General

- Entrepreneurship S1 SB File Uploaded 17/01/22, 14:47

- S1: Entrepreneurship TG File Uploaded 11/08/22, 21:39

Unit 5 : Financial awareness

TOPIC AREA3 Financial information and decision making

Sub-topic area Managing finances

Unit 5 Financial awareness

Key unit competence: To be able to access finance and make financial decisions

Ruti is a learner. He lives far from his school and is planning to buy a bicycle.

Mugisha is a business owner. He delivers bread to many hotels and restaurants in Kigali and is planning to buy a delivery van.

Answer the questions about Ruti and Mugisha.

1. Why do you think that Ruti would like a bicycle?

2. Give ideas for how Ruti could pay for the bicycle.

3. Why do you think that Mugisha would like a delivery van?

4. Give ideas for how Mugisha could pay for the delivery van.

5. Discuss the difference between the cost of things that a private person would like and the things that a business needs.

6. What are the similarities between the things that a private person needs and the things that a business needs?

7. Do you think that a business and a private person obtain (get) money to buy items in the same way? Explain your answer.

Financial management

Financial management means how we obtain, budget, save and spend money. In this topic, we will discuss how to make decisions that have to do with earning and spending money. This is called financial management. Every person and every business needs to manage how they spend money effectively. Good financial management means ensuring that your income covers your expenses. If also means that you make decisions about where we get (borrow) money if you do not have sufficient money to buy the things that you want or need.

Make a budget

To make a budget we need to know where our money comes from. In a business, money can come from the sales of products or services. An individual usually earns money from a salary, or from providing goods or services. Finance is money or funds needed for business or personal reasons.To make a budget, we also need to know the cost of things that we need or want to buy. If we do not have enough money to buy the things straight away, then we have different options. We can first save the money. We can also obtain money from:

• other people who want to invest in a business

• loans.Obtaining money to buy things for a business or a private person is called financing.

Why do we need financing?

Many items that we want or need are very costly. Some things like a bicycle or a delivery van can help us to do the tasks that we need to do every day.It is not easy to save large amounts of money. We therefore use loans from banks or ask other people to invest in a business so that we can obtain the money. This is called getting financing.

Personal and business finance

Personal finance means to manage money and plan for the future of an individual or a family unit. An individual needs to manage the salary that he or she receives. Costly personal items include buying a home, a car or paying for an education. Individuals also need to save up for retirement.Business finance means to manage money and plan for the future of a business.A business earns money by selling goods and services. The business needs money to buy raw materials, rent or buy buildings and to buy the machinery needed to produce the goods and services. A business owner usually wants to grow the business and needs to plan how much money is needed in the future.

Study the images below and answer the questions that follow.

1. Explain the difference between personal and business finance.

2. What do the family members in the picture on page 64 need to save up for? How will these items benefit the family?

3. What does the business owner in the picture on page 64 need to save up for? How will these items benefit the business?

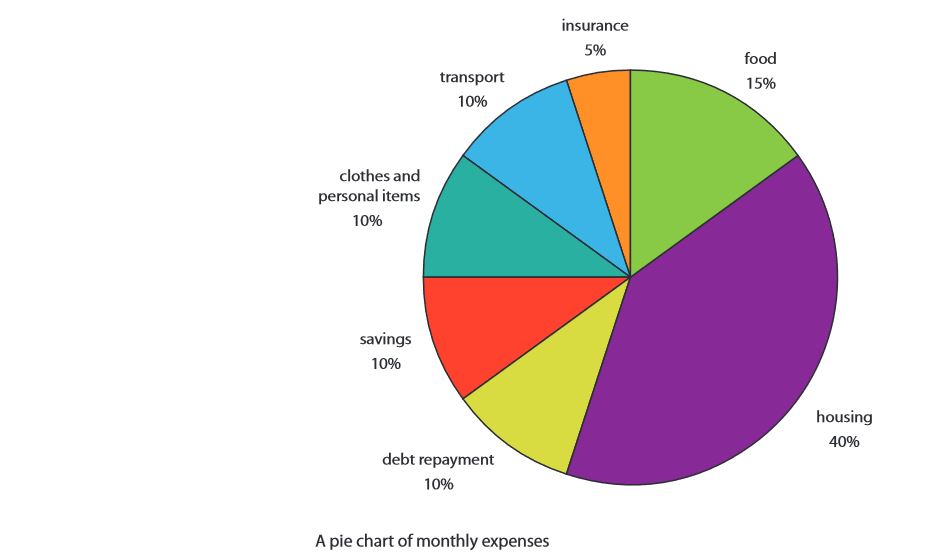

Ngoga is a young person living in Kigali. He has made a budget for his monthly costs. The pie chart shows the percentage of each cost.

