize profits. Businesses serve as conductors of economic activity and development.Business may be done by private individuals, government, companies, co-operatives or non-governmental organizations (popularly known as NGOs).1.1.3. Business idea and business opportunity

An idea is like a seed, an impression of a concept or a notion that revolves around seemingly successful product or service. A thought needs some amount of commercial validation before it shapes itself into an opportunity. Opportunity is the care and nurturing that a gardener has to endeavor for to turn the seed into a seedling and then allow it to grow into a tall tree. The gardener ensures that it gets good soil, sunshine, proper environment and protection from harsh rains or weather conditions.A business idea may not necessarily be a business opportunity; one needs to filter and sift through these ideas to realize whether they are real opportunities. Most of the times, these ideas remain dormant because of the lack of courage, resources for example time and money or mere inability to take action. In addition, those who show courage to take action generally see their dreams go off track due to lack of farsighted vision or lack of preparedness. The business owner must own the responsibility of its success or failure regardless of the circumstances. Successful entrepreneurs are good at turning ideas into opportunities, they execute to make it all happen. It takes time, resources and hard work.

Meaning of a business Idea

A business idea can be referred to as the response of a person or persons, or an organization to solve an identified problem or to meet perceived needs, realize fantasies or dreams, improving on existing situations or products, etc.Finding or generating a good business idea is the first step towards transforming the entrepreneur’s desire and creativity into a business opportunity. Essentially, entrepreneurs need ideas to start and grow their entrepreneurial ventures. Generating ideas is an innovative and creative process.Meaning of a business opportunity

An opportunity is a favorable set of circumstances that creates a need for a new product, service, or business. A business opportunity can be defined as an attractive business idea worth investing in or propositions that provide the possibility of a monetary return for the person implementing them or taking the risk of investing in them. Such opportunities are determined by customer requirements and lead to the provision of a product or service which creates or adds value for its buyers or end-users.Application Activity 1.1

As a student of entrepreneurship, come up with ideas that may result into opportunities for you to start business activities to solve identified situations in your community below.a. Lack of sufficient safe water in your community.b. High demand for charcoal as source of energy in your community.c. Increased pollution due to increased disposal of wastes in your community.1.2. Characteristics/Qualities of business ideas and business opportunities

Activity 1.2

Think about people in your community who have started business activities. Have they all been successful? Give reasons to support your response.a. Why do entrepreneurs have to generate business ideas and opportunities?b. What do you think should make a good business idea?c. What do you think should make a good business opportunity?d. Think about people in your community who have started business activities. Have they all been successful? Give reasons to support your response.1.2.1. Why generate business ideas

There are many reasons why entrepreneurs would need to generate business ideas. Some include:•You need an idea: A good idea is essential for a successful business venture – both when starting a business and to stay competitive afterwards•Respond to the market needs: Markets are made up essentially of customers who have needs and wants waiting to be satisfied•Changing fashions and requirements: Provide opportunities for entrepreneurs to respond to demand with new ideas, products and services•To stay ahead of the competition: Remember, if you do not come up with new ideas, products and services, a competitor will. So the challenge is to be different or better than others•To exploit technology – do things better: Technology has become a major competitive tool in today’s markets and for one to be better with changing technology, generation of business ideas is crucial.•Because of product life cycle: All products have a finite life. The firm’s prosperity and growth depends on its ability to introduce new products and to manage their growth•To spread risk and allow for failure: It is necessary for firms to try to spread their risk and allow for failures that may occur from time to time by constantly generating new ideas.Good entrepreneurial business ideas should be:a. Market driven•Solve a problem•Find a market need•Customer focused not product driven•Targets an identified sizeable market segmentb.Feasible•Attractive –there is a demand•Achievable –it can be done•Durable –it lasts•Value creating –it is worth something•Safe•Affordablec. Unique•Faster/Better/Cheaper•Differentiated (commodity)•They have a “Special Sauce”d. Fundable•Having a consistent Revenue stream•Manageable risk•Sustainable -Market exists with frequency of purchase•Scalable or Replicable•Barriers to entry•Growth potential•Product pipeline•Exit plan•Innovative1.2.2. Reasons for generating business ideas

There are many reasons why entrepreneurs would need to generate business ideas.A good idea is essential for a successful business venture both when starting a business and to stay competitive afterwards. Some of these reasons include;•To respond to market needs: markets are made up essentially of customers who have needs and wants waiting to be satisfied.•Changing fashions and requirements: provide opportunities for entrepreneurs to respond to demand with new ideas, products and services.•To stay ahead of the competition: Remember, if you do not come up with new ideas, products and services, a competitor will. So the challenge is to be different or better than others.•To exploit technology(do things better): Technology has become a major competitive tool in today’s markets and for one to be better with changing technology, generation of business ideas is crucial.•Because of product life cycle: All products have a finite life. The firm’s prosperity and growth depends on its ability to introduce new products and to manage their growth.•To spread risk and minimize failure: It is necessary for firms to try to spread their risk and minimize failures that may occur from time to time by constantly generating new ideas.Good business opportunities should be represented by customers’ requirements and lead to the provision of the goods or service that satisfies the customers (creates or adds value for the buyers or end user).A good business opportunity must be carefully examined and should fulfill the following criteria:•Real demand should exist for the products to be produced.•Favorable return on the investment made.•Be able to favorably compete in the market (competitive).•Should meet the investors many objectives.•There should be availability of resources necessary for the investment.Application Activity 1.2

Analyze the extract below and answer questions that followIn ‘tech’, there is an old saying, “an idea before its time is worse than a bad idea.”(Adapted from:https://www.forbes.com/sites/quora/2017/06/21/these-seven-startups-had-amazing-ideas-and-failed/#767f7914613e)a. What does the above extract mean to you regarding business ideas and opportunities?b. What should one do to avoid the situation in the extractiv1.1.3. Sources of good business ideas and opportunities

Activity 1.3

a. Referring to your community, give at least 3 examples of people or firms that have come up with good business ideas, and explain why you consider these ideas being good.b. Suggest any five (5) ways in which people in your community generate business ideas.c. Briefly explain any sources of business ideas and opportunities in Rwanda.1.3.1. How to generate business ideas (Techniques of generating business ideas)

