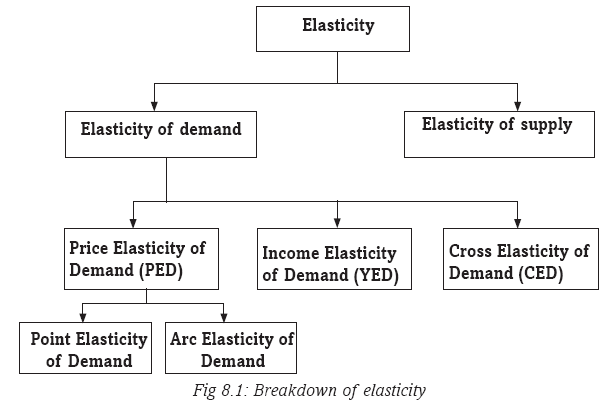

Topic outline

General

- Economics S4 SB File Uploaded 28/01/22, 13:13

- S4: Economics TG File Uploaded 11/08/22, 22:20

UNIT 1 BASIC ECONOMIC CONCEPTS AND THE IMPORTANCE OF ECONOMICS

Key unit competence: By the end of the unit, you should be able to:

(a) Use the basic concepts of Economics appropriately.

(b) Appreciate the role of Economics in the society.Activity 1.1

In groups of five, do the following.

(a) Read through the sentences below.

(i) Fewer farmers raising cattle can result in inadequate supply of milk and cheese.

(ii) After poor weather, corn crops failed to grow, resulting in inadequate supply of food for people and animals, and ethanol for fuel.

(iii) Those without access to water experience a shortage of water.

(iv) Depletion of forests in Thailand has led to limited supply of wood. This has forced individuals to take wood from demolished buildings in order to build new ones.

(v) Waste of water through long showers or allowing water to run while brushing one’s teeth can contribute to shortage of water.

(b) Identify a major economic problem raised by each of the above sentences.

(c) Discuss the field of study you would put the economic problem you have identified.From the activity above, it is evident that Economics is about choices and impact of those choices. It is connected to our lives, from the decisions we make as individuals, families, firms and governments.

Activity 1.2

In groups of five, go to the library and research on the following:

(a) Origin of Economics

(b) Importance of Economics

(c) Basic terms used in Economics.

Note down your findings on a piece of paper, flip chart or powerpoint. Make your presentations to the whole class.

N/B: The following websites may also be useful: www.wikipedia.org and www.economicsnetwork.ac.uk.1.1 MEANING, ORIGIN AND SCOPE OF ECONOMICS

1.1.1 Meaning of EconomicsActivity 1.3

(a) Form groups of five. Let each one of you write down on a piece of paper at least three sentences explaining what you understand by the term Economics. Exchange the pieces of paper amongst your groups and compare what you have written. Thereafter, read out the agreed definition to the whole class.

(b) In a class discussion, select any three definitions you would consider appropriate.Give reasons for your answer.

(c) Read through the definition of Economics from the teaching resources provided by the teacher and compare it with what you had selected as the appropriate definition.Several economists have defined Economics differently. Here are some of their definitions:

1. Economics is the study of mankind in the ordinary business life. (Alfred Marshall)

2. Economics refers to the study of nature and causes of wealth of nations. (Adam Smith)

3. Economics is a science which studies human behaviour as a relationship between ends and scarce means which have alternative uses. (Robbins)From the above definitions, many economists consider Robbins’ definition the most appropriate.

This is because:

• It gives the fundamental causes of the economic problems such as unlimited human needs,limited means to satisfy man’s needs, the alternative uses for the resources and the different importance

of wants.

• Robbins’ definition emphasises scarcity as a foundation of Economics, otherwise without scarcity,there would be no Economics.

• Man’s problem is not accumulating wealth, but satisfaction of human needs.1.1.2 Origin and scope of Economics

The modern word “Economics” has its origin in the Greek word “Oikonomos” meaning a steward. This word can be decomposed into two parts, “Oikos”, meaning a house and “nomos”, meaning a manager.

The sum up of the two words is what economics is all about. Literally, Oikonomos means house manager.There is an economic aspect to almost any topic we mention – education, employment, housing, transport, defence. Economics has developed into a comprehensive theory of how the society works. But as such, it is difficult to define. Economics developed as a separate discipline from moral philosophy in an attempt to understand how man undertook decisions on production and consumption so as to maximise profits and utility respectively. In the 17th century, Economics was referred to as study of political economy and lacked its own unique methods of analysis.

The classical economists, especially Alfred Marshal defined economics as the “Study of man in the ordinary business life”. This definition appears too vague based on what Economics is concerned with. Any definition should take account of the guiding idea in Economics, which is scarcity. The great American economist Paul Samuelson thus defined it as: “The study of how people and society choose to employ scarce resources that could have alternative uses, in order to produce various commodities and to distribute them for consumption, now or in future amongst various persons and groups in society.

The study of Economics basically revolved and still revolves around the problem of scarcity. All resources are scarce. The resources are not enough to fill everyone’s wants to the point of satiety. Therefore, the concern of Economics is on how man can utilise the scarce resources to meet his unlimited needs.

We therefore have limited resources and the economist’s job is to evaluate the choices that exist for the use of these resources. Thus we have another characteristic of Economics; choice.

The study of Economics begins with the understanding of human “wants”. Scarcity forces us to economise. We weigh up the various alternatives and select those particular bundles of goods which yield the highest return from our limited resources. Modern economists use this idea to define the scope of their studies.

Although Economics is closely connected with social sciences such as ethics, politics, sociology, psychology and anthropology, it is distinguished from them by its concentration on one particular aspect of human behaviour, choosing between alternatives in order to obtain the maximum satisfaction from limited resources.

Economics is thus based on four fundamental characteristics of human existence and investigating what happens when they all exist together. First, the needs of human beings are without limit. Second, those needs vary in value or importance. Third, the resources available for satisfying those needs are limited. Fourth, the resources have alternative uses. As a result, a decision has to be made on what goods to produce and which needs to satisfy and which ones to forego.

1.2 IMPORTANCE OF STUDYING ECONOMICS

Activity 1.4

In groups of five, attempt the following:

(a) Identify the possible professions you would pursue after your Economics course in high school.

(b) Explain how Economics prepares you to pursue those professions in future.

(c) Identify the major economic events that have taken place in your country.

(d) Explain how studying Economics helps you to interpret the effects such events haveon you and your country.

(e) Identify the major economic problems existing in your country.

(f) Explain how studying Economics helps you to identify those problems.

(g) Discuss how you can find solutions to the problems identified above.It is noted that Economics,

• Is a career subject. It prepares students for further academic and professional qualifications in fields like Commerce, Statistics, Mathematics and Environmental Sciences, among others.

• Equips learners with the knowledge regarding what takes place in the world of business.

• Makes it possible for learners to understand and appreciate economic problems existing in their countries, regions and the world, thereby finding solutions to those problems.

• Equips learners with the knowledge and skills required for them to fully participate in the economic activities aimed at developing their economies.

• Enables students understand the scarcity of resources and get knowledge on how the available resources can be utilised maximumly.

• Enables students to understand the basic economic concepts and principles of Economics and how to apply them in daily life.

• Prepares students for employment in various fields such as policy makers and economic planners, hence improving their livelihoods.1.3 BASIC TERMS USED IN ECONOMICS

Activity 1.5

In groups of five, go to the library and undertake research on the following:

(a) Meaning and types of price, commodities and goods.

(b) Meaning, forms and characteristics of services and wealth.

(c) Welfare needs and wants.

(d) Resources

(e) Household, firms government and foreign sector economic agents.

(f) Economic activities.

(g) Meaning, roles, types, characteristics, advantages and disadvantages of economic systems.

Write down your research findings.

Present your findings to the whole class.1.3.1 Wealth

Wealth refers to the stock of assets held by an individual, a firm, an organisation or a country, at any particular moment of time.Characteristics of wealth

(a) It has value: Wealth can be expressed in monetary terms.

(b) It is relatively scarce: Wealth is not found easily.

(c) It is transferable: Wealth can change ownership and possession from time to time.

(d) It possesses utility: Wealth gives satisfaction to the owner.Forms of wealth

(a) Social wealth: This refers to all public assets such as public roads, public libraries and public hospitals.

(b) Business wealth: This refers to the wealth of business organisations at any particular time.

(c) Individual wealth: This refers to the assets or wealth held privately by an individual.

1.3.2 Resources

This refers to all productive inputs used to create or produce goods and services. Resources are divided into natural resources, manmade resources, human resources, renewable resources and non-renewable resources.a) Natural resources

These are resources that occur naturally within the environment. We cannot produce natural resources. They are used by human beings to produce goods and services. Examples include air, land, mineral resources, water and sunlight.b) Human-made resources

These are resources created through the action of human beings. They include equipment and machinery such as computers, cars, houses and all forms of machines and tools used in the production process.c) Human resources

This is a set of individuals who make up the workforce of an organisation, business sector or the economy. They help in the production of goods and provision of services. They include organisational managers, supervisors and other employees. Some of these people are employed on permanent and pensionable terms, some are employed on contract and some are employed as casuals. Others work on internship programmes.Recall

Most companies prefer employing staff on contract than on permanent basis. Discuss.d) Renewable resources

These are resources that can be used over and over without being depleted. They are unlimited in supply. They can be replaced as fast as they are used up. Examples include solar energy, biomass energy, wind energy, geothermal energy and hydropower energy.e) Non-renewable resources

These are resources that once used they cannot be replaced. Their quantities are limited. This is because they get depleted. Examples include coal, petroleum, natural gas and minerals such as gold and diamond.Remember!