1. What is Ngoga’s greatest cost every month?

2. What debt do you think that Ngoga has to repay? Make three suggestions.

3. Ngoga could buy more clothes if he stops his monthly savings. Explain why this is not a good idea.

How to access business finance

A business that needs money has two options. The owner can use his or her own savings. This is called equity. The owner can also borrow the money. This is called debt.Business owners can obtain money from:

• Personal savings. This is money saved up by the business owner.

• Loans from banks and micro lenders.

• Selling a part of the business. This is called a share. A person that owns shares in a business is called a shareholder.

• Relatives and friends who want to invest in a business. This money can be a loan that must be repaid. The money can also be an investment that makes the relative a shareholder of the business.

• The government or other organizations that want to invest in the future of Rwanda. This money is paid as a grant. Most grants do not need to be repaid.A business owner who buys raw materials or products to sell can also ask for trade credits.

A trade credit means that the supplier lets you pay for the products later.

Uwera is an entrepreneur. She has used her savings to start a furniture business. Recently, Uwera received a large order from a hotel in Kigali. She needs money to buy leather and other raw materials.Uwera saves in a collective saving scheme with her five best friends. Her uncle thinks that Uwera is very talented and that her business will grow. Uwera can source the money by:

Uwera is an entrepreneur. She has used her savings to start a furniture business. Recently, Uwera received a large order from a hotel in Kigali. She needs money to buy leather and other raw materials.Uwera saves in a collective saving scheme with her five best friends. Her uncle thinks that Uwera is very talented and that her business will grow. Uwera can source the money by:• asking her uncle to invest in her business

• borrowing from her collective saving scheme • asking for a bank loan.Answer the questions on your own.

1. What is the difference between debt and equity?

2. Why does Uwera need money?

3. Write a list of the advantages and disadvantages of Uwera’s three options.

4. What do you think will happen to the order from the hotel if Uwera cannot buy the raw materials?

What is saving and how do we save?

Saving is putting aside money in a safe place like a bank account, on a regular basis, so that you have a store of money saved up. People save to buy something expensive in the future, like a bicycle or a car. People also save so they have money if there is an emergency. The best way to save money for something that you need or want is to set a savings goal.

Step 1

Write down what you want to save up for. Are you saving for an education, a personal computer (PC) or a bicycle? Cut out pictures of the item that you are saving for and make a poster. This helps you to continue to save when you are thinking of using your money for other things.

Step 2

Calculate how much money you can save every month. Then divide the cost of the item into the number of months and calculate how many months you need to save for. For example, let’s say that you are saving up for a computer that costs RWF 180,000 and you can save RWF 12,000 per month. It will take you (180,000 ÷ 12,000 = 15) fifteen months to save up for the computer.

Step 3

If you have a savings account in a bank, set up a standing order. You can also ask a parent or other family member to keep your savings for you.

Step 4:Look around for the best prices for the item that you want to buy.

Saving options

You can save money using:

• a savings account at a bank

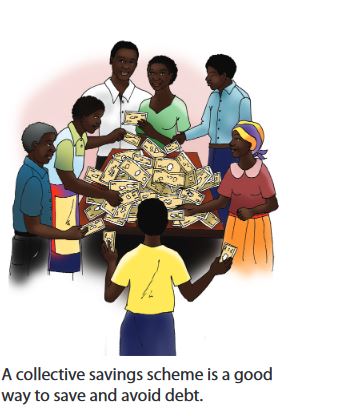

• a collective savings scheme.In a savings account, you will earn money by keeping your money in the bank.

This is called interest.When you save in a collective saving scheme, you will not earn interest.

Why is saving important

Sometimes we want to buy expensive things such as a bicycle or a computer. We usually do not have the money so we need to save up over a period of time.

As we do not know what the future holds, it is also important to save in case we are sick or lose our jobs. A person that owns a home will need to save in case the house needs repairs. A business person needs to save to invest in more machines or to grow the business.

