General

- Entrepreneurship S1 SB File Uploaded 17/01/22, 14:47

- S1: Entrepreneurship TG File Uploaded 11/08/22, 21:39

Unit 6: Initiation to accounting

Key unit competence: To be able to analyse the importance of accounting to the business.

Every day people spend money. Usually we receive a till slip or a receipt. A receipt is proof that we have paid for the goods or services that we bought.Collect receipts from your family or a business and bring them to school. In class, discuss the receipts.

• What information is on the receipts?

• Why do we keep the receipts?

• How can the receipts help us to manage money better?

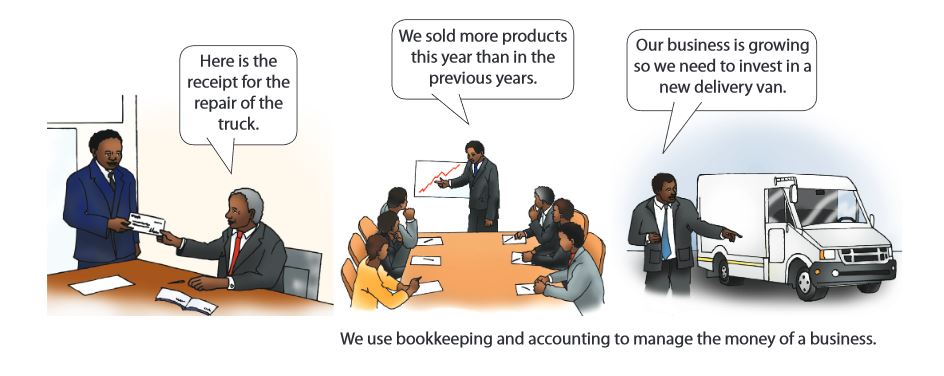

Accounting is the process of keeping financial accounts. When we buy a product or service we receive a receipt. The receipt tells us what we have bought and how much money we have paid.In a business we must write a receipt when we sell a product or service.

A business owner must also write a pay slip that shows each employee how much money they have earned and what deductions have been made.When we keep the receipts for goods and services that we have bought and add up the amounts on the receipts, we can see how much money we have spent. From the receipts that we give to our customers, we can also see how much money we have earned.

The system that we use to add up receipts and store the information is called bookkeeping.\

Bookkeeping is a very useful tool. It is a record of the money that we spend and receive.

Accountants use the records from bookkeeping to draw up financial statements about how the business managed its money.

They also use the information to plan for the future. This is called accounting.

The difference between bookkeeping and accounting Bookkeeping

is keeping a record of the money that we have spent and received.

Accounting uses the information from bookkeeping to make financial reports, often called financial statements. These reports have information that the owner of the business can use to plan for the future. The statements are also important because the government and other stakeholders want to see how much money the business makes.

1. Explain the difference between bookkeeping and accounting.

2. Describe the importance of bookkeeping and accounting for:

a) a family

b)business

c) school.

3. Do the people in the images below use bookkeeping or accounting? Explain your answer.

Accounting is an important tool for a business. We use accounting to control and plan what happens to the money in a business.

Profit and loss

When we do bookkeeping for a business, we add up all the money that we receive and all the money that we spend. We use accounting to calculate if we made a profit (we received more money than we spent) or a loss (we spent more money than we earned).

Evaluating a business

Accountants analyses and interpret financial information. This information helps business owners and managers to make good decisions.Accounting tells us if the owner invested his or her own money or if the money is a loan from a bank. We can see if the business is growing every year and if it is making a profit or a loss. This information helps us to make important decisions.

For example, if we are selling more and more products every year, we can invest in a truck to deliver the products.We can also see how many products we need to sell before we start making a profit.