Where do you find new business ideas? In your own head! Of course, you can buy an existing business. But you could also find more exciting business ideas by looking around yourself, your community, country and the world to find out what needs to be fixed, what can improve on the existing situations, what is more exciting, what eases or saves people’s lives, what can take advantage of existing or future situations, etc. Entrepreneurs can generate business ideas through any of the following ways.a. Define the Problem. Any problem, challenge or unmet customer needs and gaps need to be solved or a solution found. By thinking about different ways of solving or meeting the customer needs results into business ideas. Therefore, to generate business ideas, one needs to first define the problem and then look for ways to solve it.b.Brainstorming: This is where a group of potential entrepreneurs get together to think and generate a list of solutions to challenges or ideas to solve unmet customer needs. As the group members think and mention the ideas that they have come up with, it is written down.c. Look at parallel problems and solutions: Relate your current problem to the one that you had in the past and check for parallels between the two. The way that earlier problems were solved can assist you greatly in generating ideas to solve subsequent and current situations.d. Look at each task as a challenge: It’s true that if you look at a problem simply as a “problem” then that is exactly how many will look at it. Sure it is a problem, and therefore, it needs a solution. Coming up with solutions to solve the problem or challenge will result into business ideas to that particular challenge.e. Daydreaming: Most people while undertaking their daily duties have their subconscious continue working (day dreaming). List your dreams. What have you always wished to do? Write them down. Then look for a way to turn these ideas into practical activities that have social, cultural or economic value for which someone out there could or may be willing to pay for.f. Carry a notepad: Always have a notepad with you. Make it a habit not to live without it. Write down any interesting idea your mind comes up with in response to every situation you may be faced with or environment you find yourself in. Capture and preserve your ideas for later use when you truly want them.g.List customers’ complaints: How many times have you complained about a bad service, poor or wrong timing hours, limitations of a product you have purchased, etc? If your complaint is not unique, then you have just found an area where you could help meet a need. For example, if you were searching for a good or service on the weekend, and the store or Service Company was closed, couldn’t you capitalize on that by offering expanded hours?h. Read. Read: Read virtually every newspaper, business magazine, marketing periodicals, entrepreneurship bulletins, etc that you can find. You may not get a winning idea from each issue, but always learn something new that you can use at a later date. The more information your mind has stored away, the greater the opportunity for creativity.Every time you read about an entrepreneur who is making it on his or her own, you should be processing the data from your mind on why such an entrepreneur is successful.i. Tap your interests: Thousands of clever people have taken up hobbies and turned them into successful businesses. Unfortunately, a number of people never consider it as an important piece of work when they are doing something they love.j. Travel: Traveling opens your eyes and increases the chances for you to generate business ideas. You will for example benefit greatly if you visit well known entrepreneurs or people so that you can listen to their experiences.k. Keep your eyes open: When you see something that attracts your interest, ask yourself; what is it about this situation that is special? Then narrow your focus, so that you keep an idea that could be useful at some time later. The process of zeroing in on an idea often spawns important niche markets.l. Library or internet Research: Libraries and internet are often the underutilized sources of information for generating business ideas. The best approach is to talk to the librarian who can point out useful resources, such as industry (specific magazines, trade journals, industry reports), etc. Simply browsing through several issues of trade journals or an industry reports on a specific topic can spark new ideas.1.3.2.Sources of business ideas

•Personal interest in searching for new things/Hobbies.•Franchises (improving upon an existing idea).•Mass media (newspapers, magazines, TV, Internet).•Business exhibitions.•Surveys.•Customer needs, advice, complaints, preferences, wishes, etc.•Changes in society.•Brainstorming.•Being creative .•Prior jobs.•Seeing a need or a gap in the marketplace.•Using skills as foundation for a business.Application Activity 1.3

1. Read the following and answer as requireda. Generating business ideas from existing businesses: By reflecting on the entrepreneurs from your community; list the business activities that they are performing. Using the listed business activities, think and come up with your own business ideas.b.Generating business ideas from the available information: Take time to read newspapers, books or magazines, listening to the radio, watching television or search the internet. From whatever you have read, heard, watched or seen, generate and write business ideas in your note books.c. Generating business ideas from existing products: Analyze samples of existing products (e.g. 2 or 3 products) from your community and come up with a list of new products you think that you could make using these products (for example by improving on them, changing their uses, etc). As you think and propose the new products, be guided by their possible applications either at present or in the future.d. Totally new business ideas: Think and come up with business ideas that can satisfy or help your group achieve its dream. Present your group report to the rest of the class for discussion.e. Business ideas based on the learners’ community needs: Visit your community to observe or investigate about its existing un-served needs, future needs and dissatisfactions that they have and list them. Generate business ideas based on your findings from the community.f. Business Ideas based on existing local resources: Visit your community to observe or investigate about the existing local resources and list them. Then, discuss and generate business ideas that will make use of the existing local resources.g.Situations: Identify different real life situations (e.g. back to school days, festive seasons, weddings functions, political campaigns, road junctions, border crossing points, rainy or sunny days, etc). Based on 3 or 4 situations of your choice, generate business ideas that can take advantage of them.2. Why do you have to pay attention to issues such as gender, environment, peace among others while generating business ideas and opportunities from the different sources?1.4. Factors influencing choice of a business opportunity

Activity 1.4

In senior one, unit 4: Concept of needs, wants, goods and Services and Senior two unit 4: Markets, you studied the different forms of enterprises and the impact of the different types of markets. After graduating, you may want to start a business activity.Referring to application activity 1.3, chose one business opportunity you may decide to start and give reasons for your choice.Some factors considered while choosing of a business opportunity

Most people have been looking for new business ideas since childhood. In their early years, they have started and tried a number of business activities such as rearing small animals, selling airtime cards, selling bakery products, among others where they have made many wrong mistakes. As they grow older (and wiser), they have learned to screen and evaluate opportunities more effectively before investing in them. Different people will have different criteria depending on things like risk tolerance, career goals, budget, inheritance, etc. Below are some factors to consider when deciding what business opportunity to pursue.1. Identified market need or gap: The nature of the identified need or challenge in the market or customer need will influence an entrepreneur’s choice of a business idea. A person is likely to choose an opportunity which he/she thinks will solve the identified market needs.2. Growing market: Most people do not want to avoid the hustles of starting a new business. So, they will choose ideas or opportunities that are easy for them to start their businesses while others may choose ideas that gives them a chance to be creative.3. Low funding requirements: The amount of funding required to implement a business opportunity may influence one’s choice of a business idea. Most people will choose opportunities that do not involve a lot of funding in relation to profits.4. Vision or goals: The choice of a business opportunity will greatly depend on the vision or goals of the entrepreneur. These could be short term or long term goals.5. High profit margins: Of course, on every entrepreneur’s mind is profit. The profit margin expected from the opportunity will greatly influence one’s choice.6. Not easily copied: Every entrepreneur of course wants to protect their ideas, protect intellectual property and developing a brand reputation. So entrepreneurs are likely to choose ideas/opportunities that cannot be easily duplicated in the market at least in the short run.7. Inheritance: Inheritance is the practice of passing on properties, rights, and obligations upon the death of an individual. Most people would prefer continuing in the line of family business than going for new business opportunities.8. Skill set required: If the skill set required to execute the opportunity counts to the survival of the business, then execution risk should be less. Therefore, most entrepreneurs would go for opportunities that are in line with their skill set or experience. This may also go as far as the human resources requirements are concerned.Application Activity 1.4