1. What is your savings goal? Write down a plan for how you will save for the item that you would like to buy.

2. Ruti would like to buy a bicycle for RWF 100,000. He can save RWF 5,000 per month. How many months will it take for Ruti to save for the bicycle?

1. Investigate collective savings schemes in your community. Make a presentation to the class and explain how people use collective savings schemes to save in your community.

2. Visit a local bank. Ask how to open a savings account. Make a presentation to your class where you explain how to save money using a savings account.

Borrowing money

To borrow money means to receive money on a temporary basis from an individual or a business.When we borrow money we need to pay it back at a later stage. We also need to pay interest on the loan. Interest is money that the bank charges to lend you the money. We usually calculate interest as a percentage of a loan. If you borrow RWF 100,000 at an interest rate of 10%, then you need to pay back RWF 110,000.

Why do we need to borrow money?

A new business usually needs to buy machinery and raw materials before it can start. A business also often needs to borrow money when it is growing, for example, if it needs more machinery or a larger factory.

Mutoni Kaliza is a farmer that grows cassava. Her crops are selling well and she wants to plant more for the next season. Mutoni therefore needs money for seeds.

1. Mutoni has a savings account at I & M Bank and would like to ask this bank for a loan. Assist Ms. Kaliza by making a presentation to the bank manager where you explain why she needs to borrow money.

2. Duterimbere Microfinance Ltd agrees to lend Mutoni RWF 200,000 at an interest rate of 12%. I & M Bank lends money at an interest rate of 7%.

a) How much interest will Mutoni pay if she borrows from Duterimbere Microfinance Ltd?

b) How much interest will she pay if she borrows from I & M Bank?

c) Which institution do you think Mutoni should borrow the money from? Explain your answer.

Sources of business finance

In Rwanda, we have different types of financial institutions.

Commercial banks

A commercial bank is a bank that offers financial services to individuals and businesses. You can save money in a savings account and ask for a loan. Commercial banks in Rwanda include:

• Access Bank Rwanda

• Bank of Kigali

• I & M Bank

• BPR (Bank Populaire du Rwanda)

• Cogebanque

• Ecobank.

• GT Bank

Investment banks

An investment bank buys shares in a business and sells them to investors.The Development Bank of Rwanda (BRD) is an investment bank that buys shares from businesses mainly in agriculture and tourism.

Microfinance companies

A microfinance company offers smaller loans to individuals or businesses. The interest rates are cheaper than in a commercial bank.Microfinance companies include:

• Urwego Opportunity Bank

• Copedu

• Zigama Credit and Savings Bank.

1. List the differences between a commercial bank, an investment bank and a microfinance company.

2. Cyusa wants to sell his vegetables from a small stall in Kigali. Which institution do you think will offer him a loan to start his business?

3. Mutesa wants to open a tourist lodge in Volcanoes National Park. Where can she apply for money for this project?

4. Investigate the financial institutions in your community. List them under the headings Commercial Bank, Investment Bank and Microfinance Company.

Using banking services

If you want to use the services from a bank, you need to follow certain rules. These are called terms and conditions.Let’s say that you want to open a savings account where you will save money for your university education. The terms and conditions can be:

• minimum opening deposit of RWF 50,000

• equal monthly deposits

• interest is payable monthly

• one free withdrawal every six months.

If you want to open a current account, the bank can ask you to provide:

• a completed application form

• photocopy of your ID card

• two photographs

• letter from your employer to confirm employment and address.

Collateral for a loan

When you borrow money, the bank needs to make sure that you will pay it back. The bank therefore often asks for collateral.Collateral is something that has value for the bank. This can be a house or savings. If you do not repay the loan, the bank can take the collateral instead.

1. Visit a local commercial bank. Ask for forms to open a:

a) current account

b)savings account

c) business loan

d) personal loan.

2. Read through the terms and conditions. Explain, using your own words, what the terms and conditions for using each bank service mean.

Managing debt

When you borrow money, it is very important to manage the repayments. Many businesses fail because they cannot pay back the money that they borrow. Individuals who cannot pay back loans can lose their homes and the chance for their children to have an education. To manage debt, follow the guidelines below:

• Don’t spend money on things that you do not need. You can save money by only buying the things that are necessary.

• Don’t borrow more money. Plan ahead and save for the things that you need.

• Don’t buy anything expensive while still in debt. First pay back the money that you owe, and then plan to buy new things.