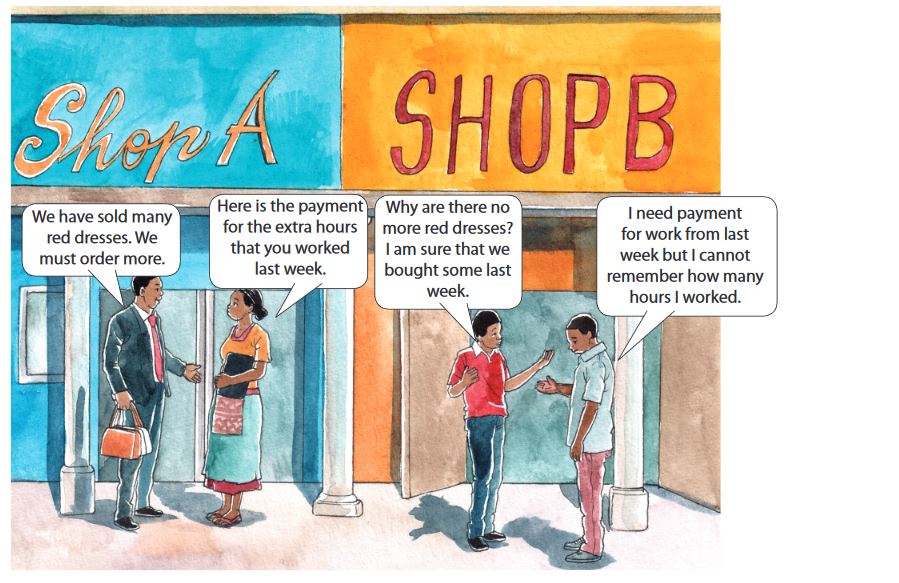

Study the two pictures.

Accounting can help us to make important decisions.

1. How does the owner of Shop A know that the red dress is popular?

2. What do you think happens when there are no more red dresses in Shop B?

3. How does accounting help the person in Shop A to pay out the correct money for work done by her employees?

4. If Shop B simply adds RWF 100 to the cost of, for example, a handbag, do you think that they make a profit? Explain your answer.

5. Use Shop A and Shop B to explain why bookkeeping and accounting are important for a business.

Accounting is a control and information tool for a business. Many different people use the information from bookkeeping and accounting.The people that own or work for the business are called internal users. People who need to see accounting information but work outside the business are called external users.

Internal users of accounting

The owner of a business is an internal user. The owner uses the information from bookkeeping and accounting to make important decisions about the business.An employee is also an internal user. As an employee you need to know how much salary you earn. Sometimes an employee like a salesperson earns commission. This means that the salesperson earns a certain amount for every product he or she sells.

We use bookkeeping to determine how many products a salesperson sells.

A shareholder is a person who owns part of a business. Shareholders receive some of the profit of a business. The share of the profit depends on how much of the business the shareholder owns.A manager also needs to control how a business spends or earns money. Managers are therefore also internal users.

1. List three different internal users of accounting in a business.

2. Shema is a shareholder in a business. He owns 25% of the shares. At the end of a year, the profit of the business is RWF 1,000,000. How much money will Shem receive?

3. Bwiza is a manager of a business that sells earrings. Suggest accounting information that Bwiza can use to manage the sales of earrings in the business.

4. Jabo is employed by a business where he drives a delivery van. He says that he does not work with the money of the business, so he is not an internal user.

Explain to Jabo why employees are internal users of accounting.

External users of accounting

A business needs to keep a record of how it spends money and makes money. This information is mostly secret. No one outside the business knows this information, except for external users.External users need to know accounting information for different reasons.

Government authorities

The government authorities of Rwanda are external users. Every business in Rwanda pays tax to the government. This tax is used to build roads, schools and hospitals and to provide many other services in Rwanda. The Rwanda Revenue Authority (RRA) collects the tax and therefore needs to know the information from a business so that the business can pay the correct amount of tax.

Other external users

Sometimes a business also has other external users. If a business needs a loan, the bank becomes an external user. The bank wants to see the accounting information to decide if the business can afford to pay back the loan.A supplier can also be an external user. If a business wants to buy products on credit, then the supplier needs to know that the business will have enough money to pay for the products in the future.Customers are also external users of accounting. They use accounting information to manage their monthly expenses. Investors are also external users; they use accounting to manage the money they have invested in different businesses.