Around your neighborhood there are many business activities taking place. Identify any 3 of them and give reasons why you think the owners chose those activities over others.1.5. Evaluating Business Ideas

Activity 1.5

There are plenty of opportunities out there in your community; it is just a matter of choosing which one is best. Many young entrepreneurs have burning ideas and visions for the future. Everyone’s personal criteria and factors will probably be different depending on their goals. Using prior knowledge on entrepreneurship and researching in different entrepreneurship books, identify at least five factors that can be considered while evaluating business ideas.Factors to consider when evaluating viable business idea and opportunities

It is very important to examine your business idea and determine your potential for success before you spend time and money developing a business plan. If you want to start a business, you will need to think carefully about your business idea. Is it a great idea that could turn into a major brand or will it fall flat at the start line?Entrepreneur needs to determine whether the business idea they have in mind is viable or not. When evaluating the viability of the business opportunity, the following factors need to be taken into consideration:a. Potential for growth: An opportunity is said to be viable, when it has the ability to grow and expand.b.Infrastructure: Easy access to infrastructure such as roads, water, electricity, telephone and postal services among others enables business enterprises to easily make orders for goods and deliver them hence reducing operating expenses. With low operating expenses, profits can be maximized.c. Market for the goods and services: An entrepreneur has to assess potential and actual market for the goods and services he or she would like to sell. There must be a clearly defined market if the opportunity is to be considered.d. Rewarding to the investor: The opportunity should be rewarding to the investor (cost-benefit consideration). He should consider the expected returns against the expected cost to ensure that the benefits outweigh the cost.e. Price structure: One has to put into consideration the price-structure of the goods and services he would like to offer. Goods and services, which are subjected to constant inflation, are likely to change in terms of price.f. Competition and Competitive advantage: Competition is regarded as a threat to business of similar kinds operating in a similar location. Although competition is a threat, it is healthy in the sense that it goes along the way in controlling price of goods offered. It is crucial for entrepreneurs therefore to consider opportunities where competition is not high as this will enable them to get reasonable market share. They should venture where competitive advantage is.g.Incentives: Offered by the government and Non-Governmental Organizations, incentives are legitimate business opportunities to exploit as they save on costs. E.g. duty free importation of sugar and maize, tax waivers, etc.h. Legal Consideration: The new idea should be in line with the legal regulatory framework e.g. an idea to sell drugs may not be viable because it is illegal.i. Financial viability: The assessment of financial viability is of significant importance when looking at the viability of the business. Capital investment requirements, break even analysis, cash flow projections, profitability of the business have to be analyzed. This is because they determine the sustenance of the business in the market-mix.j. Personnel, Training and Management: Before starting a business, it is necessary to make an assessment of the required personnel training and management. Look at the ability, cost of hiring and training human resource. Management efficiency will enable the business to succeed.Application Activity 1.5

Analyze the photo below and answer questions that follow;

Questions

a. What kind of activity is represented in the photo?b. What are the effects of such business ideas to the community?c. As an entrepreneur, suggest any two business ideas you may generate in response to the effects of the activity above.d. Picking one idea, give the factors you will base on while choosing that idea.e. What advice would you give to potential entrepreneurs while generating business ideas in relation to the photo above?1.6. Evaluating business opportunities using the SWOT Analysis

Activity 1.6

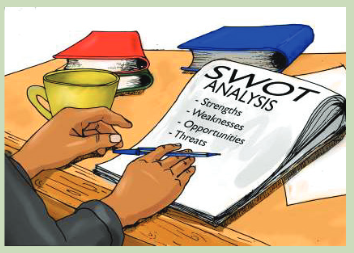

1. Refer to the above figure and explain what the following terms may mean in relation to identifying and evaluating business opportunities:a. Strengths.b. Opportunities.c. Weaknesses.d. Threats.2. Identify one successful business in your community and a. Briefly describe the factors or things you think favored its growth.b. Briefly describe the factors or things you think might affect its growth.

1. Refer to the above figure and explain what the following terms may mean in relation to identifying and evaluating business opportunities:a. Strengths.b. Opportunities.c. Weaknesses.d. Threats.2. Identify one successful business in your community and a. Briefly describe the factors or things you think favored its growth.b. Briefly describe the factors or things you think might affect its growth.1.6.1. Meaning of SWOT Analysis

As an entrepreneur, you want to know your business inside and out so you can make informed and moneymaking decisions. To do that, a SWOT analysis is the key. By conducting a SWOT analysis, you will have a comprehensive look at your company’s strengths, weaknesses, opportunities, and threats (which is what the acronym SWOT stands for).A SWOT analysis encourages owners to evaluate their businesses, looking specifically at strengths, weaknesses, opportunities, and threats that surround the company.A SWOT analysis is an analytical tool that can be used by the entrepreneur to check his/her business/product strength and weakness, opportunities and threats and to compare them with his/her competitors and therefore determine whether his/her business is in better position to compete or not.1.6.2. The purpose of SWOT