Ways of saving

There are many different ways to save. Some people save together in a joint account. These are called collective savings schemes or investment funds. You can also open a savings account at a bank where you can save up for a home or payment for an education.When you save, you plan for future expenses. You also avoid paying interest on loans.

Last month, your friend Munyana bought new shoes and this month she is looking at a new dress. She still owes her parents money for the shoes but says that the shop is willing to sell her the dress on a loan with interest. Role play a visit to Munyana where you:

1. Explain why it is important to manage debt.

2. Show why Munyana will pay more money for the dress if she buys it now than she will if she saves the money first.

3. Suggest how Munyana can buy both the shoes and the dress by planning her savings.

Managing money

It is important to manage money, both for an individual and for a business.

How to reduce expenses

You can reduce costs by only buying things that you need. When you buy items such as clothes or shoes that will last a long time, you do not have to replace them often. For example, one good suit is better than three poorly made suits. You can also reduce expenses by:

• Using public transport such as buses instead of driving in a car

• Repaying debt as soon as possible to avoid having to pay a lot of interest

• Saving on electricity by always turning off the light when you leave a room and by turning off the water heater during the day.

• Making use of inexpensive entertainment such as the library or public parks

• Cooking at home rather than eating at a restaurant

• Growing your own fruit and vegetables and raising chickens for meat and eggs. Can you think of other ways to reduce expenses?

Reuse items that are still in good condition

Take good care of machines, cars and expensive items so that you can use them for a long time.

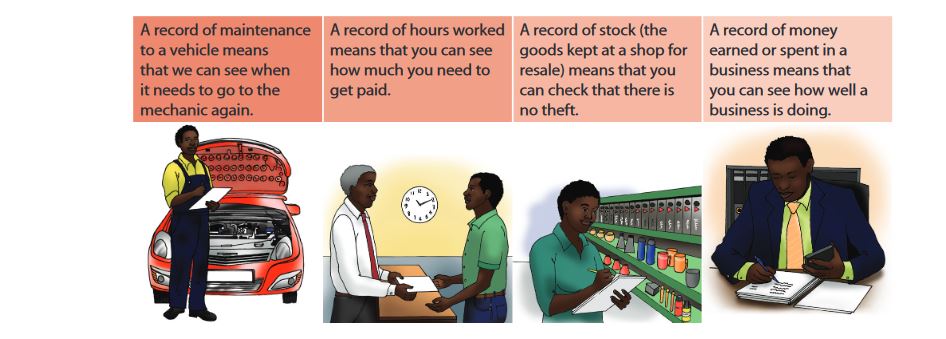

Proper record keeping

A successful business keeps information about many things. We say that the business keeps records.Here are some examples:

Record keeping is important for a business. In groups, draw up a list of records that are important for the following businesses:

1. a mechanic

2. a supermarket

3.a hairdresser

4. a taxi service.

Case study activity

Read the case study ‘Physical and financial health’ and then do the activity in question 1.

Physical and financial health

Meet Ngoga. He is a long-distance runner. Every morning he wakes up early and eats a healthy breakfast. Then he trains for many hours. He drinks plenty of water and goes to bed early to make sure that he gets enough rest. Ngoga is physically fit and healthy.A business can be healthy too, just in a different way.

A business can be financially healthy. By carefully planning how to make and spend money, you can make sure that your business becomes successful, just like a sportsman can make sure that he will do well in a race by making the right decisions about his health.

This sportsman is physically fit

.Question1.

Prepare a presentation where you compare financial health to physical health. You can use the example of Ngoga or any other sportsperson that you know.

Separating personal from business financeAs a business owner it is important to separate personal money from the money in your business. There are many reasons for this, for example:• to pay taxes to Rwanda Revenue Authority (RRA). Individuals and businesses follow different tax rules so you need to keep a separate record.• to see how well your business is doing. If you spend business money as personal money, it is difficult to see how well your business is doing.

Kirezi owns Kirezi Hairdressing. While she does braiding, she offers her clients coffee or tea. Kirezi says that she also drinks the coffee at home. She also uses her cell phone for private calls and takes home shampoo and other hair products. Kirezi says that it does not matter if she uses business items for personal use as she is the business owner.Discuss these questions in class.1. List three items that are used for both personal and business purposes in Kirezi Hairdressing.2. Explain to Kirezi why it is important to separate personal and business finances.3. Make a suggestion to Kirezi about how she can separate personal and business finances.4. Lately, Kirezi Hairdressing only shows a small profit even though Kirezi does the same amount of braiding. Explain how using business items for personal use makes it look like the business is not doing well.