Since natural resources exist within the environment, they should be used properly and sparingly. Overexploitation of resources has negative effects on the environment. It is therefore advisable and a necessity to carry out environmental impact assessment in the area before any activity. This helps to ensure proper use of resources for sustainable development and protection of the environment.1.3.3 Price

Price refers to the rate at which a commodity is exchanged in the market. It can also be defined as the relative value of a commodity expressed in monetary terms.Types of prices

(a) Market price: This refers to any price existing in the market at a particular period of time, regardless of how it is determined.

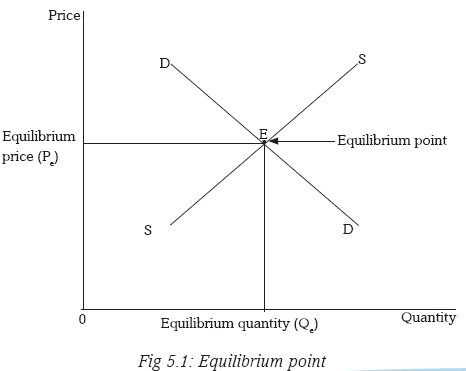

(b) Equilibrium price: This is the price established in the market when quantity demanded is equal to quantity supplied. Such prices change from time to time as determined by the market forces of demand and supply.

(c) Normal price: This refers to the long run established price after a long period of price fluctuations.

(d) Reserve price: This refers to a minimum price acceptable to a producer or a seller in order to part with a commodity.1.3.4 Economic agents

Economic agents are the major decision making units in an economy. They include:

(a) The household: This refers to a group of individuals under one roof who take joint decisions on their own economic ventures.

(b) The firm: A firm is the smallest unit of production which employs factors of production to produce goods and services.

(c) The state: This refers to an institution that has both political and economic powers to influence resource allocation and distribution. It is this agent that regulates the activities of the households and firms.

(d) Foreign sector (X - M): This comprises of exports and imports. It includes everything outside the political boundaries of the economy. It is responsible for the expenditures on gross domestic product.1.4: DIFFERENCE BETWEEN NEEDS AND WANTS AND BETWEEN GOODS AND SERVICES

Activity 1.6

Case study

Mr. Gato has a list of desires that he wants to satisfy with his monthly earning. His monthly income is 100,000 Rwf. From his income, he wants to pay rent, food, school fees for his kids, medication and a bank loan. He wishes to buy a car. He is also planning to fly out with his family during the school holidays.

(a) Based on this scenario, identify Mr. Gato’s needs and wants.

(b) Which ones (from (a) above) should he satisfy first?1.4.1 Needs

Needs are those human desires whose satisfaction is necessary to sustain life. They are also called basic needs. They include food, shelter and clothing.Recall

1. Identify the various types of food that human beings need.

2. Explain why human beings must eat a balanced diet daily.

3. Why do people fall sick?

4. Discuss why many people want to live in permanent houses.

5. Identify the various types of clothes.Which ones are specifically for ladies and which ones are for men? Why do you think so?

1.4.2 Wants

Wants are those human desires whose satisfaction makes life more comfortable, enjoyable, relaxed and pleasant. They are also called luxuries. They are not necessary for sustaining life.NOTE: Some of these wants are derived from the basic needs. They include luxurious vehicles, expensive suits and clothing, personal airplanes and mansion buildings.

Note also that some of these wants are no longer luxuries, but part of the basic needs. Many people for instance, now own vehicles to enable them carry out their daily duties faster and with ease. People also own television sets to be aware of what takes place elsewhere, to be informed, educated and entertained.

Characteristics of wants

1. They are re-current in nature.

2. They are unlimited.

3. They are complementary.

4. They have different degrees of urgency.Remember!

Given that human wants are unlimited, yet the resources to satisfy them are limited, there arises the need for proper use of resources. This requires us to make budgets when making financial decisions; it also requires us to learn a culture of saving as well as prioritising in order to make use of money properly.

1.4.3 Welfare

Welfare is the provision of minimal level of wellbeing and social support for all citizens. The level of individuals’ welfare is indicated by the quantity and quality of goods and services they can access.1.4.4 Commodities

These are products that are produced or created by use of factors of production. People use these commodities to satisfy their desires. Commodities are categorised as either goods or services.1.4.4.1. Services

Services are intangible items or things that satisfy non-material wants.Forms of services

a) Direct services

These are services that directly benefit the individual person. Examples include education, medical care and sports and games.b) Indirect services

These are services the individual benefits from indirectly or commercially. Such services facilitate business activities. They include banking, insurance, advertising, transport and communication.Characteristics of services

(i) They are intangible. Services can neither be seen, felt nor touched.

(ii) Provision of services requires use of the service providers such as teachers and doctors,physical tools such as textbooks or equipment such as communication masts or boosters.

(iii) They are consumed as they are provided. Services cannot be stored for future use.

(iv) Services cannot be transported from one place to another.Only the service providers can move or be transported to other areas or places.

1.4.4.2 Goods

These are tangible items that satisfy human desires. For example food, clothing, vehicles and furniture.Types of goods

Activity 1.7

In groups of five, carry out research on types of goods.

(a) From your research findings, discuss types of goods and make presentations.

(b) Discuss the characteristics of the different types of goods identified above.(a) Free goods: These are goods which are abundant in supply. People use these goods without paying for them. Most of these goods are provided freely by nature. Examples of such goods include air, water and land.

Recall

If water and land are free goods, why do people sell land and bottled water?(b) Economic goods/commercial goods: These are goods which are scarce in supply, require payment and yield satisfaction to the consumer. Examples include manufactured goods.

Characteristics of economic goods

(i) They are relatively scarce.

(ii) They have monetary value.(iii) They have opportunity cost, consuming economic goods necessitates sacrificing others.

(iv) They yield satisfaction or utility to the consumer.

(v) They are marketable.(c) Public goods: These are goods that are owned and enjoyed collectively. Examples include public roads, public hospitals and public schools.

Characteristics of public goods

(i) They are provided by the state or government.

(ii) They are owned collectively. One’s consumption of a public good does not exclude others.

(iii) They cannot be exhausted.

(iv) They involve indirect payment.Payment for public goods is made collectively and indirectly through taxation.

(d) Private goods: These are goods which are owned and enjoyed individually. One’s consumption of these goods excludes others. These goods involve direct payment. An example is buying a car for personal use.

(e) Merit goods: These are goods which are considered to be essential to the society. Examples include education, health and water.

(f) Economic bads: These are goods which are harmful and dangerous to the society. The government must (g) Producer goods: These are goods used in the production of other goodscontrol their production. Such goods include alcohol and drugs.Recall

List examples of producer goods.(h) Final goods: These are goods ready for consumption by the final user. Examples include manufactured goods such as foodstuffs and clothes.

(i) Complimentary goods: These are the type of goods that are used together. To get the full utility of one good, the other complementary good must be used along with it. For example, car and petro are two complementary goods.(j) Substitute goods: These are goods which can be used as alternatives. One good can be used as an alternative to the other. Examples of substitute goods include, LG and Samsung TVs, Coca-Cola and Pepsi sodas.

(k) Inferior goods: These are goods whose demand falls with an increase in the consumer’s level lf income. It is a type of good that people do not consume when their income increase, because they shift their consumption to more prestigious goods. A good example is a second-hand cloth. When the income of people increases, people avoid buying second-hand clothes and shift to more expensive clothes.

(l) Luxury goods: These are types of goods whose demand and consumption increases as type income of the consumers increase. a good example of a luxury good is the HD Television sets. When the incomes of people increase, the demand for such TV sets increases, because people can afford to buy them.

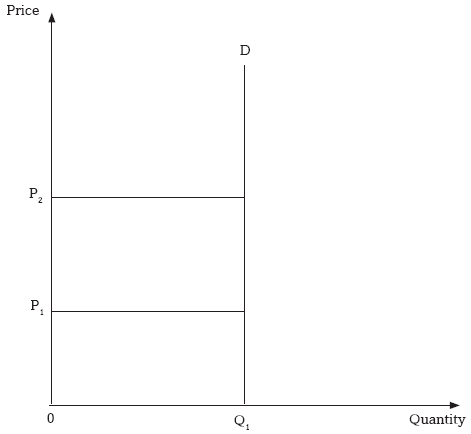

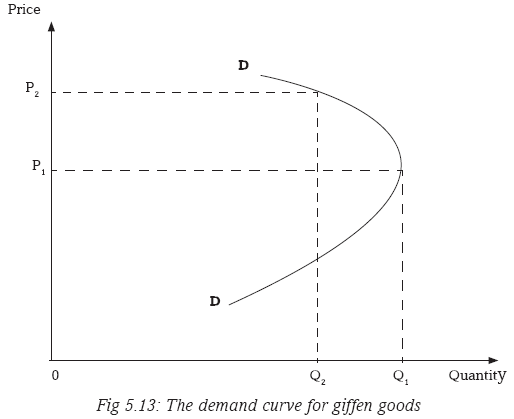

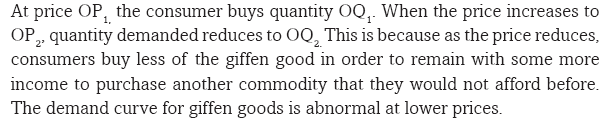

(m) Giffen goods: These are goods whose increase in price tends to increase their demand and consumption by consumers. This happens when consumers cannot afford the alternative goods, therefore stick on these types of goods. For example, low quality rice is a good example of a giffen good. As the price of the low quality rises, the peasant consumers cannot afford other alternatives because all their income is depleted on the low quality rice. Therefore, they consume more of the rice rather than buy alternatives like meat.

1.5 ECONOMIC ACTIVITIES AND ECONOMIC SYSTEMS

1.5.1 Economic activities

Activity 1.8

In groups of five,

(a) Discuss and make presentations on the definition of economic activities.