For existing businesses, a SWOT report will:•Give you a new perspective about your business.•Provide valuable information that can be used to make strategic decisions.•Allow you to assess the health of your business in real time.•Identify areas for improvement.•Give employees a chance to weigh the overall wellness of the business.•Guide future plans.For new businesses, a SWOT report will:•Highlight the benefits of your proposed business.•Identify potential problems.•Encourage you to think critically about starting a business.•Provide valuable information that you’ll need to consider now and in the future.SWOT stands for:Strengths refer to the positive internal factors a business can draw from to accomplish its goals and objectives. For example:•Skilled and motivated staff.•Modern equipment.•High quality products.•Customer friendly but profitable prices.•Ability of the product to meet customers’ needs and preferences.•Efficiency at serving customers.•Good business location.•Good and trained marketing staff.•High and effective brand name, design, trademarks, packaging, etc.•Efficient advertising and product promotion terms and strategies.•Enough capitalTips to maintain your company’s strengths;•Be truthful: It probably goes without saying, that if you’re not truthful during this process, the entire analysis won’t be effective.•Allow for feedback: As you’re brainstorming strengths, make sure your employees are comfortable offering their feedback. You may not agree on some strength, but it’s best to talk to them through.•Stay focused: You want to hear many viewpoints, but when you get several people in a room, time can get away from you. Keep the group on task.•Keep your list of strengths handy: Keep your list in an accessible spot. You’ll analyze all of the data that you collect over the next few days at the end of the week.Weaknesses refer tothe negative internal factors that inhibit a business’ ability to accomplish its goals and objectives. For example:•Being new in the market.•Weak marketing image and distribution image.•Narrow product line; location of selling points not convenient or accessible to customers.•Inability to finance needed marketing changes.•High overall unit cost compared to the key competitors.•Marketing skills that are poor or below average.Tips to identify your business’ weaknesses•Be open-minded: As your employees suggest weaknesses, remain open-minded. It’s likely that an employee will bring up a weakness that you hadn’t thought of, or disagree with. When it happens, don’t be judgmental.•Be critical of your business: Now isn’t the time for rose-colored glasses, now is the time for pure honesty. Be prepared to look at your business inside and out critically.•Remember, every business has weaknesses: When you’re finished talking about the negative aspects of your business, you might feel a bit deflated. Remember, every business has weaknesses. Today is just part of a larger process that will help you better access your business.•Keep your list of weaknesses handy: Keep your list in an accessible spot. You’ll analyze all of the data that you collect over the next few days at the end of the week.Opportunities refer to the positive external factors that a business can exploit to accomplish its goals and objectives. For example;•Possibilities of landing big orders say from government or big institutions.•Sudden shift in tastes and preferences of consumers in favour of your products.•Market trend changes due to new development like a school or large business in the area.•Faster market growth.•Falling or removal of trade barriers in attractive markets whether foreign or domestic.Tips to exploit your business’ opportunities•Do your research: Finding answers to some of these questions might require some digging. Don’t be afraid to make some calls, set up meetings, and do some market research to gauge upcoming changes.•Be creative: To find an opportunity where your competitors cannot will take skill and creativity. Don’t be afraid to think outside the box when you’re listing possible opportunities.•Keep your list of opportunities handy: We’ll add to your SWOT analysis tomorrow, so keep your list of opportunities in a safe spot.Threats refer to the negative external factors that inhibit a business’ ability to accomplish its goals and objectives. For example•Competitors reducing their prices.•New businesses getting started.•Entry of lower cost foreign competitors into the market.•Changing tastes and preferences of consumers.•Negative population changes/demographic changes.•Sudden negative change in government policies.•Negative shift in forex rates and trade policies.•Rising sales of substitute goods.•Declining availability of raw materials for the product.Tips to identify and manage threats•Do market research: As you’re looking into possible threats, you will want to conduct market research to see how your target audience is shifting.•List every threat you can think of: If you think of a threat, list it. Even if that threat has consequences that won’t be felt immediately, it’s still better to have it on your radar.•Threats exist, don’t panic: Listing threats may cause some anxiety, but remember that all businesses have threats. It’s better to know about threats than it is to turn a blind eye to them.Application Activity 1.6

Analyze the case study below and after answer questions that follow.Case study: KGF Breweries

KGF Breweries is a medium-scale brewery that is located in the growing indus-trial center of Kigali, Rwanda. This is a relatively new business in its start-up phase having been incorporated recently.We are on the brink of penetrating a lucrative market in a rapidly growing econ-omy. The current trend towards an increase in the number of entrepreneurs and competition amongst existing companies presents an opportunity for KGF Breweries to penetrate the market. Our products will be positioned very care-fully. They will be of extremely high quality to ensure customer satisfaction, supported by impeccable service to our customers. Our primary goal will be to establish and strengthen our license to trade, which will be bestowed by the communities in which we function.As KGF Breweries prospers and grows, these communities will continue to ben-efit from both the value created by KGF Breweries and its behavior as a corpo-rate citizen.We are in a highly lucrative market in a rapidly growing economy. We foresee our strengths as the ability to respond quickly to what the market dictates and to provide quality brew in a growing market. In addition, through aggressive marketing and quality management we intend to become a well-respected and known entity in our respective industry. Our key personnel have a wide and thorough knowledge of the local manufacturing market and expertise, which will go towards penetrating the market. However, we acknowledge our weakness of a medium-sized company without a lot of experience, and the threat of new competition taking aim at our niche.a. Describe all the potential opportunities or positive factors that may favour the growth of KGF Breweries.b. Describe all the potential areas of weakness or limitations to the growth of KGF.c. Describe the likely effects of KGF on the community in general.d. Suggest possible strategies KGF may apply to regulate the effects on the community.Skills Lab Activity 1.7

For the business you intend to start at home or for the products that already ex-ist in the club or at home, how will you improve or add value to them? Answer the following questions to explain the above.1. Relevance of the product or project to the community.a. What new or improved product are you making?b. What additional attributes will the product have?c. Explain how the product will be able to solve community problems.2. Increasing production.a. What will be production goal for the year?b. What strategies will you implement to have more output?c. How will you be managing produce (output produced?3. Making the product competitive.a. What will be the sales goal for the year?b. What strategies will be implemented to have a competitive advantage over other businesses in the community?c. How will the mentioned strategies above be implemented.4. Reducing negative effects on the environment.a. Why is it necessary for the clubs at school to be responsible with the environment?b. What measures will you put in place to reduce environmental hazards as a result of club activities?5. Recruitment more customersa. Discuss different strategies that you will employ to have more customers for your product.b. What measures will be put in place to maintain the clients?End of Unit 1 Assessment

1. “Not all business ideas are business opportunities” What does this statement mean to you?2. Referring to your community,i. Identify any one unmet customer need.ii. Generate any three solutions to the unmet customer need identified above.iii. Choose one idea that you think may be turned into a profitable business, and give reasons to support your choice.3. Analyze the picture below and answer questions that follow. i. What is the problem in the picture above?ii. What are the effects of such situations to the community?iii. Suppose this was in your area, generate any 3 business ideas in response to the situation aboveiv. Use the SWOT analysis to evaluate any one business idea generated above (iii) for potential businessFiles: 2

i. What is the problem in the picture above?ii. What are the effects of such situations to the community?iii. Suppose this was in your area, generate any 3 business ideas in response to the situation aboveiv. Use the SWOT analysis to evaluate any one business idea generated above (iii) for potential businessFiles: 2UNIT 2: CONTRACTS IN BUSINESS OPERATIONS

Key Unit Competency: To be able to make a valid contract and resolve conflicts in business operations

Introduction

The business environment is full of agreements between businesses and individuals. While oral agreements can be used, most businesses use formal written contracts when engaging in operations. Written contracts provide individuals and businesses with a legal document stating the expectations of both parties and how negative situations will be resolved. Contracts also are legally enforceable in a court of law. Contracts often represent a tool that businesses use to safeguard their resources.

This unit is designed to equip you with knowledge and skills as well as attitudes that will enable you to: make personal and business contracts, handle conflicts in life and business, respect agreements with other people and seek for the appropriate institutions for conflict and dispute resolution.

Introductory activity

Referring to laws in business operations and role of standards in business covered in S4, answer the following questions:

a. What is the importance of laws in business operations?

b. What is the importance of standards in business operations?

c. What do you think is a business contract?

d. Your friend met with a businessperson on a football match who requested her to supply him with beans at a price agreed on from there among the two of them. After delivering 200kgs, she was not paid the full amount of money she had been promised by the businessperson.

i. Has such a situation ever happened to you? When and what happened?

ii. What do you think was the mistake your friend did? What should she have done?

iii. How do we call such a situation?

iv. Advise your friend what to do so as to be fully paid her money.

v. What lessons do you learn from the above situation?