Kirezi owns Kirezi Hairdressing. While she does braiding, she offers her clients coffee or tea. Kirezi says that she also drinks the coffee at home. She also uses her cell phone for private calls and takes home shampoo and other hair products. Kirezi says that it does not matter if she uses business items for personal use as she is the business owner.Discuss these questions in class.1. List three items that are used for both personal and business purposes in Kirezi Hairdressing.2. Explain to Kirezi why it is important to separate personal and business finances.3. Make a suggestion to Kirezi about how she can separate personal and business finances.4. Lately, Kirezi Hairdressing only shows a small profit even though Kirezi does the same amount of braiding. Explain how using business items for personal use makes it look like the business is not doing well.

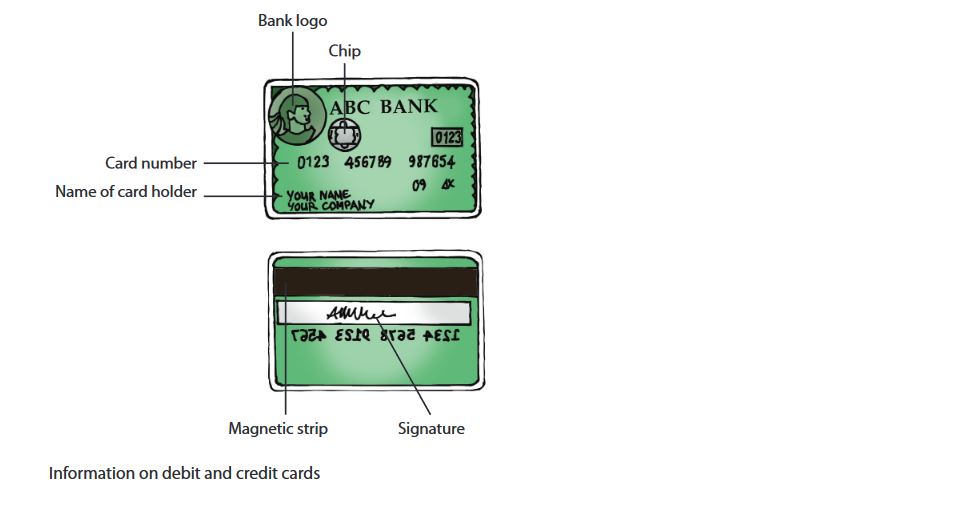

Debit and credit cards

Today, many people prefer to use cards instead of cash.It is easy to steal cash.

A card has a secret code, called a PIN(Personal Identification Number). You can only use the card if you know the PIN. It is therefore safer to use a card than cash.

Debit cards

A debit card is also called a bank card. It is a small plastic card that can be used to draw money out of your account. The card has a chip or a magnetic strip where the bank account information is stored. Some debit cards show the name of the card holder and the card number; others are blank cards that only have this information in the magnetic strip.

Credit cards

A credit card looks similar to a debit card. A debit card uses money that you already have in an account. When you pay with a credit card you are borrowing credit from the bank. This means that the bank has agreed to a certain amount that you can use, but you must pay it back. If you do not pay back all the money back at the end of the month, the bank charges interest on the money owed.

We use debit and credit cards in the same way. Shops have point of sale machines where you can either swipe the card or insert the card so that the machine can read the chip.You can also use a card to draw cash from an ATM (Automated Teller Machine).To use a card, you need to have a PIN number. This is a secret number that only you must know. If another person knows your PIN number, they can use your card to draw cash or buy goods. You must therefore always take care that no one sees your number when you use your card.To use a debit and credit card properly:

• Always keep the card clean and ensure that the magnetic strip is not scratched.

• Be careful when drawing money at an ATM. Do not tell your PIN code to anyone.

• Keep a record of the money in your account. You can only draw the money in your account from a debit card. When using a credit card, ensure that you do not spend money that you cannot pay at the end of the month.

When you use a debit card, you can only spend the money that is in your account. A credit card has a line of credit that you can spend. You need to keep the slips of every payment so that you can calculate how much money you have left or how much credit you still have.

Copy the tables and list the advantages and disadvantages of using a credit card and a debit card. See the example below.