(b) Identify and discuss the major economic activities in the country.Economic activities are the activities that involve the production, distribution and consumption of goods and services at all levels within the economy. Economic activities exist in the following major production sectors of the economy:

1. Primary level of production

2. Secondary level of production

3. Tertiary level of production1. Primary level of production

Primary production involves extraction of raw materials from their natural source. The major economic activities under primary production include farming, mining, fishing, forestry and lumbering.2. Secondary level of production

Secondary level involves transforming raw materials into finished goods that can satisfy human wants. It comprises of all the activities in the construction, processing and manufacturing industries.3. Tertiary level of production

Tertiary level involves provision of services. Examples of economic activities under tertiary sector include transport, banking, insurance, tourism, advertising and communication.1.5.2 Economic systems

Case study

In different countries, the way resources are owned, controlled, allocated and the general distribution of goods and services is different. In U.S.A for example, resources are owned and controlled by individuals with limited government intervention. In China, resources are owned, controlled and distributed by the government. Rwanda and Kenya have a mixed economy. In other countries, both the private individuals and the government own resources and participate in resource allocation.

In groups of five,

(a) Explain the meaning of an economic system, using the above case study.

(b) Identify the major economic systems that exist in the world.

(c) In small groups discuss the characteristics of the economic systems discussed above and identify the economic system in which your country belongs.

(d) Discuss the advantages and disadvantages of the above economic systems.An economic system refers to the general organisation and structure of an economy. It deals with the ownership of resources, control and allocation of resources and the general distribution of goods and services. There are three major economic systems:

(a) The free enterprise/laissez-faire/capitalist economy.

(b) The command/planned/socialist economy.

(c) The mixed economy.(a) The free enterprise/capitalist economy

This is an economic system where producers engage in economic activities with a high degree of freedom. In this economy, prices are determined by forces of demand and supply with no or limited government intervention.Features of a free enterprise economy

1. There is private ownership of property and factors of production.

2. There is no government intervention in the economic decisions. This implies that the major economic decisions such as what, when, where and how to produce are made by market forces of demand and supply, through price mechanism.

3. There is profit motivation in the production process. People engaged in the production process do so with the main aim of getting profit out of the business.

4. There is a lot of competition in the economy. This is because production is profit oriented.

5. There is freedom of choice and enterprise in the economy, since the government has limited control.

6. There is presence of social classes in the economy. The high social class (the rich) own factors of production. The low social class (the poor) are the majority. They are the workers who do not own factors of production.

7. The market forces of demand and supply determine prices.Advantages of a free enterprise economy

1. In a free enterprise economy, there is competition. This improves efficiency in production of goods. This in turn leads to production of better quality products.

2. Free enterprise economy promotes consumer sovereignty. Consumers influence the production process.3. It encourages people to work hard for a better living and resource accumulation.

4. There is increased output since producers produce and supply more goods and services in order to earn more profits.

5. Efficient firms in a free enterprise economy increase the level of employment because of increased investment.

6. There is optimum allocation of resources. Resources are allocated where they are highly demanded. As a result, inefficient firms are driven out of the industry.

7. It reduces the burden of government participation in resource allocation.Disadvantages of a free enterprise economy

1. It creates income inequalities in a society. This is because the few who own the means of production will become richer as the majority becomes poorer.

2. Free enterprise economy tends to encourage capital intensive technology. This leads to unemployment.

3. It leads to creation of monopoly as a result of inefficient firms being driven out of production, due to competition.

4. It leads to misallocation of resources. It may encourage production of luxurious products that are demanded by the rich.

5. Production in a free enterprise economy is profit motivated which lead to exploitation of consumers in form of high prices.

6. Due to absence of government intervention, there is a high degree of duplication of goods and services.(b) Command/planned economy

This is an economic system where resources are owned, allocated and distributed by a central planning authority (government) on behalf of the citizens. The government, on behalf of the citizens, takes all economic decisions.

Features of a planned economy

1. There is public ownership of all productive resources such as land.

2. A central planning authority carries out all decisions on production, resource allocation and distribution.3. There is no freedom of individuals to operate their own enterprises.

4. The major economic activities in the economy aim at offering services to the citizens.

5. The state owns and operates the means of production in the economy.Advantages of a planned economy

1. It is easy to implement government policies, as the government is in direct control of production.

2. It reduces income inequalities. A planned economy eliminates private ownership of property and competition.

3. It can lead to efficiency in production. This is because production is directed by the state in order to achieve social objectives.

4. It promotes social welfare. The objective of production is not profit maximisation, but achieving the best for the community.

5. It promotes economic stability. All economic decisions are carried out by the central planning authority.

6. Consumers are protected from exploitation. Essential services are cheaply provided by the stateDisadvantages of a planned economy

1. Planned economy is characterised by production of poor quality products. This is due to absence of competition from the private sector and failure to respond to consumers’ demands. A planning authority sets out production targets.

2. There is lack of motivation and individual initiative. This leads to limited innovation in the production process.

3. Central planning under a planned economy results into bureaucracy. This leads to delays in decision making, thereby wasting time and promoting inefficiency.

4. There is lack of consumer sovereignty in a planned economy. The right of a consumer to determine the process of resource allocation does not exist in a planned economy. Freedom of choice is also limited.

5. It increases administrative costs on the part of the government. Government agencies will be actively involved in resource allocation and distribution, all of which increases costs to the government.

6. This system tends to be characterised by mismanagement of resources. This is because corruption and nepotism are always rampant.(c) Mixed economic system

This is an economic system in which both the state and the private sector own resources and participate in resource allocation.Features of a mixed economy

1. There is co-existence of the private sector and the public sector. Thus both the government and the private sector own resources.

2. There is existence of both the planning authority and price mechanism in resource allocation.

3. There is equal existence of social welfare objectives and profit maximisation objectives. In the public sector, production aims at the wellbeing of the society. In the private sector, production aims at profit maximisation.

4. In a mixed economy, the government sets guidelines for the private to follow as they engage in the production process.

5. There is freedom of enterprise, with some minimal level of government interference.Advantages of a mixed economy

1. A mixed economy offers more employment opportunities from both the government and the private sector.

2. A mixed economy promotes fair distribution of resources due to government intervention in the allocation of resources.

3. It promotes regional balance in development since government intervention reduces the influence of price mechanism in resource allocation4. There is control of monopoly tendencies in the economy by the anti- monopoly policies set by the government.

5. It promotes stability in prices because of the price control measures that governments put in place in mixed economies.

6. There is increased investment in mixed economies because the private sector is promoted.

7. There is proper allocation of resources due existence of the central planning authority. This body ensures that resources are allocated in the most efficient manner.

8. Under a mixed economy, the government provides public goods and services, which would not be provided by the private sector alone.Disadvantages of a mixed economy

1. Government interference may undermine the private sector.

2. Government participation in production may result into state monopolies.

3. The participation of both the private sector and the state may lead to duplication of services.

4. Due to the participation of the government and the private sector in the production process, there may be over exploitation of resources.Unit Summary

In the just concluded unit the following were discussed:

• The meaning of Economics, which was defined differently by many economists such as Adam Smith, Robbins and Alfred Marshal. Basing on their definitions, Economics can be defined as a science which studies man’s attempt to satisfy his unlimited wants/desires using scarce resources that have alternative uses.

• Importance of studying Economics was also highlighted. For instance, some of the points were: preparing students for further studies in the area of commerce, enabling learners to actively participate in their countries’ development process and preparing students to get employment in various fields related to Economics.• Various concepts in Economics were also discussed. Price was defined as the rate at which a commodity is exchanged in the market.

• Factors such as haggling, auctioning, market forces and government intervention, which influence price determination, were discussed.

• Wealth as the stock of assets held by an individual, a firm or an organisation at any particular moment of time is another concept that was discussed.

• Goods as tangible items that satisfy human desires were discussed. The types of goods such as free goods, economic goods, private goods and public goods were discussed too.

• Resources, which are the inputs used to create or produce goods and services was discussed.

• Wants was another concept that was discussed.

• Economic agents such as the household, the firm, the government and the foreign sector were also discussed.• Economic systems such as the free enterprise/capitalist economy, the command/planned/ socialist economy and the mixed economy were discussed.

• Free enterprise economy is an economic system where resources are owned, controlled and allocated by private individuals without government interference.

• A command economy is one where resources are owned, controlled and distributed by a central planning authority on behalf of the citizens.

• A mixed economic system on the other hand is the one where both the government and the private individuals participate in the ownership, allocation and distribution of resources.Unit Assessment 1

1. (a) Economics was defined by many economists differently. Outline their definitions and suggest which one is more appropriate and why.

(b) Explain the reasons why studying Economics is important.

2. (a) Explain the following concepts as used in Economics: price, wealth, wants, goods, commodities and economic agents.

(b) What is an economic system? List the major economic systems that you know indicating their characteristics.

3. Explain the advantages and the disadvantages of the following economic systems:

(a) Free enterprise economy

(b) Command economy

(c) Mixed economyURL: 1Files: 3UNIT 2 FUNDAMENTAL PRINCIPLES OF ECONOMICS

Key unit competence: By the end of the unit, you should be able to:

(a) Demonstrate a good understanding of the fundamental economic principles.

(b) Demonstrate the applicability of the fundamental economic principles in daily life.2.1: DEFINITION OF THE FUNDAMENTAL PRINCIPLES OF ECONOMICS

Case study

Budgeting

Human beings hardly get satisfied in life. Those who are unemployed wish one day to be employed. The employed on their part, wish to get a promotion and a salary increase. Those with small vehicles desire to own bigger vehicles like Toyota Prados. Those owning bigger vehicles wish they could own jets. People living in rural areas want to move to urban areas, while those in urban areas want to own land in rural areas. Countries too desire to own some assets but they cannot access them.

(a) Identify other scenarios showing that human beings, families or governments are never satisfied.

(b) Why is this always the case?