2.1. Business contracts: Meaning and Forms of Business contracts

Activity 2.1

Read the following paragraph and answer questions that follow.

Musabe is operating a micro enterprise in her local home area of Musanze. She wants Mugisha to supply her goods for her business. Musabe says Mugisha can start right away to supply the goods they will discuss other issues later on BUT Mugisha insists he needs an agreement between the two especially on issues such as payment terms, delivery period, quantity and quality, among others.

a. How do you call the agreement Mugisha insists should be between them?

b. Do you think Mugisha is right to have the agreement before starting the supply of goods? Give reasons to support your answer.

c. In which form may the agreement be made between Musabe and Mugisha? Support your answerd. What do you understand by:e. Contract.

f. Business Contract.

2.1.1. Meaning of contract and Business contract

A business contract is a legally binding agreement between two or more persons/businesses to perform an agreed business transaction. It is a legally binding agreement between two or more persons or entities.Dealing with contracts is part of running a successful business. You will have a number of business relationships involving some type of contractual commitment or obligation.You may:•Be a purchaser of goods and services - as a borrower of money, in rental agreements and franchise agreements•Be a supplier of goods and services – retailer, wholesaler, independent contractor•Have a partnering agreement with other businesses – partnerships, joint ventures, and consortium.Note: •Managing your contracts and business relationships is very important.•It is important that you fully understand the terms of a contract before signing anything. You are advised to seek legal and professional advice first.

A business contract is a legally binding agreement between two or more persons/businesses to perform an agreed business transaction. It is a legally binding agreement between two or more persons or entities.Dealing with contracts is part of running a successful business. You will have a number of business relationships involving some type of contractual commitment or obligation.You may:•Be a purchaser of goods and services - as a borrower of money, in rental agreements and franchise agreements•Be a supplier of goods and services – retailer, wholesaler, independent contractor•Have a partnering agreement with other businesses – partnerships, joint ventures, and consortium.Note: •Managing your contracts and business relationships is very important.•It is important that you fully understand the terms of a contract before signing anything. You are advised to seek legal and professional advice first.2.1.2. Forms of business contracts

A business contract states the terms and conditions of any business transaction, including product sales and delivery of services. This helps the parties involved to avoid any type of misunderstanding that may arise in the absence of a written contract.If you are collaborating with a friend on your new business, then it is all more important to create a written contract. This will help you avoid any misunderstandings and consequently will save you from the rifts that might end your friendship.If you have an oral agreement, you might forget some points that you have agreed on verbally with the passage of time. However, with a written agreement, all the terms and conditions are clear at any point in time. Moreover, you can always amend the agreement with the consent of both the parties.Contracts can be verbal (spoken), written or a combination of both. Some types of contract such as those for buying or selling real estate or finance agreements must be in writing.Written contracts: This refers to the agreement between two or more parties in form of written words for example a property selling agreement, may consist of a standard form of agreement or a letter confirming the agreement.Oral/Verbal agreements (gentleman’s contract): These are agreements made between two or more parties by word of mouth or orally for example, telling the person to plough your piece of land without any written note, it relies on the good faith of all parties and can be difficult to prove.It is advisable (where possible) to make sure your business arrangements are in writing, to avoid problems when trying to prove a contract existed.Regardless of whether the contract is verbal or written, it must contain four essential elements to be legally binding.Application Activity 2.1

Read the following statements and answer questions that followNkusi wants to lend his car to Niragire for 5,000Frw per day for five days.a. Niragire agrees with a handshake to borrow the car from Nkusi and pay the money in witness of Rukundo.b. Ntezimana promises to take his girlfriend Bagirishya for an outing to Lake Kivu.c. Niyokwizerwa promises to pay 10,000Frw to whoever finds her lost phone.d. Kato puts on paper his commitment to provide printing services to Umutoni on agreed terms.e. Mutesi promises to pay for her brother’s school fees and puts it in writing.Questions:

Which of the above statements are:i. Contracts.ii. Not contracts.iii. Business contracts.iv. Verbal contracts.v. Written contracts.2.2. Elements of a written contract and a valid contract

Activity 2.2

Analyze the sample contract below and answer questions that follow

Questions

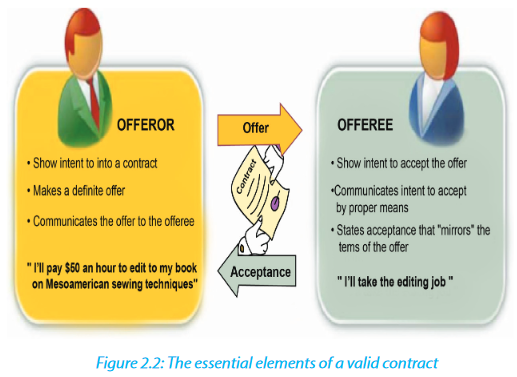

a. Do you think the above sample is a contract? Give reasons to support your answer.b. Name the elements of the written contract above.c. Do you think the sample above is a valid contract? Support your response by mentioning the elements of a valid contract in the sample.2.2.1. Elements of a written contract

Written contracts may follow a structure that can include, but are not limited to, the following elements:•Details of the parties to the contract, including any sub-contracting arrangements•Duration or period of the contract•Definitions of key terms used within the contract.•A description of the goods and/or services that your business will receive or provide, including key deliverables.•Payment details and dates, including whether interest will be applied to late payments.•Key dates and milestones.•Required insurance and indemnity provisions.•Guarantee provisions, including director’s guarantees.•Damages or penalty provisions.•Renegotiation or renewal options•Complaints and dispute resolution process.•Termination conditions.•Special conditions.2.2.2. Essential elements of a valid contract

Contracts can be verbal (spoken), written or a combination of both. Some types of contract such as those for buying or selling real estate or finance agreements must be in writing.Regardless of whether the contract is verbal or written, it must contain the following essential elements to be legally binding:a. Intention to be bound by the contract: The two parties should have intended that their agreement be legal. Domestic agreements between husband and wife are not taken as valid.b.Offer and acceptance: There must be an offer and the two parties must lawfully come to acceptance leading to a valid contract. Until an offer is accepted, it’s not a valid contract.c. Consideration/price: This is the price agreed upon by the parties to the contract and paid by one party for the benefit received or promise of the other parties.d. Capacity of the parties: The parties to the contract must have contractual capacity for the contract to be valid, i.e. should be sober, above 18years old, not bankrupt, not insane, properly registered.e. Free Consent: Parties to the contract must agree freely without any of the parties being forced to accept or enter the contract.f. Legality/lawful object: The consideration/object of the contract must be legal and not contrary to the law and public policy.g.Possibility of performance: If the contract is impossible in itself either physically or legally, then such contract is not valid and cannot be enforced by law.h. Certainty: The terms of the contract must be clear and understandable for a contract to be valid. If the terms are vague or ambiguous, where even the court may be able to tell what the parties agreed, then it will be declared invalid.