Case study

Read the case study as a group and then answer the questions.

Shema borrowed money to buy his truck. He has a debt to pay back at the bank.

Shema borrowed money to buy his truck. He has a debt to pay back at the bank.Shema is the owner of a transport business. He transports fruits and vegetables from farmers to Kigali. To buy his trucks, he borrowed money from the Bank of Kigali. He employs five drivers.

Questions

1. Why are bookkeeping and accounting important to Shema?

2. Identify internal and external users of accounting for Shema’s business.

3. Explain why each user you identified in question 2 needs the accounting information.

A business transaction happens when the business buys or sells a product or service. Business transactions can be cash or credit transactions.

Cash transactions

When we buy a product or service and pay at the same time, then we conduct a cash transaction. For example, if you go to a hairdresser and pay after receiving a haircut. When we conduct a cash transaction we can pay with cash (money that you hand over) or with a debit card.

Credit transactions

We can also pay on credit. This means that we pay for the product or service at a time in the future. Credit transactions are usually thirty days in the future. This means that we pay one month after we buy the product or service.When we buy on credit, the business must trust that we are going to make the payment.

Paying in installments

Sometimes we buy expensive things that we cannot pay for in one go. Then we can pay in installments. If an item costs RWF 100,000, then we can pay ten installments of RWF 10,000 each.When we use installment payments, we usually need to pay interest. For example, if an item costs RWF 100,000 with a 10% interest payment, then we need to pay ten installments of RWF 11,000 each. We will then pay RWF 110,000 for the item.

When we pay cash for an item, we need to save up the money first and then buy it.When we buy on credit, we can have the item straight away, but then we still need to pay later. We will also have to pay interest. This means that we pay more.

Copy the table below and describe the advantages and disadvantages of paying with cash and credit.

Modes of payment

We pay for cash transactions with cash. In Rwanda, we use Rwandan Francs. Our bank notes range from RWF 100 to RWF 5,000. A bank can also assist with making a payment from a bank account. We can ask the bank to transfer the money to another person’s or business’ account.We can use the Internet to make electronic payments. We can access the account using the Internet. Then we can transfer the money to another account.Sometimes we need to pay for an item before we receive it. This is called prepayment.

1. Role play a range of business transactions. Then ask your classmates to identify cash transactions, credit transactions and instalment payments.

2. Discuss different situations where your family has paid for different products or services. Explain which mode of payment they used and why. What was the advantage and disadvantage of this mode of payment?

Section A

Shema wants to start a new business. He wants to open a bakery that sells from a shop and delivers bread to supermarkets. To start his business he needs to invest in an oven, a delivery van, advertising, flour and other ingredients for his bread. He is renting a shop in the centre of Muhanga and wants to hire two bakers. Shema has been working for a baker for the past five years and has savings in the bank.

1. Shema would like to pay for the oven and the van with his savings, but he does not have enough savings. Explain why a new business needs financing. (5)

2. Shema’s brother wants to invest in his business.

a) What is the difference between debt and equity? (4)

b)List one advantage and one disadvantage of each option. (4)

3. How can Shema use accounting information to make decisions about his business? (5)

4. List two external users of accounting information for Shema’s business. (2)

[20]

Section B

Dianne is an entrepreneur who sells crafts at a market in Kigali.

1. Explain the difference between personal and business finance. (4)

2. Dianne wants to buy a new range of crafts. She can pay by cash or by credit. Evaluate the modes of payment by providing a table with disadvantages and advantages of each option. (8)

3. List three internal users of accounting and describe how each user makes use of accounting information to make decisions. (8)

[20]

Section C

Financial awareness is an important skill for every entrepreneur. Identify a savings goal. Then develop and design a personal savings plan. (10)

[10]

Total marks: 50