(c) Suggest any solutions to the above scenarios.Human wants are unlimited and the resources to satisfy them are limited. As a result, the basic principles of Economics explain this concept. These principles further show the fundamental problems of human beings in their bid to try and use the scarce resources to satisfy the unlimited wants. These principles are:

(a) Scarcity

(b) Choice

(c) Opportunity costa) Scarcity

This refers to the limited supply or insufficiency of resources in satisfying the needs of an individual, family or state, in relation to the unlimited wants. Due to the problem of scarcity, one has to make rational choices by satisfying the most pressing wants first and then the least pressing ones last.As a result, there is need to prioritise by making a list of one’s wants in order of satisfaction. In the list, the most pressing needs are put at the top to be satisfied first, then the less pressing ones are put last on that list. This list is known as the scale of preference.

b) Choice

Choice refers to the act of making the right decision at the right time so as to use limited or scarce resources to satisfy the unlimited wants. For instance, a student who has a fixed amount of money can opt to buy a textbook to use in the classroom, rather than buying sports shoes to be wearing over the weekends.c) Opportunity cost

This refers to the second best alternative foregone when a choice is made. It can be illustrated using the opportunity cost curve, which shows the amount sacrificed on one commodity in order to get more of another.2.2: PRODUCTION POSSIBILITY FRONTIER (PPF)

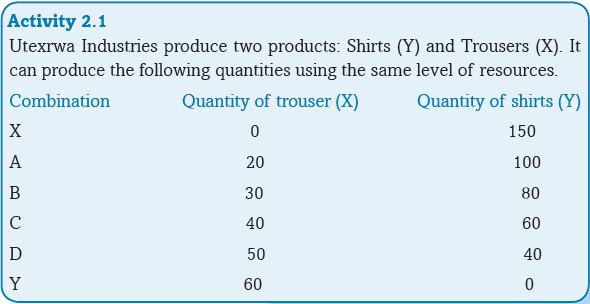

(a) Refer to the table on page 23. Discuss (in groups of five) what the firm can do to increase on production of Trousers (X).

(b) Derive the production possibility frontier (PPF) by plotting the quantities of Y on the y-axis and the quantities of X on the x- axis. Later, join the points.

(c) Carry out research on the assumptions on which the PPF is based and the importance of the PPF. Make a power point presentation.A production possibility frontier (PPF) is a locus of points showing the possible combinations of two commodities that can be produced when all the resources are fully utilised. It is also called the transformation curve or the opportunity cost curve.

(a) Assumptions of the PPF

• It assumes that only two commodities are produced.

• It assumes that the level of technology is fixed and constant.

• It assumes that all resources are fully utilised.

• It assumes that similar resources will be used to produce either or both of the two goods.(b) Importance of the PPF

• The PPF shows whether there is economic growth or decline in the country. An outward shift indicates economic growth. An inward shift indicates economic decline.

• The PPF shows the rate of unemployment by showing the rate at which resources are employed or utilised. Points along the PPF show full employment and utilisation of resources. Points inside the PPF show the unemployment and underutilisation of resources.

• The PPF shows the combination of goods and services that can be produced in an economy.

• It indicates technological advancement within an economy. When the level of production increases, the PPF shifts outwards. This indicates technological advancement.The hypothetical possibility schedule

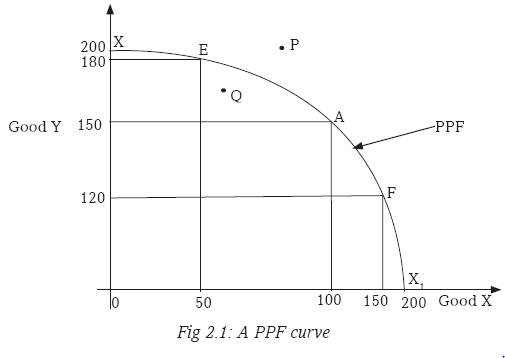

In the above illustration, X and X1 are the possibilities in which the producer can produce either 200 units of Good Y only or 200 units of Good X only with given resources. However, the assumption is that both are produced. There are therefore various combinations E, A and F that can be produced.

On combination E, 180 units of Good Y are produced and 50 units of Good X are produced. On combination A, 150 units of Good Y are produced and 100 units of Good X are produced. At combination F, 120 units of Good Y and 150 units of Good X are produced.

The PPF shows that when more units of Good X are produced, less units of Good Y are produced. This implies that the producer withdraws some resources from the production of Good Y and uses them in producing more units of Good X. This transforms resources producing Good Y into production of Good X. It is for this reason that the curve is also called a transformation curve.

As resources are moved from production of Good X to production of Good Y, the efficiency is lost hence same level of output is not achieved as the trade off is not proportional. This explains why the PPF curve is convex.

Point Q inside the PPF, indicates that the level of output is attainable but undesirable. This is because rationality requires that one prefers more to less. Point P outside the PPF, is not attainable using the available resources. However, it may be attained should the available resources be increased.2.3 THE RELATIONSHIP BETWEEN SCARCITY, CHOICE AND OPPORTUNITY COST

Activity

In groups of five, discuss the relationship between scarcity, choice and opportunity cost, using the PPF above. Make presentations after the discussion.The PPF indicates what is attainable and what is not attainable given the level of resources. Due to scarcity of resources, a producer cannot produce the maximum level of output for both the two goods at once. The producer makes a choice to either produce more of Good X and less of Good Y and vice- versa. If the producer produces more of Good X he foregoes units of Good Y (opportunity cost) as shown by the PPF.

2.4 SHIFTS IN THE PPF

Activity

(a) In groups of five, visit the library and carry out research on the shifts in the PPF.

(b) After undertaking the research, discuss inward and outward shifts of the PPF.

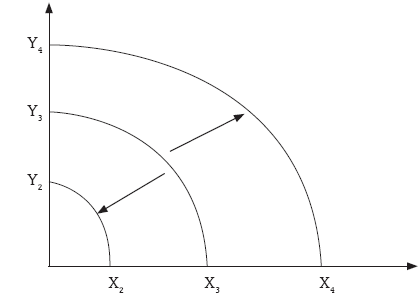

(c) Explain the reasons why the PPF may shift inwards or outwards.The PPF may shift inwards or outwards. A shift of the PPF inwards indicates economic decline while a shift outwards indicates economic growth.

An outward shift from Y3X3 to Y4X4 indicates economic growth. This may be due to any of the following reasons:

• Discovery of new natural resources.

• Advancement in technology that leads to production of more goods and services.

• Expansion of markets that encourage production of more goods and services.

• Improvement in the skills of labour that results into efficiency in production.

• Increased investment as a result of improved entrepreneurship skills.An inward shift from Y3 X3 to Y2 X2 indicates an economic decline. Similarly, there is a reduction in the quantity produced of both Goods Y and X. This may be due to any of the following reasons:

• Lack of new natural resources.

• Decline in the invention and use of technology that leads to production of poor quality and fewer goods and services.

• No new markets that encourage production of more goods and services.

• Decline in the availability of trained manpower, through retrenchment of workers. This results into less output and inefficiency in production.

• Decreased investment as a result of poor entrepreneurship skills.2.4.1 Types of PPF

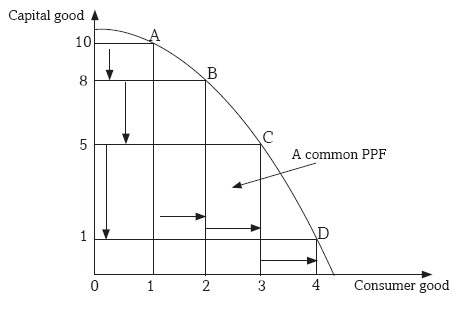

1. Common PPF: This is a PPF where there is an increase in opportunity cost as the production of one good is increased.

Fig 2.3: A common PPF

From the above PPF, in order to produce an additional unit of consumer good, two units of capital goods have to be foregone. But additional unit of consumer good, will cause three units of capital goods to be foregone and another additional unit of consumer good will cause four units of capital good to be foregone. A common PPF is also known as a concave PPF.

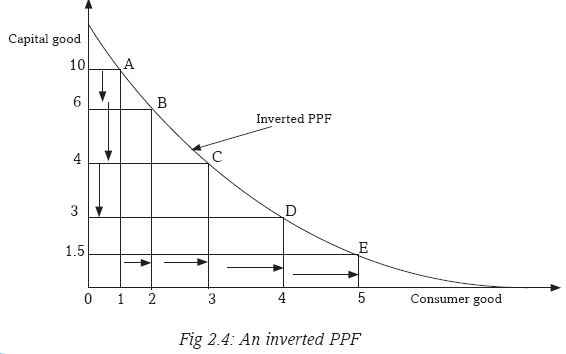

2. Inverted PPF: This is a PPF where the opportunity cost is decreasing with each of one good

From the above PPF, to produce an additional unit of consumer good, four units of capital good are foregone. But another additional unit of consumer good will cause two units of capital good to be foregone. Any further additional unit of consumer goods will cause one unit of capital goods to be foregone. Opportunity cost will continue to decrease with any additional unit of consumer goods being produced. An inverted PPF is also known as a convex PPF.

3. A straight line PPF: This is a PPF where the opportunity cost is constant with an increase in the production of one good.

From the above PPF, an increase in production of one unit of consumer goods causes an opportunity cost of two units of capital goods. Each subsequent production of one additional unit of consumer goods will have a constant opportunity cost of two units of capital goods. A straight line PPF is also known as a constant PPF.

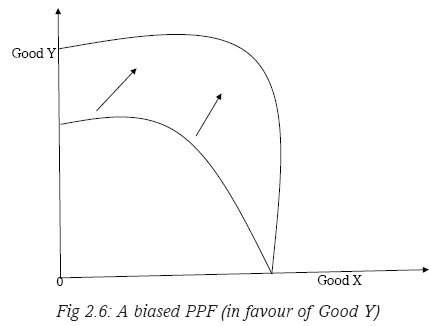

4. Biased PPF: This is a PPF that shifts outwards in favour of one commodity only. In this case, the PPF shifts outwards more in one direction than the other. This is caused by improvement in technology and increased factors of production that are in favour of one commodity.