Contracts can be verbal (spoken), written or a combination of both. Some types of contract such as those for buying or selling real estate or finance agreements must be in writing.Regardless of whether the contract is verbal or written, it must contain the following essential elements to be legally binding:a. Intention to be bound by the contract: The two parties should have intended that their agreement be legal. Domestic agreements between husband and wife are not taken as valid.b.Offer and acceptance: There must be an offer and the two parties must lawfully come to acceptance leading to a valid contract. Until an offer is accepted, it’s not a valid contract.c. Consideration/price: This is the price agreed upon by the parties to the contract and paid by one party for the benefit received or promise of the other parties.d. Capacity of the parties: The parties to the contract must have contractual capacity for the contract to be valid, i.e. should be sober, above 18years old, not bankrupt, not insane, properly registered.e. Free Consent: Parties to the contract must agree freely without any of the parties being forced to accept or enter the contract.f. Legality/lawful object: The consideration/object of the contract must be legal and not contrary to the law and public policy.g.Possibility of performance: If the contract is impossible in itself either physically or legally, then such contract is not valid and cannot be enforced by law.h. Certainty: The terms of the contract must be clear and understandable for a contract to be valid. If the terms are vague or ambiguous, where even the court may be able to tell what the parties agreed, then it will be declared invalid.Application Activity 2.2

Assume, you have rental houses at home; Help your parents design a rent-alcontract that will be signed with the tenants. (Refer to elements of written contract)2.3. Importance and termination of business contracts

If you run a business, your business depends on all kinds of relationships: With customers or clients; with employees; with vendors of goods and services; with lenders and property owners, just to name a few. Each party to a business relationship brings to it a set of expectations with respect to what he or she will give and get. A contract is a useful tool for describing and defining the expectations of each party to a business relationship.Activity 2.3

1. Referring to the activities in the previous lessons, do you think it is important to have contracts in business operations? Give reasons to support your answer.2. Referring to the Contract for the sale of used car in activity 2 above, what do you think or when do you think the contract may end?3. What do you understand by termination of business contract?2.3.1. Importance of business contracts

A written contract plays a vital role in any business transaction. Apart from making the agreement between concerned parties legally binding, contracts can also serve as future references, part of the business’ policies, as well serve as proof in the event of misunderstandings, complaints or disputes needing litigation proceedings.Entrepreneurs sign many contracts with suppliers, financiers, workers, customers, transporters and government. A contract is important in the following ways:•Contracts reduce business risks by compelling business partners to perform what they have agreed to as per contract.•Business contracts specify terms and conditions of business transactions including price, quantities, quality, date of delivery, etc which avoids misunderstandings•Contracts help entrepreneurs to get goods on credit because the suppliers are aware that the entrepreneur is bound by contract and therefore will make effort to pay•Written contracts are important because it is easy to forget details you have agreed upon verbally and therefore provide a permanent record•Contracts may be used by entrepreneurs to convince bankers that the entrepreneur has a business that will generate income so as to obtain loans2.3.2. Termination of business contracts

To terminate a contract means to end the contract prior to it being fully performed by the parties. In other words, prior to the parties performing all of their respective obligations required by the contract, their duty to perform these obligations ceases to exist.Most contracts end once the work is complete and payment has been made.Contracts can also end:•By performance: If the contract is performed and fulfilled as expected under the terms and conditions of the contract and both parties are satisfied, the contract may be terminated.•By agreement: The parties to the contract may freely agree to end the contract if both consent to end the contract.•By destruction of the subject matter: The contract may be put to an end when the subject matter of the contract ceases to exist such as being destroyed, stolen or died.•By operation of the law: The contract may be terminated by law if it is illegal, if one party becomes bankrupt, insane or dies.•By frustration: A contract can be put to an end when a condition set in hinders one of the parties from performing his/her contractual obligations.•For convenience: Where the contract allows a party to terminate the contract at any time by providing notice to the other party eg employment contract.•Due to a breach: Where one party has not complied with an essential contract condition, the other party may decide to terminate the contract and seek compensation for damages.Application Activity 2.3

Read the following paragraph and answer questions that follow:Musoni started a business selling general merchandise in his community. He is renting the place where his business operates. He buys his goods from a nearby town through a fellow businessperson. He says he trusts his friend so they never write down anything when sending for goods but just gives him the money. He always sells good to his customers on credit but rarely make any record of such transactions. Recently, after some advice from a friend, he contracted a construction company to build for him a two-roomed building from where he will shift his shop.Questions:

a. Mention some of the mistakes Musoni is doing in his business activitiesb. What are the likely consequences of Musoni’s actions mentioned above?c. What advice would you give to Musoni to avoid the consequences above and why?d. What may cause Musoni to terminate the contract with the construction company?2.4. Types of Common Business Contracts

Activity 2.4

Analyze the following statements and answer questions that follows.i. You order a meal at a restaurant.ii. ‘Lost wallet, brown with One hundred thousand Rwandan francs in it. Return to owner and receive a 10.000Frw reward.’Questions:

a. Which of the above statements is a contract? Support your response.b. Concerning contracts, what is the difference between the two statements?c. What do you think is the difference between;i. Unilateral and bilateral contracts.ii. Gratuitous and onerous contracts.iii. Simple and adhesion contract.iv. Commutative and Aleatory contracts.Types of business contracts

a. Unilateral and bilateral contracts: In terms of the number of people or parties promising an action, bilateral contracts need at least two, while unilateral contracts only obligate action on one part. Unilateral contracts involve only promisor while bilateral contracts involve both a promisor and a promisee.A unilateral contract is a contract in which one party makes a promise to whomever takes action as prescribed in the offerA bilateral contract is where two parties enter into an agreement where both parties promise to do something.b.Gratuitous and onerous contracts: Gratuitous contracts are those of which the object is the benefit of the person with whom it is made, without any profit or advantage received or promised as a consideration for it. A gratuitous contract is sometimes called a contract of beneficence.Onerous contracts are those in which something is given or promised as a consideration for the engagement or gift, or some service, interest, or condition is imposed on what is given or promised, although unequal to it in value.c. Simple and adhesion contract: A simple contract is one, the evidence of which is merely oral, or in writing, not under seal, nor of record.As contracts of this nature are frequently entered into without thought or proper deliberation, the law requires that there be some good cause, consideration or motive, before they can be enforced in the courts. The party making the promise must have obtained some advantage, or the party to whom it is made must have sustained some injury or inconvenience in consequence of such promise; this rule has been established for the purpose of protecting weak and thoughtless persons from the consequences of rash, improvident, and inconsiderate engagements.A contract of adhesion refers to a contract drafted by one party in a position of power, leaving the weaker party to “take it or leave it.” Adhesion contracts are generally created by businesses providing goods or services in which the customer must either sign the boilerplate contract or seek services elsewhere.d. Commutative and Aleatory contracts: Aleatory contract is a type of contract1. whose execution or performance depends on a contingency or an uncertain (random) event beyond the control of either party, and/or2. under which the sums paid by the parties to each other are unequal. Most insurance policies are aleatory contracts because the insured may collect a large amount or nothing in return for the premiums paid.Commutative Contract is one in which each of the contracting parties gives and, receives an equivalent. The contract of sale is of this kind. The seller gives the thing sold, and receives the price, which is the equivalent. The buyer gives the price and receives the thing sold, which is the equivalent.Application Activity 2.4