The above illustration shows an increase in production of Good Y while there is no increase in production of Good X. This implies that the improvement in technology and increase in resources caused increase in production of Good Y only.

The above illustration shows an increase in production of Good X with no increase in production of Good Y. This implies that the improvement in technology and increase in resources was in favour of production of Good X only, causing an increase in production of Good X.

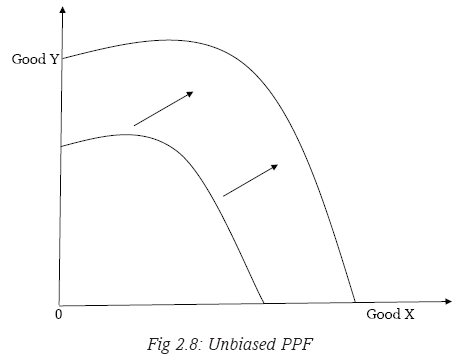

5. Unbiased PPF: This is the PPF that shifts evenly such that, there is an increase in production of both goods. This therefore implies that an improvement in technology and increase in resources favours both goods, thereby causing an increase in production of both Goods X and Y.

2.5: ECONOMIC QUESTIONS

Case study

Inyange Industries Ltd is a firm that deals in production of milk, ghee, juice and bottled water. In starting the firm, proprietors made a number of choices concerning its location, the tools and human resources to employ, the time to engage in production, and the kind of goods to produce. They also identified the consumers of their products.

In groups of five, identify and discuss the various economic questions, using the above case study.In allocating resources in the production of goods and services, countries and production firms face a number of fundamental economic questions. These fundamental economic questions include:

a) What to produce

Here the firm needs to decide on the nature of the goods to produce. The firm may decide to produce capital goods or consumer goods.b) How to produce

The producer has to decide on the methods and techniques to be used in the production process. The producer may decide to use capital intensive techniques of production or labour intensive techniques of production. The technique of production minimises costs while at the same time maximises the level of output.c) When to produce

The producer is required to decide whether to produce now or to produce in future. The producer is normally guided by the demand for the products in the market. The best time for production is when the demand for the goods or services is the highest.d) Where to produce

The producer has to determine on the location of his or her firm or industry. The location will depend on availability of the market, the source of raw materials, security and transport and communication networks. All in all, a thorough assessment of the impact of that firm to the environment must be carried out and evaluated.e) For whom to produce

The producer considers the target consumers that will use the goods to be produced. The produce may be for the young, the rich, the poor, the rural people or for the urban people.Unit Summary

The following fundamental economic principles were discussed:

• Scarcity; the limited supply of resources in relation to the unlimited wants.

• Choice; the act of making the right decision at the right time so as to use limited/scarce resources to satisfy unlimited wants.

• Opportunity cost; the second best alternative foregone when a choice is made.

• Production possibility frontier (PPF), or transformation curve or the opportunity cost curve; the locus of points showing the possible combinations of two goods that can be produced when all resources are fully utilised.

• Assumptions of the PPF such as:

(a) Assumes that only two commodities are produced.

(b) Assumes that the level of technology is fixed.

(c) Assumes that all resources are fully utilised.

• Economic questions such as:

(a) What to produce

(b) How to produce

(c) when to produce

(d) where to produce

(e) For whom to produceUnit Assessment 2

1. What are the fundamental economic principles?

2. With the help of the PPF, explain the relationship between the fundamental economic principles mentioned above.

3. How does the PPF explain economic growth or decline in the country?

4. Discuss the major economic questions that an entrepreneur has to answer as he or she prepares to engage in production. Present a report to your class.UNIT 3 NATURE AND SCOPE OF ECONOMICS

Key unit competence: By the end of the unit, you should be able to describe the nature and scope of Economics as applied in various domains.

3.1. NATURE OF ECONOMICS

Activity 3.1

(a) In groups of five, debate why you would call History an arts subject and Biology a science subject.

(b) Using the knowledge derived from the debate in (i) above, discuss why Economics is an arts and a science subject.

(c) Make a presentation to the whole class after the discussion.In this unit, we are concerned with the question: ‘Is Economics an arts subject or a science subject?’ We shall look at the methodologies used by economists to arrive at their conclusions so as to answer this question. The unit is also concerned with the substance of Economics.

Scholars such as Lionel Robbins, J. B. Says and J. S. Mill, in their definitions of Economics, look at Economics as a science.

J S Mill defines Economics as ‘a practical science of production and distribution of wealth and problems involved in production and distribution.’

Lionel Robbins defines Economics as ‘a science that studies human behaviour as ends and scarce means which have alternative uses.’J B Say talks of Economics as ‘a science of production, distribution and consumption of wealth.’

From the above, we can conclude that Economics is a social science subject. It falls in the same category as Psychology, Political Science and Sociology.

As a social science (arts), Economics studies human beings and the decisions they make to influence the economic environment of the society they live in. It uses scientific inquiry based on observation, and deductions to build models that can explain phenomena.As a science subject, Economics uses scientific approaches when establishing truths about an economic event. Economics defines concepts and quantifies them for purposes of evaluation and testing.

Hypotheses are developed from the scientific approach used, which stand periods of time to become laws, principles, and theories that explain economic behaviours of individuals, groups, and societies. It uses data into the theories developed to test and predict behavior.

3.2 POSITIVE AND NORMATIVE ECONOMICS

Activity 3.2

In groups of five, read through the following statements:

(a) (i) Workers are paid good salaries.

(ii) HIV/AIDS kills many people in Sub Saharan Africa.

(b) (i) Workers should be paid good salaries.

(ii) Everybody should learn how to save and invest.

What is the difference(s) in the above statements?

Identify the statements that are objective and give what actually happens on the ground.

What can you say about the other statements?Positive Economics is a branch of Economics that studies variables the way they are, that is, the way they exist in real life. Positive economics is factual and can be verified. It uses objective explanations. For instance, a statement like ‘Prices for agricultural products fluctuate frequently’ is a positive statement.

Normative Economics is a branch of Economics that studies variables the way they ought to be, as a desirable condition. It uses subjective explanations. For instance, a statement like, ‘Prices in the market should be stable,’ is a normative statement.

3.3. ECONOMIC VARIABLES

Activity 3.3

Twahirwa is a commercial Irish potato farmer in Musanze District. His target is to produce high quality potatoes in large quantities.

In groups of five:

(a) Explain how the following will affect his anticipated yields.

(i) A favourable season.

(ii) Use of improved seeds and firm tools.

(iii) The price of Irish potatoes.

(iv) Government legislation.

(b) On which of the above variables does Twahirwa have control?

(c) Analyse and find out whether a change in the amount of output

produced can have an influence on the four variables.A variable is a factor that can change. A variable is measurable. Examples of variables include prices of the commodities, government policies and amount of output produced.

These variables can either be endogenous (dependent) or exogenous (independent).Endogenous factors originate from within the system. Exogenous factors originate from outside the system. Changes in the exogenous factors affect the endogenous factors. Changes in the endogenous factors may not influence the exogenous factors. The amount of Irish potatoes produced (in the above activity) is an endogenous variable. It is influenced by seasonal changes. Factors that originate within the economy and affect it but can be controlled are endogenous.

Exogenous factors are not affected by changes in the endogenous factors. For instance in the above activity, change in season is an exogenous variable. It is not influenced by change in output. Factors that originate from outside the economy and are beyond the economy’s control are exogenous.

3.4. BRANCHES OF ECONOMICS

Activity 3.4

In groups of five:

(a) List the different parts of the body.

(b) Brainstorm and explain how each part functions independently.

(c) Discuss how all parts of the body work together to make the body function.

(d) Relate the discussion to Economics and its branches: microeconomics and macroeconomics.Microeconomics is a branch of Economics that studies individual units of the economy. Such units may be households, firms or prices of commodities, among others. It looks at how these single units function individually. It looks at areas such as household decisions on consumption, the firm’s production and profit maximisation decisions, market prices and their regulations.

Macroeconomics is a branch of Economics that studies all units of the economy as an aggregate. It looks at the economy as a single functioning unit. This is because the different individual units of the economy are interrelated. It looks at areas like the causes of economic growth, changes in interest rates and their effects on the economy, effects of monetary and fiscal policies.

Activity 3.5

(a) Do you like the view in the picture above?

(b) Name the natural features identified in it.

(c) How important are the features in today’s economic world?

(d) What can be done to protect such features?Unit Summary

In this unit, the following were discussed:

• Economics as an art subject.

• Economics as a science subject.

• Positive economics.

• Normative economics.

• Economic variables such as endogenious and exogenious factors as variables.

• Branches of economics as mircoeconomics and macroeconomics.Unit Assessment 3

1. Differentiate between the following:

(i) Positive economics and normative economics.

(ii) Endogenous factors and exogenous factors.

(iii) Microeconomics and macroeconomics.

2. Read through the following and classify each statement as either microeconomics or macroeconomics.

(i) Study of the functioning of prices in an economy.

(ii) Rwanda’s economy is growing at a fast rate.

(iii) Study of employment levels and unemployment levels in the economy.

(iv) Study of the operation of firms.

(v) Taxation

(vi) Every member of labour force in the country should be employed.UNIT 4 EQUATIONS AND FRACTIONS IN ECONOMIC MODELS

Key unit competence: By the end of this course unit, you will be able to describe economic phenomenon using mathematical tools

4.1 EQUATIONS IN ECONOMICS

4.1.1 Linear equations and linear graphs

(a) Linear EquationsActivity 4.1

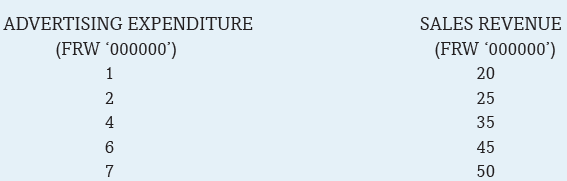

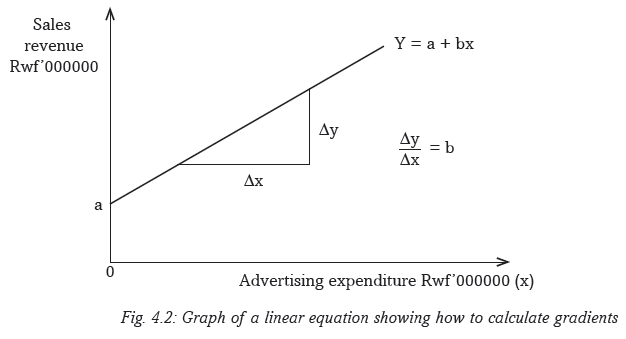

The table below shows the sales revenues and advertising expenditures of Quality Supermarket.

In groups of five,

(a) Explain the relationship between advertising and sales as reflected in the above table.

(b) Determine the sales revenue generated at FRW 9 million and FRW 10 million levels of advertising.

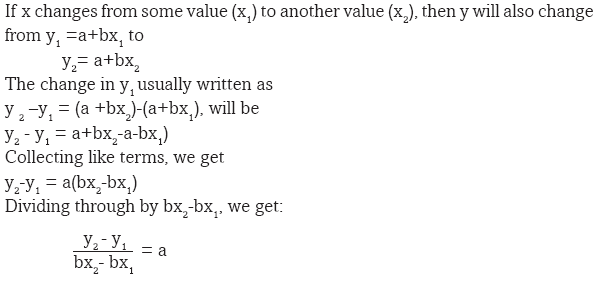

Give reasons for your answer.Facts

From the table given in the question above, we can see that the supermarket makes more sales as a result of higher advertising. This shows a relationship between advertising expenditure and sales revenue. We can say that the higher the advertising expenditure, the higher the sales by the supermarket.Sales revenue therefore depends on advertising. In this case we call sales revenue a dependent variable while advertising an independent variable. This is because sales depend on advertising. Advertising is independent because it is not being affected by sales or any other factor. We will come across such cases in Economics and Mathematics more often.

This relationship can be expressed as an equation, as follows:

Y =a +b x, Where

y is the dependent variable (sales revenue in this case).

x is the independent variable (advertising in this case).

a is a constant figure. It represents the amount sold without any form (at zero level) of advertising i.e. If x=0, y =a. In the case on page 41, Activity 4.1, sales made without advertising are lower than 20,000,000 FRW. (Assuming advertising begins at 1 million FRW).

b is a coefficient. It shows how much y will change every time x changes by one unit.

The above case is an example of a linear equation. Linear equations are referred to as first degree polynomials.

From the table above, following advertising and sales figures of Quality Supermarket, we can see that sales increase by 5 million from 1 million advertising expenditure.

Therefore, at zero advertising expenditure, sales would be 20m-5m=15 million.

Therefore our equation, y =a+bx

Would be y= 15+5x.Given this equation, we can be able to find out:

The amount of sales arising from a given expenditure in advertising.

The amount of advertising necessary to generate a desired amount of sales revenue.Example 1

The sales revenue generated by 10 million advertising expenditure would be:Y=15 +(5x10)

=15 +50 =65mExample 2

If Quality Supermarket targeted sales revenue of 75 million FRW, determine the advertising expenditure that it would have to incur.Solution

y = a + b x

75 =15+5x

60=5x

X=12

Therefore the amount of advertising needed to yield 75 million FRW would be 12 million FRW.(b) Sketching linear graphs

The data from the table on sales and advertising for Quality Supermarket (Activity 4.1) can be plotted on a graph.The graph has two sides called axes. The upright side (side having an arrow pointing up) represents the vertical axis. The bottom side (side having an arrow pointing to the right) represents the horizontal axis.

The values of the dependent variable (sales revenue in this case) will be represented on the horizontal axis. The values of the independent variable (advertising expenditure in this case) will be represented on the vertical axis.

Values on the horizontal axis increase as we move to the right, from the point of origin. Similarly, values on the vertical axis increase as we move upwards, from the origin.

In the case of Quality Supermarket, y stands for sales while x stands for advertising.

Each row of the table gives us a pair of numbers, or a combination of x and y.

We have 1 and 20, 2 and 25 and so on.These pairs are written as (1, 20), (2, 25)...

To plot the pair (x,y) begin at the origin where the two axes meet. Count rightward x units on the horizontal axis and then count y units above this level, parallel to the vertical axis. Mark this spot. Continue with the process for the different pairs of x and y. After identifying and marking all the pairs, then connect the pairs. This can be done by drawing a line that passes through all the points.Using the example of Quality Supermarket, all the pairs are along the same straight line.

From our equation y= a+bx, ‘a’ represents the point at which the line joining the paired points cross the dependent line. In economical and mathematical terms, we say the derived line intercepts the vertical axis at point a. ‘a’ is therefore referred to as the vertical or y intercept.

‘b’ on the other hand is the slope of the line.

The slope ‘b’ tells us the rate at which the y variable changes with a unit change in x.

Recall

What do we call ‘b’ in Mathematics?Note that ‘a’ has no effect on the slope of the graph.

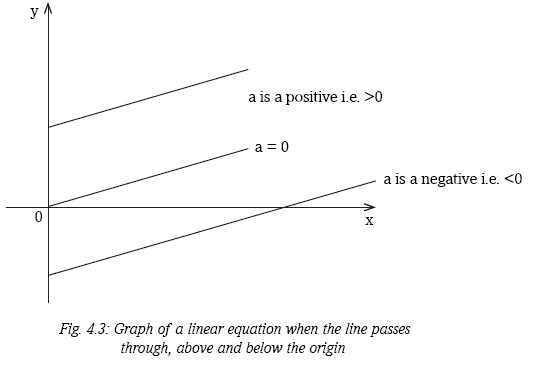

Let us point out that the value of ‘a’ can be either positive, negative or zero.

When the value of ‘a’ is positive, the graph will intercept the vertical axis above the origin.

When the value of ‘a’ is negative, the graph will intercept the vertical axis below the origin.

When the value of ‘a’ is zero, the graph will intercept the axis at the origin.

Examples of linear equations in economics

There are several types or examples of linear equations as used in Economics.

The main examples are:

1. The production possibility frontier; a graph that shows combinations of goods and services that can be produced with a given level of resources.

2. The demand function; an equation showing the various quantities of goods purchased by customers at given prices.

3. The supply function; an equation showing the various quantities of goods brought to the market by suppliers at a given market price.

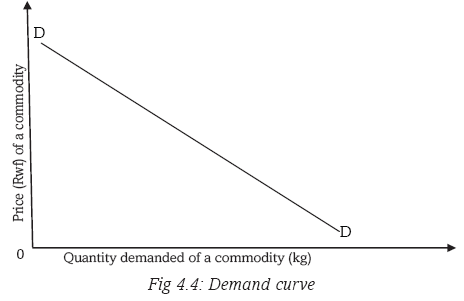

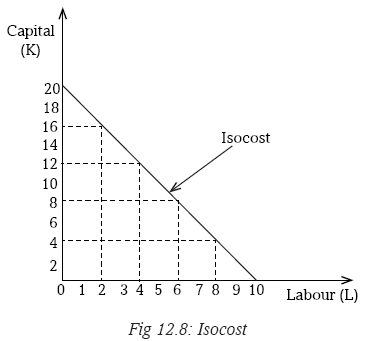

4. Isocost line; a graph showing different combinations of labour and capital that can be purchased by a given firm.The demand curve

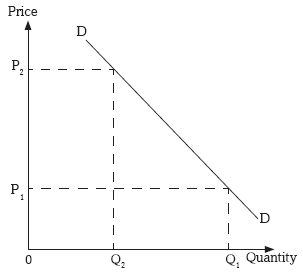

The demand curve shows the relationship between the quantity demanded of a commodity and the price of that commodity. This is a negative slope. It shows that an increase in the independent variable (price) leads to a decrease in the dependent variable (quantity demanded).

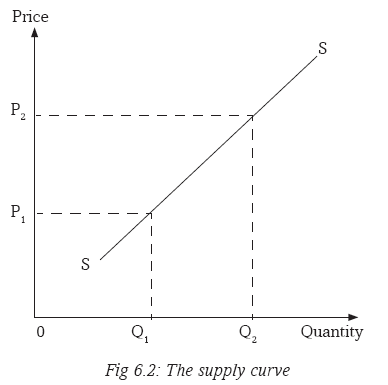

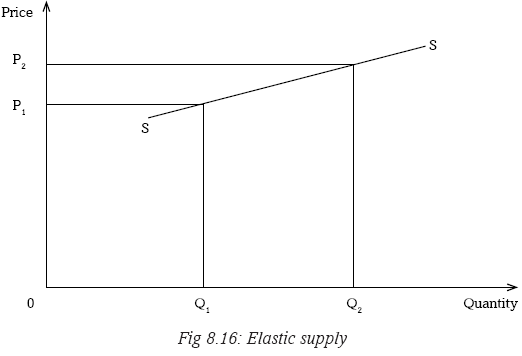

The supply curve

The supply curve shows the relationship between the quantity supplied of a commodity to the market by suppliers and the price of the commodity. This has a positive slope. It shows that both the price (the independent variable) and quantity supplied (the dependent variable) change in the same direction.