Analyze the following statements and answer the questions that follow;1. You use your “Tap and Go card” to move from Nyabugogo Taxi park to Remera taxi park.2. Payment of insurance premium every month for your new car.3. The shop keeper hands you the new IPhone you have just paid for.4. You borrow a book from a friend who insists you have to buy an envelope to take it in but it seems not necessary to you.5. You continue paying service fee or monthly payments for water connections even when you no longer use the water.6. You promise to buy a new dress to your sister.With reasons, identify the types of contracts implied in the above statements1. ..........................................2. ..........................................3. .........................................4. .........................................5. .........................................6. .........................................2.5. General business contracts: Employment related contract and Leases

Activity 2.5

Complete the following statements as used in business contracts using the list of words below.1. (Bill of Sale, Agreement for the Sale of Goods, Purchase Order, Warranty, Limited Warranty, Security Agreement, Employment Agreement, Employee Non-compete Agreement, Independent Contractor Agreement, Consulting Agreement, Distributor Agreement, Sales Representative Agreement, Confidentiality Agreement, Reciprocal Nondisclosure Agreement, Employment Separation Agreement, Real Property Lease, Equipment Lease, Franchise Agreement, Advertising Agency Agreement, Indemnity Agreement, Covenant Not to Sue, Settlement Agreement, Release, Assignment of Contract, Stock Purchase Agreement, Partnership Agreement, Joint Venture Agreement, Agreement to Sell Business).a. ...................................Transfers ownership of a good from one party to anotherb. ................................... A contract for the sale, may be confirmed by a bill of sale after the transaction goes through.c. ......... .............. .......... First official offer made by a buyer to a seller.d. ......... ........................Any conditions or actions that would avoid the contract.e. ..................... ............Warranty limited to just one or a few parts.f. .................................. Contract between a lender and borrower of a loan.g. ............................... .... A contract for employment, including details about payment, job responsibilities, etc.h. .................................An agreement to not work for a direct competitor for a specified period of time after termination.i. .......................................Similar to an employment agreement, but outlines the terms to which the limited work contract applies.j. ..........................Outline of the tasks and responsibilities (and compensation in return) for a consulting relationship.k. ...........................Defines the relationship with a distributor.l. .................................Typically used to define the amount of commission, and how it’s tabulated, for a salesperson. m. ...............................Agreement to not disclose certain information to third parties.n. .........................................Non disclosure agreement in which both parties agree not to disclose certain trade secrets.o. .....................................Also referred to as a termination agreement, this formally ends the employment relationship.p. ...........................A contract to lease office, manufacturing, or commercial real estate between the landlord and the business.q. ..........................Agreement to lease equipment for a specified period of time.r. .........................Outlines the relationship between the franchisor and the franchisee, such as support, advertising, use of brand, etc.s. .................................Establishes the scope of duties to be performed by the agency, duration, payment, etc.t. .........................An agreement to transfer risk from one party to another.u. .........................One party claiming damages agrees not to sue the responsible party.v. ..........................Agreement between two parties to end a lawsuit in exchange for certain concessions (usually cash paid to the plaintiff ).w. ............Typically refers to a release from liability (which are common for businesses where customers assume a reasonable risk of some sort).x. .............................A legal transfer of the benefits and obligations of a contract from one party to another.y. ...............................Contractual agreement to sell a certain amount of stock to a named individual (often used for stock options at private companies).z. ...........................Official agreement among two or partners, including responsibilities of each.aa. .............................Lays out the obligations, goals, and financial contributions of all parties involved in a joint venture.bb. ................................Documents the terms of a business sale.Employment related contract

While all valid contracts must include certain elements particularly an offer, consideration, and acceptance. There are several different kinds of contracts addressing various business scenarios. Most small businesses will end up using the same kinds of contracts at various times, such as employment contracts or purchase orders, and will become quite familiar with these.Some of the more common types of business contracts that you may enter into are included in the following:a. Sales-related Contracts;•Bill of Sale:Transfers ownership of a good from one party to another.•Agreement for the Sale of Goods: A contract for the sale, may be confirmed by a bill of sale after the transaction goes through.•Purchase Order: First official offer made by a buyer to a seller.•Warranty: Any conditions or actions that would void the contract.•Limited Warranty: Warranty limited to just one or a few parts.•Security Agreement: Contract between a lender and borrower of a loan.b.Employment-Related Contractsi. Employment Agreement: A contract for employment, including details about payment, job responsibilities, etc.ii. Employee Non-compete Agreement: An agreement to not work for a direct competitor for a specified period of time after termination.iii. Independent Contractor Agreement: Similar to an employment agreement, but outlines the terms to which the limited work contract applies.iv. Consulting Agreement: Outline of the tasks and responsibilities (and compensation in return) for a consulting relationship.v. Distributor Agreement:Defines the relationship with a distributor.vi. Sales Representative Agreement:Typically used to define the amount of commission, and how it’s tabulated, for a salesperson.vii. Confidentiality Agreement: Agreement to not disclose certain information to third parties.viii. Reciprocal Nondisclosure Agreement:Nondisclosure agreement in which both parties agree not to disclose certain trade secrets.ix. Employment Separation Agreement:Also referred to as a termination agreement, this formally ends the employment relationship.c. Leasesi. Real Property Lease: A contract to lease office, manufacturing, or commercial real estate between the Property owner and the business.ii. Equipment Lease: Agreement to lease equipment for a specified period of time.d. General Business Contractsi. Franchise Agreement: Outlines the relationship between the franchisor and the franchisee, such as support, advertising, use of brand, etc.ii. Advertising Agency Agreement: Establishes the scope of duties to be performed by the agency, duration, payment, etc.iii. Indemnity Agreement: An agreement to transfer risk from one party to anotheriv. Covenant Not to Sue: One party claiming damages agrees not to sue the responsible party.v. Settlement Agreement: Agreement between two parties to end a lawsuit in exchange for certain concessions (usually cash paid to the plaintiff ).vi. Release: Typically refers to a release from liability (which are common for businesses where customers assume a reasonable risk of some sort).vii. Assignment of Contract: A legal transfer of the benefits and obligations of a contract from one party to another.viii. Stock Purchase Agreement: Contractual agreement to sell a certain amount of stock to a named individual (often used for stock options at private companies).ix. Partnership Agreement: Official agreement among two or partners, including responsibilities of each.x. Joint Venture Agreement: Lays out the obligations, goals, and financial contributions of all parties involved in a joint venture.xi. Agreement to Sell Business: Documents the terms of a business sale.Application Activity 2.5