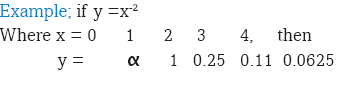

4.1.2 Non linear equations and non linear graphs

Non-linear algebraic equations are polynomial equations of a degree that is greater than one. They are mathematical relationships that describe non linear graphs. They take various types. For instance, we have the following main non- linear equations:

(a) Polynomials

(b) Logarithmic equations

(c) Conic equations

(d) Exponential equationsActivity 4.2

The following tables show the changes in variable Y as a result of changes in variable X.Table 1

Table 2

(a) Sketch the information given in Tables 1 and 2 in their respective charts.

(b) In groups, discuss the relationship between the two variables as revealed by the charts.4.1.2.1 Features of non linear equations

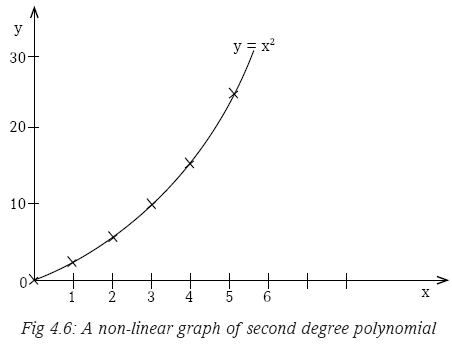

1. In non linear equations, the independent variable has a certain power to it. If we have y as the dependent variable and x as the independent variable, the relationship could be:

2. The features of non linear equations vary, depending on the gradient or slope of the curve.

3. Where there is one independent variable whose power is greater than one,the dependent variable will increase at an increasing rate as the power of the independent variable rises.

For example if

The graph from the equation above would curve upwards. As y increases at a faster rate than x. This is shown below.

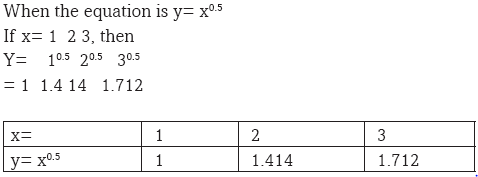

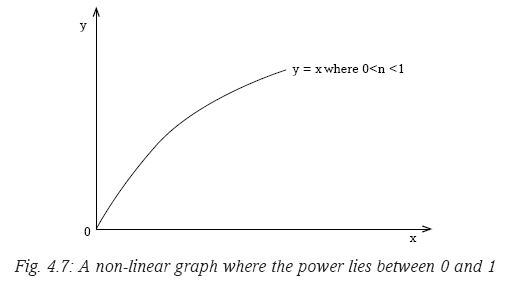

4. Where the power of the independent variable (x) lies between 0 and 1, then the value of y will also be increasing as x increases.

Example

5 Where the power of x is negative with the value of x being positive, the graph derived would slope downwards. This graph would take a convex curve shape.

In this case, the dependent variableincreases as the independent variable (x) decreases.

Fig. 4.8: A non-linear graph where the power is negative (less than zero)

4.1.3 Simultaneous equations

Specific objectives

By the end of this sub-unit, you should be able to:

(a) Identify different methods of solving simultaneous linear equations.

(b) Solve simultaneous linear equations.Activity 4.3

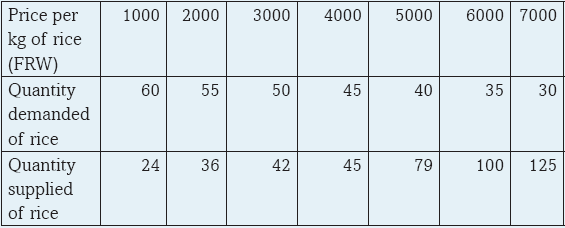

The following table shows the demand and supply conditions relative to the change in the price of commodity x.

(a) In groups of five, discuss the relationship between:

(i) The price and the demand for the commodity.

(ii) The price and the supply for the commodity.

(b) Sketch the demand and supply relationships in a chart.4.1.3.1 Necessary conditions for simultaneous equations

These conditions include that:

(i) There should be more than one functional relationship, between a set of specified variablessuch as x and y or q and p.

(ii) That all the functional relationships are in linear form.It is then that we try to find the value of the unknown variables in the equations.

In the case where we have only two variables in the equations, it is then possible to subject the equations to graphical solutions.

Simultaneous equations can be solved using various methods.4.1.3.2 Methods used in solving simultaneous equations

a) The substitution methodThis method entails representing one unknown in terms of the other unknown.

Example

Find the values of x and y in the following equations using the substitution method.

20 x + 6 y =500…………….. (i)

10x – 2 y = 200……….......... (ii)If we arrange equation (ii) so as to define or represent y in terms of x, we get:

10x - 200=2y

Dividing through by 2, we get:

5x-100 =yWe then substitute the new value of y (obtained in equation (ii)) in equation (i) as follows:

20x +6y=500 .....(i) now becomes

20x +6(5x-100) =500 ........(iii)

On opening the brackets, we get:

20x +30x -600=500

On collecting like terms, we get:

50x=1100

x=22We would then substitute the value of x in equation (ii) to get:

220-2y=200

220=200 +27

20= 2y

y =10b) Row operation method

We can also use the row operation to get the same result. Using the above example,

Where 20x + 6y =500 and ………..(i)

10x – 2 y =200……….. (ii)

Multiplying equation (ii) by 3, we get:

30x - 6y=600………… (iii)

Adding equation (iii) to equation (i), we get

50x =1100

x =22We then substitute for x in any of the equations to get y=10.

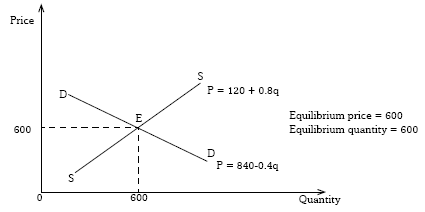

We can apply the concept to solve for demand and supply relationships, when given the demand and supply functions.Note: Unlike in the usual linear relationship between the dependent and independent variables, in this case, our relationships are expressed in a reversed manner. For example, p=f(q) and not q=f(p). The dependent variable is on the horizontal axis while the independent variable is on the vertical axis. This is because price is normally measured on the vertical axis. The principle is the same and the idea is to get the true relationship of the variables.

Therefore, if we are given the following demand and supply equations:

p=840—0.4q as a demand schedule

And p =120+0.8 q as a supply schedule,

We can solve for both p and q

(i) Multiplying demand schedule by 2, we get:

2P+1680 -0.8q

(ii) Adding the new demand schedule to the supply schedule, we get:

3P=1800

P=600(iii) Substituting for P in any of the equations, we get:

600=120+0.8q

0.8q=480

8 q =4800

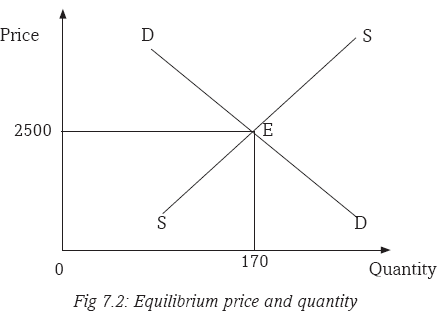

q=600We could also use the equation method to solve for the demand and supply quantities such that:

840-0.4q=120+0.8q

720+1.2 q

q=600Substituting for q in any of the two equations, we get:

P=600

Fig. 4.9: Graph showing equilibrium price and equilibrium quantity

Activity 4.4

Taking P for price and the other unknown for quantity, solve the simultaneous linear equations. They represent the various demand and supply functions we come across in our daily lives. Illustrate your findings on graphs. Make class presentations.Group A

1. Q = 3P + 2, Qs = 2 - P

2. 3P + 7Q = 10, 4P - Q = 3

3. 5P + 10Q = 10, 2P - Q = 1

4. 2P + Q = 7, 3P + Q = 10Group B

5. 5P + 3Y = 7, 4P - 5Y = 3

6. 4P + 6Q = -13, 3P - 5Q = 14

7. 6P + 3Q = 1, 4P - 2Q = 2

8. 3P + 5Q = 12, 6P - 4Q = 3Group C

9. 6P + 3Q = 2P + Q = 1

10. 2P + Q = 7, 4P + Q = 11

11. 5P + 7Q = 12, 6P - 3Q = 3

12. 2P + 3Z = 2, 6P - 12Z = 13Note: You can use any of the above methods earlier learned, or any of these methods.

(a) Elimination method

(b) Matrix method

(c) Graphical method

(d) Crammer’s method

(e) Inverse methodOther examples of non linear graphs in Economics

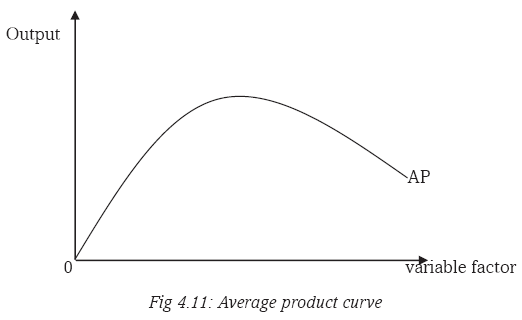

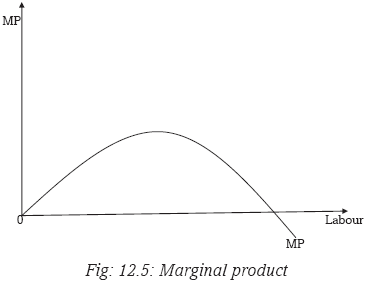

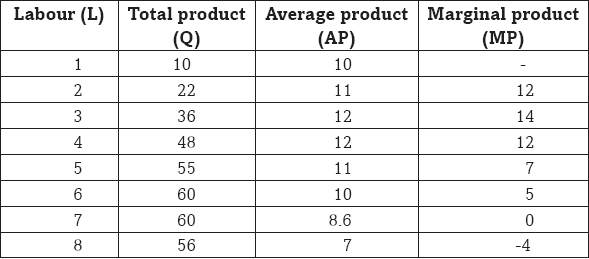

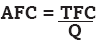

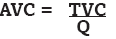

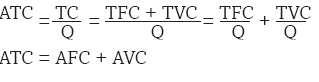

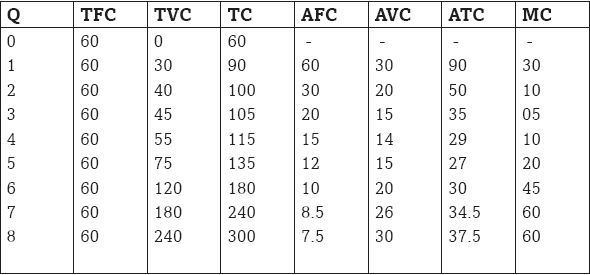

a) Average cost curve

The average cost curve (AC) shows the relationship between the output produced and the variable cost spent on producing each unit of this output.

b) The average product curve

The average product curve (AP) shows the relationship between the variable factor employed and the output produced from each unit of the variable factor.

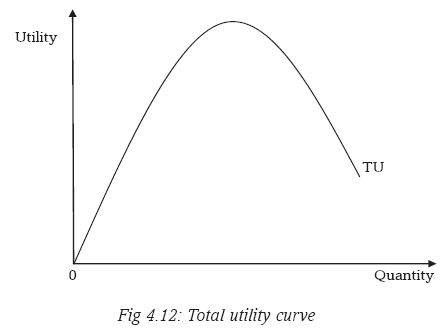

c) Total utility curve

4.1.4 Differential equations and graphs

A differential equation is a mathematical equation that relates some function with its derivatives. Functions are usually represented by physical quantities. Derivatives represent the rates at which the physical quantities change. Thus differential equations define the relationship between the two.

Differential equations have types. For instance:

• Ordinary differential equations.

• Partial differential equations.An ordinary differential equation (ODE) is an equation that contain a function of one independent variable and its derivative. These equations can either be linear or non linear. For instance,

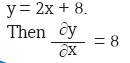

A partial differential equation (PDE) is a differential equation that contains unknown multivariable functions and their partial derivatives. These equations are used to formulate problems involving functions of several variables. For instance,

y = 2x∂x + 84.1.4.1 Linear and non-linear differential equations

Maxima and minima pointsMaximum (maxima) and minimum (minima) points have an important application in Economics.

Economic application

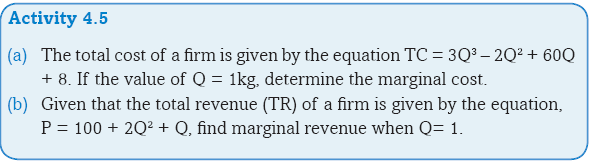

Example

Given A total revenue function

TR = 120Q-2.5Q2

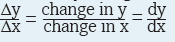

Find marginal revenue function.The derivative is denoted dy or f(x) and is given by dividing the change in y

dx

variable by change in change in x variable.

Rules of differentiation (Elementary level/basic level)

1. Constant rule

if given a function y=k where k is a constant, then

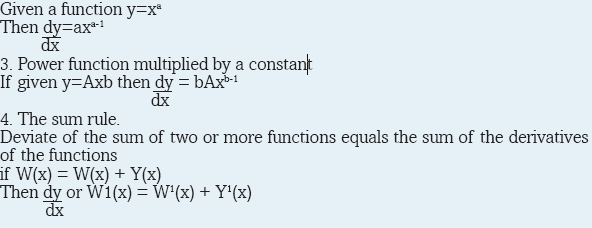

2. Power function rule

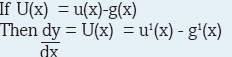

5. The difference rule

The derivative of the difference of two or more functions equals the difference of the derivatives of the functions.The derivative of the difference of two or more functions equals the difference of the derivatives of the functions.

Both ordinary and partial differential equations are broadly classified as linear and non linear equations. A differential equation is linear if and only if the unknown function and its derivative appears to be power 1. Otherwise it is non linear. For instance,

dy = 8 is a linear differential equation.

dx

y = 8x + C is a non linear differential equation.In Economics, differential equations are essential in computing marginal values of a nature

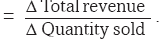

Marginal revenue

This is the additional revenue accruing to the firm from the sale of an additional unit of output.

This is the additional revenue accruing to the firm from the sale of an additional unit of output.Marginal product

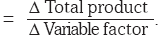

This is the additional/extra units of output that are derived from the employment of an additional unit of a variable factor.

This is the additional/extra units of output that are derived from the employment of an additional unit of a variable factor.Marginal cost

This is the additional cost of producing and extra unit of output.

This is the additional cost of producing and extra unit of output.4.2 FRACTIONS IN ECONOMICS

Specific Objectives

By the end of this sub - unit, you should be able to:

(a) Express the ratios of quantities of various items or variables in Economics.

(b) Determine the proportions of given quantities of an item relative to the whole amount of the item.

(c) Calculate the percentages of given quantities of economic variables.

(d) Derive the reciprocals of given numbers of economic variables.

(e) Calculate averages and index numbers from given economic data.

(f) Derive absolute values from given values.Activity 4.6

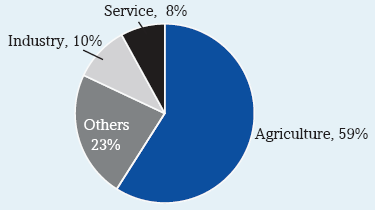

The annual budget for country X was 550b US $. It was allocated as shown below.Sectoral budgetary allocation

Use the figures above to answer the questions that follow.

(a) Determine how much was allocated to the service sector.

(b) Express the agricultural allocation in billions as a ratio of the total budget.

(c) What fraction of the budget went to other sectors?

(d) What proportion of the 550b $ was allocated to the industrial sector?

(e) Agriculture was allocated a lion’s share of the budget. In your own view, why do you think could have been the reason for this.

(f) Identify the sectors that may be included in the ‘others’.

(g) Would you take the above to be a good budgetary allocation to suit your country? Support your answer.Facts

Fractions are numbers that are expressed with numerators and denominators. The numerator represents part of a whole unit. In a class for instance, if you are forty students and half of them are boys, then we will say 20 out of 40 or half the class are boys.Activity 4.7

Simon, a large scale farmer, has the following livestock on his farm:

1) 50 dairy cattle, 40 of which are currently being milked;

2) 100 beef cattle, 60 of which are cows;

3) 200 goats, 40 of which are he- goats.Required:

(a) Determine:

i) The total number of livestock that the farmer has.

ii) The total number of male livestock.

iii) The total number of cattle.

(b) In groups, discuss the reasons that may have made Simon to:

i) Keep more goats than cattle on his farm.

ii) Keep more beef cattle than dairy cattle.4.2.1 Ratios

Activity 4.8

In groups of five, work out the following:

(a) For a sugar-producing firm, the ratio of total fixed costs to total costs is 4:10. Determine value of its total variable costs if it spends 40 millions FRW as fixed costs.

(b) In a class, the ratio of girls to boys is 7:3 and the ratio of day scholars to borders (both girls and boys) is 2:8. If the number of boarders is 400 students, determine the number of and girls in this class.

(b) Christine works with Rwanda Environment Authority and consumes 400000 FRW of her net salary per month. If the ratio of her savings to net salary is 6:20, determine how much she saves.Facts

The question that we need to answer here is, what is a ratio?

Simply stated, a ratio is a number representing a comparison between two things that are in a way related. For example, if we look at the farm of Simon in the activity given at the beginning of this unit, we see that there are 40 dairy cattle that are being milked out of 50. Therefore, the number of dairy cattle that is not being milked is 10. From this information, we can derive the following ratios:i) The ratio of the number of cows being milked to the total number of dairy cattle is 40:50. This can also be expressed in the form of a fraction as 40/50.

ii) The ratio of the dairy cattle that are not being milked to those that are being milked is 10:40. This ratio can also be expressed as 10/40.

iii) The ratio of the number of the cattle that are not being milked to the total number of the dairy cattle is 10:50. This ratio can also be expressed as 10/50.

The ratio derived can be further simplified to the lowest form possible such that in i), we would get a ratio of 4:5, in ii) we get 1:4, while in iii), we get 1:5.Recall

From the information given in the activity at the beginning of this unit, determine:

(a) The ratio of beef cattle to the total number of cattle in the farm.

(b) The ratio of bulls to cows in the case of the case of the beef cattle in the farm.

(c) The ratio of cattle to goats in the farm.

(d) The ratio of the hegoats to the shegoats.4.2.2 Proportions

A proportion is the quantity of a given item that is part of the whole amount or number of that item. For example, supposing Juma who earns $200 a month saves $50 every month. Then the proportion of income saved by Juma is 50 out of 200, or 5 out 20 or further simplified to 1 out 4. We can therefore say that out of every $1 that Juma earns, he saves $0.25. This is the marginal rate of saving by Juma.At the macro level, we could also be able to determine the proportion of the total budget that the Government spends on either education or on health or on armament. In this way, we could be able to gauge whether resources are being optimally allocated or not.

Activity 4.9

Visit the National Institute of Statistics Rwanda website [statistics/] and write short notes after discussion on the following:

(a) Contribution of each of the following sector to cross domestic product (in percentage) of ratio.

- Agriculture

- Industry

- Services(b) Percentage of population living below poverty line.

(c) Economic growth for year 2013, 2014.

(d) Population growth, fertility rates.

(e) Gender composition of total population.

(f) Literacy levels.4.2.3 Percentages

Activity 4.10

In groups of five, work out the following:

(a) Umuhoza Patience spent 20000 FRW of her monthly salary on transport. Express this as a percentage of her salary if she earns 250000 FRW monthly.

(b) In a class of 40 students, 25 are girls. Express the number of boys as a percentage of the whole class.

(c) Given that the price of commodity X increased from 500 FRW to 850 FRW per unit, what is the percentage change in price of commodity X?