a. Read the following paragraphs and answer the questions that follow:While walking along the beach, you notice a sign attached to a palm tree that reads, ‘Lost wallet, brown with one million Rwandan francs in it. Return to owner and receive a 100,000Frw reward.’ This picks your interest, and you begin sifting through the sand, turning over seashells, and flipping beach towels in search of the missing wallet. After all, you could use the 100,000Frw claims!i. Name the form of contract above.ii. Name the type of contract above.b. Kizito offered 10,000Frw for the return of his lost dog, but then he refused to pay because he thought the person who brought the dog back had stolen it.i. Was there a valid contract in the paragraph aboveii. Do you think Kizito is right? Give reasons to support your answer.iii. What advice would you give to the person who brought the dog back?2.6. Breach of a contract

Activity 2.6

Read the paragraph below and answer questions that follows.Kizito offered 10,000Frw for the return of his lost bag, but then he refused to pay because he thought the person who brought the bag back had stolen it.Questions:

a. Was there a valid contract? Give reasonsb. What do you think is happening in the paragraph?c. Do you think Kizito is right?d. How do we call the behavior of Kizito in business contracts?e. What should the person who brought the bag back do?f. How do we call Kizito’s behavior in business?2.6.1. Breach of a contract

Breach of a contract is a legal term that describes a violation of a contract or agreement in which one party fails to fulfill its promises or by interfering with the ability of another party to fulfill its duties. A contract may be breached in whole or in part.Most contracts end when both parties have fulfilled their contractual obligations, but it is not uncommon for one party not to completely fulfill his or her part of the contract agreement.Breach of a contract is the most common reason contract disputes are brought to court for resolution. In order for a breach of contract to be upheld by a court it must meet all of these requirements:i. The contract must be valid; that is, it must contain all the essential contract elements so that it can be heard by a court. If all essential elements are not present, the contract is not valid and there is no lawsuit.ii. The accuser must show that the defendant breached the contract.iii. The accuser did everything required in the contract.iv. The accuser must have notified the defendant of the breach. If the notification is in writing, this is better than a verbal notification.Types of breach of a contract

i. Material breach is a breach that is significant enough to excuse the aggrieved party from fulfilling its part of the contract.ii. Partial breach is not as significant, and it does not excuse the aggrieved party from its duties.iii. Anticipatory breach: A party may breach a contract by doing, or failing to do, something that shows intention not to complete duties under a contract.2.6.2. Defenses to breach of a contract

A defendant may offer a reason (defense) why the alleged breach is not really a breach of contract. Common defenses against a breach of contract are:i. Fraud: Which “knowing misrepresentation of the truth or concealment of a material fact to induce another to act to his or her detriment.” The defendant is saying that the contract is not valid because the plaintiff failed to disclose something important or made a false statement about a material (important) fact. The defendant must show that the fraud is deliberate.ii. Duress: Which occurs when one person compels another to sign a contract through physical force or other threats. This too invalidates the contract, since both parties did not sign of their own free will.iii. Undue influence is similar to duress: In that one party has a power advantage of another and uses that advantage to force the other to sign the contract.iv. Mistake: A mistake by the defendant cannot invalidate a contract and take away a breach of contract case. However, if the defendant can prove that both parties made a mistake about the subject matter (a car, let us say), it may be enough to serve as a defense.v. Statute of limitations: Many types of cases have a time limit by which a case must be brought. If the defendant can show that the statute of limitations has expired, the breach of contract case may be thrown out. Statutes of limitations are set by individual states. Here is an example of the state statutes of limitations on debt.2.6.3. Remedies to a breach of a contract

If one party is found to be in breach of a contract, the plaintiff has several ways to be made whole; called a remedy. The most common remedy is monetary payment. Some other common remedies for a loss resulting from a breach of contract are:i. Damages: Including compensatory damages (to compensate for the actual loss) and punitive damages.ii. Injunction: To get a court to require the other party to stop an action that is causing damage.iii. Rescission: Sometimes the plaintiff has been so badly damaged by the breach that the injured party is allowed to rescind (terminate) the contract.iv. Consequential and incidental damages: Money for losses caused by the breach that were foreseen, that is each side knew at the time of the contract that its breach would cause loss to the other party.v. Lawyer’s fees and costs: These are paid if it was clearly stated in the contractvi. Liquidated damages: Damages stated in the contract that would be payable if there is any fraud, dishonesty or breach of the contract.vii. Punitive damages: Money charged to punish the offending person to discourage them from such behavior.viii. Specific performance of the contract: Under certain circumstances, the court may direct the breaching person or business to perform that very obligation which he had promised to undertake.Application Activity 2.6

Analyze the illustration below and answer questions that follow. a. Do you think there was a valid contract in the illustration above? Give reasons to support your answer.b. Do you think there was a breach of contract in the illustration? Give reasons to support your answer.c. With reasons, which type of breach is illustrated?d. Suggest the possible remedies for the breach of contract above.

a. Do you think there was a valid contract in the illustration above? Give reasons to support your answer.b. Do you think there was a breach of contract in the illustration? Give reasons to support your answer.c. With reasons, which type of breach is illustrated?d. Suggest the possible remedies for the breach of contract above.2.7. Conflicts and disputes in business

2.7.1. Business disputes and conflicts

A business dispute is a disagreement over the existence of a commercial legal duty or right, or over the extent and kind of compensation that may be claimed by the injured party for a breach of such a duty.Conflicts between business owners and employees typically involve differences of opinion, style, or approach that are not easily resolved. These can lead to hurt feelings and altercations among employees.Conflict may occur between co-workers, or between supervisors and subordinates, or between service providers and their clients or customers. Conflict can also occur between groups, such as management and labor, or between whole departments.However, some conflicts reflect real disagreements about how an organization should function. If the winner of the conflict happens to be wrong, the organization as a whole could suffer. Some conflicts involve bullying or harassment of some kind, in which case a fair resolution must involve attention to justice.In addition, if one party out-ranks the other, the power disparity could complicate resolution even if everybody concerned means well.2.7.2. Business conflicts with stakeholders